Saudi Arabia E-commerce Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

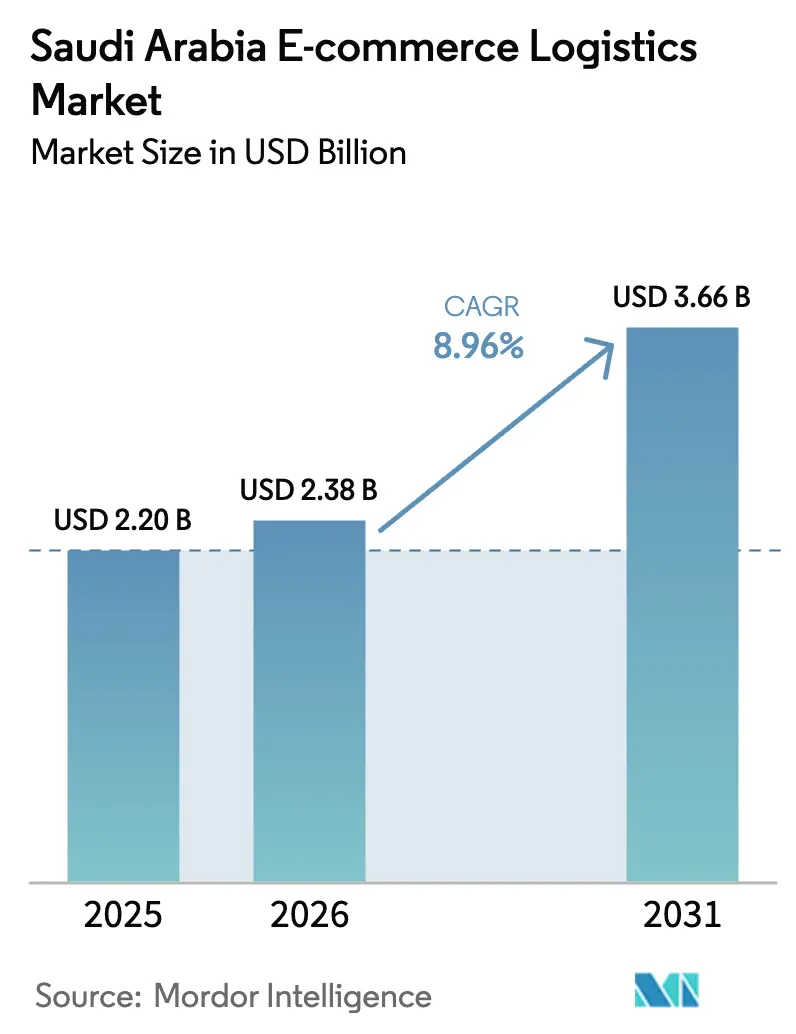

| Base Year Market Size (2025) | USD 2.20 Billion |

| Market Size (2026) | USD 2.38 Billion |

| Market Size (2031) | USD 3.66 Billion |

| Growth Rate (2026 - 2031) | 8.96% CAGR |

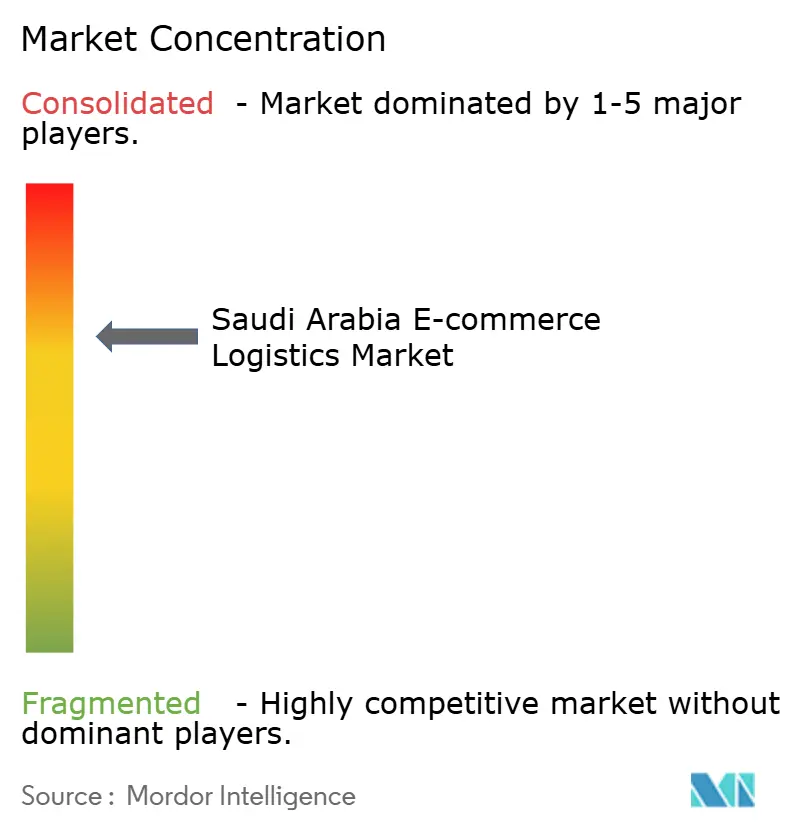

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia E-commerce Logistics Market Analysis by Mordor Intelligence

The Saudi Arabia E-commerce Logistics Market size is expected to grow from USD 2.20 billion in 2025 to USD 2.38 billion in 2026 and is forecast to reach USD 3.66 billion by 2031 at 8.96% CAGR over 2026-2031.

Momentum is propelled by Vision 2030 reforms, SAR 280 billion (USD 74.6 billion) of logistics infrastructure commitments, and the National Transport and Logistics Strategy that positions the Kingdom as a tri-continental trade bridge. Rising digital payments-79% of all transactions in 2024 continue to convert cash-on-delivery users, while a mandatory national address system effective January 2026 removes a key last-mile bottleneck. Cross-border capacities are rebounding after the Red Sea crisis, helped by nonstop Riyadh freighter links and simplified customs on the Fasah platform. Quick-commerce dark stores, AI-enabled routing, and value-added services such as kitting are widening operating margins even as core transport rates soften. Labor localization, reverse-logistics costs, and limited cold-chain capacity temper the growth outlook but have not derailed investor appetite.

Key Report Takeaways

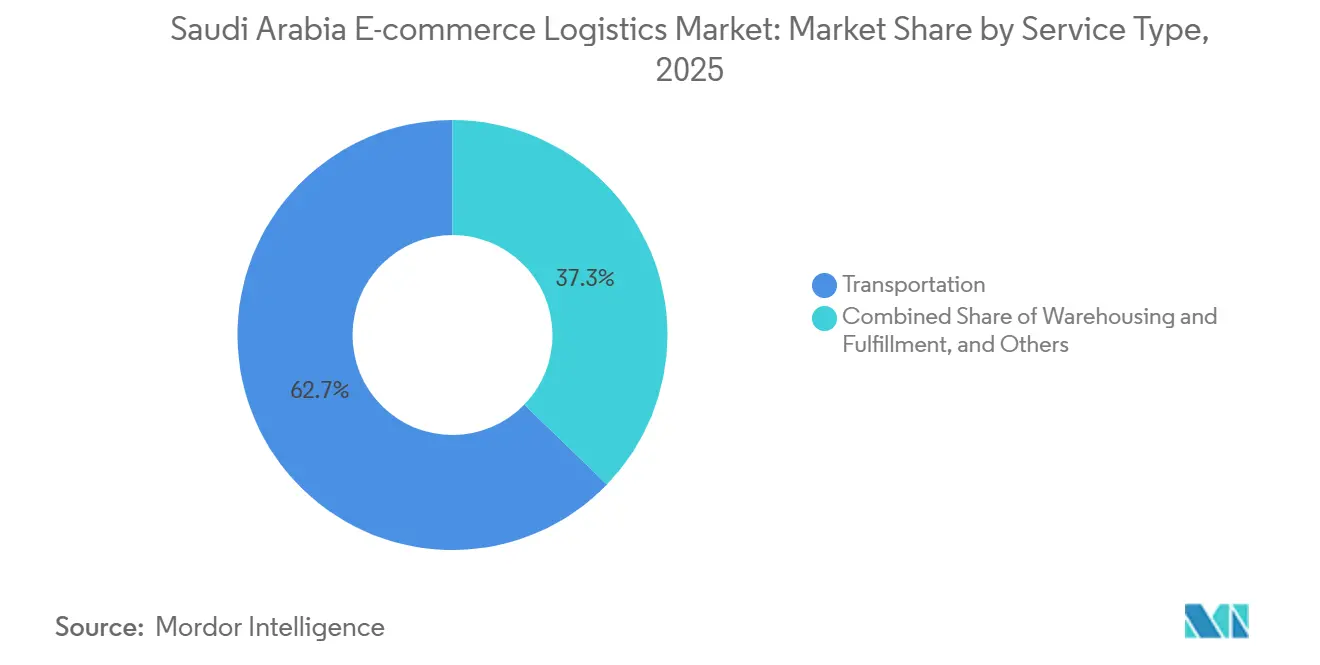

- By service, transportation led with 62.75% of Saudi Arabia e-commerce logistics market share in 2025, while value-added services are projected to expand at a 10.80% CAGR between 2026-2031.

- By business model, B2C dominated with 72.21% revenue share in 2025, whereas B2B is forecast to rise at 12.30% CAGR between 2026-2031.

- By destination, domestic flows accounted for 81.14% of the Saudi Arabia e-commerce logistics market size in 2025, and cross-border shipments are expected to climb at a 13.90% CAGR between 2026-2031.

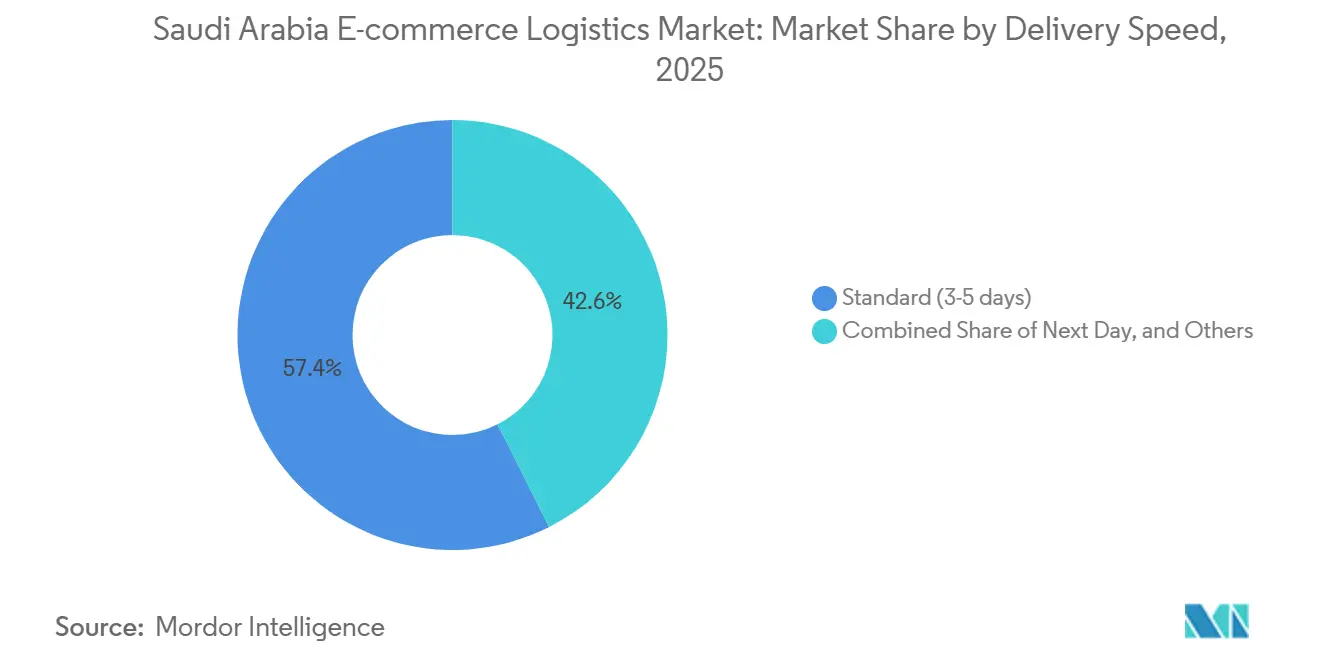

- By delivery speed, standard 3-to-5-day services held a 57.43% share in 2025; same-day fulfillment is advancing at a 19.70% CAGR between 2026-2031.

- By product category, fashion and lifestyle captured 28.15% share in 2025, while beauty and personal care are on track for the fastest 14.40% CAGR between 2026-2031.

- By geography, Riyadh Province controlled a 46.37% share in 2025; Eastern Province registered the quickest 11.20% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia E-commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging internet and smartphone penetration | +1.8% | National; early gains in Riyadh, Makkah, Eastern | Short term (≤ 2 years) |

| Cashless payment adoption accelerating online retail | +2.1% | Urban centers | Short term (≤ 2 years) |

| Government Vision 2030 logistics reforms | +2.3% | National priority cities | Long term (≥ 4 years) |

| Rise of social-commerce driven micro-fulfillment | +1.2% | Riyadh, Jeddah expanding | Medium term (2-4 years) |

| Dark-store and quick-commerce expansion | +1.4% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| AI-enabled route optimization reducing costs | +0.9% | National pilots | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Internet and Smartphone Penetration

Mobile penetration exceeded 120% in 2024, with smartphones ubiquitous among the under-35 cohort that forms over 60% of the population. Fiber rollout reached 95% of urban households by 2025, removing latency and boosting impulse purchasing. Each extra percentage point of smartphone penetration corresponded with a 1.5-point lift in order volumes, prompting a 90-day-to-30-day courier-licensing reform that enabled fast entry of new last-mile players. Rural connectivity still lags, but universal broadband targets extend nationwide reach by 2028, widening the Saudi Arabia e-commerce logistics market[1]“Broadband Coverage Report 2025,” Communications, Space & Technology Commission, CST.GOV.SA .

Cashless Payment Adoption Accelerating Online Retail

Mada e-commerce transactions climbed to SAR 197.42 billion (USD 52.6 billion) in 2024, up 25.82% year-on-year, while cash-on-delivery fell to 21%. Digital wallets such as Tamara and Tabby captured 18% of online checkouts by mid-2025, boosting high-ticket categories that need white-glove delivery. Secure payment circulars required chain-of-custody protocols, which logistics firms repurposed for valuables. International card acceptance hit 92% of Saudi sites, accelerating import flows and reinforcing the Saudi Arabia e-commerce logistics market[2]“Payment Systems Report 2024,” Saudi Central Bank, SAMA.GOV.SA.

Government Vision 2030 Logistics Reforms

The National Transport and Logistics Strategy earmarks SAR 280 billion (USD 74.6 billion) to rank the Kingdom among the world’s top 10 logistics hubs. Preferential SIDF loans helped Agility add 100,000 m² of EDGE-certified warehousing in Riyadh by Q1-2025. Fasah automation cut import clearance times to under 24 hours for 87% of consignments, down from 48 hours in 2022. A mandatory national address system from January 2026 trims failed first attempts by more than one-third, strengthening the Saudi Arabia e-commerce logistics market.

Rise of Social-Commerce Driven Micro-Fulfillment

Social commerce held 12% of e-commerce GMV in 2025, fueled by influencer live-stream sales. Monsha’at’s Mahali platform onboarded 1,200 SMEs in Q1-2025, many shipping only 10-50 parcels daily. Third-party hubs such as ISNAAD aggregate this long-tail inventory, offering modular pricing and integrated returns. Large carriers launched pay-per-shipment solutions to capture this micro-market, adding density and diversifying revenue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Last-mile addressing and geolocation gaps | -1.3% | Rural & unplanned zones | Short term (≤ 2 years) |

| Labor shortages amid Saudization targets | -1.1% | Nationwide warehouses & fleets | Medium term (2-4 years) |

| High reverse-logistics cost for fashion and electronics | -0.8% | Riyadh, Jeddah, Dammam | Medium term (2-4 years) |

| Limited cold-chain capacity for e-grocery | -0.6% | Outside top three cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Last-Mile Addressing and Geolocation Gaps

Even with the national address mandate, only 68% of online shoppers input compliant data, forcing couriers to phone-verify locations and adding 5-10 minutes per stop. Landmark navigation inflates rural delivery costs by up to 12%. Proprietary geocoding systems lowered failure rates by 6–8 points but require continual updates. Summer heat regulations that halt outdoor work from 12:00-15:00 compress windows, worsening congestion and delaying same-day promises[3]“Outdoor Work Ban Circular,” Ministry of Human Resources and Social Development, HRSD.GOV.SA .

Labor Shortages amid Saudization Targets

Freight forwarding roles were localized in May 2024, yet warehouse picking and driving remain unattractive to many Saudis. Female participation rose to 36.3% in Q1-2025, but is concentrated in office and inventory control functions. Outdoor work bans during peak summer shave 18-20% off daily productive hours, pushing operators to hire extra shifts. High-capital automation like AutoStore robots can cut manual picking up to 50%, though costs limit uptake to top-tier facilities[4]“Temperature-Controlled Transport Standards,” Saudi Food and Drug Authority, SFDA.GOV.SA.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Value-Added Gains as Differentiation Tool

Transportation delivered 62.75% of Saudi Arabia e-commerce logistics market share in 2025, fuelled by a 50,000-km highway grid and rising air-cargo frequencies. FedEx introduced six weekly Boeing 777 freighters to Riyadh in September 2025, accelerating cross-border parcel flows. Warehousing clusters totaled 72 million m² nationwide, yet aging stock outside Riyadh, Jeddah, and Dammam requires upgrades. Value-added services will outpace other lines at a 10.80% CAGR (2026-2031) because Arabic labeling mandates and promotional bundling raise demand for kitting, packaging, and personalization.

Maersk’s EDGE-Advanced Jeddah park integrates 19,000 m² fulfillment with 32,000 m² cold storage and solar arrays, letting shippers cite carbon-neutral distribution. DHL’s Fulfillment Network runs seven Saudi warehouses with custom packaging that secures 15-25% margins, far above the 5-8% transport margin norm. The Saudi Arabia e-commerce logistics market, therefore, sees operators pivot to high-margin ancillary services as freight rates soften.

By Business Model: B2B Digitization Outpaces Consumer Growth

B2C retained 72.21% of the Saudi Arabia e-commerce logistics market in 2025, yet B2B channels are projected for a 12.30% CAGR between 2026-2031 on the back of industrial marketplaces and digitized procurement. The CEVA-Almajdouie venture unites 1.2 million m² of warehousing and 2,000 vehicles to serve automotive, construction, and chemicals verticals. ASMO, launched by DHL and Aramco in February 2024, offers vendor-managed inventory that cuts industrial lead times by 30-40%.

Academic work on 513 MSMEs found that e-commerce adoption yielded significant financial gains by improving transparency and delivery reliability, reinforcing B2B logistics momentum. Converging fulfillment, where a single facility serves both corporate buyers and households, blurs the traditional divide, further enlarging the Saudi Arabia e-commerce logistics industry.

By Destination: Cross-Border Flows Rebound Post-Crisis

Domestic shipments represented 81.14% of market revenue in 2025, yet cross-border volumes are set for a 13.90% CAGR (2026-2031) as Red Sea disruptions ease. Fasah automation trims clearance to sub-24 hours for 87% of parcels. Mawani recorded 27.63 million t of cargo in May 2024, up 8.09% year-on-year, showing recovery. Land bridges and planned rail corridors, such as the India-Middle East-Europe Corridor, could slash Asia-Europe transit by 40%, positioning the Kingdom as a terrestrial pivot.

Investment follows: the SAL-Sela SAR 4 billion (USD 1.06 billion) Falcon City zone near Riyadh airport opens by H1-2026 with bonded warehousing and multimodal links. DSV-NEOM’s USD 10 billion joint venture eyes 20,000 logistics jobs in Tabuk Province, cementing future gateway status.

By Delivery Speed: Same-Day Premium Widens

Standard delivery held a 57.43% revenue share in 2025, but same-day services are forecast to climb 19.70% CAGR between 2026-2031. Consumers pay SAR 15–25 (USD 4-6.67) premiums for 15- to 30-minute windows, making density vital. Jahez’s robot program for gated communities cuts labor costs by roughly 45% and will scale beyond Riyadh pending regulation. National address adoption curbs failed first attempts from 12-15% to near-7%, further improving same-day profitability.

Heat-related work curfews create two peak runs, morning and evening, which dark stores circumvent by staging inventory within 2 km of demand clusters. Economy services remain essential for rural corridors below 50 inhabitants per km², keeping overall Saudi Arabia e-commerce logistics market coverage balanced.

By Product Category: Beauty and Personal Care Scales Fastest

Fashion and lifestyle led with 28.15% of revenue share in 2025, but high returns continue to erode retailer margins. Beauty and personal care will post a 14.40% CAGR (2026-2031), supported by a female labor force that reached 36.3% participation in Q1-2025. These items generate lower return ratios and higher average order values, justifying cold-chain investments like Maersk’s Jeddah facility. Electronics logistics focuses on secure handling, while furniture orders drive demand for white-glove crews.

Integrated parks with ambient, chilled, and secure zones enable operators to serve mixed inventories efficiently. Absence of detailed SFDA e-grocery guidelines slows fresh-food expansion, but growing beauty, electronics, and lifestyle segments sustain market depth.

Geography Analysis

Riyadh Province anchored 46.37% of the Saudi Arabia e-commerce logistics market in 2025, benefiting from 24.5 million m² of warehousing and the upcoming King Salman International Airport cargo hub. Agility’s EDGE-certified expansion added 100,000 m² by Q1-2025, while the SAL-Sela Falcon City zone delivers 1.5 million m² of modular space by 2026.

Eastern Province is the fastest-growing pocket, forecast at 11.20% CAGR (2026-2031). The CEVA-Almajdouie platform consolidates 1.2 million m² of facilities to service cross-border trucking through King Fahd Port. Maersk’s 13,300 m² cold store and SMSA’s bonded hub near Dammam airport elevate import efficiency. Mawani-ARASCO’s grain-centric 40,000 m² center reveals potential for diversified e-commerce capacity once current contracts mature.

Makkah Province leans on Jeddah’s Red Sea port, where Maersk’s 225,000 m² logistics park opened in August 2024, integrating e-commerce zones with 32,000 m² of cold storage powered by 32,000 solar panels. DP World’s 415,000 m² site opens in 2025, multiplying capacity. Rest-of-Kingdom areas from Tabuk to Najran remain underserved, but Jahez’s leap from 19 to 52 city footprints in 12 months shows that secondary corridors are entering the Saudi Arabia e-commerce logistics market mainstream.

Competitive Landscape

No operator holds more than 15% revenue, placing overall concentration at the mid-range. DHL secured a minority stake in AJEX in August 2025, gaining 60 facilities and 1,200 vehicles. Q Logistics’ 63.26% acquisition of Aramex in July 2025 fuses port assets with a 70-country parcel network. Maersk signed a July 2025 MoU with Saudi Post that splits customs and last-mile duties, illustrating ecosystem partnerships.

Tech plays a shape differentiation: SMSA-Huawei’s cloud pact aims for real-time optimization, while Jahez pioneers autonomous robots. Asset-light startups such as Olivery enable 200 clients with no-code orchestration tools. Cold-chain last mile remains a white-space, fewer than 500 refrigerated vans serve national demand, offering room for new entrants. Reverse-logistics aggregation is another gap, with retailers still self-managing costly flows.

Consolidation is expected to continue as global integrators chase scale, and regulatory clarity favors capital-intensive solutions.

Saudi Arabia E-commerce Logistics Industry Leaders

Saudi Post

SMSA Express

Zajil Express

Aramex

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: DHL finalized a minority stake in AJEX, adding 60+ facilities and 1,200 vehicles.

- August 2025: Jahez Logistics began an autonomous robot pilot in Riyadh under Transport General Authority approval.

- July 2025: Q Logistics completed a 63.26% takeover of Aramex, integrating port-to-door services.

- July 2025: Maersk and Saudi Post signed an MoU linking Jeddah fulfillment with national last-mile reach.

Saudi Arabia E-commerce Logistics Market Report Scope

E-commerce logistics, referred to as e-logistics, is a process e-commerce brands use to get an order out the door and into the hands of the customer. After shoppers make an online purchase, the order is packed, shipped, delivered, and sometimes returned. It includes inventory management, Pricing, Packing, Shipping, Order fulfillment, Warehousing, and Last-mile delivery.

The Saudi Arabia e-commerce logistics market is segmented by service (transportation, warehousing, and inventory management, and value-added services (labeling, packaging, etc.)), by business (B2B and B2C), destination (domestic and international/cross-border), by product (fashion and apparel, consumer electronics, home appliances, furniture, beauty and personal care products, and other products (toys, food products, etc.)). The report offers market size and forecasts in value (USD) for all the above segments.

| Transportation | Road |

| Air | |

| Rail | |

| Maritime | |

| Warehousing and Fulfilment | |

| Value-Added (Labelling, Packaging, Kitting) |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| Domestic |

| Cross-Border/International |

| Same-day (less than 24 h) |

| Next-day (24-48 h) |

| Standard (3-5 days) |

| Economy (more than 5 days) |

| Others |

| Foods and Beverages |

| Beauty and Personal Care |

| Fashion and Lifestyle (accessories, apparel, footwear) |

| Furniture |

| Electronics and Household Appliances |

| Other Products |

| Riyadh Province |

| Makkah Province |

| Eastern Province |

| Rest of Saudi Arabia |

| By Service | Transportation | Road |

| Air | ||

| Rail | ||

| Maritime | ||

| Warehousing and Fulfilment | ||

| Value-Added (Labelling, Packaging, Kitting) | ||

| By Business Model | Business-to-Business (B2B) | |

| Business-to-Consumer (B2C) | ||

| Consumer-to-Consumer (C2C) | ||

| By Destination | Domestic | |

| Cross-Border/International | ||

| By Delivery Speed | Same-day (less than 24 h) | |

| Next-day (24-48 h) | ||

| Standard (3-5 days) | ||

| Economy (more than 5 days) | ||

| Others | ||

| By Product Category | Foods and Beverages | |

| Beauty and Personal Care | ||

| Fashion and Lifestyle (accessories, apparel, footwear) | ||

| Furniture | ||

| Electronics and Household Appliances | ||

| Other Products | ||

| By Geography | Riyadh Province | |

| Makkah Province | ||

| Eastern Province | ||

| Rest of Saudi Arabia |

Key Questions Answered in the Report

How large will the Saudi Arabia e-commerce logistics market be by 2031?

How large will the Saudi Arabia e-commerce logistics market be by 2031?

Which segment is growing fastest in service offerings?

Which segment is growing fastest in service offerings?

Which province shows the highest growth potential?

Which province shows the highest growth potential?

How is same-day delivery economics evolving?

How is same-day delivery economics evolving?

What are the main constraints facing operators?

What are the main constraints facing operators?

Are global integrators increasing their footprint?

Are global integrators increasing their footprint?

Page last updated on: