Japan Mining Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 6.57 Billion |

| Market Size (2030) | USD 8.55 Billion |

| Growth Rate (2025 - 2030) | 5.40% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Mining Equipment Market Analysis by Mordor Intelligence

The Japan mining equipment market size stands at USD 6.57 billion in 2025 and, on the strength of a 5.40% CAGR, is projected to reach USD 8.55 billion in 2030, anchoring robust demand for advanced machinery that supports the nation’s critical-mineral policy push. Acute incentives for resource self-sufficiency, the rise of deep-sea extraction projects, and the surge in battery-grade metal demand are shaping procurement strategies across legacy pits and offshore fields. Technological upgrades, especially in autonomous haulage, AI-enabled drilling, and battery-electric powertrains, continue to redefine capital-expenditure priorities as operators seek higher productivity with lower environmental footprints. Competition is intensifying but remains moderate, with domestic majors leveraging manufacturing depth while international specialists supply niche electrification and digitalization solutions. Momentum in rare-earth exploration, combined with carbon-neutral mandates, positions precision rigs and hybrid marine-mining systems as pivotal growth pockets throughout the forecast window.

Key Report Takeaways

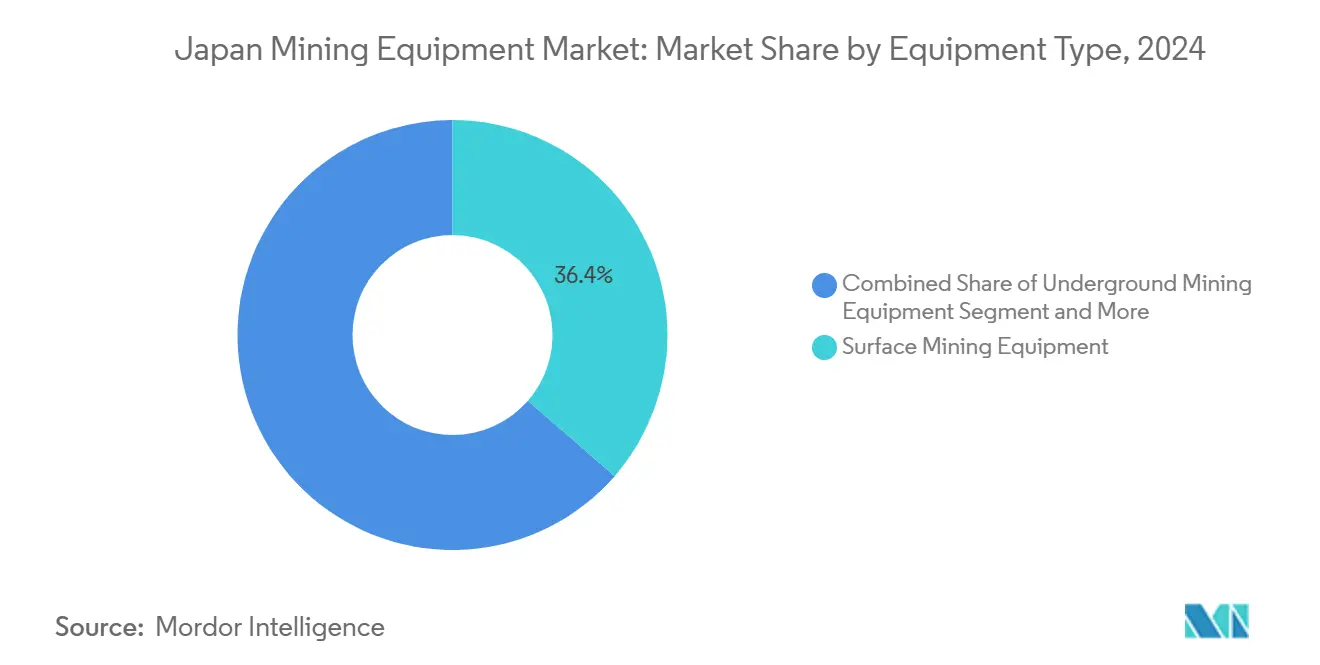

- By equipment type, surface mining captured 36.42% of the Japan mining equipment market share in 2024; drills and breakers are advancing at an 11.84% CAGR through 2030.

- By automation level, manual machinery held 52.07% of the Japan mining equipment market size in 2024, while fully autonomous systems are growing at a 15.19% CAGR to 2030.

- By powertrain, internal-combustion equipment led with 72.58% share in 2024; battery-electric vehicles are expanding at 19.43% CAGR over the forecast period.

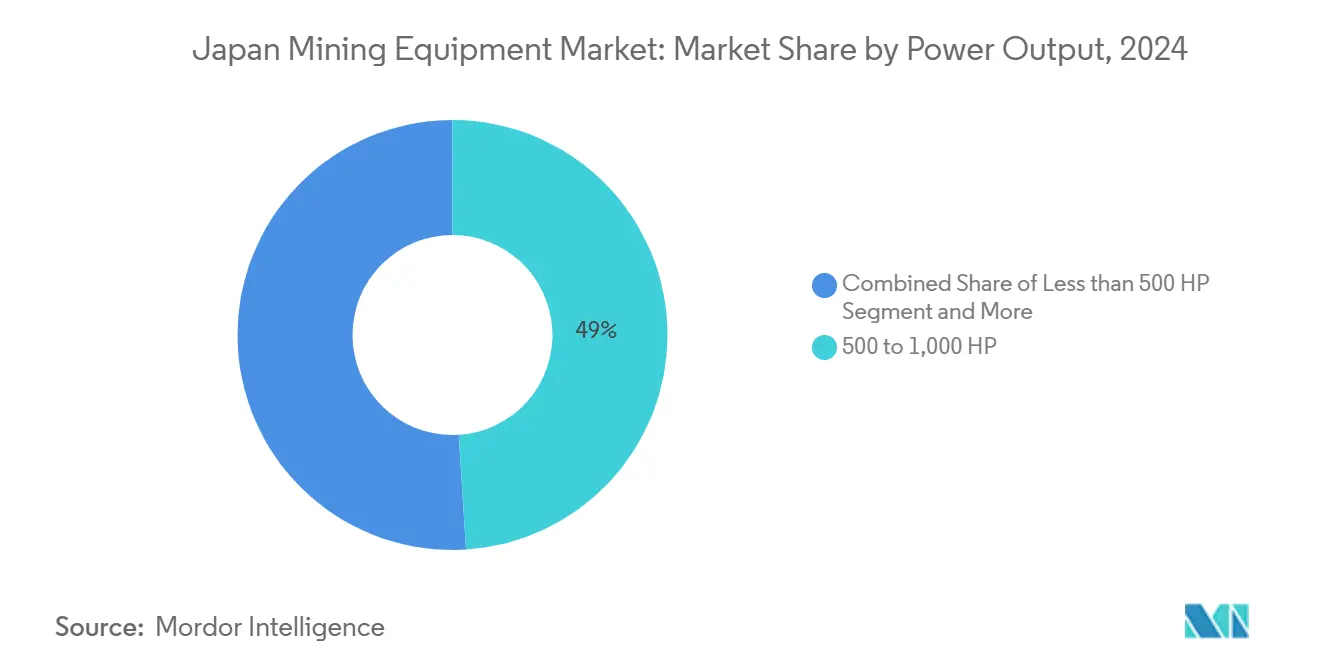

- By power output, the 500–1,000 HP band commanded 49.01% of the Japan mining equipment market share in 2024, whereas sub-500 HP machines posted the fastest 12.64% CAGR up to 2030.

- By application, metal mining accounted for 55.31% of the Japanese mining equipment market size in 2024, and rare-earth mining is projected to climb at a 13.12% CAGR through 2030.

Japan Mining Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Incentives for Critical-Mineral Self-Sufficiency | +1.8% | National, with concentration in Minami-Torishima and Nankai Trough regions | Medium term (2–4 years) |

| Surging EV-Battery Metal Demand | +1.5% | National, with spillover to ASEAN supply chains | Long term (≥ 4 years) |

| Tech Advances in AI-Enabled Exploration Rigs | +1.2% | National, with early adoption in Hokkaido and Kyushu mining regions | Medium term (2–4 years) |

| National Push for Methane-Hydrate and Deep-Sea Resources | +0.9% | Coastal regions, particularly Nankai Trough and Pacific EEZ | Long term (≥ 4 years) |

| Ageing Workforce Spurring Remote-Operation Uptake | +0.6% | National, with higher impact in rural mining areas | Short term (≤ 2 years) |

| Carbon-Neutral Targets Favouring Battery-Electric Rigs | +0.5% | National, aligned with industrial decarbonization zones | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Critical-Mineral Self-Sufficiency

Japan's Economic Security Promotion Act has designated key metals and mining equipment as "critical," paving the way for preferential financing, tax relief, and expedited permitting. The act mandates supply-chain resilience, guaranteeing multi-year purchasing pipelines for essential equipment like loaders, crushing circuits, and offshore robotics. This initiative aims to reduce dependency on imports and bolster domestic production capabilities. Additionally, fiscal support and swift regulatory processes provide a stable outlook for brownfield upgrades and new greenfield projects, fostering long-term growth in the mining sector.

Surging EV-Battery Metal Demand

The national electrification roadmap aligns auto, energy, and mining sectors around cobalt, nickel, and lithium sourcing. A joint Japan–Europe digital platform launching in 2025 tracks metal flows and raises purity thresholds, compelling mines to adopt precision drills, advanced sorters, and contamination-free haulage. Polymetallic nodule fields holding 610,000 tons of cobalt can alone cover 75 years of domestic use, triggering prototype deep-sea crawlers tailored for battery-grade recovery[1]"Japan plans 'world first' deep-sea mineral extraction," phys.org.. Equipment requests increasingly specify robotically managed loading chutes and real-time ore-grading analytics to meet high-performance cathode requirements. Engineering teams retrofit processing lines with sensor arrays, enabling closed-loop control of particle size and moisture capabilities pivotal to downstream gigafactory contracts. Consequently, procurement managers tilt capex toward rigs that guarantee metallurgical consistency and traceability.

Tech Advances in AI-Enabled Exploration Rigs

Machine-learning modules embedded in drill masts now automate trajectory planning, torque control, bit-wear prediction, lifting penetration rates, and curbing downtime. Komatsu’s acquisition of Octodots Analytics injects cloud-based image recognition into its fleet, allowing real-time rock-face classification. Similar systems inform explosives dosing, optimizing fragmentation, and reducing processing energy. IoT sensors relay high-frequency vibration and gas data via 5G, enabling predictive maintenance that lifts asset availability. The cumulative result is that drill-and-blast costs fall, safety margins widen, and demand concentrates on software-defined, upgradeable rigs.

National Push for Methane-Hydrate and Deep-Sea Resources

Beyond polymetallic nodules, Japan investigates methane hydrates in the Nankai Trough, a frontier demanding hybrid energy–mineral solutions. Engineering firms rush to supply corrosion-resistant alloys, high-power optical tether cables, and low-temperature drilling fluids suitable for hydrate stability. Such projects rely on winch systems calibrated for dynamic vessel motion, generating incremental orders for marine-grade actuation kits. The exploration timeline crosses a decade, yet prototype contracts for pumps, risers, and mud-gases separators have already surfaced, signaling a multiyear tail of specialized equipment demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Permitting | -0.8% | National, with stricter enforcement in coastal and protected areas | Short term (≤ 2 years) |

| Commodity-Price Volatility | -0.6% | Global impact with domestic amplification through currency effects | Short term (≤ 2 years) |

| Land Scarcity Versus Urban Development | -0.4% | Metropolitan areas and industrial corridors | Medium term (2–4 years) |

| Fragile Supply Chain for High-Precision Components | -0.5% | National, with critical dependencies on European and North American suppliers | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Environmental Permitting Challenges Constrain Project Timelines

Environmental Impact Assessment law imposes sequential studies on biodiversity, water quality, and cultural heritage, extending the timeline for risk assessment for both onshore and offshore mines. Deep-sea schemes face heightened scrutiny due to limited baselines for benthic ecosystems. Mining promoters must show rehabilitation funding at financial close, raising up-front capex. These conditions push equipment orders into later project phases and incentivize modular, redeployable plants that minimize permanent seabed alteration. The additional compliance workload raises soft-cost ratios and tempers the velocity of new fleet installations.

Commodity Price Volatility Impacts Investment Decisions

Construction equipment manufacturing grapples with global supply chain disruptions. Fueled by price volatility in aluminum and steel, these disruptions lead to unpredictable cost structures for producing and maintaining crawler machinery. U.S. tariff policies on steel and aluminum imports further tighten global supply chains. This directly impacts equipment assembly operations in Singapore and the availability of aftermarket parts. The cascading effects of these challenges are evident across the supply and value chain. As a result of this supply volatility, inventory management costs have surged for dealers and rental companies. Some operators now maintain parts inventories for 18 months, a significant jump from the traditional 6-month buffer. This shift increases working capital requirements and adds to operational complexity. The extended inventory periods also necessitate enhanced storage solutions and robust forecasting models to mitigate risks associated with fluctuating demand and supply constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Surface Operations Lead While Precision Drills Accelerate

Surface machinery held 36.42% of the Japanese mining equipment market share in 2024, reflecting the prevalence of open-pit and quarry sites across Hokkaido, Honshu, and Kyushu. Fleet renewal is driven by stricter dust and noise standards, prompting orders for enclosed-cab excavators and low-vibration shovels. Underground systems remain essential for legacy zinc and gold veins, yet limited new shafts mute incremental growth. Mineral-processing lines secure steady aftermarket spend as operators upgrade to battery-grade output specifications required by cathode makers.

Drills and breakers, the fastest-growing subset at 11.84% CAGR, benefit from AI-assisted collar placement and micro-fracturing technologies that support deep-sea pilot holes. The Japan mining equipment market size for this segment is projected to widen as seabed licensees specify high-torque, low-rpm heads to minimize sediment plumes. Crushing-screening units see retrofits for moisture control, ensuring stable throughput despite humid monsoon conditions. Loaders and haul trucks integrate collision-avoidance radars, aligning with the national zero-accident vision.

By Automation Level: Manual Prevalence Confronts Rapid Autonomous Growth

Manual equipment accounted for 52.07% of the Japan mining equipment market size in 2024, but face attrition as demographic pressures mount. Human-operated bulldozers dominate smaller quarries where capex discipline outweighs tech adoption. Yet, the Japan mining equipment market is pivoting: fully autonomous systems exhibit a 15.19% CAGR, underpinned by stable wireless networks, cloud analytics, and favorable safety regulations.

Semi-autonomous fleets bridge the transition, offering driver-assist modules that cut idle burn and reduce tire wear. Over the forecast horizon, remote operations centers concentrate in urban hubs, permitting round-the-clock supervision of multiple pits. Japan mining equipment market share captured by autonomous trucks rises as Komatsu’s 980E-AT proves 15% cycle-time savings and 13% fuel cuts. Software subscription revenues expand, embedding OEMs deeper into mine workflows.

By Powertrain Type: Electrification Gains Pace Amid Dominant ICE

Internal combustion engines held a 72.58% share in 2024, reflecting extensive diesel infrastructure and proven reliability during sub-zero winters. However, battery-electric rigs grew at a 19.43% CAGR, propelled by renewable-power discounts and ESG loan covenants tying interest rates to emission intensity. The Japan mining equipment market size attributed to BEVs will grow at a considerable pace till 2030, with trolley-assist haulage cutting emissions on steep ramps.

Hybrid drives serve transitional deployments where grid upgrades lag. Auxiliary hydrogen fuel cells are being trialed in underground settings to reduce diesel particulate exposure. Charging infrastructure packages bundled with fleet sales, often backed by public power utilities, accelerate the tipping point toward zero-tailpipe fleets.

By Power Output: Mid-Range Engines Dominate, Compact Units Surge

The 500–1,000 HP bracket commanded 49.01% of Japan mining equipment market share in 2024, favored for versatility across mid-depth pits and tunnel headings. Equipment in this range balances torque and fuel efficiency, maintaining popularity among contractors switching between contract mining jobs. Above-1,000 HP machines retain importance for limestone and granite quarries but face site-access limits amid Japan’s mountainous terrain.

Units below 500 HP log the quickest 12.64% CAGR as precision mining, selective blasting, and battery-powered underground loaders proliferate. The Japan mining equipment market size for compact rigs benefits from modularity that fits narrow drifts and can be freighted via regional rail. Automation software now optimizes fleets of smaller machines operating in coordinated clusters, lifting net throughput without oversizing individual assets.

By Application: Metal Mining Leads, Rare-Earth Extraction Soars

Metal mining delivered 55.31% of the Japan mining equipment market size in 2024, mirroring strategic stockpiling of copper, nickel, and cobalt. Government funding de-risks metallurgy plants aligned with EV supply-chain localization. Mineral mining for ceramics and industrial fillers keeps baseline equipment utilization, while coal’s structural decline continues under the Seventh Strategic Energy Plan.

Rare-earth sites emerge with 13.12% CAGR, catalyzed by seabed nodules containing dysprosium and terbium crucial for permanent magnets. The Japan mining equipment market share tied to these elements accelerates through contracts for remotely operated vehicles and high-pressure slurry pumps. Processing lines integrate solvent-extraction columns equipped with AI-driven flow-control valves to maximize recovery and minimize chemical usage.

Geography Analysis

Hokkaido anchors legacy coal and polymetallic operations, with sub-zero winters necessitating enclosed-cab dozers, cold-start diesel packages, and heated hydraulic lines. The prefecture’s Special Zone status for green transformation attracts grants for electrified excavation fleets[2]"Section3. National Strategic Special Zones "Special Zones for Financial and Asset Management Businesses," JETRO Invest Japan Report 2024, jetro.go.jp.. Kyushu, especially Kagoshima, hosts renewed gold exploration financed by foreign capital, driving inquiries for high-precision core drills capable of operating in fractured volcanic strata. These southern projects leverage proximity to ports, easing inbound shipping of oversized crushers and outbound concentrate.

Chugoku and Shikoku witness modest demand tied to limestone quarrying for cement but increasingly deploy dust-suppression sprayers to meet urban air-quality rules. Central Honshu’s manufacturing clusters spur demand for mineral-processing kits that feed directly into regional electronics supply chains. Okinawa’s seabed research stations support prototype trials for low-impact harvesting arms, expanding collaborative opportunities between marine institutes and OEMs.

Most transformative is the Exclusive Economic Zone around Minami-Torishima, where extraction at 5,500 meters compels bespoke riser pipes, navigation sonars, and dynamic-positioning drill ships. The Nankai Trough complements this frontier with methane-hydrate pilots, calling for dual-use pumps applicable to both gas and mineral workflows. As offshore permits mature, supply chains extend from Kansai shipyards to onshore staging yards, generating new clusters of service jobs and stimulating ancillary equipment leasing markets.

Competitive Landscape

Komatsu leads domestic sales by pairing broad product breadth with worldwide autonomous-haulage credentials; its FrontRunner platform manages multiple trucks on five continents and underpins Japanese fleet trials.

International challengers Epiroc and Sandvik win drilling and bolting contracts by offering battery-electric rigs that cut ventilation costs in underground headings. Service offerings move center-stage: subscription monitoring, remote firmware, and embedded analytics become sticky revenue streams. OEMs emphasize lifecycle support, drone parts logistics, and on-demand 3D printing to mitigate Japan’s island logistics constraints.

Partnerships between equipment makers and academic labs address deep-sea environmental monitoring, embedding multiparameter sensors into cutting heads to satisfy permit compliance. Overall, bargaining power tilts toward suppliers with integrated digital and sustainability credentials as mines prioritize total cost and compliance guarantees.

Japan Mining Equipment Industry Leaders

-

Komatsu Ltd.

-

Epiroc AB

-

Caterpillar Inc.

-

Sandvik AB

-

Hitachi Construction Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ABB inked a memorandum of understanding with Japan’s Sumitomo Corporation's construction and mining systems unit, focusing on net-zero emissions solutions for mining equipment. Their teams aim to conceptualize and integrate their systems for a greener mining future.

- November 2024: Five foreign firms - Canada's Japan Gold Corp., Irving Resources Inc., BeMetals Corp., Australia's Kin-Gin Exploration Pty., and Cipango Pty. - unveiled plans to explore gold mining across 42 sites in Japan. These ventures are set to escalate the demand for machinery, from loaders and excavators to mining trucks.

- May 2024: Komatsu unveiled the battery-electric variants of its second-generation Z2 product line, enhancing its underground hard rock drilling and bolting equipment offerings.

Japan Mining Equipment Market Report Scope

| Surface Mining Equipment |

| Underground Mining Equipment |

| Mineral Processing Equipment |

| Drills and Breakers |

| Crushing, Pulverizing and Screening |

| Loaders and Haul Trucks |

| Manual Equipment |

| Semi-Autonomous Equipment |

| Fully Autonomous Equipment |

| Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles |

| Hybrid Vehicles |

| Less than 500 HP |

| 500 to 1,000 HP |

| Above 1,000 HP |

| Metal Mining |

| Mineral Mining |

| Coal Mining |

| By Equipment Type | Surface Mining Equipment |

| Underground Mining Equipment | |

| Mineral Processing Equipment | |

| Drills and Breakers | |

| Crushing, Pulverizing and Screening | |

| Loaders and Haul Trucks | |

| By Automation Level | Manual Equipment |

| Semi-Autonomous Equipment | |

| Fully Autonomous Equipment | |

| By Powertrain Type | Internal-Combustion Engine Vehicles |

| Battery-Electric Vehicles | |

| Hybrid Vehicles | |

| By Power Output | Less than 500 HP |

| 500 to 1,000 HP | |

| Above 1,000 HP | |

| By Application | Metal Mining |

| Mineral Mining | |

| Coal Mining |

Key Questions Answered in the Report

How large is the Japan mining equipment market in 2025?

It is valued at USD 6.57 billion, with projections reaching USD 8.55 billion by 2030 on a 5.40% CAGR.

Which equipment category is growing the fastest?

Drills and breakers post the highest 11.84% CAGR, propelled by deep-sea pilot programs and AI-enhanced exploration.

What share do battery-electric vehicles hold?

Although internal-combustion rigs still dominate, BEV units expand rapidly and are forecast to top USD 1 billion in sales by 2030.

Why is rare-earth mining important to Japan?

Seabed rare-earth deposits secure long-term supplies for EV and electronics manufacturing, cutting reliance on external sources.

Which region leads Japan’s mining activity?

Hokkaido remains the heart of traditional mining, while the offshore Minami-Torishima area anchors new deep-sea ventures.

Who are the key market players?

Domestic majors Komatsu and Hitachi Construction Machinery dominate, with Epiroc, Sandvik, and ABB supplying advanced drilling and electrification technologies.

Page last updated on: