Kenya Warehousing And Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

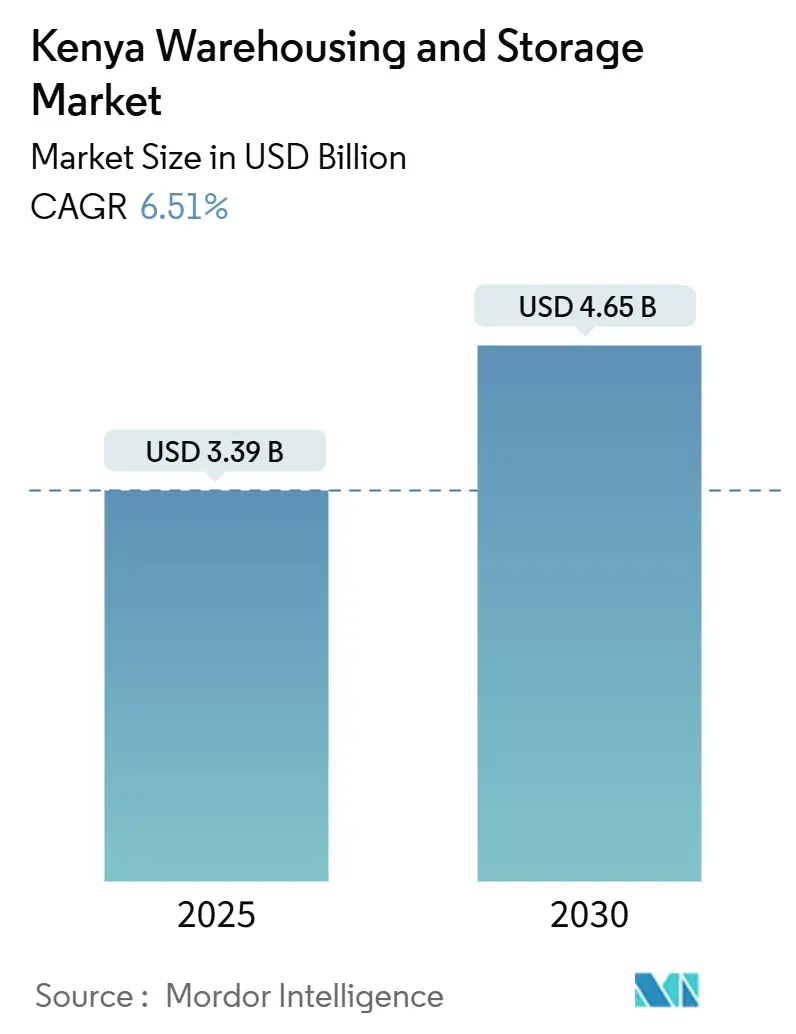

| Market Size (2025) | USD 3.39 Billion |

| Market Size (2030) | USD 4.65 Billion |

| Growth Rate (2025 - 2030) | 6.51% CAGR |

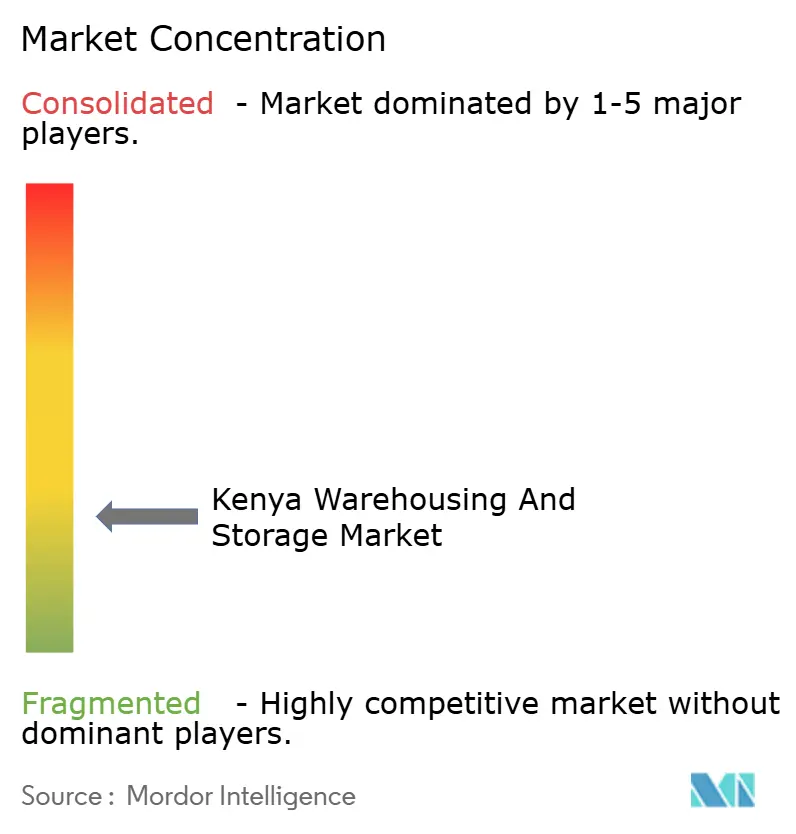

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kenya Warehousing And Storage Market Analysis by Mordor Intelligence

The Kenya Warehousing And Storage Market size is estimated at USD 3.39 billion in 2025, and is expected to reach USD 4.65 billion by 2030, at a CAGR of 6.51% during the forecast period (2025-2030).

Robust Vision 2030 infrastructure spending, the country’s gateway role for land-locked neighbors, and a sharp uptick in online shopping collectively anchor this growth path. Port-side capacity upgrades and the Standard Gauge Railway strengthen the corridor linking Mombasa and Nairobi, which remains the spine of domestic and regional distribution[1]International Maritime Organization, “Mombasa Port Expansion Completed,” imo.org. Demand also benefits from fast-rising FMCG consumption in rural areas that pulls modern storage networks deeper into the interior. At the same time, energy-efficient designs, on-site solar systems, and automation curb operating costs that weigh on operators facing some of East Africa’s highest electricity tariffs.

Key Report Takeaways

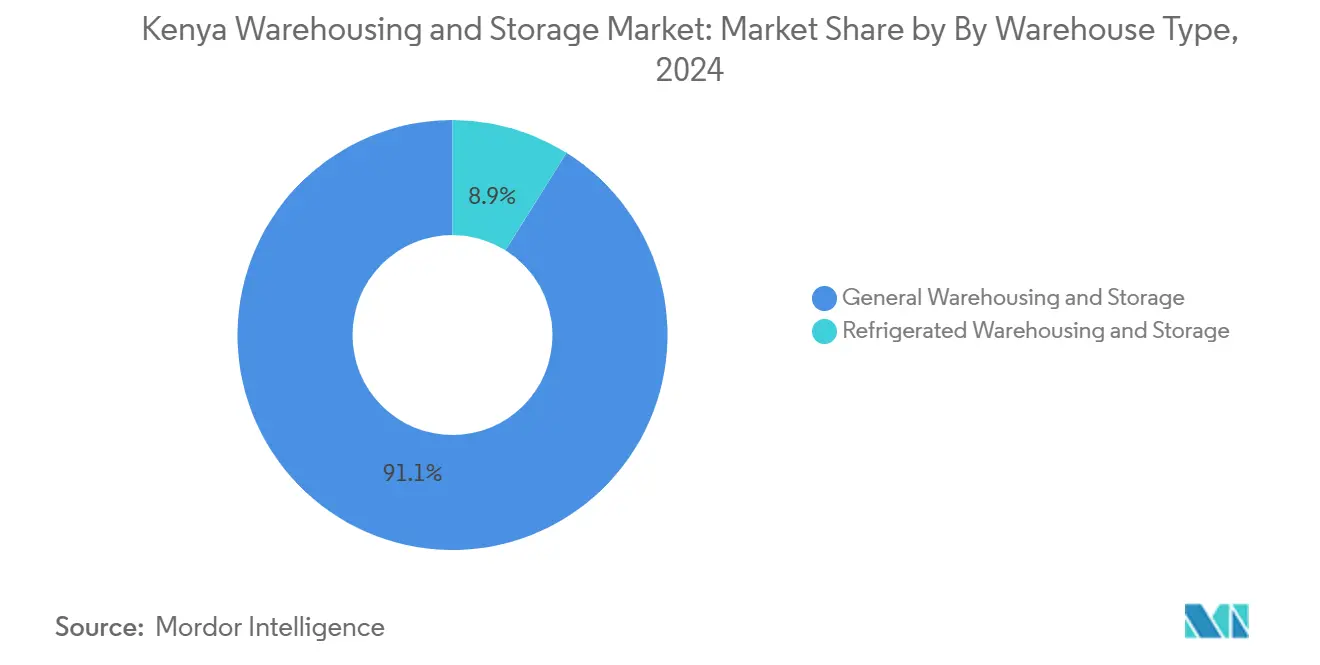

- By warehouse type, general warehousing and storage held 91.12% of the Kenya warehousing and storage market share in 2024, while refrigerated warehousing and storage is expanding at a 6.83% CAGR through 2030.

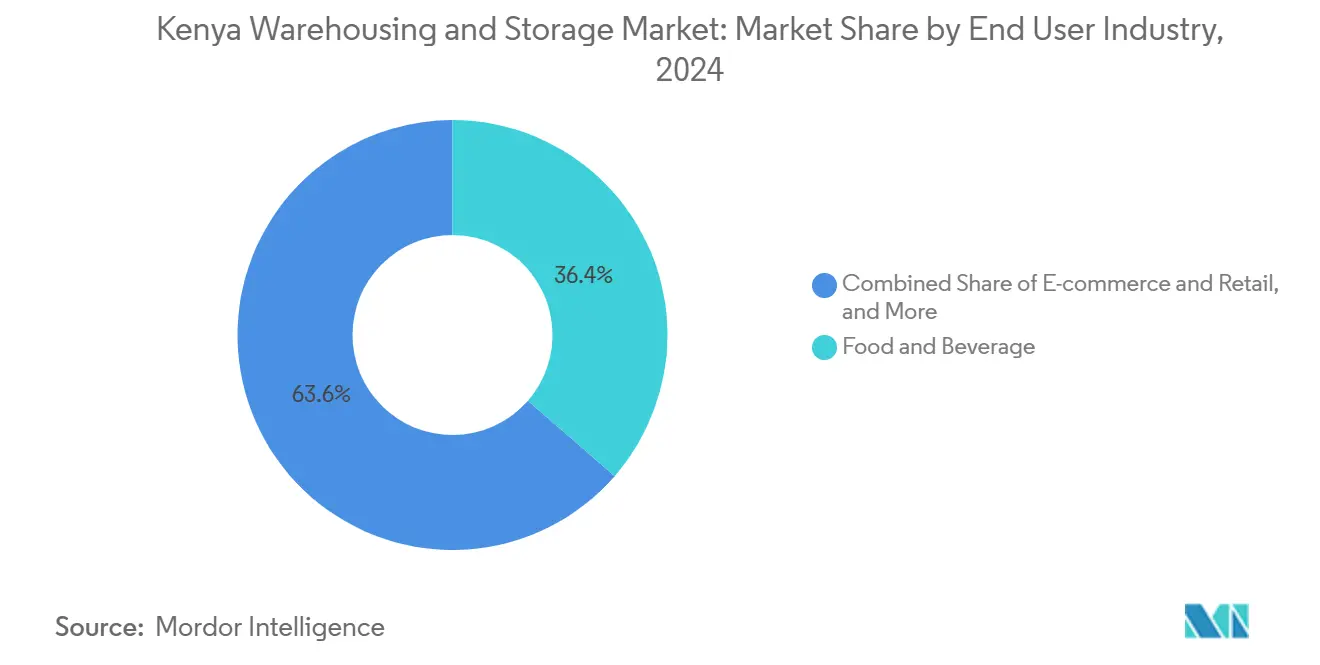

- By end user industry, food and beverage accounted for 36.40% of the Kenya warehousing and storage market size in 2024, whereas e-commerce and retail are advancing at a 6.90% CAGR to 2030.

Kenya Warehousing And Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce & omnichannel retail | +1.2% | Nairobi, Mombasa, Kisumu | Short term (≤ 2 years) |

| Expansion of FMCG consumption | +0.9% | National rural focus | Medium term (2–4 years) |

| Infrastructure upgrades under Vision 2030 & LAPSSET | +1.5% | National with corridor focus | Long term (≥ 4 years) |

| Rising cold-chain demand for agri-exports & pharma | +1.1% | Mombasa–Nairobi axis | Medium term (2–4 years) |

| Emergence of SEZs & tax-incentivized logistics parks | +0.8% | Mombasa, Nairobi, county parks | Long term (≥ 4 years) |

| Mobile-money enabled micro-fulfilment networks | +0.6% | Urban and peri-urban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce & Omnichannel Retail

Digital commerce growth is reshaping facility location and design. Online sellers now favor micro-fulfilment hubs near dense urban neighborhoods to cut delivery times, driving a pipeline of smaller, technology-rich warehouses in Nairobi and Mombasa. County plans to launch integrated fresh-produce markets, adding demand for temperature-controlled cross-docks that match omnichannel distribution requirements. Cross-border e-commerce linked to the East African Community accelerates demand for customs-bonded storage that can manage high SKU counts. Mobile-money integration underpins cash-on-delivery models and raises the need for robust reverse-logistics zones inside warehouses. Operators therefore invest in automated sorters and IoT-enabled inventory tools to handle surging order volumes without compromising accuracy or speed.

Expansion of FMCG Consumption

Rural middle-income growth shifts warehousing footprints toward hub-and-spoke networks that reach county towns quickly. Newly announced County Aggregation and Industrial Parks provide multi-tenant space, reducing outbound haulage costs for consumer-goods makers. Cold rooms are being added as dairy, frozen meat, and personal-care categories expand. Facilities must accommodate mixed-pallet picking and rapid cycle times that differ from bulk import storage. Rural nodes also encourage the Kenya warehousing and storage market to integrate renewable energy because grid power is patchier outside major cities.

Infrastructure Upgrades Under Vision 2030 & LAPSSET

The LAPSSET highway, rail, and pipeline corridor opens new logistics arcs from Lamu Port toward Ethiopia and South Sudan, prompting plans for multi-modal warehouses near Isiolo and Moyale[2]African Development Bank, “LAPSSET Corridor Development Master Plan Study,” afdb.org. Standard Gauge Railway inland depots near Nairobi and Naivasha now attract transit-cargo storage facilities. Vision 2030 allocations also back dedicated logistics parks that integrate road, rail, and pipeline links, locking in long-term land for warehouse development. Port of Mombasa expansion creates additional yard and bonded-warehouse demand to maintain berth productivity once capacity rises.

Rising Cold-Chain Demand for Agri-exports & Pharma

Kenya’s push to cut post-harvest losses and uphold export quality propels investment in temperature-controlled storage. New farm-gate cooling hubs and IATA CEIV Pharma-certified facilities in Nairobi handle rising volumes of fresh produce, vaccines, and biologics. Continuous-power requirements make solar-plus-battery systems attractive despite higher upfront costs, helping operators secure premium rents while staying within energy-cost limits. Technical and regulatory hurdles limit market entry, which increases pricing power for qualified suppliers[3]Food and Agriculture Organization, “Food Loss and Waste in Sub-Saharan Africa,” fao.org.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity & utility costs | -0.7% | National, industrial zones | Short term (≤ 2 years) |

| Land acquisition & zoning hurdles | -0.5% | Urban and SEZ areas | Medium term (2–4 years) |

| Poor rural last-mile road connectivity | -0.4% | Rural network | Long term (≥ 4 years) |

| Scarcity of automation-skilled technicians | -0.3% | Major hubs | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Electricity & Utility Costs

Tariffs remain the highest in East Africa, squeezing margins and slowing automation rollouts. Cold-storage operators face demand charges that inflate power bills just as they install energy-hungry refrigeration units[4]International Energy Agency, “Kenya Energy Profile,” iea.org. Although recent tariff cuts offer relief, reliance on diesel back-up generators persists because grid outages still disrupt operations. Solar rooftops, efficient lighting, and variable-speed compressors lower bills but raise capital outlays that smaller firms struggle to absorb. Reliability issues force redundant power systems, adding to development costs and complicating project financing.

Land Acquisition & Zoning Hurdles

The multi-layer approval process under the Physical and Land Use Planning Act lengthens lead times and raises compliance costs. Scarce serviced plots near ports and highway interchanges fetch premium prices. Zoning inconsistencies across counties create uncertainty for networks that span several jurisdictions. New building codes increase structural requirements and insurance costs, yet they also elevate construction standards that appeal to multinational tenants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Cold Storage Drives Premium Growth

Refrigerated warehousing registers a 6.83% CAGR through 2030, outpacing general storage, which captured 91.12% of Kenya warehousing and storage market share in 2024. This differential reflects exporters’ demand for post-harvest freshness and strict pharmaceutical temperature mandates, both of which attract investors seeking higher margins than ambient facilities can offer. Kenya warehousing and storage market size for cold rooms is projected to widen further once Value Added Tax exemptions on food-grade equipment take effect in 2026.

Cold-chain operators invest in power-redundant designs and remote monitoring to comply with global food-safety codes, erecting barriers to new entrants. Government-backed community cooling hubs are also expanding, providing smaller farmers with access to modern storage and linking them to export pack-houses. While power costs erode returns, the ability to charge rental premiums and secure long-term anchor tenants keeps this niche attractive.

By End User Industry: E-commerce Reshapes Distribution Patterns

Food and beverage accounted for 36.40% of the Kenya warehousing and storage market size in 2024, but e-commerce and retail are set to expand at a 6.90% CAGR through 2030 as mobile buying climbs. Online platforms rely on urban micro-fulfilment centers equipped with automated pick stations and real-time inventory visibility, features that differ from bulk-pallet food storage.

Kenya warehousing and storage market growth in e-commerce encourages the conversion of older factory shells into multi-level sorting hubs that reduce last-mile times within Nairobi’s traffic-congested suburbs. Food distributors, in contrast, keep expanding regional depots along new county roads to serve rural grocers quickly. Both segments increasingly share third-party logistics providers to manage seasonal peaks, signalling opportunities for asset-light operators.

Geography Analysis

Kenya's warehousing and storage market activity clusters along the Mombasa–Nairobi freight corridor that moves most import and export flows. Port-adjacent yards handle rising container throughput and supply bonded storage that speeds customs clearance. Inland depots at Embakasi and Naivasha benefit from Standard Gauge Railway linkages, trimming truck congestion and anchoring new distribution parks.

Northern expansion under the LAPSSET program is opening warehouse opportunities near Isiolo, Garissa, and the Ethiopian border, though timelines hinge on road finishes and energy availability. Kisumu’s lake port gives shippers multimodal options into Uganda and Tanzania, yet shallow-draft limitations curb volumes for now.

County industrial parks in Eldoret, Nakuru, and Meru decentralize storage closer to agricultural production zones. These nodes lower rural delivery costs and shorten farm-to-market cycles, but they rely on ongoing rural-road upgrades to sustain capacity utilization. Special Economic Zones in Mombasa and Nairobi offer ten-year tax holidays and duty exemptions, drawing global 3PLs that want cost savings without compromising connectivity.

Competitive Landscape

The Kenya warehousing and storage market is fragmented. DHL, DSV, and Africa Global Logistics command premium contracts in port-side and cross-border trade because of strong capital bases and technology adoption. Local specialists such as Siginon Group and Cold Solutions Kenya thrive in pharma and fresh-produce niches where local know-how and cold-chain certification matter.

Technology is the new battleground. Operators deploy IoT sensors, WMS platforms, and automated conveyors to cut picking errors and woo e-commerce clients. Acquisition trends continue, illustrated by DSV’s planned purchase of Schenker, which will double its Sub-Saharan footprint and strengthen its position in Kenya. Cold-chain players raise barriers through IATA CEIV Pharma and ISO 22000 certifications that lock in multinationals needing compliance assurance.

White-space opportunities persist in rural fulfillment and hazardous-goods storage where regulatory hurdles deter rapid entry. Investors with deep pockets and skilled technicians stand to consolidate smaller depots, gaining scale economies that currently elude the sector.

Kenya Warehousing And Storage Industry Leaders

Africa Global Logistics

Sheffield Cargo Logistics Limited

Mitchell Cotts Kenya

Siginon Group

Freight Forwarders Kenya Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: DHL Group earmarked EUR 300 million (USD 312 million) for Sub-Saharan infrastructure, including new Nairobi fulfillment centers.

- April 2025: DSV announced the EUR 14.3 billion (USD 14.9 billion) acquisition of Schenker to deepen African network coverage.

- October 2024: Africa Global Logistics Kenya acquired a 5-acre parcel in Mombasa to expand regional storage capacity.

- January 2024: AGL received 20 acres at Naivasha SEZ, secured through a government land-lease award.

Kenya Warehousing And Storage Market Report Scope

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

| E-commerce & Retail |

| Food & Beverage |

| Manufacturing and Automotive |

| Healthcare, Pharmaceuticals, and Life Sciences |

| Chemicals & Specialty Materials |

| Others |

| By Warehouse Type | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By End User Industry | E-commerce & Retail |

| Food & Beverage | |

| Manufacturing and Automotive | |

| Healthcare, Pharmaceuticals, and Life Sciences | |

| Chemicals & Specialty Materials | |

| Others |

Key Questions Answered in the Report

What is the 2025 value of Kenya’s warehousing sector?

The Kenya warehousing and storage market size is USD 3.39 billion in 2025.

How fast is cold-storage capacity growing?

Refrigerated warehousing is expanding at a 6.83% CAGR through 2030, the fastest among warehouse types.

Which end-user segment is expanding most quickly?

E-commerce and retail facilities are growing at a 6.90% CAGR to 2030 as mobile shopping scales.

Why is the Mombasa-Nairobi corridor pivotal?

It handles most port traffic and is supported by Standard Gauge Railway links that attract new inland depots.

What keeps operating costs high for warehouse operators?

Elevated electricity tariffs and grid unreliability require costly back-up power and energy-efficient upgrades.

Page last updated on: