United Kingdom Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

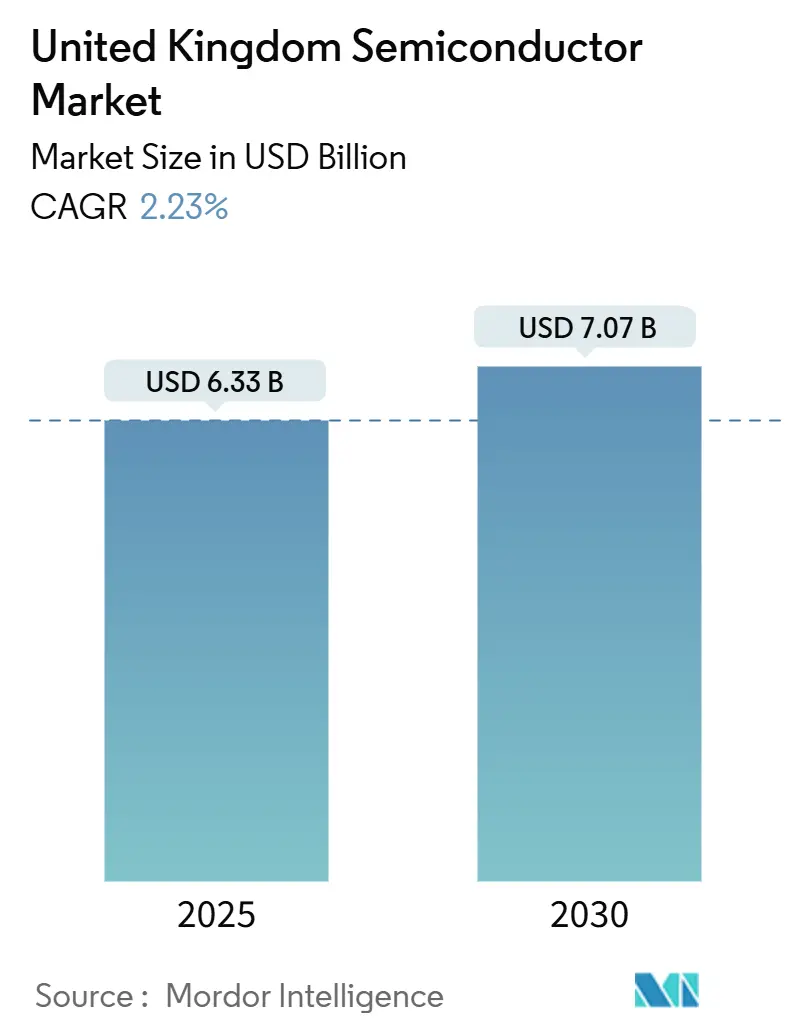

| Market Size (2025) | USD 6.33 Billion |

| Market Size (2030) | USD 7.07 Billion |

| Growth Rate (2025 - 2030) | 2.23% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Semiconductor Market Analysis by Mordor Intelligence

The United Kingdom semiconductor market size is valued at USD 6.33 billion in 2025 and is forecast to reach USD 7.07 billion by 2030, expanding at a 2.23% CAGR during the period. Maturing domestic demand, steady design-IP royalties, and a widening base of compound-semiconductor production position the country as a pivotal design and specialty-manufacturing hub within Europe.[1]Department for Science, Innovation and Technology, “UK Semiconductor Workforce Study: Executive Summary,” GOV.UK Government funding, private expansion projects, and rising device content in electric vehicles, 5G infrastructure, and AI data centers underpin revenue growth. Policy incentives embedded in the GBP 1 billion National Semiconductor Strategy attract anchor investors such as Vishay Intertechnology, while EU Chips Joint Undertaking access broadens collaborative R&D pathways. Persistent supply-chain tightness and engineering-talent gaps temper growth, yet long-term opportunities in silicon-carbide (SiC), gallium-nitride (GaN), and photonics sustain the United Kingdom semiconductor market’s competitive edge. Cost-curbing measures on industrial electricity starting in 2026 are expected to improve fabrication economics for energy-intensive processes.

Key Report Takeaways

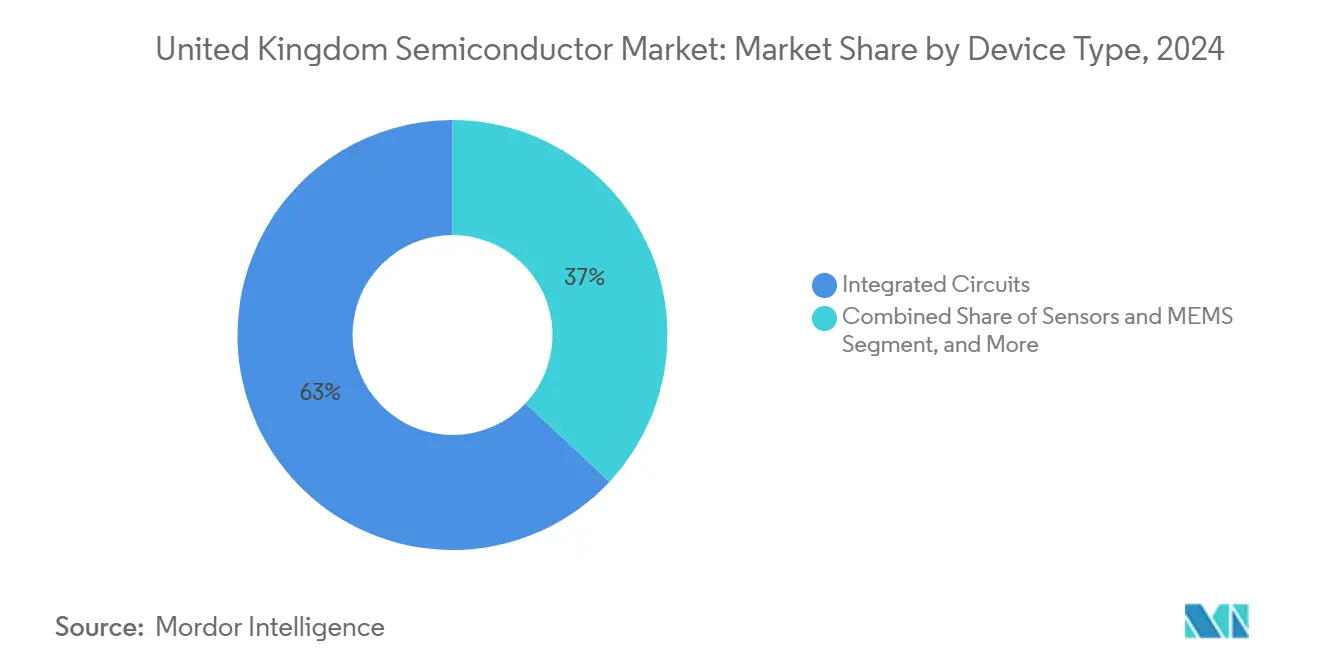

- By device type, Integrated Circuits held 63.04% of United Kingdom semiconductor market share in 2024; Sensors and MEMS recorded the fastest 3.11% CAGR through 2030.

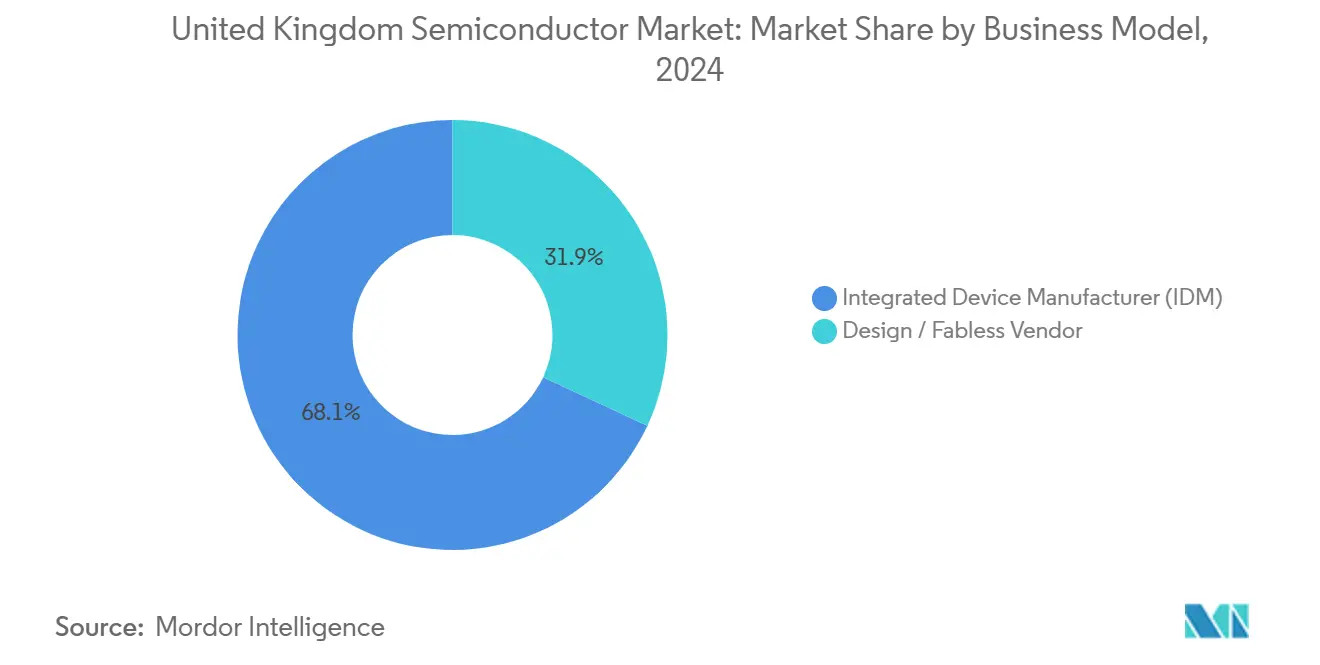

- By business model, IDMs accounted for 68.07% share of the United Kingdom semiconductor market size in 2024, whereas design/fabless vendors are projected to advance at a 3.20% CAGR during 2025-2030.

- By end-user industry, automotive led with 29.25% revenue share in 2024, while AI applications post the steepest 3.82% CAGR outlook to 2030.

United Kingdom Semiconductor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for automotive electrification | +0.80% | UK-wide, concentrated in Midlands automotive corridor | Medium term (2-4 years) |

| Rapid 5G and edge-computing deployment | +0.60% | National, with early gains in London, Manchester, Edinburgh | Short term (≤ 2 years) |

| UK£1 billion national semiconductor strategy funding | +0.40% | National, with focus on Newport, Cambridge, Bristol clusters | Long term (≥ 4 years) |

| Compound-semiconductor cluster momentum (Newport, Cambridge) | +0.30% | Regional, South Wales and Cambridge ecosystems | Medium term (2-4 years) |

| Photonics and quantum-chip R&D acceleration | +0.20% | National, concentrated in university research hubs | Long term (≥ 4 years) |

| Flexible electronics "fab-in-a-box" roll-outs | +0.10% | National, with manufacturing focus in Durham, Cambridge | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Automotive Electrification

SiC and GaN power devices are displacing legacy silicon components in traction inverters, on-board chargers, and DC-DC converters, driving material demand across the Midlands vehicle corridor. Vishay’s GBP 250 million expansion in Newport earmarks SiC wafers for European EV platforms.[2]Evertiq Staff, “Vishay to Make $320M Investment in UK’s Largest Chip Factory,” EVERTIQ.COM Semiconductor content per vehicle is progressing from USD 250 in ICE models toward USD 2,000 in high-voltage EV and ADAS-rich architectures, lifting discrete power, sensor, and MCU volumes. UK specialists such as Transense Technologies integrate surface-acoustic-wave sensing into 800 V drivetrain controls under a GBP 11 million R&D program. Compound-semiconductor proficiency gives domestic fabs an edge in meeting automotive thermal and reliability thresholds. The rise of centralized E/E architectures further accelerates adoption of chiplet-based power-domain controllers, reinforcing long-range demand for the United Kingdom semiconductor market.

Rapid 5G and Edge-Computing Deployment

Nationwide 5G densification and emerging edge-cloud nodes require high-frequency RF amplifiers, beam-forming ICs, and AI inference accelerators. The UK secured eligibility under the EUR 1.3 billion Chips Joint Undertaking to co-fund RISC-V and automotive RF projects. University of Bristol scientists reported GaN SLCFET breakthroughs exceeding 1,000 fins at sub-100 nm widths, underpinning 6G radio prototypes. IQE supplies 55% of global epitaxial wafers for 5G base stations, leveraging its Newport line for high-mobility GaN layers. Edge AI requirements for low-latency vision and speech workloads create design slots for UK fabless houses, while the telecom diversification strategy reduces dependency on single-vendor RAN chipsets, enlarging addressable revenues for the United Kingdom semiconductor market.

UK GBP 1 Billion National Semiconductor Strategy Funding

The 20-year plan channels GBP 1 billion into design leadership, compound-semiconductor scale-up, and supply-chain resilience. A dedicated UK Semiconductor Institute coordinates academia and industry through GBP 200 million seed allocations for 2023-2025 infrastructure. Cardiff University’s GBP 99 million hub advances low-power optoelectronics for quantum computing and 6G. ChipStart has triggered GBP 40 million private investment for startup cohorts, while the UK-Japan bilateral program adds GBP 2 million in joint grants. Skills pipelines remain crucial as 39% of the semiconductor workforce approaches retirement; the Talent Expansion Programme injects GBP 35 million into chip-design curricula to safeguard the United Kingdom semiconductor market’s future labour base.

Compound-Semiconductor Cluster Momentum (Newport and Cambridge)

South Wales hosts Europe’s largest compound-semiconductor concentration. IQE’s Newport fab delivers GaAs, GaN, and SiC epitaxy for global handset, automotive, and photonics buyers, commanding 55% world share of outsourced compound-wafer supply. Welsh Government’s GBP 51 million stake in Newport Wafer Fab, now under Vishay’s expansion program, anchors end-to-end SiC power device capacity. Cambridge supplements with quantum-chip and photonics startups; Wave Photonics secured GBP 4.5 million to scale integrated-photonics libraries. Compound substrates outperform silicon in high-voltage switches, RF PAs, and LiDAR lasers, allowing the United Kingdom semiconductor market to specialize where silicon economics falter.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarce domestic wafer-fab capacity | -0.70% | National, particularly affecting volume production | Medium term (2-4 years) |

| Engineering-talent shortage post-Brexit | -0.50% | National, concentrated in London, Cambridge, Bristol tech hubs | Short term (≤ 2 years) |

| High UK industrial-energy costs | -0.40% | National, disproportionately affecting manufacturing operations | Short term (≤ 2 years) |

| Single-site compound-fab supply-risk | -0.20% | Regional, concentrated in South Wales cluster | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarce Domestic Wafer-Fab Capacity

Vishay’s Newport line processes 30,000 200 mm wafers per month—modest versus Asian mega plant output—leaving the United Kingdom semiconductor market dependent on overseas foundries for sub-28 nm logic. Coherent’s Newton Aycliffe GaAs fab purchase by the UK Government for GBP 20 million addresses sovereign supply for defense photonics, yet scale remains limited. Pragmatic’s distributed flexible lines partially mitigate risk, but leading-edge logic still requires external nodes, exposing design houses to geopolitical supply shocks.

Engineering-Talent Shortage Post-Brexit

Eighty percent of chip-design firms report vacancies; only 3,245 students pursued relevant degrees in 2024. The Semiconductor Workforce Study notes 39% of employees will retire within 15 years, shrinking experience pools. Visa barriers and global competition inflate hiring costs, while female participation sits at 26%. Although GBP 35 million in skills funding is approved, near-term design schedules continue to slip, reducing utilization rates in the United Kingdom semiconductor market.[3]Department for Business and Trade, “Huge Boost for UK Industry as Government Powers Ahead with Cuts to Electricity Costs,” GOV.UK

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Integrated Circuits Maintain Revenue Leadership

Integrated Circuits captured 63.04% of United Kingdom semiconductor market share in 2024, reflecting their ubiquity across automotive powertrains, mobile computing, and telecom infrastructure. Revenue stability derives from Arm-based CPU licensing, analog front ends, and microcontrollers built on 28 nm and above. Sensors and MEMS, though smaller, will post a 3.11% CAGR to 2030, buoyed by ADAS lidar, tire-pressure monitors, and industrial IoT nodes. Discrete SiC MOSFETs and GaN HEMTs remain mainstays in traction inverters, while optoelectronics gains from datacentre and 5G optical-link proliferation.

Emergent chiplet configurations let domestic design houses supply power-management, security, or RF tiles integrated into multi-die packages fabricated offshore. This modular trend aligns with the country’s design focus and reduces the capital-intensity barrier, reinforcing the United Kingdom semiconductor market size gains in value-add IP rather than wafer volume. Regulatory ISO 26262 obligations propel safety-certified MCU shipments, sharpening demand for verification services as well.

By Business Model: IDM Scale Meets Fabless Agility

IDMs controlled 68.07% of the United Kingdom semiconductor market size in 2024 through legacy captive fabs and vertically integrated sales channels. Yet design/fabless vendors will outpace them at 3.20% CAGR because they tap advanced overseas nodes without incurring depreciation drag. Over 110 UK-based design companies leverage this capital-light profile to spin AI, security, and RF SoCs, feeding TSMC and GlobalFoundries pipelines. Arm’s USD 3.2 billion royalty and license revenues illustrate the scalability of pure-IP models. Hybrid approaches such as Pragmatic’s flexible-electronics lines meld local manufacturing with fabless design, illustrating model diversification inside the United Kingdom semiconductor market.

Both structures benefit from the Chips Joint Undertaking, which subsidizes multi-project wafer shuttles for prototyping. The surge of automotive ASIC tenders encourages collaboration: EnSilica’s USD 20 million custom-chip award exemplifies fabless traction in safety-critical applications.

By End-User Industry: Automotive Dominates While AI Surges

Automotive maintained 29.25% share in 2024 as OEMs transition toward high-voltage EV platforms and shift to software-defined vehicles. Content gains span SiC traction modules, ADAS sensor arrays, and zonal domain controllers. AI workloads represent the fastest 3.82% CAGR, spanning data-center training accelerators, enterprise inference cards, and edge-vision processors. Arm-based AI cores slated for 2025 will deepen domestic design wins. Communication equipment benefits from OpenRAN deployments demanding programmable RF ICs and low latency backhaul switch silicon. Industrial automation drives intelligent-sensor demand, while consumer electronics remains stable but less dynamic within the United Kingdom semiconductor market.

Geography Analysis

South Wales delivered GBP 600 million semiconductor revenue in 2024, anchored by Newport Wafer Fab, IQE epitaxy, and SPTS etch-tool production.[4]Scotland Office, “Powering Britain’s Future,” GOV.UK Cambridge hosts quantum and photonics design clusters supported by deep-tech venture funds. Bristol pioneers GaN device and 6G RF research, leveraging University of Bristol labs. Scotland’s Edinburgh-Glasgow corridor secures GBP 2 billion in digital-tech funding, fuelling AI accelerator design programs. London concentrates financial, corporate, and legal functions enabling capital access for fabless startups, while Manchester and Newcastle specialize in industrial-power semiconductors. National Epitaxy Facility in Sheffield offers cross-cluster wafer services, strengthening UK-wide collaboration.

Inter-city rail and fibber links facilitate workforce mobility among hubs, enhancing knowledge spillovers critical for the United Kingdom semiconductor market. Proximity to continental Europe supports export logistics and joint EU R&D calls, while selective sovereign controls on defense-grade chips preserve security of supply.

Competitive Landscape

Arm Holdings retains global CPU IP leadership, licensing designs embedded in more than 99 billion chips to date, thus anchoring the United Kingdom semiconductor market. IQE dominates outsourced compound-semiconductor epitaxy, while Imagination Technologies competes in GPU IP for automotive HMI clusters. Pragmatic Semiconductor differentiates through low-cost flexible IC production, targeting brand-owner NFC tags. Graphcore’s acquisition by SoftBank for USD 500 million underscores consolidation pressures in AI accelerators yet injects new capital for road-map continuation.

Strategic moves center on capacity expansion, IP portfolio broadening, and vertical alignment with growth verticals:

Vishay allocated GBP 250 million to scale SiC modules in Newport, securing EV and renewable contracts.

SPTS invested GBP 81 million in a Newport HQ to expand etch-equipment capacity and local hiring.

onsemi absorbed Qorvo’s SiC JFET assets for USD 115 million, sharpening its power-device breadth within UK distribution channels.

Patent densification and standards-body participation remain key competitive levers, with UK entities actively contributing to ISO-and IEEE working groups on automotive safety, 5G, and quantum communication.

United Kingdom Semiconductor Industry Leaders

Arm Ltd.

IQE plc

Nexperia Newport Ltd.

Graphcore Ltd.

Pragmatic Semiconductor Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: PsiQuantum opened an R&D center at Daresbury Laboratory with GBP 9 million government support for cryogenic quantum systems.

- March 2025: Vishay Intertechnology committed GBP 250 million to the Newport facility to manufacture advanced SiC semiconductors for EVs, creating 500 jobs.

- January 2025: onsemi completed acquisition of Qorvo’s SiC JFET business for USD 115 million, expanding its power portfolio for AI data centers.

- July 2024: SoftBank Group acquired Graphcore for USD 500 million, ensuring continued development of UK-based AI accelerators.

United Kingdom Semiconductor Market Report Scope

| Discrete Semiconductors | Diodes | ||

| Transistors | |||

| Power Transistors | |||

| Rectifier and Thyristor | |||

| Other Discrete Devices | |||

| Optoelectronics | LEDs | ||

| Laser Diodes | |||

| Image Sensors | |||

| Optocouplers | |||

| Other Device Types | |||

| Sensors and MEMS | Pressure | ||

| Magnetic Field | |||

| Actuators | |||

| Acceleration and Yaw Rate | |||

| Temperature and Others | |||

| Integrated Circuits | By Integrated Circuit Type | Analog | |

| Micro | Microprocessors (MPU) | ||

| Microcontrollers (MCU) | |||

| Digital Signal Processors | |||

| Logic | |||

| Memory | |||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | ||

| 3nm | |||

| 5nm | |||

| 7nm | |||

| 16nm | |||

| 28nm | |||

| 28nm | |||

| Integrated Device Manufacturer (IDM) |

| Design / Fabless Vendor |

| Automotive |

| Communication (Wired and Wireless) |

| Consumer |

| Industrial |

| Computing / Data Storage |

| Data Center |

| AI |

| Government (Aerospace and Defense) |

| By Device Type (Shipment Volume for Device Type is Complementary) | Discrete Semiconductors | Diodes | ||

| Transistors | ||||

| Power Transistors | ||||

| Rectifier and Thyristor | ||||

| Other Discrete Devices | ||||

| Optoelectronics | LEDs | |||

| Laser Diodes | ||||

| Image Sensors | ||||

| Optocouplers | ||||

| Other Device Types | ||||

| Sensors and MEMS | Pressure | |||

| Magnetic Field | ||||

| Actuators | ||||

| Acceleration and Yaw Rate | ||||

| Temperature and Others | ||||

| Integrated Circuits | By Integrated Circuit Type | Analog | ||

| Micro | Microprocessors (MPU) | |||

| Microcontrollers (MCU) | ||||

| Digital Signal Processors | ||||

| Logic | ||||

| Memory | ||||

| By Technology Node (Shipment Volume Not Applicable) | Less than 3nm | |||

| 3nm | ||||

| 5nm | ||||

| 7nm | ||||

| 16nm | ||||

| 28nm | ||||

| 28nm | ||||

| By Business Model | Integrated Device Manufacturer (IDM) | |||

| Design / Fabless Vendor | ||||

| By End-user Industry | Automotive | |||

| Communication (Wired and Wireless) | ||||

| Consumer | ||||

| Industrial | ||||

| Computing / Data Storage | ||||

| Data Center | ||||

| AI | ||||

| Government (Aerospace and Defense) | ||||

Key Questions Answered in the Report

How large is the United Kingdom semiconductor market in 2025?

The market stands at USD 6.33 billion in 2025 and is projected to reach USD 7.07 billion by 2030.

Which device category dominates domestic semiconductor revenues?

Integrated Circuits lead with 63.04% share, driven by Arm-based CPUs, analog power, and embedded MCUs.

What growth rate is expected for Sensors and MEMS devices?

Sensors and MEMS will expand at a 3.11% CAGR, buoyed by ADAS and industrial IoT adoption.

Why is automotive the largest end-user for semiconductors?

Electrification mandates and rising electronic content push automotive demand to 29.25% of market revenue.

How does government policy support semiconductor expansion?

The GBP 1 billion National Semiconductor Strategy funds R&D, skills, and infrastructure, complemented by cuts in industrial electricity fees from 2026.

Where is the UK’s main compound-semiconductor hub located?

South Wales, centered on Newport Wafer Fab and IQE’s epitaxy campus, forms Europe’s largest compound-semiconductor cluster.

Page last updated on: