Brazil Mining Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

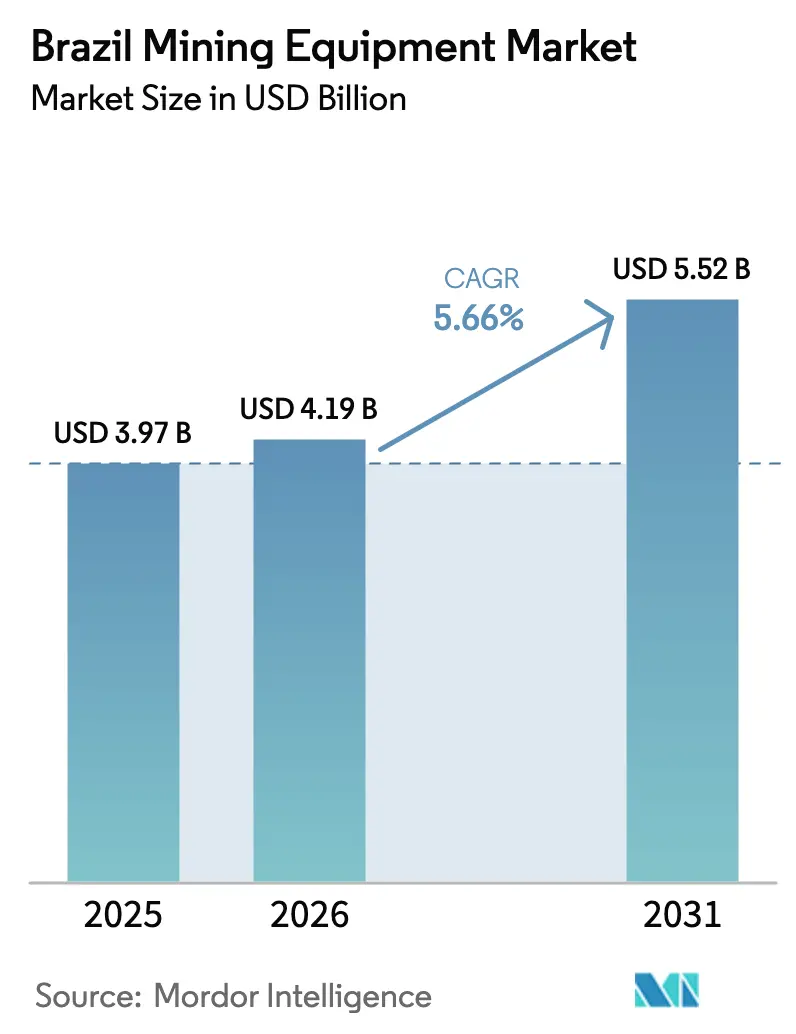

| Base Year Market Size (2025) | USD 3.97 Billion |

| Market Size (2026) | USD 4.19 Billion |

| Market Size (2031) | USD 5.52 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Mining Equipment Market Analysis by Mordor Intelligence

The Brazil Mining Equipment Market size is expected to grow from USD 3.97 billion in 2025 to USD 4.19 billion in 2026 and is forecast to reach USD 5.52 billion by 2031 at 5.66% CAGR over 2026-2031. The upward trajectory is anchored in Vale’s USD 12 billion outlay at Carajás that raises iron-ore capacity by 13% and triggers large-scale procurement of haul trucks, drills, and process plants. Surging investments in rare-earth and lithium projects, a 67% concentration of Brazil’s mineral reserves in Minas Gerais, and government financing lines sustain equipment demand across open-pit and underground operations. The Brazil mining equipment market benefits from the rapid uptake of battery-electric machines, autonomy packages, and condition-monitoring systems that improve productivity and cut emissions. Diesel platforms dominate fleets, yet fleet-wide electrification pilots and renewable power availability are setting the groundwork for future replacements. Competitive intensity remains moderate as global OEMs defend installed bases while local suppliers and automation specialists capture niche opportunities.

Key Report Takeaways

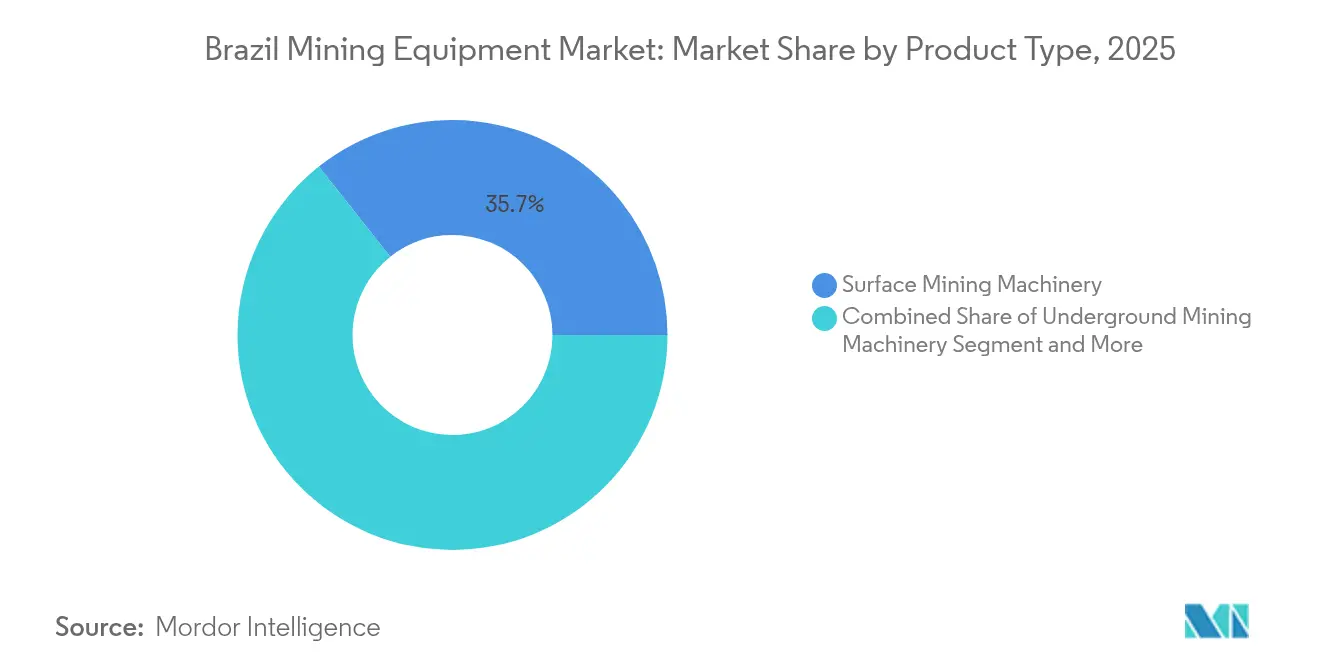

- By product type, Surface Mining Machinery led 35.68% of Brazil's mining equipment market share in 2025; Battery-Electric Equipment is projected to advance at a 5.73% CAGR through 2031.

- By application, the Metals segment accounted for a 51.25% share of the Brazil mining equipment market in 2025, while Lithium and rare-earth Projects registered the highest CAGR at 5.86% to 2031.

- By function, Excavation captured 45.52% of Brazil's mining equipment market share in 2025; Processing equipment is forecast to grow at a 5.88% CAGR up to 2031.

- By powertrain, Diesel platforms represented 83.35% of the Brazil mining equipment market size in 2025, and Battery-Electric variants are expanding at a 6.02% CAGR over the same horizon.

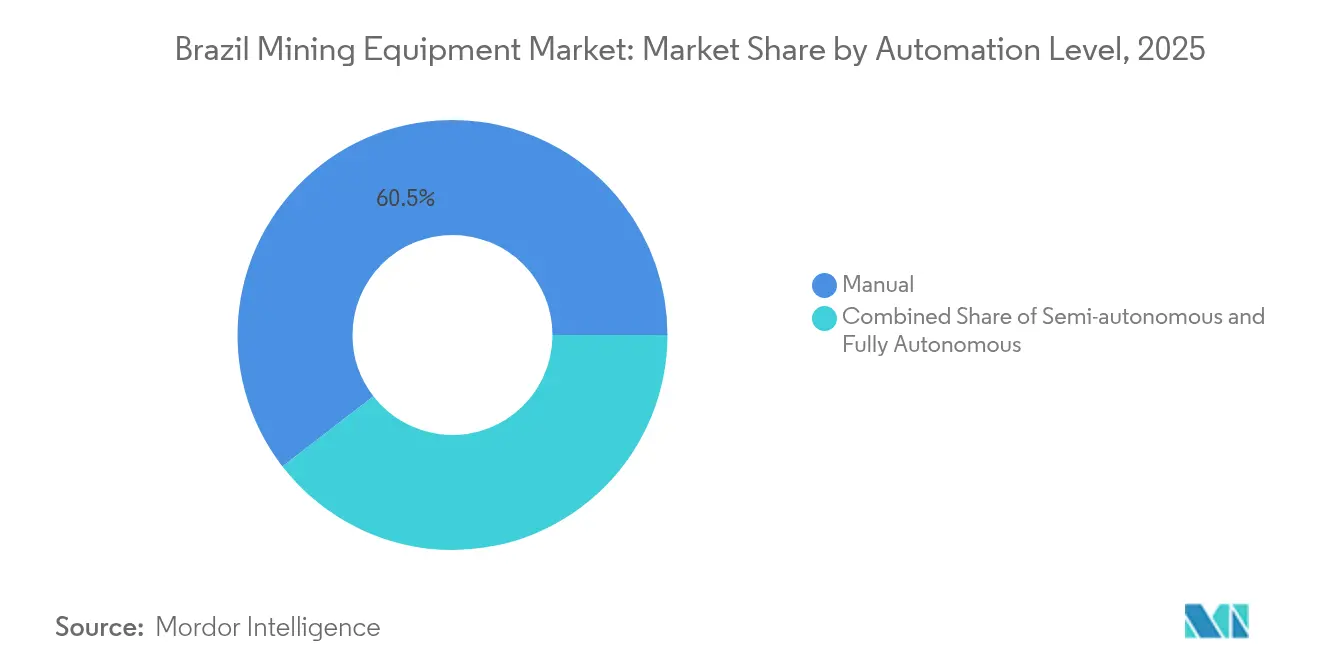

- By automation level, Manual operations held 60.48% share of the Brazilian mining equipment market in 2025, whereas Fully Autonomous systems are rising at a 5.71% CAGR through 2031.

- By end-user commodity, Iron Ore applications commanded 37.12% of Brazil's mining equipment market share in 2025; lithium and rare Earths led growth at a 5.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Iron-ore Expansion Capex | +1.3% | Minas Gerais, Pará, concentrated in Carajás and Quadrilátero Ferrífero regions | Medium term (2-4 years) |

| Automation and Autonomy Adoption | +1.1% | National, with early gains in Carajás, Brucutu, and major Vale operations | Long term (≥ 4 years) |

| EV-Critical-Mineral Project Pipeline | +1.0% | Goiás, Minas Gerais, Bahia for lithium and rare earths development | Medium term (2-4 years) |

| New Mining-Rights Auctions | +0.9% | National, particularly Bahia, Goiás, and emerging mineral provinces | Short term (≤ 2 years) |

| BNDES Localisation Incentives | +0.7% | National, with emphasis on domestic manufacturing hubs in São Paulo, Minas Gerais | Medium term (2-4 years) |

| ESG-Linked Demand | +0.6% | National, particularly affecting large-scale operations with international stakeholders | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Iron-Ore Expansion Capex

Vale’s USD 12.3 billion Novo Carajás program lifts Brazil’s iron-ore output to a projected exponential growth by 2030 and drives record orders for shovels, autonomous trucks, and processing plants. Higher throughput requirements favour large-capacity crushers, overland conveyors, and stackers that lower unit costs and reduce diesel use. The procurement wave ripples to port upgrades at Ponta da Madeira and Tubarão, where ship loaders and railcar dumpers are being modernised. These developments reinforce the Brazilian mining equipment market as a stable destination for OEM manufacturing localisation.

Automation & Autonomy Adoption

Vale’s 100 million ton milestone moved by autonomous trucks at Brucutu confirmed 11% productivity gains with zero accidents and spurred replication at Carajás and S11D. Anglo American and CSN Mineração initiated autonomous haulage studies, broadening the Brazil mining equipment industry adoption base. Sandvik’s AutoMine platform and Epiroc’s Scooptram automation packages allow mixed-fleet operations to run under a single supervisory system, improving cycle-time consistency. Robotics decreases exposure to dust and noise, a key issue in Pará’s high-temperature pits. Demand for LIDAR, collision-avoid systems, and high-precision GPS grows alongside aftermarket contracts that secure data analytics revenues.[1]“AutoMine Underground Drills Launch,” Sandvik AB, sandvik.com

EV-Critical-Mineral Project Pipeline

Serra Verde in Goiás, the country’s first commercial rare-earth mine, commenced exports to Asia in 2025 and underpinned orders for magnetic separators, rotary kilns, and solvent-extraction units. Aclara’s Carina project schedules its first concentrate in 2028, specifying dry-stack tailings and battery-electric loaders to meet investor ESG metrics. Sigma Lithium’s green lithium model at Vale do Jequitinhonha relies on power from hydro plants, promoting all-electric crushing circuits and regenerative downhill conveyors. Government support for critical-mineral projects ensures a predictable offtake and sustains vendor confidence in stocking specialised parts locally.[2]“Sustainability Report 2025,” Sigma Lithium Corp., sigmalithium.com

New Mining-Rights Auctions & Financing Flows

ANM’s 2025 auction agenda covers Rio Capim kaolin and 500 other tenements that attract juniors and mid-tiers, each requiring fleets of medium excavators, drills, and modular plants. The R$1 billion BNDES-Vale fund offers low-cost credit for critical-mineral ventures with revenue below R$300 million, unlocking equipment leases for projects previously considered sub-scale. Co-investment from the US International Development Finance Corporation diversifies the capital pool, allowing suppliers to structure multi-year framework agreements. Accelerated licensing for brownfield expansions further reduces lead times between concession award and production start, compressing ordering cycles in the Brazilian mining equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-Price Volatility | -1.1% | National, with higher impact on iron ore-dependent regions like Minas Gerais and Pará | Short term (≤ 2 years) |

| Lengthy Environmental Licensing | -0.8% | National, particularly affecting new projects in Amazon and Atlantic Forest regions | Long term (≥ 4 years) |

| ANM Understaffing | -0.5% | National, with concentrated impact on new mining projects and expansions | Medium term (2-4 years) |

| Grey-Market Used-Equipment Inflows | -0.4% | National, particularly affecting price-sensitive segments and smaller operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Commodity-Price Volatility

Iron-ore prices slipped 12% to USD 95.30 /t in 2024, cutting Vale’s earnings by 21% to R$31.6 billion and prompting order deferrals for discretionary technology upgrades. Mid-tier producers hedge only part of their output, amplifying cash-flow swings that cascade to equipment budgets. During down-cycles, miners prioritise essential spares over fleet expansion, compressing OEM production schedules and inflating unit costs. Conversely, sharp rebounds trigger rush orders that strain assembly capacity for large wheel-loaders and face shovels. This boom-and-bust pattern complicates workforce planning at local plants and generates lumpy revenue recognition across the Brazilian mining equipment industry.

Lengthy Environmental Licensing

ANM operates with only 664 staff against a legal mandate of 2,121, producing review queues that stretch procurement schedules. Projects in the Amazon and Atlantic Forest biomes undergo multi-agency assessments exceeding 36 months. Judicial suspensions of tailings-reuse rules create planning uncertainty and force miners to delay signing equipment contracts until licences are in hand. OEMs respond by holding higher inventory at Minas Gerais and Pará distribution centers, tying up working capital. Suppliers also extend payment terms to 150 days to accommodate unpredictable shipment windows, which squeezes margins in the Brazilian mining equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Surface Mining Machinery Remains the Workhorse

Surface equipment held a 35.68% share of the Brazilian mining equipment market in 2025 as open-pit operations dominate iron-ore, bauxite, and phosphate extraction in Minas Gerais and Pará. High-bench depths and wide haul roads favour ultra-class trucks and hydraulic shovels whose payload efficiency underpins the country’s export competitiveness. The Brazil mining equipment market size for battery-electric units is still small, yet its 5.73% CAGR to 2031 reflects accelerating ESG mandates at Vale and Anglo American. Companies also invest in crushers, screens, and grinding mills that support beneficiation growth, a trend reinforced by higher royalties on unprocessed ore. An expanding parts and attachments segment sustains workshop activity in Itabira and Parauapebas, where undercarriage rebuilds and GET replacement require rapid service turnaround.

Second-generation autonomous kits now retrofit Komatsu 930E fleets in Carajás, improving haul-cycle consistency during night shifts. Meanwhile, Wabtec’s FLXdrive battery locomotives on the Vitória-Minas Railway cut diesel by 30%, showcasing electrification beyond the pit. The product mix, therefore, tilts toward interconnected fleets where drills relay ore-block data to excavator operators and downstream crushers adjust gap settings accordingly. This ecosystem approach differentiates suppliers in the Brazilian mining equipment market.

By Application: Metals Stay Dominant while Energy-Transition Minerals Accelerate

Metals applications commanded 51.25% of Brazil's mining equipment market share 2025, as iron ore, copper, and nickel underpin export revenues. Vale’s Base Metals division targets 900 kt/y copper and 300 kt/y nickel, elevating demand for high-pressure grinding rolls and flash smelters with lower unit emissions. Lithium & Rare-Earth projects expand at 5.86% CAGR, supported by federal credit lines and international offtake contracts that de-risk investment. Coal lags due to Brazil’s renewable-heavy power matrix, while industrial minerals like kaolin enjoy steady demand from ceramics producers.

Equipment requirements diverge: Iron ore uses 400-t trucks and semi-mobile crushing, whereas rare-earth operations deploy compact sizes and multi-stage solvent extraction. OEMs, therefore, segment support teams by commodity to align expertise with process nuances. This strategy strengthens customer loyalty and fuels recurring revenue in the Brazilian mining equipment market.

By Function: Processing Systems Capture Value-Addition Spend

Excavation retained 45.52% of Brazil's mining equipment market share in 2025, thanks to bulk-material movement needs at Carajás and S11D. However, processing equipment records the highest 5.88% CAGR as miners pursue pelletizing, concentrate upgrading, and downstream metal production that capture a higher value share. Projects deploy smart MCCs, online particle-size analysers, and AI-based thickener controls that lift recovery rates while cutting reagent costs.

In parallel, transportation systems adopt predictive bearing analytics and lightweight rake designs that reduce energy per tonne-kilometre. The functional shift underscores Brazil’s industrial policy push toward local value-addition and lowers exposure to seaborne freight volatility.

By Powertrain: Diesel Still Rules but Electric Options Scale Up

Diesel accounted for 83.35% of the Brazilian mining equipment market size in 2025, owing to remote-site constraints and established fuel logistics. Battery-electric platforms grow at 6.02% CAGR, catalysed by falling battery costs and a national grid boasting renewable electricity. Early deployments focus on trolley-assist haulage at Sossego and pit-to-crusher conveyors powered by solar installations. Hybrid powertrains bridge the transition by pairing downsized diesels with regenerative braking, delivering 25% fuel savings on steep gradients.

OEMs collaborate with WEG to source traction motors and ESS modules domestically, reducing import costs and lead times. Service contracts now include state-of-health monitoring that predicts battery replacement, embedding suppliers deeper into operational workflows in the Brazilian mining equipment market.

By Automation Level: Gradual Shift from Manual to Fully Autonomous

Manual operation prevails at 60.48% in 2025 as capex constraints and skills transfer slow adoption among junior miners. Semi-autonomous systems provide immediate productivity lifts with moderate investment, typified by Trimble-enabled dozers that cut rework on haul-road maintenance. Fully autonomous fleets expand at 5.71% CAGR, justified by safety gains that reduce lost-time injuries and lower insurance premiums. The transition is project-specific: S11D targets 100% autonomous haulage by 2028 while small gold mines continue manual blasting cycles.

OEMs now bundle autonomy software with equipment leases, aligning payment to achieved utilisation KPIs. This model eases upfront capital outlay and accelerates technology penetration across the Brazilian mining equipment industry.

By End-User Commodity: Iron-Ore Dominance Balanced by Critical Minerals Growth

Iron-ore applications dominated the Brazilian mining equipment market in 2025, with a 37.12% share, and remain the anchor for high-capacity equipment demand. Lithium and rare Earths post a 5.77% CAGR as Brazil is a secure supplier outside Asia. Gold, bauxite, copper, and nickel present diversified demand streams that smooth cyclical risk.

The government's selection of 56 strategic mineral projects supports order visibility across the commodity spectrum. Vale’s partnership with Manara Minerals injects USD 2.5 billion into base-metals expansion, increasing long-term offtake certainty and underpinning equipment financing structures.

Geography Analysis

Minas Gerais and Pará jointly generate the bulk of sales in the Brazilian mining equipment market. Minas Gerais hosts the majority of national iron-ore production and more than three-fifths of total mineral reserves, supporting continuous demand for shovels, drills, conveyor components, and pellet-plant upgrades. Belo Horizonte and Itabira service hubs benefit from mature road and rail links that shorten parts delivery times. Quadrilátero Ferrífero’s planned capacity additions and ongoing tailings-dam decommissioning ensure a steady backlog for earthmoving and filtration units.

Pará, responsible for more than two-fifths of iron-ore output, concentrates mega-scale operations at Carajás and S11D. These sites require ultra-class equipment, autonomous technology, and dedicated rail rolling stock, driving large-ticket orders that shape global production schedules at OEM plants in the United States and China. The Estado’s port of Ponta da Madeira continues to modernise ship-loaders and stacker-reclaimers, adding to material-handling spend. Bahia emerges as a growth pole with BYD assessing lithium and phosphate resources to feed its electric-vehicle value chain. Infrastructure improvements around the Port of Ilhéus improve equipment logistics and attract OEM interest in setting up satellite warehouses. Goiás gains relevance through the Serra Verde rare-earth and Carina projects, which need niche processing lines and environmental-control systems. Amapá’s DEV Mineração restart injects new orders for rebuild kits and mid-range excavators suited to softer ore bodies. These regional patterns require suppliers to balance centralised manufacturing economies with decentralised service delivery. Rail bottlenecks outside Minas Gerais and Pará necessitate modular plant designs that can be truck-hauled. Port congestion risks at Santos and Paranaguá influence decision-making on spare-parts stockholding within the Brazilian mining equipment market.

Competitive Landscape

Global OEMs such as Caterpillar, Komatsu, and Sandvik anchor production in Brazil, leveraging local labour and MERCOSUR tariff advantages. Caterpillar manufactures over a huge number of models across two plants with a workforce exceeding 6,000, ensuring quick turnaround on adaptation to local regulations.[3]“Brazil Operations Fact Sheet 2025,” Caterpillar Inc., caterpillar.com Komatsu’s autonomous-ready trucks build on field data from Pilbara to shorten commissioning at Carajás. Sandvik integrates surface and underground fleets under AutoMine, capturing premium margins on software licences and recurring analytics.

Japanese entrants Hitachi Construction Machinery and Marubeni formed a joint sales and service venture in 2024, intensifying competition, particularly for hydraulic excavators. Automation specialists PSI and MIRS offer robotic arm solutions for mill relining and tyre handling, nibbling at niches underserved by diversified OEMs.

Competition is balanced by high capital requirements and long product life cycles that favour established suppliers. Service quality, parts availability, and financing flexibility outweigh sticker price in purchase decisions. Strategic alliances between OEMs and miners on R&D pilots lock in multi-year technology roadmaps, cementing relationships and preserving share in the Brazilian mining equipment market.

Brazil Mining Equipment Industry Leaders

Caterpillar Inc.

Komatsu Ltd.

Sandvik AB

Epiroc AB

Liebherr-International AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Vale confirmed a USD 12 billion investment at Carajás through 2030 to lift iron-ore output by 13%, catalysing record equipment demand.

- September 2024: Hitachi Construction Machinery and Marubeni agreed to establish a dedicated mining-machinery sales and service company in Brazil.

- April 2024: Vale finalised a USD 2.5 billion transaction with Manara Minerals for a 10% stake in Vale Base Metals, funding copper and nickel capacity expansion.

Brazil Mining Equipment Market Report Scope

| Underground Mining Machinery |

| Surface Mining Machinery |

| Drills & Breakers |

| Crushing, Pulverizing & Screening |

| Mineral Processing Machinery |

| Parts & Attachments |

| Coal |

| Industrial Minerals |

| Metals (Ferrous & Non-ferrous) |

| Transportation |

| Processing |

| Excavation |

| Diesel |

| Battery-Electric |

| Hybrid |

| Manual |

| Semi-autonomous |

| Fully Autonomous |

| Iron Ore |

| Gold & Precious Metals |

| Bauxite |

| Lithium & Rare Earths |

| Copper & Nickel |

| By Product Type | Underground Mining Machinery |

| Surface Mining Machinery | |

| Drills & Breakers | |

| Crushing, Pulverizing & Screening | |

| Mineral Processing Machinery | |

| Parts & Attachments | |

| By Application | Coal |

| Industrial Minerals | |

| Metals (Ferrous & Non-ferrous) | |

| By Function | Transportation |

| Processing | |

| Excavation | |

| By Powertrain | Diesel |

| Battery-Electric | |

| Hybrid | |

| By Automation Level | Manual |

| Semi-autonomous | |

| Fully Autonomous | |

| By End-user Commodity | Iron Ore |

| Gold & Precious Metals | |

| Bauxite | |

| Lithium & Rare Earths | |

| Copper & Nickel |

Key Questions Answered in the Report

What is the 2026 value of the Brazilian mining equipment market?

The Brazilian mining equipment market size reached USD 4.19 billion in 2026.

How fast is the market expected to grow through 2031?

The market is forecast to expand at a 5.66% CAGR, taking value to USD 5.52 billion by 2031.

Which product segment holds the largest share?

Surface Mining Machinery leads with a 35.68% share of the Brazilian mining equipment market.

Which application area is growing fastest?

Equipment for Lithium & Rare-Earth projects shows the highest growth at a 5.86% CAGR.

How dominant are diesel powertrains currently?

Diesel units comprise 83.35% of installed equipment, although battery-electric variants are scaling up.

What regional markets drive the bulk of demand?

Minas Gerais and Pará account for most equipment purchases due to their iron ore mines and processing hubs.

Page last updated on: