Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

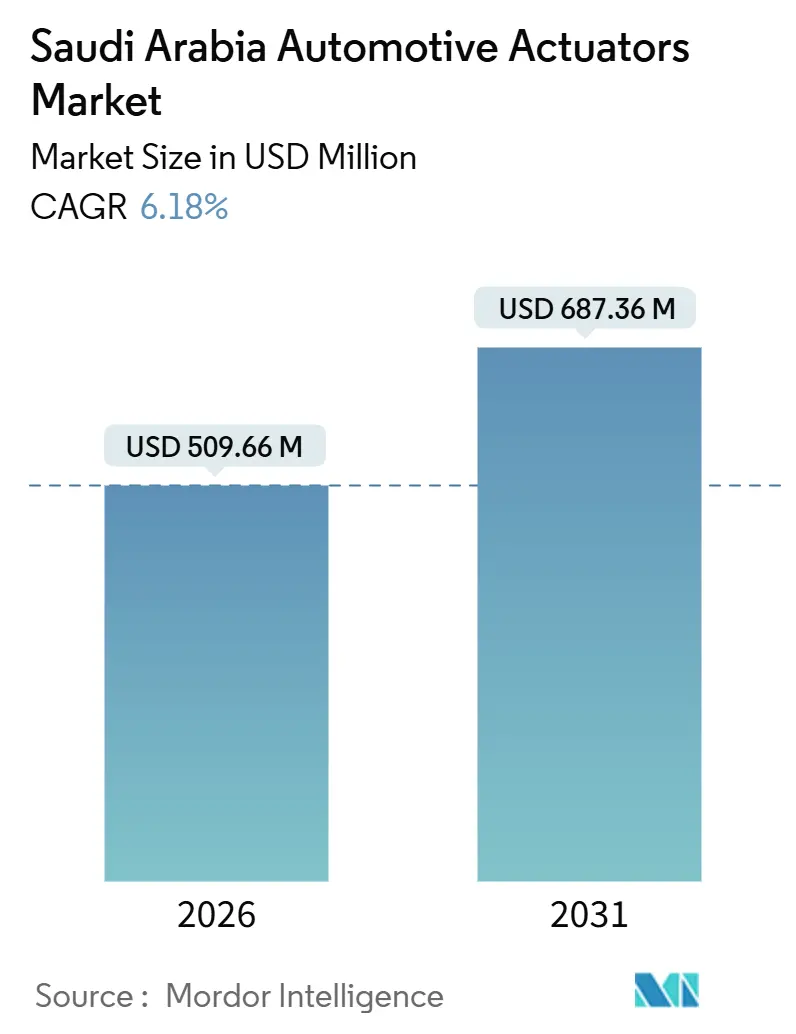

| Market Size (2026) | USD 509.66 Million |

| Market Size (2031) | USD 687.36 Million |

| Growth Rate (2026 - 2031) | 6.18% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Saudi Arabia Automotive Actuators Market Analysis by Mordor Intelligence

The Saudi Arabia automotive actuators market size stood at USD 509.66 million in 2026 and is projected to reach USD 687.36 million by 2031, reflecting a 6.18% CAGR. This trajectory positions the Saudi Arabian automotive actuators market as a pivotal enabler of the Kingdom’s dual objectives: stricter CAFE standards that tighten by about 4% every year and Vision 2030’s goal to localize 40% of the automotive value chain. Propulsion electrification accelerates actuator demand because every battery-electric vehicle (BEV) needs 30-40% more actuators than a comparable internal-combustion-engine (ICE) platform.

Key Report Takeaways

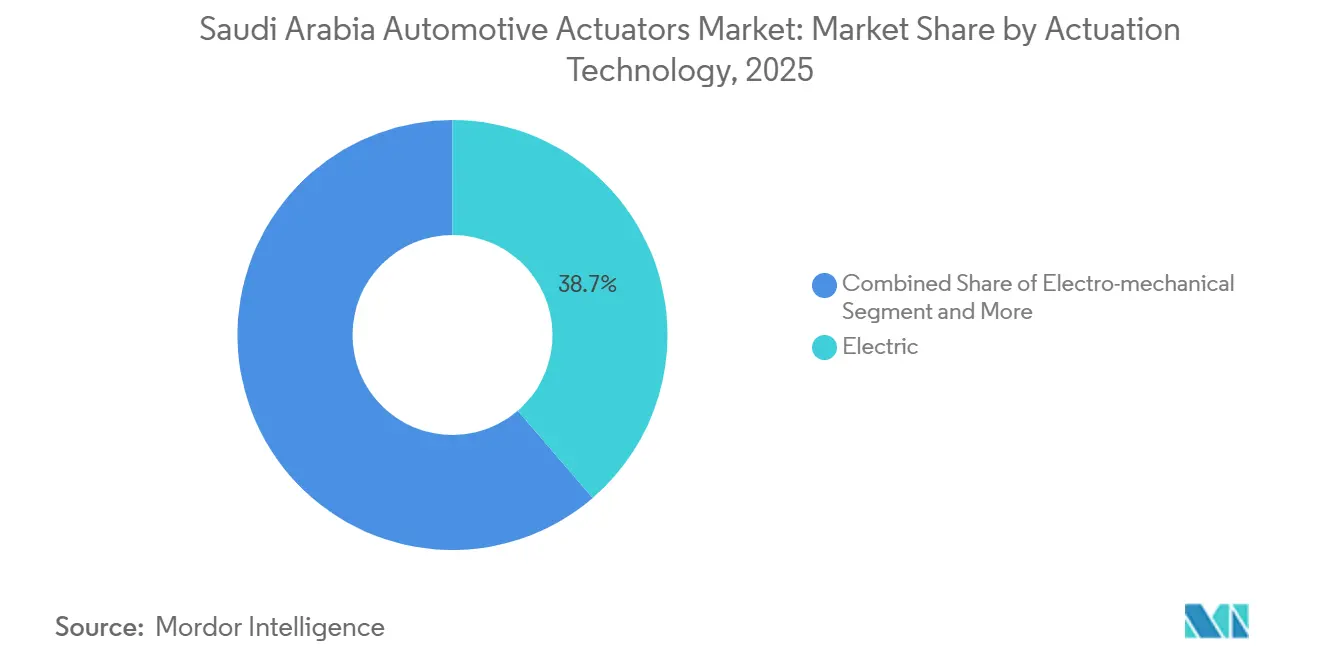

- By actuation technology, electric solutions dominated with 38.67% Saudi Arabia automotive actuators market share in 2025, while piezoelectric types posted the fastest 12.83% CAGR through 2031.

- By motion type, linear actuators led with a 64.92% slice of the Saudi Arabia automotive actuators market size in 2025; rotary actuators are projected to expand at a 9.26% CAGR to 2031.

- By application, throttle devices commanded 22.58% of the Saudi Arabian automotive actuators market share in 2025, whereas brake actuators are set to grow at a 9.94% CAGR.

- By propulsion, ICE vehicles still generated 51.74% of the 2025 value, but BEV applications will surge at a 14.68% CAGR.

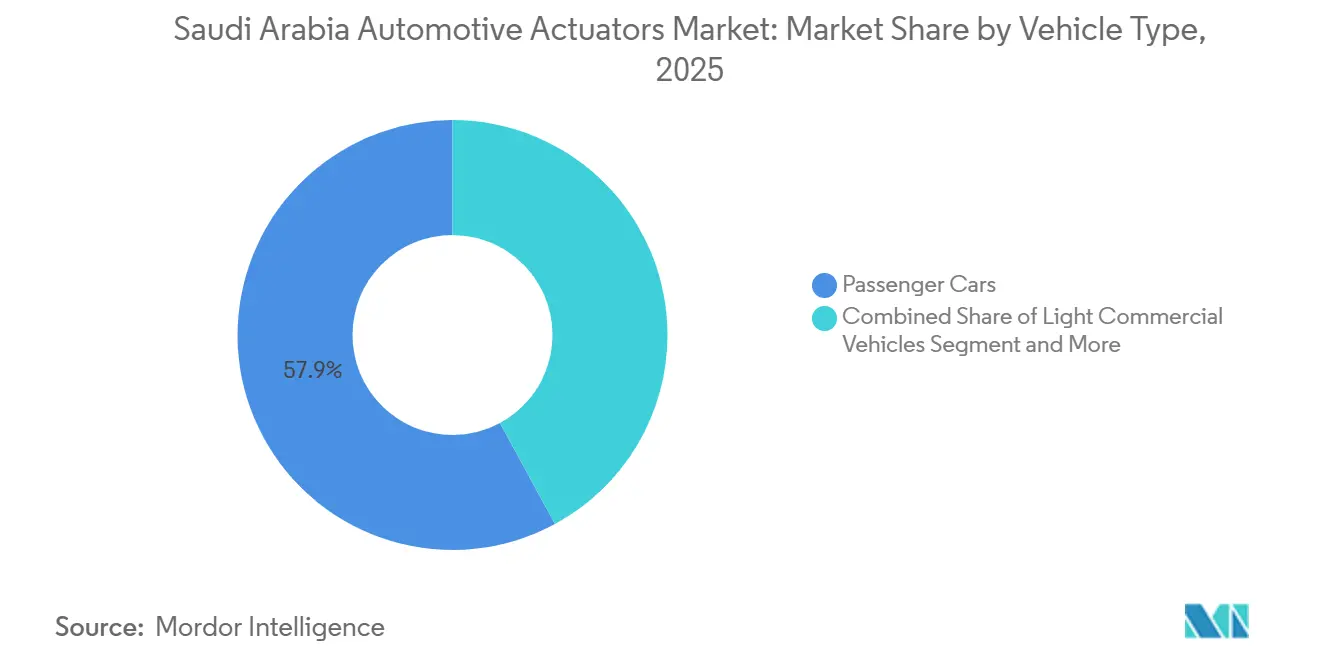

- By vehicle type, passenger cars retained 57.93% revenue in 2025, yet medium and heavy commercial fleets will surge at the highest 8.41% CAGR.

- By sales channel, OEMs accounted for 86.47% of 2025 shipments, although aftermarket revenues are poised to demonstrate 11.42% CAGR as inspections and e-commerce uptake spur replacements.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Automotive Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Advanced Safety Features | +2.2% | Saudi Arabia, spillover to GCC | Medium term (2-4 years) |

| Surge in Vehicle Electrification | +2.1% | KAEC, Jeddah, Riyadh | Long term (≥ 4 years) |

| Stricter Emission Targets | +0.9% | National | Short term (≤ 2 years) |

| OEM Local-Content Mandates | +0.8% | King Salman Automotive Cluster | Medium term (2-4 years) |

| Retrofit Demand from Giga-Projects | +0.6% | NEOM, Oxagon, Qiddiya | Long term (≥ 4 years) |

| OTA-Calibrated Software-Defined Actuators Cut Downtime | +0.5% | Riyadh, Jeddah premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Advanced Safety and Comfort Features

Saudi consumers pivot toward active-safety technology as the nation’s 2024 road-fatality rate of 12.13 per 100,000[1]Harry Stuckler, "The Ministry of Interior released the 2024 Annual Traffic Safety Report," KSA News, ksa.com. remains one of the highest in the G20. Brake actuators supporting automatic emergency braking and adaptive cruise control now appear in mainstream trims after Hyundai’s PIF joint venture confirmed Level 2 ADAS will be standard across 50,000 units annually from 2025. Comfort is equally decisive; 68% of new-vehicle sales in 2025 were mid-size SUVs and full-size sedans, both averaging 25-30 actuators per vehicle versus 15-18 in compact hatchbacks. ISO 26262 ASIL-D redundancy further lifts actuator counts by mandating dual brake devices per car. Together, safety and comfort embed a structural floor beneath actuator demand even while overall light-vehicle sales rise only 3-4% a year.

Surge in Vehicle Electrification and EV Production

Lucid’s Saudi Arabia facility in King Abdullah Economic City (KAEC) exists and began operations assembling Lucid Air vehicles from semi-knockdown (SKD) kits, but its annual capacity is around 5,000 units per year in the initial phase[2]"Lucid Group Makes History in Saudi Arabia as it Opens Country's First-Ever Car Manufacturing Facility," LUCID, ir.lucidmotors.com.. With the Public Investment Fund committing to buy 50,000 Lucid vehicles over ten years and CEER budgeting USD 1.3 billion to commission a 150,000-unit BEV plant, the Saudi Arabian automotive actuators market will see actuator intensity peak between 2026 and 2028. Yet solid-state batteries arriving post-2028 could cut cooling-loop actuators by 25-30% per BEV. Local battery capacity targets of 15 GWh by 2028 and a USD 800 million lithium-hydroxide facility in Yanbu favor co-located actuator assembly to secure LCGPA’s 10-20% price preference.

Stricter Saudi CAFE and Emission Targets

Regulatory compliance under SASO 2864:2022 requires importers and manufacturers of light-duty vehicles in Saudi Arabia to meet progressively stricter fuel-economy standards through 2028[3]"List of GSO Technical Regulations for Motor Vehicles," GCC Standardization Organization (GSO), gso.org.sa.. Penalties of SAR 5,000 per kilometer-per-liter shortfall for high-volume OEMs incentivize over-specification of actuators even if consumer willingness to pay lags. Real-world driving-emission testing introduced in 2025 under 45-50 °C summer conditions already boosted validation budgets at Continental and ZF by around 12%.

OEM Local-Content Mandates Driving Actuator Localization

The Local Content and Government Procurement Authority targets 40% domestic value by 2030 and weights local sourcing at 40% in bid evaluations, pressing tier-ones to open regional plants or risk market exit. Bosch responded with a Middle East competence center that localizes software and final assembly, while Denso feeds KAEC modules from its USD 300 million Thailand plant to qualify for content credit without duplicating capital-heavy motor-winding lines. Yet only three of the twenty profiled suppliers had committed manufacturing footprints by early 2026, reflecting uncertainty over whether domestic production would reach the 300,000-unit goal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High BOM Cost of Next-Gen Smart Actuators | -0.7% | Saudi Arabia | Short term (≤ 2 years) |

| Reliability Issues in Extreme Desert Duty-Cycles | -0.5% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Solid-State E-Drivetrains Lowering Actuator Counts | -0.4% | Premium BEV segment | Long term (≥ 4 years) |

| Rare-Earth Magnet Supply-Chain Volatility | -0.3% | Saudi Arabia, Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High BOM Cost of Next-Gen Smart Actuators

Smart actuators integrating sensors and controllers carry a 30-50% premium; Bosch’s 2025 line averages EUR 50-150 versus EUR 30-80 for legacy units. With 62% of 2025 light-vehicle sales below SAR 100,000, OEMs struggle to absorb the cost delta. ISO 26262 validation adds up to two years, and cybersecurity mandates under UNECE R155 require secure boot and encrypted OTA channels, restricting price relief. Continental’s integrated brake control enters luxury BEVs at a 40% premium, illustrating affordability barriers in mass segments.

Reliability Issues in Extreme Desert Duty-Cycles

Summer ambient temperatures of 45-50 °C push under-hood peaks past 120 °C, doubling actuator failure rates relative to temperate climates. Thermal cycling accelerates backlash in gear trains and dust ingress degrades brushless motors; ZF’s 2025 Riyadh field study recorded 22% HVAC-actuator failure within 36 months, twice the global average. Mitigation such as conformal coatings and high-temperature lubricants adds USD 8-12 per actuator, squeezing margins in entry trims. Extended warranties introduced by SASO in 2024 transfer liability upstream, pressuring suppliers to over-specify thermal derating.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Actuation Technology: Piezoelectric Gains on Precision Needs

Electric systems accounted for 38.67% of 2025 revenue, as brushless DC motors balance torque density with 10,000-hour lifespans in roles such as seats, mirrors, and HVAC systems. Hydraulic brake actuators are expected to hold a single-digit share as brake-by-wire layouts proliferate. At the same time, pneumatic solutions continue to persist in medium and heavy trucks for ABS-ready air-brake modulation. Piezoelectric devices, forecast at 12.83% CAGR, satisfy microsecond valve control in gasoline direct-injection engines and 800 V battery thermal loops. The Saudi Arabia automotive actuators market size for piezoelectric types is projected to expand with a CAGR of 12.83% by 2031, cementing their status despite dependence on lead-zirconate-titanate ceramics. Shape-memory-alloy concepts remain niche because 60-90 °C activation temperatures overlap with the under-hood heat in Saudi Arabia, demanding cooling hardware that offsets weight savings.

Second-order effects include Bosch allocating 8% of its EUR 1.4 billion annual actuator R&D to piezoelectric and SMA technologies, protecting future earnings should solid-state battery packs shrink electric-motor demand. Meanwhile, suppliers like Valeo use Morocco plants for cost-optimized 48 V HVAC actuators, reserving French lines for high-margin 800 V piezoelectric units, creating a bifurcated supply chain poised to converge only if BEV uptake meets Vision 2030 targets.

By Motion Type: Rotary Demand Climbs in Multi-Axis HVAC

Linear units held a 64.92% market share in 2025 shipments, driven by dominance in throttle, brake, and seat applications. Yet, rotary actuators, projected to grow at a 9.26% CAGR through 2031, benefit from tri-zone HVAC systems that utilize up to eight blend doors to manage 45°C desert heat. The Saudi Arabia automotive actuators market size attached to rotary devices is poised to surpass USD 220 million by 2031. ZF’s universal actuator platform merges linear and rotary stages on a common motor-controller, cutting SKUs by 40% and aligning with LCGPA’s push for regional assembly. Competition intensifies as Nidec and Johnson Electric price integrated motor-sensor modules 20% cheaper than CTS stand-alone sensors, pressuring mid-tier specialists.

Within HVAC, Valeo’s 2024 system for the Lucid Air leverages rotary motion to lower cold-start energy by 18%, directly extending BEV range in high-temperature urban cycles. Adoption accelerates alongside digital mirror laws across the GCC, which require real-time camera repositioning actuators.

By Application Type: Brake Devices Accelerate on Safety Push

Throttle actuators retained a 22.58% market share in 2025 but are expected to decline as BEV penetration increases. Brake units are advancing at a 9.94% CAGR, supported by UNECE R13-H electronic brake distribution and energy-recovery mandates that demand redundancy. Continental’s integrated brake control adds USD 180 per vehicle yet doubles pad life through wear optimization, illustrating the cost-benefit calculation for ADAS-ready platforms. HVAC and thermal actuators account for 15% of volume but risk a 37% drop per vehicle if solid-state batteries remove liquid cooling hardware by 2029.

Seat-adjustment devices, steady at 12% share, confront price compression—average unit prices fell from SAR 420 to SAR 310 between 2020 and 2025. Door, closure, and active-aero actuators collectively grow in mid-single digits as SUVs drive demand for power liftgates and grille shutters, each improving highway fuel economy by 2-3%.

By Vehicle Propulsion: BEV Intensity Defines Upside

ICE platforms still generated the most 2025 revenues, with a 51.74% market share; however, the Saudi Arabia automotive actuators market size tied to BEVs is expected to surge at a 14.68% CAGR. Each Lucid Air carries 38 actuators, compared to 24 in a hybrid and 18 in a contemporary ICE sedan, thereby increasing the per-unit value. Plug-in hybrids struggle with the complexity of dual drivetrains, while fuel-cell trucks remain experimental, despite NEOM’s USD 5 billion green-hydrogen initiative.

Supply bifurcates: Denso, Bosch, and Valeo emphasize high-volume ICE and hybrid orders, whereas Continental and ZF target low-volume, high-margin BEV smart actuators. Managing R&D parity across both tiers poses a challenge to EBIT targets, especially for mid-cap players.

By Vehicle Type: Commercial Fleets Outpace Passenger Growth

Passenger cars held 57.93% of the 2025 turnover. Medium and heavy commercial fleets exhibit the highest 8.41% CAGR as e-commerce giants Noon and Jarir electrify their last-mile vans to meet the Green Riyadh mandates. Each electric light commercial vehicle carries 22-26 actuators, including load-leveling suspension and telematics-enabled locks, compared with 15-18 in diesel equivalents. Medium and heavy trucks gain market share through NEOM autonomous logistics, utilizing redundant actuators that meet ISO 26262 ASIL-D standards.

ZF’s 2026 modular chassis, which shares 70% of its parts across vehicle classes, supports local assembly economics, crucial for suppliers balancing low-volume, heavy-duty orders with those of passenger cars.

By Sales Channel: Aftermarket Expands on Retrofits

OEM shipments represented 86.47% of 2025 units, while the aftermarket segment is poised to rise at 11.42% CAGR as the seven-year average vehicle age aligns with peak actuator failure. Fahes safety inspections identify inoperable HVAC dampers and mirror folding units, while Jarir and Noon compress price gaps, siphoning share from dealer networks. SASO’s 2026 QR-code traceability combats a 12-15% counterfeit share yet raises compliance costs that small distributors struggle to meet.

Retrofits tied to giga-projects create a lucrative sub-segment: Valeo’s eight-actuator HVAC kit enables diesel bus upgrades to comply with low-emission zones at one-third OEM cost, highlighting price-value arbitrage in fleet conversions.

Geography Analysis

Riyadh, Makkah, and the Eastern Province concentrated 74% of 2025 demand, mapping the Kingdom’s population nodes and assembly hubs in KAEC and Jeddah. Riyadh alone targets 30% EV penetration by 2030 under the Green Riyadh plan, stimulating brake-by-wire and thermal-management actuator orders for last-mile fleets. The Eastern Province’s oil fleet—12,000 vehicles—requires IP68-rated devices capable of 120 °C under-hood operation; Saudi Aramco tendered 2,400 electric SUVs in 2024 with such specifications.

NEOM contributes less than 2% of present sales yet sets strategic direction. Its 100% electric, autonomous mobility mandate across THE LINE will need up to 2 million actuators by 2030, many with safety integrity levels exceeding current passenger-car norms. Oxagon’s tax-free industrial zone priced at SAR 10 per square meter lures Valeo and Schaeffler to contemplate regional assembly, but capital commitments hinge on Hyundai and CEER delivering on volume promises. The geography, therefore, splits into mature metros with established aftermarket ecosystems and giga-projects offering greenfield upside but schedule risk.

Standardization under the GCC umbrella aligns local rules with UNECE, lowering technical hurdles for Turkish and Indian entrants. Mako Elektrik and Minda Corporation opened Saudi sales offices in 2025, bringing price competition that threatens incumbent margins.

Competitive Landscape

The largest suppliers, Bosch, Denso, Continental, and ZF, held a significant share of the 2025 shipment value. Localization mandates, however, spur fragmentation as regional assemblers emerge. Bosch’s asset-light competence center focuses on calibration and final assembly; Denso ships sub-assemblies from Thailand to KAEC; Continental opened a Dubai service hub to support in-region OTA updates. White-space lies in retrofit actuators for 12 million vehicles on Saudi roads, IP69K-rated devices for NEOM’s autonomous fleets, and piezoelectric fuel-injection modules underserved by electromotor-centric suppliers.

Technology differentiates winners. Continental’s 2024 patent for wear-sensing brake-by-wire actuators doubles service intervals, shifting revenue toward uptime guarantees. ZF earmarked USD 14 billion through 2028 for actuator intelligence, embedding machine-learning fault prediction into hardware. Yet cybersecurity compliance under UNECE R155 adds USD 12-18 per smart actuator—an expense smaller firms like CTS and Sensata struggle to absorb, threatening consolidation via regulatory cost pressure.

SASO’s QR-code traceability requirement from January 2026 further favors scale players who can amortize labeling and database costs. Nevertheless, Chinese disruptors Inovance and Leadrive captured 8% of the 2025 LCV aftermarket by pricing 25-30% below incumbents—evidence that cost leadership can still carve share despite regulatory headwinds.

Saudi Arabia Automotive Actuators Industry Leaders

-

Robert Bosch GmbH

-

Denso Corporation

-

Nidec Corporation

-

Aptiv

-

Mitsubishi Electric Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Saudi Arabia, in a significant move towards local automotive production, inked a memorandum of understanding with Stellantis and Petromin Corporation. The agreement aims to delve into the feasibility of establishing a full vehicle manufacturing plant within the Kingdom.

- April 2025: Industry experts at Automechanika Riyadh 2025 underscored nanotechnology's promise to revolutionize the Saudi automotive aftermarket. This innovation not only enhances vehicle durability and part performance but also signals a shift in actuator materials and efficiency in future designs, particularly for high-performance and challenging environments.

Saudi Arabia Automotive Actuators Market Report Scope

Automotive actuators are mechanical or electrical devices used in vehicles to control various functions and systems. These actuators convert electrical or manual signals into physical actions, allowing for precise control over functions like engine performance, emissions, steering, braking, and HVAC (Heating, Ventilation, and Air Conditioning).

Saudi Arabia automotive actuators market is segmented by vehicle type, actuator type, and application type. By vehicle type, the market is bifurcated into passenger cars and commercial vehicles. By actuator type, the market is segmented into electrical actuators, hydraulic actuators, and pneumatic actuators. By application type, the market is segmented into throttle actuators, seat adjustment actuators, brake actuators, closure actuators, and other application types. The report offers market size and forecasts for the Saudi Arabia automotive actuators in value (USD) for all the above segments.

By Actuation Technology

| Electric |

| Electro-mechanical |

| Piezoelectric |

| Others |

By Motion Type

| Linear |

| Rotary |

By Application Type

| Throttle |

| Brake |

| Transmission/Drivetrain |

| Seat Adjustment |

| Door/Closure |

| HVAC and Thermal |

| Suspension and Chassis |

| Mirror and Lighting |

By Vehicle Propulsion

| Internal-Combustion (ICE) |

| Hybrid Electric (HEV) |

| Battery-Electric (BEV) |

| Plug-in Hybrid (PHEV) |

| Fuel-Cell Electric (FCEV) |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Highway and Special-Purpose |

By Sales Channel

| OEM |

| Aftermarket |

| By Actuation Technology | Electric |

| Electro-mechanical | |

| Piezoelectric | |

| Others | |

| By Motion Type | Linear |

| Rotary | |

| By Application Type | Throttle |

| Brake | |

| Transmission/Drivetrain | |

| Seat Adjustment | |

| Door/Closure | |

| HVAC and Thermal | |

| Suspension and Chassis | |

| Mirror and Lighting | |

| By Vehicle Propulsion | Internal-Combustion (ICE) |

| Hybrid Electric (HEV) | |

| Battery-Electric (BEV) | |

| Plug-in Hybrid (PHEV) | |

| Fuel-Cell Electric (FCEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| Off-Highway and Special-Purpose | |

| By Sales Channel | OEM |

| Aftermarket |

Key Questions Answered in the Report

How fast is actuator demand growing in Saudi vehicles?

The Saudi Arabia automotive actuators market is forecast to post a 6.18% CAGR from 2026 to 2031, outpacing overall vehicle sales due to electrification and ADAS uptake.

Which actuator type will expand the quickest?

Piezoelectric devices are set for a 12.83% CAGR through 2031 as gasoline direct-injection and 800 V battery platforms require microsecond valve control.

How many actuators does a typical BEV in the Kingdom use?

A Lucid Air assembled at KAEC integrates about 38 actuators, roughly 30-40% more than a comparable ICE sedan.

What drives aftermarket growth for actuators?

Mandatory inspections, a seven-year average vehicle age, and e-commerce price transparency lift aftermarket sales at an 11.42% CAGR through 2031.

How do local-content rules affect suppliers?

LCGPA’s 40% domestic-value target forces tier-ones to establish regional assembly or risk penalties, fragmenting supply chains and shifting some production to KAEC and Oxagon.

Page last updated on: