Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.12 Billion |

| Market Size (2026) | USD 7.32 Billion |

| Market Size (2031) | USD 8.40 Billion |

| Growth Rate (2026 - 2031) | 2.80% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Telecom MNO Market Analysis by Mordor Intelligence

The Qatar Telecom MNO Market size is expected to grow from USD 7.12 billion in 2025 to USD 7.32 billion in 2026 and is forecast to reach USD 8.4 billion by 2031 at 2.8% CAGR over 2026-2031. In terms of subscriber volume, the market is expected to grow from 4.65 million units in 2025 to 5.14 million units by 2030, at a CAGR of less than 2.02% during the forecast period (2025-2030). This growth pace demonstrates how the market is transitioning from network-building momentum to a service monetization focus, while universal fiber coverage of 99% and 96% 5G availability continue to underpin premium data uptake. The Communications Regulatory Authority plans to sunset 3G by December 2025, freeing up low-band spectrum that operators will redeploy for capacity-efficient LTE and 5G layers, thereby improving the user experience and increasing mobile data ARPU. Near 170% mobile penetration limits fresh subscriber additions, so operators prioritize tiered data packs, enterprise-managed services, and private-network projects to raise revenue per line. Government smart-infrastructure programs, including Lusail Smart City and post-World Cup stadia reuse, channel demand toward IoT connectivity, cloud links, and edge-computing nodes that expand the addressable spend for both incumbents.

Key Report Takeaways

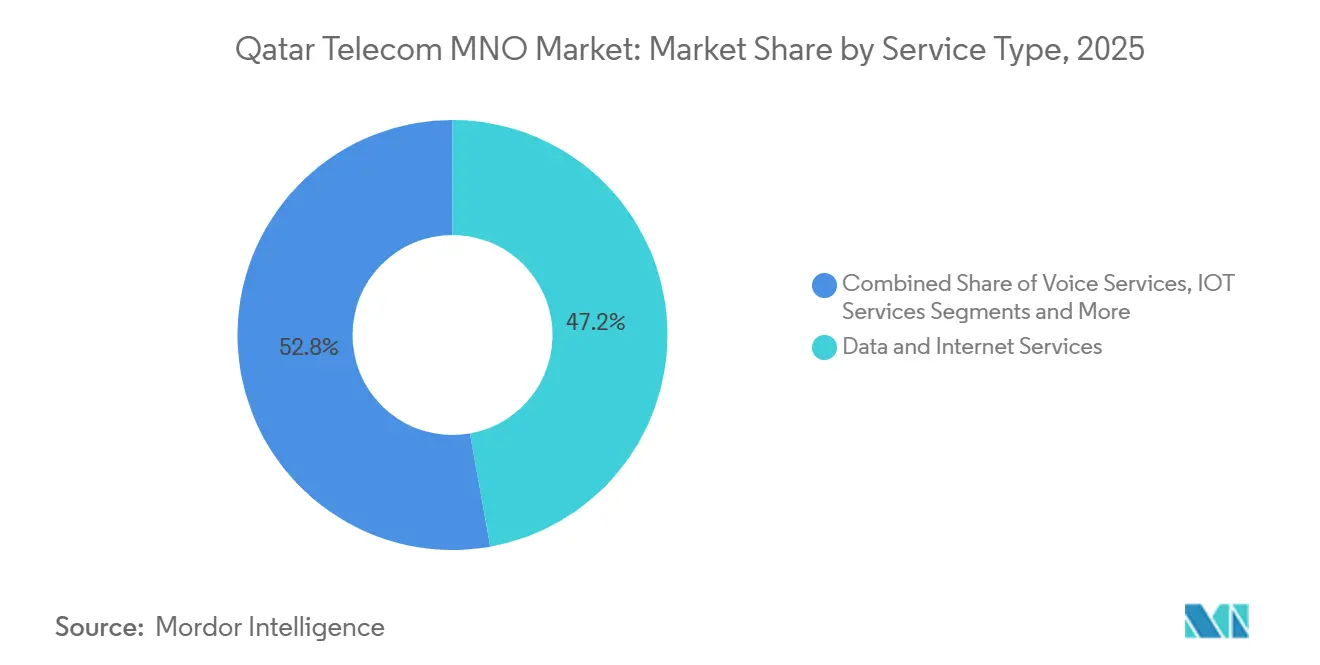

- By service type, data services captured 47.20% revenue share in 2025 while advancing at a 3.00% CAGR to 2031.

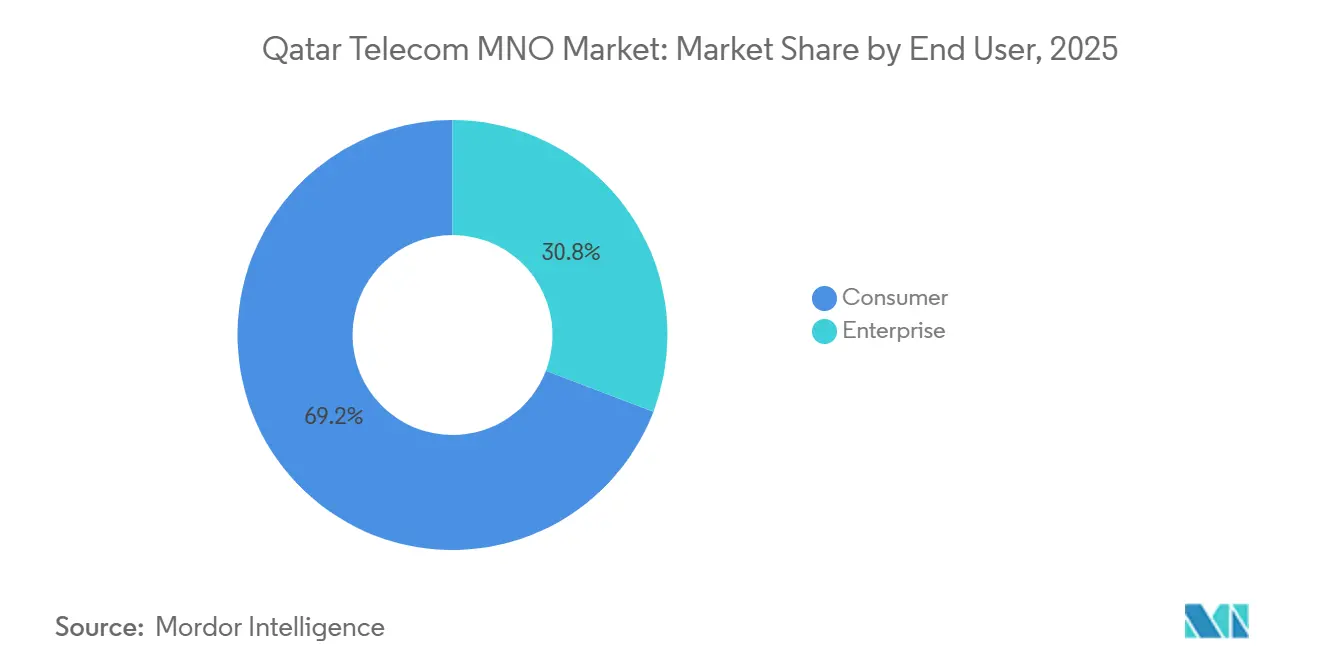

- By end-user, the enterprise segment held 30.80% of total 2025 revenues and delivers the highest 3.18% CAGR, compared with 2.68% for consumer.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G population-wide coverage lifts mobile data ARPU | +1.2% | Doha, Lusail, Al Wakrah | Medium term (2-4 years) |

| National Digital Agenda 2030 targets universal fiber | +0.8% | Nationwide, strongest in urban centers | Long term (≥ 4 years) |

| Post-World-Cup smart-stadia repurposing fuels IoT demand | +0.4% | Stadium districts in Doha, Al Rayyan, Al Wakrah | Short term (≤ 2 years) |

| Hyper-connected mega-projects pull enterprise data spend | +0.6% | Lusail Smart City, Hamad Port expansion | Medium term (2-4 years) |

| 3G shutdown reallocates low-band spectrum to LTE/5G | +0.3% | National | Short term (≤ 2 years) |

| Satellite backhaul extends rural and maritime coverage | +0.2% | Western and northern maritime zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Population-Wide Coverage Lifts Mobile Data ARPU

By 2024 operators reached 96% 5G population coverage, enabling premium unlimited-data tiers and network-slicing offers that raise blended ARPU levels above legacy 4G plans. Ooredoo rolled out Ericsson Mediation to support dynamic pricing and usage-based charging, while Vodafone partnered with Nokia to swap all 4G sites for 5G-ready gear. Speed tests show median 5G downlink rates exceeding 300 Mbps, which supports UHD streaming, cloud gaming, and enterprise VPNs. These service attributes justify price ladders up to QR 550 per month for top-tier plans. Monetization momentum continues as private 5G networks for logistics operators and oil and gas sites go live, cementing mobile broadband as the primary growth lever. [1]Ericsson, “Resilient Mega-Event Networks with Ooredoo Qatar,” ericsson.com

National Digital Agenda 2030 Targets Universal Fiber

The Digital Agenda commits to 90% end-to-end digitization of public services, driving fiber subscription penetration to 95% of households by 2025. State-backed Qatar National Broadband Network invested USD 550 million to blanket the country with GPON, guaranteeing a minimum of 100 Mbps symmetrical speeds.[2]QNBN, “Qatar National Broadband Network,” qnbn.qa Ooredoo’s successful Wi-Fi 7 trials on fiber-to-the-room gateways demonstrated four-fold throughput gains, preparing the access layer for 8K streaming and low-latency enterprise VR.

Post-World-Cup Smart-Stadia Repurposing Fuels IoT Demand

The 2022 FIFA World Cup generated a dense small-cell footprint, dimensioned for an average daily traffic of 2,800 TB at peak, which operators now repurpose for commercial IoT and private networks. Venue owners convert stadiums into multipurpose arenas, requiring CCTV analytics, crowd-flow sensors, and cashless retail, all of which rely on URLLC 5G slices. Operators bundle managed Wi-Fi, edge computing, and cybersecurity into turnkey offerings, unlocking incremental enterprise ARPU without the need for costly greenfield builds. The existing dark-fiber rings around stadium precincts shorten deployment cycles for adjacent smart-district projects.

Hyper-Connected Mega-Projects Pull Enterprise Data Spend

Lusail Smart City’s USD 60 million AI operating system contract with ST Engineering integrates traffic, utilities, and public safety data onto a unified edge cloud. Each subsystem requires low-latency, redundant links, which translates into multi-gigabit circuits sold on five-year terms. Hamad Port expansion adopts IoT yard management and automated crane control, requiring deterministic connectivity and local breakout facilities for real-time analytics. These mega-projects brand Qatar as a regional digital-infrastructure hub, drawing multinational tenants that sign enterprise VPN and SD-WAN agreements with both operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Near-170% mobile penetration caps subscriber growth | -0.8% | Nationwide | Long term (≥ 4 years) |

| High expatriate churn distorts subscriber base | -0.4% | Doha, industrial corridors | Medium term (2-4 years) |

| Regulatory ARPU caps limit pricing flexibility | -0.3% | National | Long term (≥ 4 years) |

| Supply-chain exposure to imported RAN equipment | -0.2% | National, heightened for new 5G rollouts | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Near-170% Mobile Penetration Caps Subscriber Growth

Subscriber counts have exceeded the population size since 2016, reaching a 170% SIM density by 2024, which means that organic additions contribute little to top-line growth. Dual-SIM ownership by expatriates inflates headline numbers, masking the stagnation in unique users. Operators respond with feature-rich bundles and loyalty rewards to increase revenue per account, but regulatory scrutiny on tariff transparency limits aggressive upselling tactics. Network utilization gains rather than subscriber expansion now drive investment business cases.[3]Ooredoo Qatar, “5G Data SIM Postpaid Plans,” ooredoo.qa

High Expatriate Churn Distorts Subscriber Base

Expatriates make up 85% of residents and turn over at an average 35% a year as construction cycles ebb and flow. Postpaid lines tied to employment visas cancel when workers leave, creating abrupt revenue lapses and spikes in SIM recycling costs. Number portability rules allow switching within days, so operators run retention campaigns with device-financing holidays and flexible exit clauses, actions that raise operating costs and dilute margin improvements from digital-channel migration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data Services Anchor Revenue Transformation

Data and Internet Services generated 47.20% of 2025 revenue and are forecast to grow at 3.00% CAGR, outperforming the overall Qatar telecom MNO market by 20 basis points. The segment benefits from 5G speed enhancements, cloud migration, and increased video streaming intensity, which raise the average monthly data usage per subscriber to 28 GB. Voice Services hold 17.65% as VoLTE substitution tempers the decline curve, while Messaging Services shrink as OTT alternatives dominate. IoT and M2M are recording the strongest growth, expanding at a 3.05% CAGR on a 5.85% base, as smart-meter deployments, fleet telematics, and e-health pilots multiply. By 2031, Data Services are expected to surpass USD 4.07 billion, accounting for 48.50% of Qatar's telecom MNO market size.

Subscribers choosing unlimited mobile-data packs pay 22% more than those on capped plans, sustaining a higher cash flow available for network densification. Fixed data bundles over fiber are increasingly sold with managed Wi-Fi, cybersecurity, and OTT-video add-ons, boosting average household revenue. The emerging wholesale Ethernet-over-fiber category caters to demand from hyperscale data center entrants seeking diverse routing to Europe and the Far East through AAE-1 and SEA-ME-WE 5 subsea systems. This adds high-margin backhaul traffic that further strengthens segment economics.

By End User: Enterprises Outpace Consumers

Enterprise accounts delivered 30.80% of 2025 turnover and are projected to grow at 3.18% CAGR, faster than the consumer book, thereby pushing their contribution toward one-third of the Qatar telecom MNO market by 2031. Growth stems from cloud connectivity, SD-WAN, and fully managed smart-building setups tied to stringent service-level agreements. Government ministries anchoring the Digital Agenda sign multi-year capacity contracts that lock in predictable cash flows. Consumer revenues rise at a slower 2.68% CAGR, reflecting price competition in unlimited-data tiers and slowing prepaid top-ups.

Operators cross-sell cybersecurity, colocation, and analytics over existing connectivity footprints, lifting enterprise ARPU to roughly 2.1 times consumer ARPU in 2025. Vodafone’s Microsoft Azure-stack hosting service and Ooredoo’s Google Cloud partnership showcase how bundles expand contract scope beyond pipes. The result is a broader solution portfolio that shields the Qatar telecom MNO market from the risks of voice and SMS commoditization.

Geography Analysis

Doha holds the lion’s share of revenue, buoyed by dense population clusters, the highest household incomes and the early adoption of premium 5G tiers. The capital’s smart-district initiatives, including Msheireb Downtown and Education City, create concentrated demand for edge nodes and NB-IoT sensors that operators monetize with higher-ARPU enterprise contracts. Lusail is emerging as the fastest-growing pocket, posting a 3.55% CAGR on the back of smart-city automation and upscale property developments that specify gigabit fiber as a basic utility.

Al Rayyan leverages stadium-convergence infrastructure, now converted into mixed-use event venues, to anchor digital-signage networks and venue-analytics platforms. The coastal Al Wakrah industrial corridor benefits from port expansion projects that deploy private 5G for crane automation and yard management. Rural areas covering the northern peninsula and western maritime zones rely on satellite backhaul and FWA to fill the fiber gap, adding incremental subscribers without extensive trenching.

The 2025 national broadband audit confirms that every municipality enjoys at least 95% household fiber coverage, positioning the Qatar telecom MNO market share for fixed broadband above 45.80% of total revenue by 2031. Seasonal expatriate inflows linked to construction peaks temporarily swell SIM activations in Al Khor and Dukhan, underscoring why operators use agile e-KYC digital onboarding to process short-cycle accounts efficiently.

Competitive Landscape

The Qatar telecom MNO market is a tightly regulated duopoly. Ooredoo leveraged first-mover status in 5G to market premium ARPU bundles and enterprise SD-WAN but saw 2024 revenue contract 8.5% as consumer ARPU slid under competitive pressures. Vodafone narrowed the performance gap after its nationwide network-modernization agreement with Nokia, raising average downlink speeds 40% year on year. Both incumbents focus on enterprise verticals-oil and gas, banking, logistics-to diversify revenue while consumer tariffs remain under regulatory scrutiny.

Strategic moves include Ooredoo’s adoption of Ericsson’s mediation layer for AI-driven charging models and Vodafone’s launch of a cloud security suite in concert with Microsoft to differentiate beyond connectivity. Wholesale alliances on submarine-cable consortia guarantee cost-effective international bandwidth that supports hyperscaler edge nodes in Doha. Satellite newcomer Starlink Qatar secured a service license for maritime coverage but is unlikely to erode the core urban revenue base given spectrum rules that favor terrestrial incumbents.

Regulatory oversight centers on accounting separation, cost-oriented interconnect and quality-of-service benchmarks, safeguarding consumer interests while ensuring a fair return on capital invested in next-generation networks. The duopoly structure, together with high entry barriers, sustains the Qatar telecom MNO market’s cash-generation profile, yet leaves little room for complacency as enterprise demands evolve.

Qatar Telecom MNO Industry Leaders

Ooredoo Group

Vodafone Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Qatar signed a five-year pact with Scale AI to deploy 50+ AI applications across public services.

- February 2025: Ooredoo integrated Ericsson Mediation for flexible 5G monetization.

- January 2025: ST Engineering won a USD 60 million deal to build Lusail’s AI smart-city platform.

- December 2024: The Ministry of Communications selected 25 start-ups for the TASMU Accelerator.

Qatar Telecom MNO Market Report Scope

Telecom, or telecommunication, refers to the exchange of information over substantial distances by electronic means, encompassing all types of voice, data, and video transmission. It encompasses various information-transmitting technologies and communication infrastructures, including wired phones, mobile devices, cell phones, microwave communications, fiber optics, satellites, radio and television broadcasting, and the internet.

The Qatar Telecom MNO Market Report is Segmented by Service Type (Voice Services, Data and Internet Services, Messaging Services, IoT and M2M Services, OTT and PayTV Services, and Other Services), End User (Enterprises, Consumers). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Subscribers).

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming And International Services, Enterprise And Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the Qatar telecom market in 2026 and how fast is it growing?

It stands at USD 7.32 billion in 2026 and is tracking a 2.8% CAGR toward 2031, driven mainly by data-service monetization and enterprise digital-transformation contracts.

Which service line contributes the most revenue?

Data and Internet Services generate nearly half of 2025 turnover thanks to wide 5G and fiber footprints that support high-usage applications.

Why are enterprises growing faster than consumers?

Digital Agenda 2030 mandates cloud and AI adoption in both public and private sectors, leading enterprises to sign multi-year, high-value connectivity and managed-service deals.

What impact will the 3G shutdown have?

It frees low-band spectrum for faster LTE and 5G, improving capacity and lowering the cost per bit, which should lift ARPU in the medium term.

Page last updated on: