Japan Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

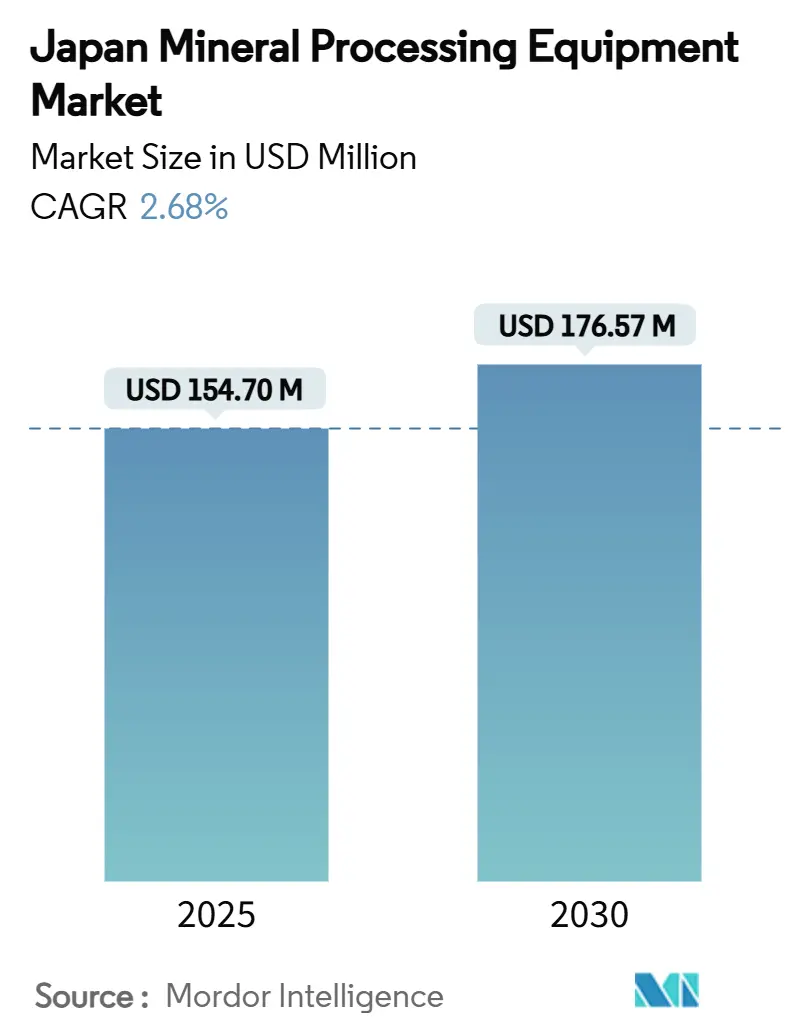

| Market Size (2025) | USD 154.70 Million |

| Market Size (2030) | USD 176.57 Million |

| Growth Rate (2025 - 2030) | 2.68% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Japan Mineral Processing Equipment Market Analysis by Mordor Intelligence

Japan mineral processing equipment market size reached USD 154.70 million in 2025 and is forecast to expand at a 2.68% CAGR to USD 176.57 million by 2030. This mature yet strategically important market is pivoting toward three high-growth pockets: deep-sea mining systems growing at 12.38%, fully automated equipment advancing 14.07%, and lithium-focused lines expanding 11.83%. Government decarbonization mandates accelerate adoption of energy-efficient crushers, mills, and conveyors, while tax credits offset up to 30% of qualifying CAPEX. International suppliers are scaling presence through joint R&D on subsea slurry pumps and battery-electric drill rigs, intensifying competition around sustainability specifications. The biggest constraint is a persistent shortage of skilled automation technicians, which lengthens commissioning cycles and raises service premiums.

Key Report Takeaways

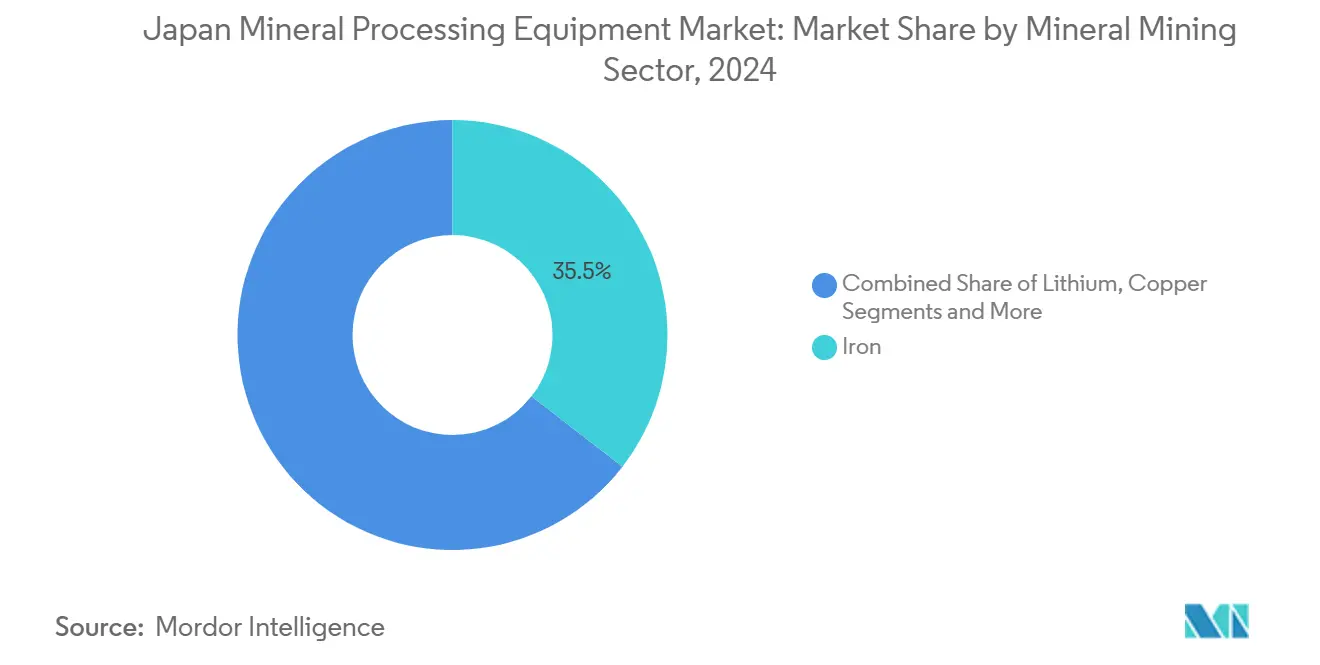

- By mineral mining sector, iron captured 35.47% of the Japan mineral processing equipment market share in 2024; lithium is projected to post the fastest 11.83% CAGR through 2030.

- By equipment type, crushers held 29.83% share of the Japan mineral processing equipment market size in 2024, while deep-sea mining systems are forecast to expand at a 12.42% CAGR between 2025-2030.

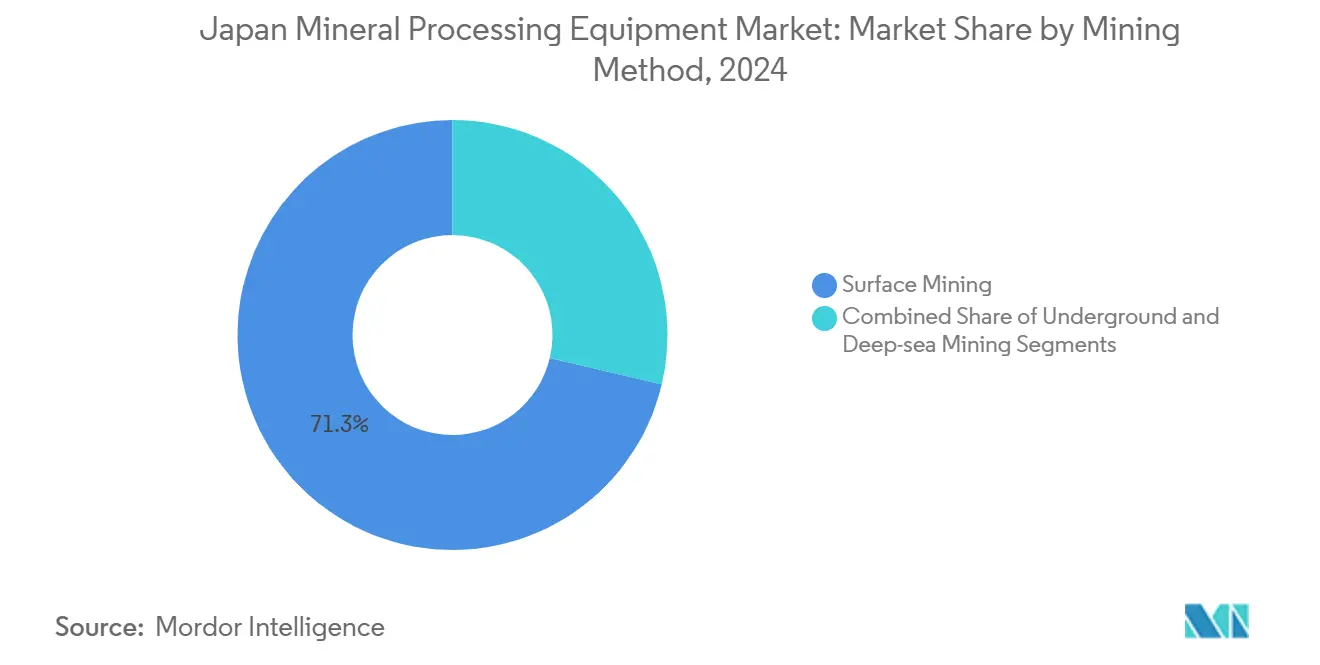

- By mining method, surface operations accounted for 71.27% of the Japan mineral processing equipment market size in 2024; deep-sea mining exhibits the highest 12.38% CAGR outlook to 2030.

- By automation level, semi-automated lines led with 54.64% share in 2024; fully automated units are advancing at a 14.07% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Japan representing one among them. The global report on mineral processing equipment market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Japan Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic Rare-Earth Exploration Push | +0.9% | National, concentrated in Okinawa Trough and Minamitori Island | Medium term (2–4 years) |

| Resurgence of Copper-Gold Projects | +0.8% | National, with early gains in Kyushu, Hokkaido | Medium term (2–4 years) |

| Government CAPEX and Tax Incentives for Energy-Efficient Plants | +0.7% | National, emphasis on industrial zones | Short term (≤ 2 years) |

| Accelerating Replacement Cycle of Ageing Mills and Crushers | +0.6% | National, concentrated in established mining regions | Long term (≥ 4 years) |

| Data-Driven Predictive-Maintenance Adoption by Mid-Tier Miners | +0.4% | National, spill-over to regional processing facilities | Medium term (2–4 years) |

| Offshore Polymetallic Nodule Trials in Okinawa Trough | +0.3% | Regional, focused on Okinawa Trough and surrounding EEZ | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Domestic Rare-Earth Exploration Drives Equipment Modernization

Japan's strategic pivot toward domestic rare earth production represents the most significant market driver, with the Japan Agency for Marine-Earth Science and Technology (JAMSTEC) initiating experimental drilling operations near Minamitori Island in January 2026. The project targets 230 million tons of polymetallic nodules containing 610,000 tons of cobalt and 740,000 tons of nickel, sufficient to meet Japan's consumption needs for 75 and 11 years respectively[1]"200 million tons of rare metal rocks found in seabed off Japan island," Kyodo News, kyodonews.net.. This initiative necessitates specialized deep-sea processing equipment capable of handling sticky, abrasive mud at 6,000-meter depths, requiring durable pipes and advanced slurry conversion systems that traditional land-based equipment cannot accommodate.

Government CAPEX Incentives Accelerate Energy-Efficient Plant Investments

Japan's Green Transformation Act establishes a USD 1 trillion investment framework over the next decade. The legislation introduces tax incentives for companies implementing production plans in strategic sectors, including mineral processing operations demonstrating measurable energy efficiency improvements[2]"Japan Green Transformation: A bold ambition to speed up the transition in Asia," amundi.com.. This policy framework particularly benefits mid-tier mining operations seeking to upgrade aging equipment, as the incentives can offset some share of capital expenditures for qualifying energy-efficient processing systems.

Copper-Gold Project Resurgence Fueled by Foreign Investment

Five foreign-capitalized companies are actively exploring gold mining across 42 locations in Japan, led by Canada's Japan Gold Corp., which has 26 projects primarily in Hokkaido and Kagoshima. The revised Mining Act of 2012 has facilitated this foreign investment surge. Japan Gold's Barrick Alliance launched its second 2025 drill program at the Ebino Project in Kyushu, targeting concealed epithermal vein systems near the high-grade Hishikari Mine[3]"5 foreign capital firms aiming to develop gold mines in at least 42 locations in Japan," Mainichi Japan, mainichi.jp.. These developments demand specialized processing equipment for high-grade ore concentrates, particularly flotation systems and gravity separation technologies optimized for precious metal recovery.

Accelerating Equipment Replacement Cycles Address Infrastructure Decay

Japan's materials industry faces a critical infrastructure crisis, with facilities "literally falling apart" due to decades of deferred maintenance and investment hesitancy. Companies like Nippon Steel have begun substantial modernization programs, investing in new coke oven facilities at the Nagoya plant, signaling a broader industry shift toward proactive equipment replacement. The Overall Mining Equipment Effectiveness (OMEE) methodology is gaining adoption among operators to optimize replacement timing, with studies indicating potential 12% reductions in scheduled maintenance costs and 30% decreases in overall maintenance expenses through strategic equipment upgrades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Carbon-Emission Caps on Mineral Processors | -0.6% | National, stricter enforcement in industrial zones | Short term (≤ 2 years) |

| High Electricity Tariffs Versus Regional Peers | -0.4% | National, particularly affecting energy-intensive operations | Medium term (2–4 years) |

| Shortage of Skilled Automation Technicians | -0.5% | National, concentrated in advanced manufacturing regions | Long term (≥ 4 years) |

| Seismic-Risk Design Costs for Heavy Fixed Plant | -0.3% | National, heightened requirements in high-seismicity zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Carbon Emission Caps Impose Compliance Costs on Processors

Japan's commitment to 46% greenhouse gas emission reductions by 2030 creates immediate compliance pressures for mineral processing operations, with carbon-intensive equipment facing potential operational restrictions or carbon pricing mechanisms. The government's focus on industrial decarbonization through the Green Transformation initiative prioritizes energy-efficient equipment adoption, but smaller operators struggle with the capital requirements for comprehensive system upgrades. This regulatory environment favors larger operators with resources to invest in advanced, low-emission processing technologies while potentially consolidating market share away from smaller, less-capitalized competitors.

Skilled Automation Technician Shortage Constrains Technology Adoption

Nearly 50% of small and medium-sized manufacturers report personnel shortages in equipment maintenance and inspection departments, with over half requiring at least two additional skilled technicians. The shortage has persisted for over four years in many companies, primarily due to insufficient hiring and the specialized nature of automation technology training. Japan's "2024 problem" - new overtime regulations limiting working hours - exacerbates this constraint, with the construction sector experiencing a workforce decline over the past decade and some workers now over 55 years old. This skills gap directly impacts the adoption of advanced automation systems that require specialized maintenance expertise, potentially slowing the deployment of next-generation mineral processing equipment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Iron Dominance Yields to Lithium Innovation

Iron mineral processing commands 35.47% market share in 2024, reflecting Japan's substantial steel industry infrastructure and established processing capabilities for imported iron ore concentrates. However, lithium processing equipment emerges as the fastest-growing segment with 11.83% CAGR from 2025-2030, driven by Japan's strategic investments in battery supply chain security and domestic lithium extraction initiatives. The rare earth metals segment benefits from government-backed exploration programs, while copper processing gains momentum from renewed mining activities in the Kyushu and Hokkaido regions, supported by foreign investment partnerships.

Bauxite and other mineral processing segments maintain stable but modest growth trajectories, constrained by Japan's limited domestic resources and reliance on imported concentrates. The historical CAGR comparison reveals accelerating growth in specialty minerals processing, particularly for battery metals and rare earths, contrasting with the mature iron processing sector's steady but slower expansion. This shift reflects Japan's industrial evolution toward high-tech manufacturing and strategic mineral security, positioning lithium and rare earth processing equipment as key growth drivers despite their currently smaller market shares.

By Equipment Type: Crushers Lead While Deep-Sea Mining Equipment Surges

Crushers maintain the largest market share at 29.83% in 2024, supported by Japan's extensive materials processing infrastructure and ongoing equipment replacement cycles in aging facilities. Traditional crushing equipment benefits from steady demand for maintenance and upgrades, particularly as companies address infrastructure decay issues highlighted by industry reports of facilities "literally falling apart". Grinding mills, conveyors, and screens represent established segments with predictable replacement cycles, while feeders and drilling equipment serve specialized applications in Japan's limited mining operations.

Deep-sea mining equipment emerges as the fastest-growing segment with 12.42% CAGR, despite its nascent market position, driven by Japan's pioneering polymetallic nodule extraction initiatives. This specialized equipment category includes subsea pumps, slurry handling systems, and remote-operated processing modules designed for extreme-depth operations. The segment's rapid growth reflects Japan's strategic commitment to domestic rare earth production and the technical innovation required for deep-sea mineral extraction, positioning Japanese manufacturers at the forefront of this emerging technology category.

By Mining Method: Surface Mining Dominance Challenged by Deep-Sea Innovation

Surface mining equipment commands 71.27% market share in 2024, reflecting Japan's geographic constraints and emphasis on processing imported materials rather than extensive domestic extraction. This dominance stems from Japan's industrial structure, where large-scale processing facilities handle imported ore concentrates using surface-accessible equipment configurations. Underground mining represents a smaller segment due to Japan's limited underground resources and geological challenges, though specialized applications exist in precious metal extraction operations.

While currently representing a small market share, deep-sea mining equipment demonstrates the highest growth potential at 12.38% CAGR from 2025-2030. This emerging segment addresses Japan's strategic imperative for domestic mineral security, with the Okinawa Trough and Minamitori Island projects requiring entirely new equipment categories. The deep-sea mining method necessitates specialized technologies, including autonomous underwater vehicles, subsea processing systems, and advanced materials handling equipment capable of operating at depths exceeding 6,000 meters, representing a technological frontier that positions Japan as a global leader in next-generation mineral extraction.

By Automation Level: Semi-Automated Systems Bridge to Full Autonomy

Semi-automated equipment will hold the largest market share, at 54.64% in 2024, representing the current sweet spot between operational efficiency and capital investment requirements for Japanese mineral processing operations. This segment benefits from established operator familiarity and proven reliability while offering productivity improvements over manual systems without requiring comprehensive workforce retraining. Manual operations retain relevance in specialized applications and smaller facilities where automation investment cannot be justified economically.

Fully automated equipment demonstrates the strongest growth trajectory at 14.07% CAGR, driven by Japan's acute skilled labor shortage and technological leadership in automation systems. Komatsu's Autonomous Haulage System (AHS) exemplifies this trend, with over 700 commercial deployments globally and continuous expansion in mining applications. The automation trend accelerates due to Japan's "2024 problem" - new overtime regulations limiting working hours and exacerbating existing labor shortages across industrial sectors. Fully automated systems solve workforce constraints while improving safety and operational consistency. This is particularly valuable in Japan's seismically active environment, where unmanned operations reduce human risk exposure.

Geography Analysis

Japan's mineral processing equipment market exhibits unique geographic characteristics shaped by the country's island geography, limited domestic mineral resources, and strategic focus on processing imported materials. The market concentrates around major industrial zones, including the Tokyo-Yokohama corridor, Osaka-Kobe region, and Nagoya industrial complex, where large-scale processing facilities handle imported ore concentrates. These regions benefit from established port infrastructure, skilled workforce availability, and proximity to end-user industries. However, they face increasing challenges from aging infrastructure and rising energy costs relative to regional competitors.

The emergence of deep-sea mining operations creates new geographic dynamics, with the Okinawa Trough and waters surrounding Minamitori Island becoming focal points for next-generation mineral extraction activities. These offshore developments require specialized equipment deployment and maintenance capabilities, potentially shifting market dynamics toward coastal regions with deep-water port access and advanced marine technology capabilities. The historical CAGR comparison between 2019-2024 and the 2025-2030 forecast reveals accelerating growth in regions supporting deep-sea mining infrastructure development, contrasting with more modest expansion in traditional land-based processing centers.

Regional energy cost differentials significantly impact equipment selection and operational strategies, with Japan's electricity tariffs exceeding regional peers and creating pressure for energy-efficient equipment adoption. The government's Green Transformation Act provides targeted support for energy-efficient equipment investments, particularly benefiting industrial regions with established manufacturing bases and technical expertise. This policy framework favors regions with existing industrial infrastructure while potentially constraining development in areas lacking established energy-efficient processing capabilities.

Mordor Intelligence provides coverage of the mineral processing equipment market across other key regional markets. Detailed country-level analysis extends to China, South Korea, Oman, Egypt, Morocco, South Africa, Italy, Brazil, and Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

Japan's mineral processing equipment market exhibits moderate concentration with established domestic players leveraging automation expertise and international suppliers focusing on specialized technologies. Market leadership centers on companies with comprehensive service capabilities and proven reliability in Japan's demanding operational environment. Komatsu Ltd. dominates through its integrated approach, combining equipment manufacturing with advanced automation systems. The company's Autonomous Haulage System represents a key competitive advantage, with over 700 commercial deployments globally demonstrating technological leadership in mining automation.

Hitachi Construction Machinery maintains a strong position through its value chain business model, generating revenue while emphasizing aftermarket services and predictive maintenance solutions. The company's ConSite monitoring system exemplifies the strategic shift toward data-driven equipment management, creating recurring revenue streams and strengthening customer relationships. International players, including Metso, Sandvik, and Epiroc, intensify competition through specialized technology offerings and strategic partnerships with Japanese operators.

White-space opportunities emerge in deep-sea mining equipment and energy-efficient processing technologies, where traditional suppliers lack specialized capabilities. The nascent deep-sea mining segment requires entirely new equipment categories, creating opportunities for innovative companies to establish market leadership before established players adapt their offerings. Additionally, Japan's skilled technician shortage creates demand for equipment with simplified maintenance requirements and remote monitoring capabilities, favoring suppliers who can integrate advanced diagnostics and automated maintenance scheduling into their systems.

Japan Mineral Processing Equipment Industry Leaders

-

Komatsu Ltd.

-

Hitachi Construction Machinery Co. Ltd.

-

Metso

-

Sandvik AB

-

FLSmidth

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: The Japan Agency for Marine-Earth Science and Technology announced plans to begin experimental rare earth extraction near Minamitori Island in January 2026. The agency will utilize the Chikyu deep-sea drilling vessel to access the world's third-largest rare earth reserve.

- June 2025: Japan Gold Corp. launched its second 2025 drill program under the Barrick Alliance at the Ebino Project in Kyushu, targeting concealed epithermal vein systems near the high-grade Hishikari Mine with three drill holes totaling approximately 1,300 meters.

Japan Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Copper |

| Rare-earth Metals |

| Others |

| Crushers |

| Grinding Mills |

| Conveyors |

| Drills and Breakers |

| Screens and Separators |

| Feeders |

| Others |

| Surface Mining |

| Underground Mining |

| Deep-sea Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Copper | |

| Rare-earth Metals | |

| Others | |

| By Equipment Type | Crushers |

| Grinding Mills | |

| Conveyors | |

| Drills and Breakers | |

| Screens and Separators | |

| Feeders | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| Deep-sea Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

How large is the Japan mineral processing equipment market in 2025?

The market is valued at USD 154.70 million in 2025 and is projected to reach USD 176.57 million by 2030.

Which mineral segment is growing fastest in Japan?

Equipment for lithium processing shows the strongest 11.83% CAGR on the back of battery-supply-chain initiatives.

What is the outlook for deep-sea mining equipment demand?

Deep-sea systems are forecast to expand at a 12.38% CAGR as trials in the Okinawa Trough and near Minamitori Island progress toward commercialization.

How are government incentives influencing equipment upgrades?

Under the Green Transformation Act, processors can offset up to 30% of capital costs for energy-efficient machinery, accelerating replacement of older crushers and mills.

Which companies lead the competitive landscape?

Komatsu, Hitachi Construction Machinery, Metso, Sandvik, and Epiroc collectively hold roughly 60%–65% of the market thanks to automation expertise and broad service networks.

What role does automation play in Japan’s market growth?

Fully automated equipment is advancing at a 14.07% CAGR as labor shortages and new overtime regulations push operators toward autonomous haulage and remote diagnostics.

Page last updated on: