Middle East E-commerce Warehouse Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

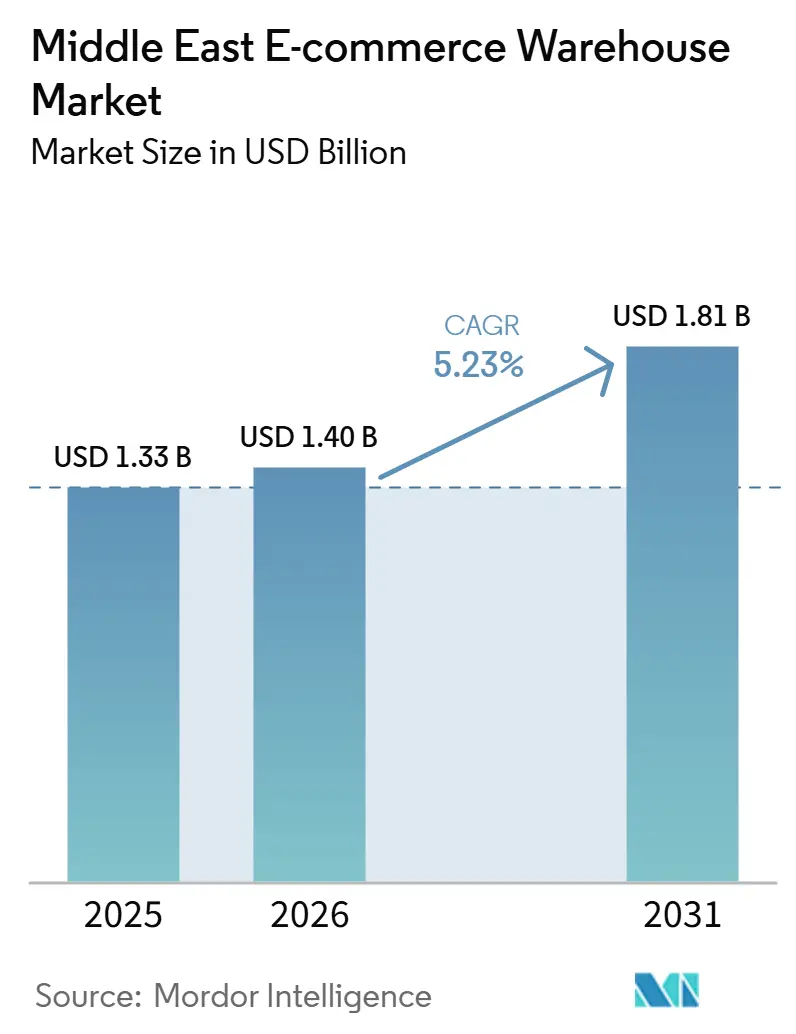

| Base Year Market Size (2025) | USD 1.33 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.81 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

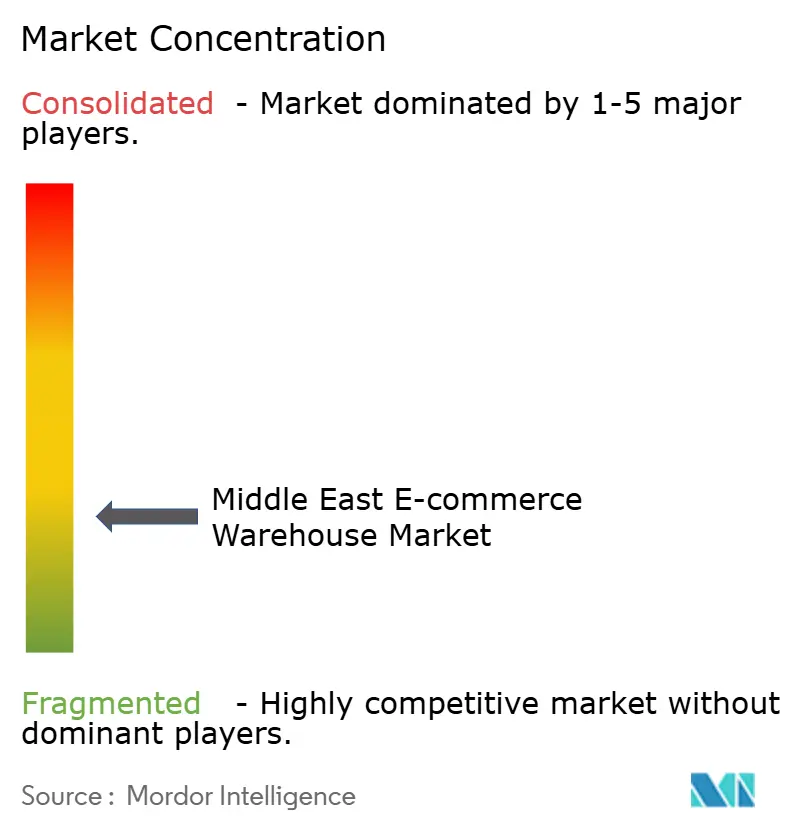

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East E-commerce Warehouse Market Analysis by Mordor Intelligence

The Middle East e-commerce warehousing market size is projected to be USD 1.33 billion in 2025, USD 1.40 billion in 2026, and reach USD 1.81 billion by 2031, growing at a CAGR of 5.23% from 2026 to 2031.

The market is expanding as fast-growing online retail volumes, wider digital-payment adoption, and new cross-border trade agreements shorten fulfillment cycles and push operators to build smarter, better-located facilities.[1]General Authority for Statistics, “Monthly Wholesale and Retail Indices,” stats.gov.sa Investments are flowing into temperature-controlled buildings, last-mile dark stores, and AI-enabled inventory systems, while sovereign wealth funds continue to bankroll mega-logistics parks that integrate ports, airports, and free zones. Automation suppliers are finding an eager customer base, yet capital constraints keep many small and mid-tier firms reliant on semi-manual operations. Competitive intensity is shifting to capability depth control-tower visibility, returns handling, and ESG compliance rather than sheer warehouse count, and operators able to combine technology with service breadth are winning high-margin contracts.

Key Report Takeaways

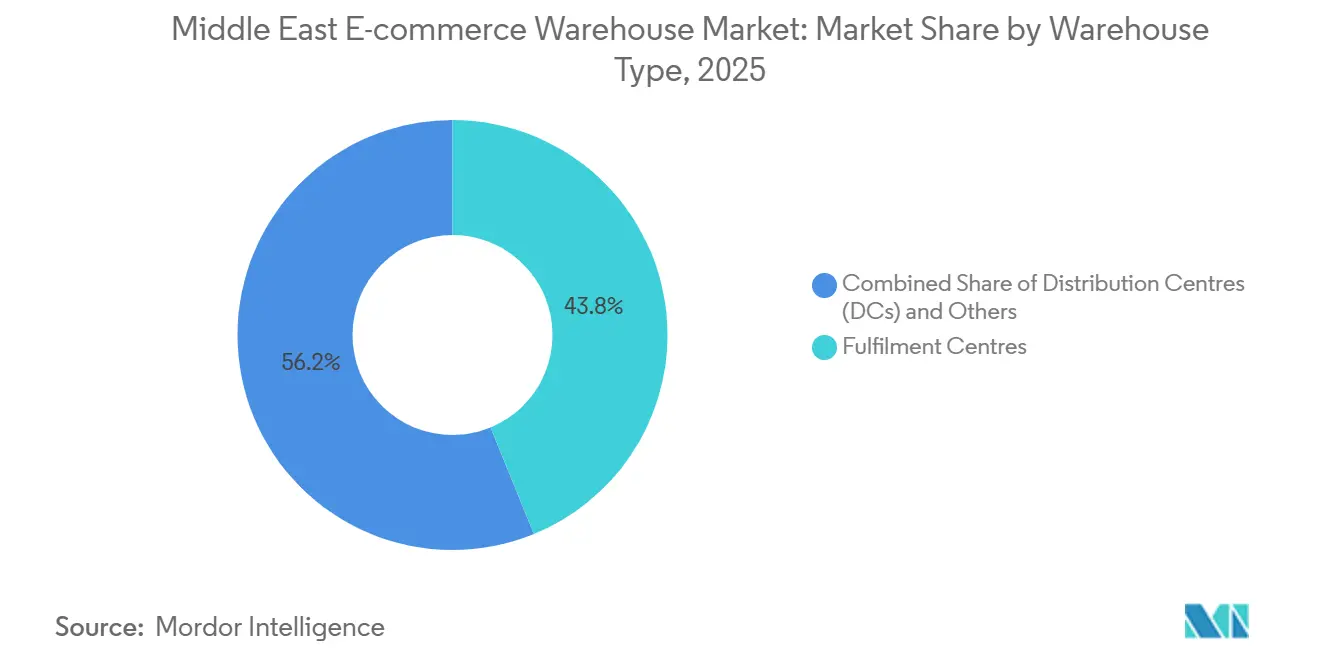

- By warehouse type, fulfillment centers led with 43.81% of the Middle East e-commerce warehousing market share in 2025, while micro-fulfillment and dark stores are forecast to grow at a 10.68% CAGR to 2031.

- By service, storage captured 50.07% of the Middle East e-commerce warehousing market size in 2025, and value-added services are advancing at a 10.15% CAGR through 2031.

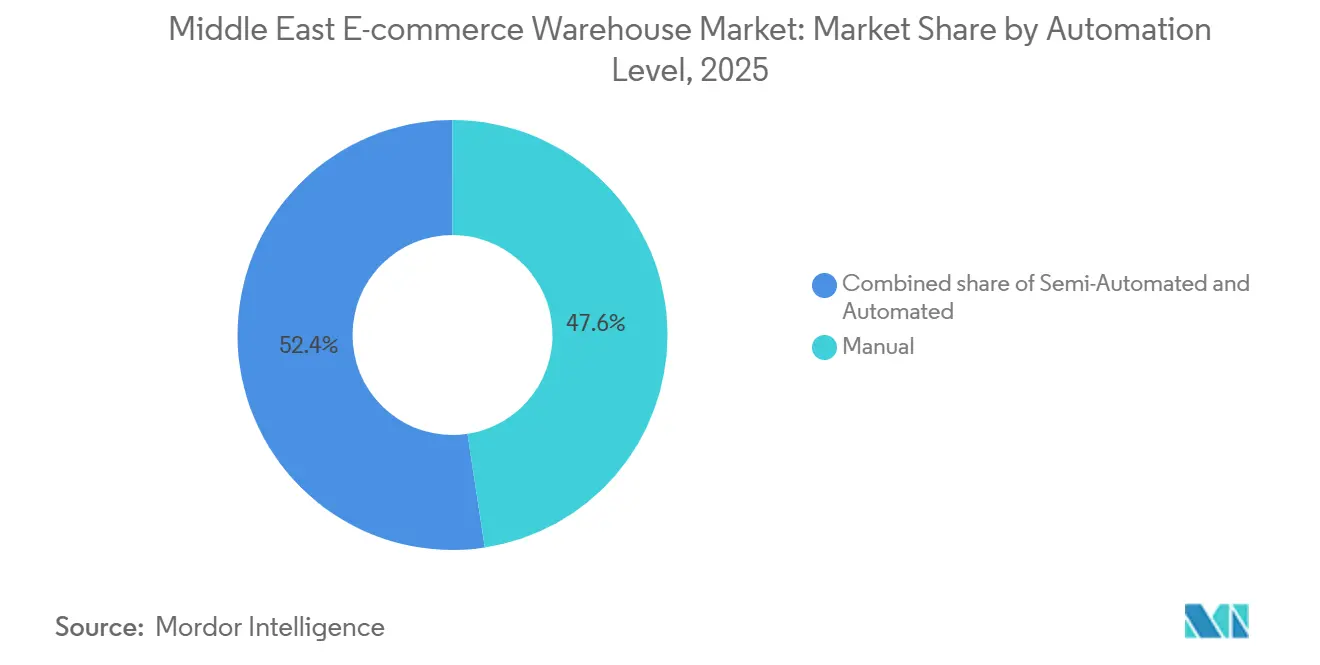

- By automation, manual sites retained 47.6% of the Middle East e-commerce warehousing market share in 2025, whereas fully automated facilities are poised to expand at a 9.76% CAGR over 2026-2031.

- By end user, consumer electronics accounted for 27.14% of the Middle East e-commerce warehousing market size in 2025; grocery and FMCG is the fastest-growing vertical at a 10.26% CAGR to 2031.

- By geography, Saudi Arabia held 31.53% of the Middle East e-commerce warehousing market share in 2025, and the United Arab Emirates is projected to post the quickest growth at a 6.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Middle East E-commerce Warehouse Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding digital-payment penetration unlocking prepaid fulfillment capacity | +1.6% | UAE, Saudi Arabia, Bahrain | Short term (≤ 2 years) |

| Regional free-trade pacts shrinking intra-GCC customs cycle times | +1.3% | All GCC markets | Medium term (2-4 years) |

| Post-pandemic shift toward online-first grocery and pharmacy replenishment | +1.1% | Dubai, Riyadh, Doha | Short term (≤ 2 years) |

| Plug-and-play 4PL control towers enabling SME cross-border scaling | +0.8% | Dubai, Jeddah, Kuwait City | Medium term (2-4 years) |

| Rapid rise of circular-economy recommerce platforms spurring dedicated returns hubs | +0.7% | UAE, Saudi Arabia | Long term (≥ 4 years) |

| AI-driven inventory-prediction engines justifying high-throughput automation | +0.9% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Digital-Payment Penetration Unlocking Prepaid Fulfillment Capacity

Digital wallets and buy-now-pay-later options have moved cash handling out of the warehouse and onto fintech rails. Prepaid orders reduce working-capital lockups, enable leaner safety stocks, and allow fulfillment teams to promise same-day dispatch without cash-on-delivery reconciliation steps. Lower theft risk and insurance premiums add a cost bonus, and banks’ real-time confirmation APIs now trigger warehouse wave picking within minutes of checkout. Faster cash cycles are particularly evident in the UAE, where prepaid penetration already tops 70% of online orders, giving operators room to scale without proportional inventory buildup.

Regional Free-Trade Pacts Shrinking Intra-GCC Customs Cycle Times

The January 2025 expansion of the GCC Integrated Customs Tariff has turned formerly national networks into one regional pool. Harmonized codes and single-window clearance allow a fulfillment center in Riyadh to replenish shoppers in Kuwait or Oman in under 72 hours with no re-declaration paperwork.[2]GCC-STAT, “GCC Integrated Tariff Handbook,” gccstat.org Saudi Arabia’s 50-year tax exemptions inside new Special Integrated Logistics Zones accelerate the hub-and-spoke shift, while Dubai leverages its bonded corridors to keep ports and airports synchronized. Trade friction is falling fastest for high-velocity goods such as smartphones and fast fashion, giving operators new options to stock inventory once and sell it many times across the Gulf.

Post-Pandemic Shift Toward Online-First Grocery & Pharmacy Replenishment

The rapid expansion of the Middle East e-commerce warehouse market is driven by the permanent consumer shift toward high-frequency digital replenishment of essentials. This has necessitated massive investment in hyper-local "dark stores" and automated cold-chain infrastructure to support the region's surge in on-demand grocery and pharmacy delivery. Grocery baskets ordered online have stayed high even after lockdowns ended. Cold-chain nodes must now meet pharmaceutical-grade traceability, keeping temperature logs and batch serials that regulators can audit on demand.[3]Ministry of Health and Prevention, “Cold Chain Compliance Guide 2026,” mohap.gov.ae Heavy investment is flowing into multi-temperature mezzanines, plus IoT sensors that alert staff before spoilage risk spikes.

Plug-And-Play 4PL Control Towers Enabling SME Cross-Border Scaling

Fourth-party logistics (4PL) platforms combine cloud WMS, multi-carrier shipping, and compliance services so a micro-brand in Kuwait can sell across the Gulf overnight. By aggregating SME demand, they negotiate volume rates on space and transport, pushing more pallets through existing warehouses without new construction. Investors poured USD 9 million into Locad’s GCC rollout to exploit the model’s asset-light appeal. For operators, white-label control towers translate into sticky contracts because merchants embed their storefronts and customer promises into the platform’s workflows.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of Grade-A logistics land outside free-trade zones inflating lease premiums | -0.9% | Dubai, Abu Dhabi, Riyadh | Short term (≤ 2 years) |

| Volatile industrial electricity tariffs eroding cold-chain profit margins | -0.5% | Saudi Arabia, UAE | Medium term (2-4 years) |

| ESG disclosure mandates escalating capex for solar-powered and carbon-neutral warehouses | -0.4% | UAE, Saudi Arabia, Qatar | Long term (≥ 4 years) |

| Cash-on-delivery persistence complicating reverse-logistics flows and cash recovery | -0.3% | Egypt, secondary GCC cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Grade-A Logistics Land Outside Free-Trade Zones Inflating Lease Premiums

Most modern warehouses sit inside free zones, and land beyond them often lacks height allowances, fire systems, or foreign-ownership clarity. Rents in Dubai’s prime corridors rose by double digits in 2025 as supply lagged demand, pushing second-tier operators into outlying plots with weaker road links. Speculative developers are breaking ground, but permitting cycles take years, so capacity tightness will linger. Build-to-suit deals lock in tenants yet require long leases that smaller brands hesitate to sign, keeping market entry tough for new players.

Volatile Industrial Electricity Tariffs Eroding Cold-Chain Profit Margins

GCC subsidy reforms mean kilowatt-hour prices now swing quarterly, and cold rooms can consume 40% of a site’s opex. Operators hedge by installing rooftop solar and battery arrays. Ford’s Dubai parts center added a 400 kW system, but payback stretches if tariffs dip again. Uneven reforms create cost gaps: a freezer in Riyadh may pay twice the power bill of its Bahrain equivalent, distorting contract bids. Such unpredictability delays investment in new chillers unless a blue-chip grocer guarantees multi-year volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Fulfillment Centers Anchor Regional Networks

Fulfillment centers accounted for 43.81% of the Middle East e-commerce warehousing market share in 2025, reflecting their role as multi-channel inventory pools that feed line-haul, parcel, and click-and-collect networks. Typically sized 10,000–50,000 m², they sit on peri-urban land that balances rent with access to ports and highways. Operators outfit them with high-bay racking, mezzanines for value-added services, and WMS integrations that sync with carrier APIs. Demand is steady as merchants shift from single-store rooms to shared third-party sites where they gain scale without owning assets.

Urban dark stores and micro-fulfillment centers post the fastest growth at a 10.68% CAGR through 2031, driven by quick-commerce apps promising 30-minute grocery or pharmacy delivery. These 300–2,000 m² nodes specialize in top-selling SKUs, use dense tote-based grids, and benefit from AI that predicts neighborhood demand by hour. The Middle East e-commerce warehousing market size for micro-fulfillment is still modest, yet land scarcity inside city limits has sparked creative solutions such as mall basements and rooftop conversions. Kuehne + Nagel’s 23,000 m² site in Dubai’s EZDubai zone shows how legacy 3PLs mix large fulfillment halls with adjacent micro hubs to cover both bulk storage and ultrafast delivery.

By Service Type: Storage Dominates, but Value-Added Services Accelerate

Storage services generated 50.07% of the Middle East e-commerce warehousing market size in 2025, because e-commerce still rests on safe, climate-controlled inventory holding. Pallet positions, clear height, and fire protection remain the primary leasing criteria for most tenants. However, commoditization keeps margins thin, and operators search for stickier income streams. Value-added services, expanding at a 10.15% CAGR, include kitting, postponement manufacturing, personalized packaging, and photo studios. The Middle East e-commerce warehousing market size linked to such services rises as brands demand local customization to shorten supply chains and comply with language or regulatory labeling rules.

Expeditors’ 23,200 m² Dubai South facility illustrates the shift, offering order management, returns grading, and export documentation under one roof. Brands pay premiums for last-minute localization that enables region-specific launches or seasonal bundles. Picking and packing remain essential, yet automation here, voice-directed headsets, pick-to-light shelves, reduces labor minutes per order, focusing competitive positioning on higher-value assembly or customization tasks instead of basic cartons-in, cartons-out.

By Automation Level: Manual Sites Still Rule, but Robots Climb the Curve

Manual facilities held 47.6% of the Middle East e-commerce warehousing market share in 2025, favored by mid-sized merchants due to lower upfront costs and flexibility to handle odd shapes or limited volumes. Workers perform receipt, putaway, and pick tasks with RF scanners and forklifts. Semi-automated sites bridge the gap, adding conveyors, vertical lift modules, or pick-assist robots in the highest-traffic zones. Fully automated buildings, though only a minority today, are growing fastest at a 9.76% CAGR as robotics costs fall and labor scarcity intensifies.

The Middle East e-commerce warehousing market size tied to automated operations expands whenever throughput exceeds 3,000 orders per hour, and accuracy demands hit 99.9%. Swisslog’s AutoStore grids quadruple storage density and cut travel time, making automation viable even where land is pricey. Operators finance these systems through multi-year contracts with anchor tenants, aligning depreciation schedules with revenue certainty. Green performance dashboards baked into modern WMS help landlords hit ESG goals while squeezing extra kilowatt savings by orchestrating robot charging off-peak.[4]Swisslog, “AutoStore Deployments in the GCC,” swisslog.com

By End-User Industry: Electronics Commands, Grocery Surges

Consumer electronics captured 27.14% of the Middle East e-commerce warehousing market size in 2025, relying on security cages, serialized tracking, and anti-static zones to move high-value goods quickly and safely. Short product lifecycles demand rapid turnover; hence, electronics brands favor warehouses wired for cycle-count automation and real-time stock alerts. The share reflects affluent Gulf buyers upgrading phones and wearables frequently.

Grocery and fast-moving consumer goods (FMCG) blaze the growth trail at a 10.26% CAGR to 2031. Cold, chilled, and ambient chambers coexist inside single premises, and food-grade racking meets strict hygiene codes. RSA Cold Chain’s 40,000-pallet complex in Jebel Ali demonstrates multimodal reach, shipping milk nationwide within hours while hosting pharma SKUs that need 2-8 °C. The Middle East e-commerce warehousing market size for chilled products is smaller today but expanding fast as regional grocery chains drive online baskets and offer one-hour delivery slots.

Geography Analysis

Saudi Arabia accounted for 31.53% of the regional market in 2025, reflecting Vision 2030 programs that pour capital into road, rail, and air freight nodes while offering 50-year tax holidays inside Special Integrated Logistics Zones. DP World’s USD 240 million, 185,000 m² bonded logistics park at Jeddah Islamic Port exemplifies Grade A inventory arriving at pace. Customs fee cuts to 0.15% of goods value in October 2024 improved cross-border economics, turning Riyadh into a natural hub for multi-country e-commerce flows.

The United Arab Emirates is projected to expand at a 6.08% CAGR through 2031 as Dubai South cements itself as a digital-commerce sandbox where bonded air-sea corridors slash dwell time, and Abu Dhabi’s KEZAD megazone lures manufacturing-linked logistics. Mature port and airport networks keep dwell times low. Dark stores near Dubai Marina fulfill sub-one-hour grocery demand, while upstairs micro-fulfillment nodes inside malls illustrate how the Emirates monetizes scarce city land for last-mile gains.

Smaller Gulf states pursue niche plays: Qatar focuses on high-value perishables via Hamad Port, and Bahrain leverages free-trade access to Saudi’s Eastern Province. Egypt offers scale outside the Gulf; AD Ports Group’s long-term concessions to modernize Safaga and other Red Sea ports bridge Gulf suppliers to North African consumers. Although infrastructure gaps persist, first-mover operators enjoy lower land costs and pent-up demand, positioning Egypt and Oman as future growth hotbeds once regulatory clarity improves.

Competitive Landscape

Competition is fragmenting into capability tiers. Sovereign-backed giants such as ADQ-armed Aramex and DP World wield cheap capital and priority land access, letting them roll out multi-country parks, solar roofs, and robotics without balance-sheet strain. Global integrators such as DHL, FedEx, and UPS deploy proven technology stacks and global account contracts to lock in high-spend retailers. Niche specialists focus on regulated verticals like pharma or luxury returns, earning margin premiums through expertise.

Strategic moves concentrate on vertical integration. DP World funnels freight from its ports straight into on-site e-commerce sheds, eliminating drayage. DHL committed USD 570 million to Middle East automation by 2030, adding sorters and robotics that handle peak singles-day volumes with ease. ADQ’s 2025 takeover of Aramex injects sovereign heft into a parcel leader, hinting at deeper integration with Abu Dhabi’s Etihad Cargo belly capacity.

Technology is the new battleground. AI-driven control towers give real-time inventory heat maps, predictive restocking, and carbon dashboards. Operators building proprietary data layers drive switching costs, as merchants tying storefronts to an API hesitate to re-engineer processes elsewhere. ESG capability differentiates at the RFP stage: tenants now request LEED Gold or solar coverage thresholds before signing multiyear leases. Smaller local players, squeezed between capital intensity and compliance creep, may seek joint ventures to survive or position themselves for acquisition.

Middle East E-commerce Warehouse Industry Leaders

Aramex

UPS Supply Chain Solutions

FedEx Logistics

DHL Group

DSV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Agility Logistics Parks signed Heads of Terms to structure a joint venture with ROSHN Group, a Saudi Arabia-based Public Investment Fund company. The joint venture aims to develop a massive 1 to 1.5 million square meter logistics and warehousing park in a strategic Saudi Arabian corridor to support trade efficiency and regional supply chains.

- January 2026: CEVA Logistics opened a dedicated 247,000 sq ft e-commerce fulfillment warehouse in the Dubai South Free Zone. Built with a heavy focus on sustainability, it features 1,600 sqm of solar panels, full B2B/B2C fulfillment capabilities, and advanced warehouse management systems, already processing over 30,000 units daily upon opening.

- December 2025: DHL Group officially opened its newly expanded Middle East & Africa (MEA) Innovation Center. In parallel, DHL Supply Chain announced a EUR 120 million investment to develop a 55,000 square-meter, carbon-neutral, multi-user contract logistics warehouse in Dubai South to serve global and regional supply chains.

- December 2025: DSV advanced its regional logistics footprint by announcing a 30,000 sqm logistics hub in Jebel Ali South, Dubai. Designed for high-volume contract logistics, the facility features 22m high-bay storage, 74,000 pallet positions, and advanced temperature-controlled chambers for FMCG and pharmaceutical clients.

Middle East E-commerce Warehouse Market Report Scope

| Fulfilment Centres |

| Distribution Centres (DCs) |

| Cold-Chain Warehouses |

| Dark Stores / Micro-Fulfillment Centers |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.) |

| Storage |

| Picking & Packing |

| Value-Added Services and Others (Kitting, Labelling) |

| Manual |

| Semi-Automated |

| Automated |

| Apparel and Footwear |

| Consumer Electronics |

| Grocery and FMCG |

| Pharmaceuticals, Beauty and Wellness |

| Home Essentials and Furnishings |

| Others |

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Kuwait |

| Bahrain |

| Oman |

| Egypt |

| Rest of Middle East |

| By Warehouse Type | Fulfilment Centres |

| Distribution Centres (DCs) | |

| Cold-Chain Warehouses | |

| Dark Stores / Micro-Fulfillment Centers | |

| Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.) | |

| By Service Type | Storage |

| Picking & Packing | |

| Value-Added Services and Others (Kitting, Labelling) | |

| By Automation Level | Manual |

| Semi-Automated | |

| Automated | |

| By End-User Industry | Apparel and Footwear |

| Consumer Electronics | |

| Grocery and FMCG | |

| Pharmaceuticals, Beauty and Wellness | |

| Home Essentials and Furnishings | |

| Others | |

| By Country (Value) | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Kuwait | |

| Bahrain | |

| Oman | |

| Egypt | |

| Rest of Middle East |

Key Questions Answered in the Report

How large will e-commerce warehousing revenues in the Middle East be by 2031?

The market is forecast to reach USD 1.81 billion by 2031, expanding from USD 1.33 billion in 2025 at a 5.23% CAGR.

Which warehouse type leads regional revenues today?

Fulfillment centers hold 43.81% of 2025 revenues because they balance inventory breadth with multi-channel shipping capability.

What is the fastest-growing end-user vertical?

Grocery and FMCG is projected to rise at a 10.26% CAGR through 2031 as consumers maintain online ordering habits and demand chilled delivery.

Why are automated warehouses gaining popularity?

AI-powered demand forecasting now delivers sub-5% error rates, justifying the capital outlay for robotics by boosting throughput and cutting labor costs.

How are Gulf governments supporting the sector?

Vision-aligned programs grant long tax holidays, invest in mega-parks like Jeddah Logistics Park, and unify customs codes to speed cross-border e-commerce flows.

What keeps manual facilities relevant despite the rise of robotics?

Lower upfront spending, flexibility for odd-shaped or low-volume SKUs, and easier staffing make manual sites attractive to smaller merchants that cannot yet justify full automation.

Page last updated on: