Saudi Arabia Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

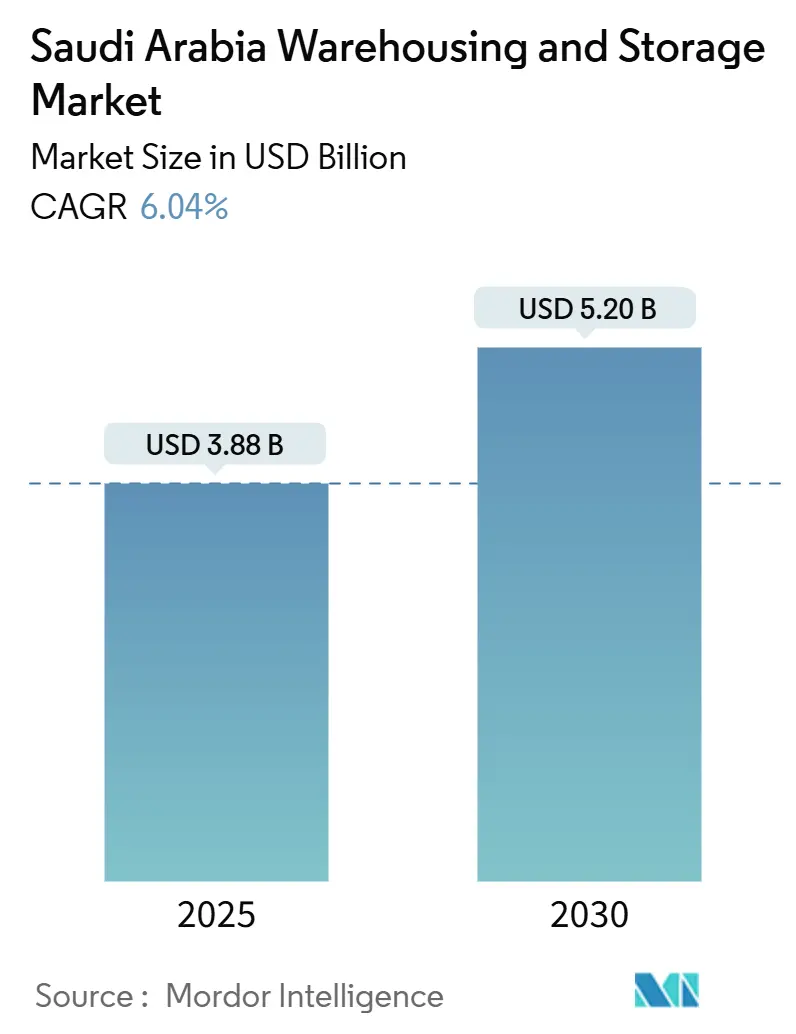

| Market Size (2025) | USD 3.88 Billion |

| Market Size (2030) | USD 5.20 Billion |

| Growth Rate (2025 - 2030) | 6.04% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Warehousing And Storage Market Analysis by Mordor Intelligence

The Saudi Arabia Warehousing And Storage Market size is estimated at USD 3.88 billion in 2025, and is expected to reach USD 5.20 billion by 2030, at a CAGR of 6.04% during the forecast period (2025-2030).

The expansion is anchored in Vision 2030 logistics reforms, government funding for 18 purpose-built logistics zones, and double-digit growth in mobile-enabled commerce transactions. General warehousing dominates capacity because most domestic manufacturers and retailers still rely on ambient facilities, yet refrigerated capacity is scaling faster as food security and pharmaceutical traceability rules tighten. Foreign-ownership liberalization is drawing global operators that inject automation, robotics, and higher safety standards, prompting local incumbents to upgrade facilities or form partnerships with technology suppliers. The market’s strategic geography—midway between Asia, Europe, and Africa—continues to create multimodal opportunities as port, road, and rail infrastructure converges around the forthcoming 1,390 km Landbridge railway.

Key Report Takeaways

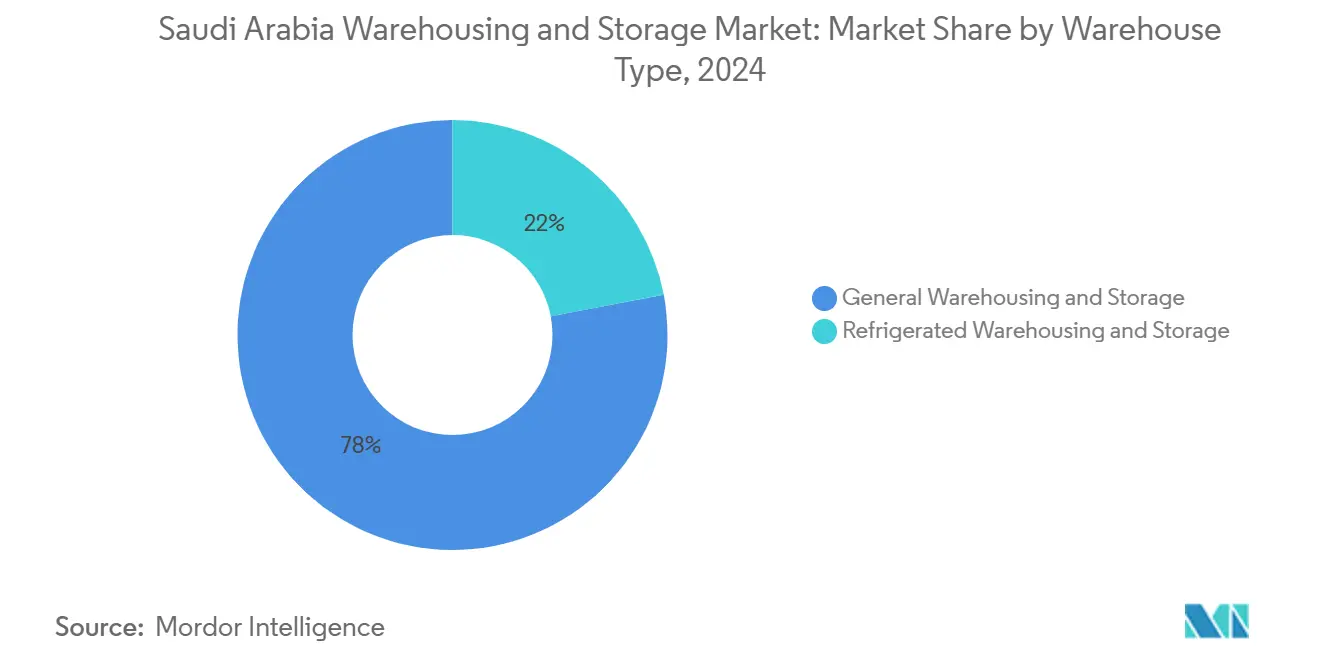

- By warehouse type, general warehousing and storage led with 78.01% of the Saudi Arabia warehousing and storage market share in 2024; refrigerated warehousing is projected to post the fastest 6.32% CAGR through 2030.

- By end user industry, the e-commerce and retail segment accounted for 32.10% share of the Saudi Arabia warehousing and storage market size in 2024 and is advancing at a 6.17% CAGR through 2030.

Saudi Arabia Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vision-2030-driven e-commerce boom | +1.5% | National, with concentration in Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Government investment in logistics zones | +1.2% | National, with early gains in Eastern Province, Makkah, Riyadh | Long term (≥ 4 years) |

| Rising cold-chain demand (food & pharma) | +0.8% | National, with pharmaceutical focus in Riyadh, food in Eastern Province | Medium term (2-4 years) |

| Expansion of organised FMCG/retail networks | +0.7% | National, with urban concentration in major metropolitan areas | Short term (≤ 2 years) |

| Saudi Landbridge rail integration | +0.6% | Eastern and Western regions, connecting Red Sea to Arabian Gulf | Long term (≥ 4 years) |

| 100% foreign-ownership liberalisation | +0.5% | National, with initial focus on major economic centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Vision-2030-Driven E-Commerce Boom

Saudi shoppers under age 35 embrace mobile checkout, pushing online sales far ahead of traditional retail. Retailers now place inventory in fulfillment centers within 30 km of dense population clusters, which shifts warehouse location models toward micro-hubs and increases demand for bonded facilities that can pre-clear imports. Digital Economy Strategy targets to increase tech-enabled activities by 2030, so operators are scaling automated sortation and omnichannel inventory systems to handle the surge. Customs authorities accommodate cross-border flows by expanding smart-gate clearance, which compresses delivery lead times and elevates service-level benchmarks. The overall effect is structural—not cyclical—demand for modern space in the Saudi Arabia warehousing and storage market[1]Ministry of Commerce, “E-Commerce Transaction Growth 2024,” mc.gov.sa.

Government Investment in Logistics Zones

The Industrial Development Fund has earmarked SAR 10 billion (USD 2.67 billion) for 18 advanced logistics zones that embed 5G, IoT, and streamlined customs desks. First-phase sites opening before 2026 already post cargo-clearance times of four hours, one-third the waiting period in legacy yards. Eastern Province plots sit adjacent to petrochemical complexes, while Riyadh parks use intermodal rail sidings to cut long-haul road mileage. Operators working inside these fenced zones enjoy reduced bureaucracy and discounted utility tariffs, improving project IRRs and pulling the Saudi Arabia warehousing and storage market toward globally competitive cost structures[2]MODON, “Logistics Zones Development Initiative 2024,” modon.gov.sa.

Rising Cold-Chain Demand (Food & Pharma)

The National Unified Procurement Company mandates temperature-controlled handling across all healthcare imports, instantly elevating pharma cold-store demand. Meanwhile, the Ministry of Environment, Water, and Agriculture pursues food-security stockpiles to buffer seasonal import shocks, raising the need for multi-temperature storage in coastal ports and inland DCs. Private dairy processors, meat suppliers, and vaccine distributors financed capacity expansions during 2024, supported by favorable land leases inside newly built zones. The Saudi Food and Drug Authority now inspects temperature logs in real time, adding compliance costs yet improving service premiums for certified operators. These factors anchor long-run growth in the chilled and frozen subset of the Saudi Arabia warehousing and storage market[3]NUPCO, “Cold Chain Mandate for Healthcare Supply Chains,” nupco.com.

Expansion of Organized FMCG/Retail Networks

Grocery hypermarkets, discount chains, and fashion franchises are scaling brick-and-mortar outlets while placing e-commerce inventory in shared facilities to cut dead-stock risk. Consolidated distribution models replace traditional wholesaler drop-offs, so retailers demand integrated warehousing, kitting, and light assembly services. Updated food-safety protocols require end-to-end traceability, which nudges smaller ambient sheds to upgrade IT or exit. Organized retail real estate climbed in tandem, providing a steady pull for high-footprint DCs in Jeddah and Riyadh. Consequently, downstream tenant mix diversifies beyond petrochemicals toward consumer-centric occupiers in the Saudi Arabia warehousing and storage market[4]Saudi Central Bank, “Digital Payment Systems 2024,” sama.gov.sa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High land & construction costs | -0.4% | National, with acute pressure in Riyadh, Jeddah metropolitan areas | Short term (≤ 2 years) |

| Skilled labour shortage in automation | -0.3% | National, with particular challenges in Eastern Province industrial zones | Medium term (2-4 years) |

| Patchy last-mile connectivity beyond major hubs | -0.2% | Secondary cities and rural areas outside main metropolitan centers | Medium term (2-4 years) |

| Elevated utility tariffs for cold stores | -0.1% | National, with higher impact on energy-intensive refrigerated facilities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Land & Construction Costs

Steel and concrete prices escalated in 2024 as megaprojects soaked up bulk supplies. Elevated interest rates added 150 bps to loan charges compared to the previous year, compressing developer margins and trimming speculative builds. Modular construction helps lower capex per pallet but extends procurement lead times, which threatens project timelines for operators racing to secure first-mover advantage. The cost burden is most acute for smaller firms, tilting the Saudi Arabia warehousing and storage market toward capital-rich players.

Skilled Labor Shortage in Automation

Automated shuttle systems, sortation arms, and high-bay AS/RS installations outpaced local technician training pipelines, leaving firms to hire expatriate engineers at premium salaries. The Human Resources Development Fund introduced targeted programs in 2024, yet demand is still projected to triple by 2027, widening the gap. Certification requirements imposed by the Saudi Standards, Metrology, and Quality Organization delay project commissioning for up to six months when approved manpower is scarce. Labor scarcity, therefore, caps the speed at which facilities can shift from manual to automated flows in the Saudi Arabia warehousing and storage market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Cold Storage Drives Future Growth

Refrigerated facilities will expand at a 6.32% CAGR through 2030—faster than the overall Saudi Arabia warehousing and storage market—on sustained pharmaceutical and perishables demand. In contrast, general warehousing retains 78.01% of current capacity, riding e-commerce fulfillment and industrial spare-parts flows. General operators now retrofit air-conditioned chambers to secure pharma overflow contracts, blurring lines between ambient and cold storage. Stringent SFDA temperature-log mandates steer high-value goods away from non-certified sheds, accelerating share gains for purpose-built cold chain players. Over the horizon, the Landbridge rail will shorten sea-to-Gulf transits, raising throughput and bolstering the refrigerated subset of the Saudi Arabia warehousing and storage market size.

Regulatory compliance differentiates returns. Pharma reserves require 90-day inventory buffers, guaranteeing steady occupancy. Agri exporters of dates leverage new pre-coolers to safeguard quality during long-haul journeys to Asia and North America. As margins compress in ambient space—where clients demand kitting, VAS, and just-in-time staging—operators diversify into temperature-controlled niches that command premium rents. This transition reinforces multi-product site designs, forming a core strategy for incumbents intent on keeping wallet share in the Saudi Arabia warehousing and storage market.

By End User Industry: E-commerce Reshapes Demand Patterns

E-commerce and retail led with 32.10% revenue in 2024 and will grow 6.17% annually through 2030, propelled by omnichannel strategies and faster click-to-door expectations. Major platforms lease cross-docked hubs near population centers to guarantee next-day delivery, expanding pallet demand at twice the clip of legacy wholesale channels. Food & beverage networks rely on chilled nodes to uphold the shelf-life of dairy and poultry lines, yet growth moderates after rapid pandemic-era expansion. Manufacturing and automotive clients such as SABIC and Ma’aden adopt regional distribution to trim stock-carrying costs, reinforcing the importance of secure, compliant storage.

The Saudi Arabia warehousing and storage market size for chemical and hazardous materials expands as Tristar’s Dammam Class 3/8 facility illustrates a stringent compliance’s competitive moat. Finally, niche segments—defense spares, renewable-energy equipment—add volume diversity that smooths occupancy cycles for large campuses. Supply chains pivot toward shared, multi-tenant formats where 3PLs manage inventory peaks across verticals. This pooling model enhances space utilization and dilutes fixed costs, thus shaping the future competitive balance of the Saudi Arabia warehousing and storage market.

Geography Analysis

Riyadh, the Eastern Province, and the Jeddah–Makkah corridor form the primary logistics triangle. The Eastern Province captures a significant share of the existing footprint thanks to port adjacency and petrochemical value-chain clustering. Jeddah leverages Red Sea connectivity and religious tourism cargo to sustain high warehouse rents. The in-built Saudi Landbridge will compress Red-Sea-to-Gulf transit to under 48 hours, redirecting some maritime flows inland and amplifying intermodal hubs in both Dammam and Jeddah.

Secondary cities such as Tabuk and Abha now attract logistics parks tied to agriculture and mining, nudging capacity outward and aligning with Vision 2030 balanced-growth aims. Northern Border Province positions Arar as a gateway for Jordan and Iraq trade, with a 2026 logistics center to streamline overland trucking. Regulatory disparities—special tax regimes in NEOM, customs-light zones in King Abdullah Economic City—pull global 3PLs to set up regional HQs, reinforcing Saudi Arabia’s aspiration as a transshipment middle ground.

While 75% of future capacity will crowd into six national clusters, geographic diversification remains a hedge against land price inflation and infrastructure shifts. Operators that plant multi-node networks will be better positioned to flex around evolving trade lanes and policy adjustments, underpinning long-term competitiveness in the Saudi Arabia warehousing and storage market.

Competitive Landscape

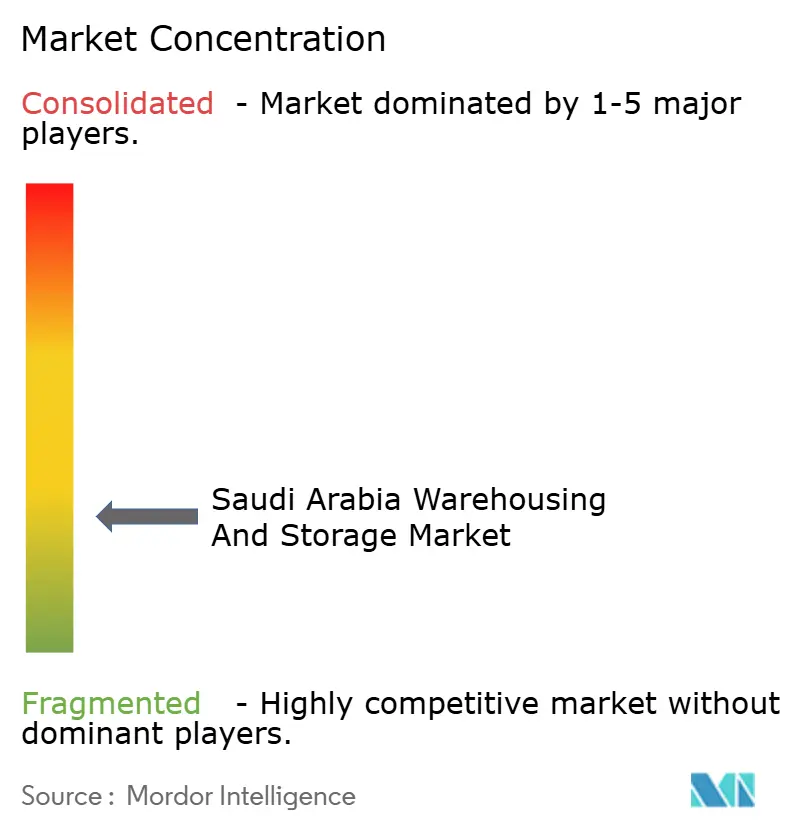

The Saudi Arabia warehousing and storage market balances local incumbents and global entrants. SAL Saudi Logistics Services and Almajdouie leverage historic client ties and regulatory fluency, while DHL, GEODIS, and Aramex advance automation and standardized SOPs. Market share remains fragmented, yet consolidation accelerates as capital-heavy firms acquire smaller sheds to build nationwide grids. The top-tier races to deploy AS/RS systems, robotic picking, and AI-driven WMS to lift pallet-turn velocity and reduce error rates.

White-space opportunities center on pharma, automotive spares, and hazardous chemicals, each demanding certifications that create high entry barriers. Technology is the new moat, where operators integrating IoT sensors, digital twin yard maps, and ESG-ready solar installations secure multinational clients that prize data transparency.

Saudi Standards updates push compliance spends upward, squeezing margins for manual operators and hastening sell-off to better-capitalized rivals. International joint ventures—such as Almajdouie–Maersk cold-chain tie-ups—illustrate hybrid models blending global know-how with local market access.

Saudi Arabia Warehousing And Storage Industry Leaders

SAL Saudi Logistics Services Co.

Almajdouie Logistics

DHL Group

Aramex

Al-Futtaim Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SAL Logistics opened a 45,000 m² distribution center in southern Riyadh’s Logistics Park to serve pharma, FMCG, and e-commerce tenants.

- June 2025: DHL earmarked EUR 500 million (USD 520.8 million) for GCC expansion, allocating a large share to new Saudi Arabia contract-logistics warehouses.

- April 2025: MAWANI and Sultan Logistics agreed to build a SAR 200 million (USD 53.2 million) logistics park at King Abdulaziz Port, adding 35,000 m² of warehouse space.

- January 2025: Aramex activated an automated robotic sortation system at Jeddah Islamic Port, processing up to 96,000 parcels daily.

Saudi Arabia Warehousing And Storage Market Report Scope

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

| E-commerce & Retail |

| Food & Beverage |

| Manufacturing and Automotive |

| Healthcare, Pharmaceuticals, and Life Sciences |

| Chemicals & Specialty Materials |

| Others |

| By Warehouse Type | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By End User Industry | E-commerce & Retail |

| Food & Beverage | |

| Manufacturing and Automotive | |

| Healthcare, Pharmaceuticals, and Life Sciences | |

| Chemicals & Specialty Materials | |

| Others |

Key Questions Answered in the Report

How large is the Saudi Arabia warehousing and storage market in 2025?

It is valued at USD 3.88 billion, with a 6.04% CAGR projected through 2030.

Which warehouse type grows the fastest?

Refrigerated facilities, expanding at 6.32% CAGR due to pharma and food regulations.

What drives foreign investment into Saudi warehouses?

100% ownership liberalization, specialized logistics zones with tax perks, and Vision 2030 export ambitions.

Which region logs the highest near-term capacity growth?

Riyadh, projected at 7.1% CAGR on rising fulfillment center demand.

What challenges constrain warehouse construction?

Elevated land and building costs plus a shortage of automation-skilled technicians keep new-build timelines tight.

Page last updated on: