Egypt Mineral Processing Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

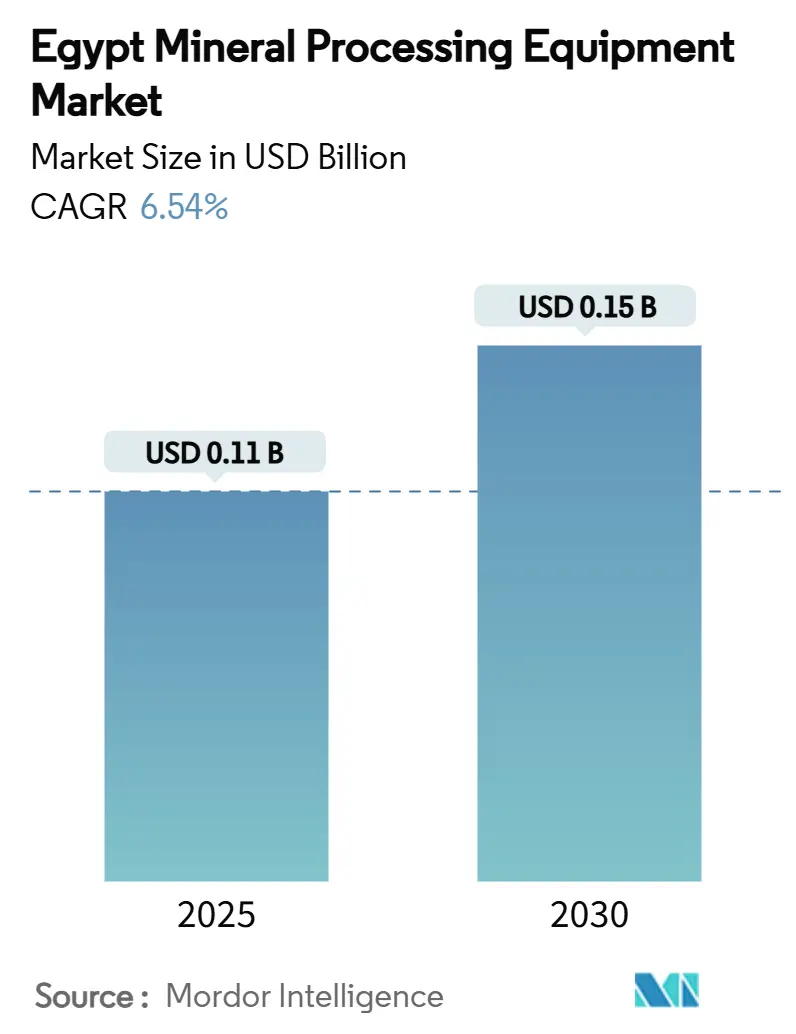

| Market Size (2025) | USD 0.11 Billion |

| Market Size (2030) | USD 0.15 Billion |

| Growth Rate (2025 - 2030) | 6.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Mineral Processing Equipment Market Analysis by Mordor Intelligence

The Egypt Mineral Processing Equipment Market size is estimated at USD 0.11 billion in 2025, and is expected to reach USD 0.15 billion by 2030, at a CAGR of 6.54% during the forecast period (2025-2030). The outlook reflects the government’s pivot from exporting raw ore to upgrading minerals domestically, a strategy meant to lift mining’s GDP share and to capture rising Gulf‐backed investment. Greater downstream capacity opens new opportunities for local suppliers of crushing, grinding, and separation systems, especially as mandatory local-content rules introduced in the 2024 Mining Law incentivize on-shore assembly lines. At the same time, AD Ports Group and other UAE investors inject capital into Red Sea logistics hubs, improving the supply chain for high-tonnage processing assets. Operators aiming for export-grade product quality roll out semi-automated circuits first. Phase in full automation as carbon-credit schemes shorten payback periods for energy-efficient mills and screens.

Key Report Takeaways

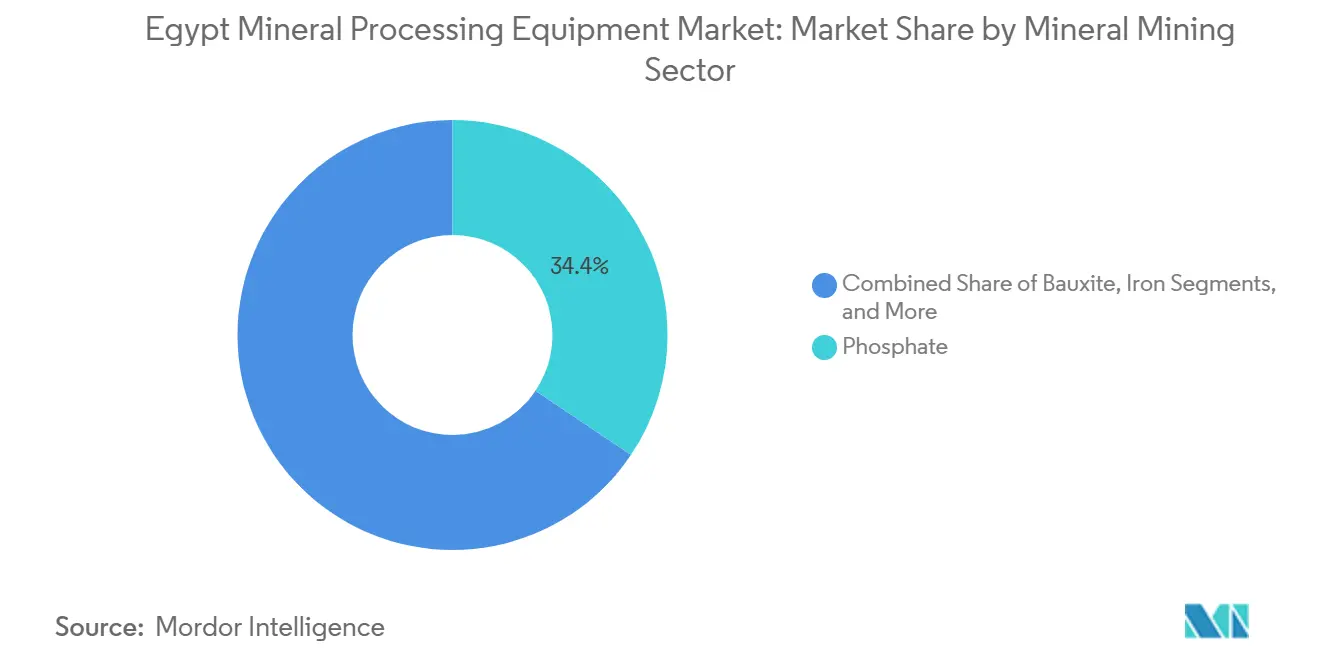

- By mineral mining sector, phosphate captured 34.37% of the Egyptian mineral processing equipment market share in 2024, while lithium equipment demand is on track for a 6.67% CAGR to 2030.

- By equipment type, crushers led the Egyptian mineral processing equipment market, with 26.51% of the market size in 2024; mills and screens carry the fastest forecast growth at 6.61% CAGR through 2030.

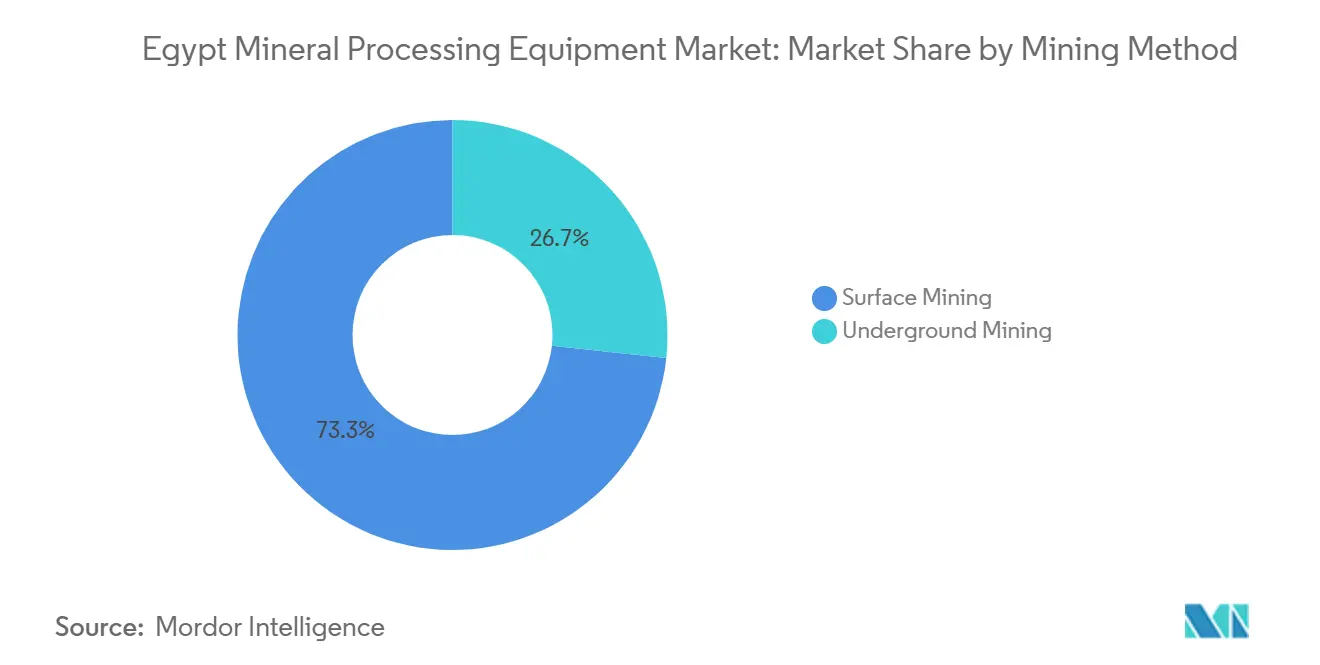

- By mining method, surface operations held 73.29% of the Egyptian mineral processing equipment market size in 2024, yet underground solutions show a stronger 6.59% CAGR outlook to 2030.

- By automation level, semi-automated lines commanded 47.83% of the Egyptian mineral processing equipment market share in 2024, whereas fully automated packages advance at a 6.77% CAGR to 2030.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of Egypt. The mineral processing equipment market share in our global report expresses these relative weights.

Egypt Mineral Processing Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast-Tracking of USD 1.2 Bn Abu Tartour Phosphate Downstream Complex | +1.8% | Upper Egypt, Qena governorate | Short term (≤ 2 years) |

| Growing Domestic Gold-Ore Throughput at Sukari | +1.2% | Eastern Desert, Red Sea zone | Medium term (2-4 years) |

| National Hydrogen-Steel Roadmap Boosting Demand | +1.1% | Alexandria, Suez Canal Economic Zone | Medium term (2-4 years) |

| Mandatory Local-Content Policy | +0.9% | National, concentrated in Cairo-Suez corridor | Long term (≥ 4 years) |

| CAPEX Race Among Gulf-funded "Green Gold" Refiners | +0.8% | Red Sea governorate, Eastern Desert | Medium term (2-4 years) |

| Carbon-Credit Revenue-Sharing Pilots Lowering Payback on Energy-Efficient Crushers | +0.6% | National, early adoption in industrial zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast-Tracking of USD 1.2 Billion Abu Tartour Phosphate Downstream Complex

The Golden Triangle hosts roughly 1 billion tons of phosphate ore, giving the new Abu Tartour complex a natural feedstock base[1]“Corporate Fact Sheet 2024,” Misr Phosphate Company, misrphosphate.com. Egypt ranks eighth worldwide in phosphate rock, so shifting from ore shipping to phosphoric-acid and fertilizer output creates steady demand for rotary kilns, horizontal dryers, and triple-superphosphate granulators. Misr Phosphate’s existing five-million-ton platform provides operational synergies, while newly negotiated off-take agreements lock in feed for wet-process phosphoric acid units. Equipment makers supplying corrosion-resistant pumps and fluorine scrubbers find early-mover advantage as the complex targets commissioning before 2027.

Growing Domestic Gold-Ore Throughput at Sukari & Other New Mines

Centamin produced 450,058 ounces at Sukari in 2024 and targets a steady 500,000-ounce annual run-rate after its reinvestment program, sustaining an 88.7% recovery through advanced gravity-CIP circuits. Discoveries exceeding a million ounces in the Eastern Desert are prompting Shalateen Mineral Resources Company to budget more than USD 1 billion for fresh plants that require large-capacity primary crushers, SAG mills, and CIL tanks. A state-backed refinery in Marsa Alam, designed for 1 million ounces a year, further widens the intake funnel for downstream lines. Together with in-situ leaching pilots calling for specialized solvent extraction columns, these projects anchor the Egyptian mineral processing equipment market for gold through 2030.

National Hydrogen-Steel Roadmap Boosting Demand for High-Grade Iron-Ore Processing

Egypt turned out 9.8 million tons of crude steel in 2024, ranking second in the MENA bloc. Ezz Steel’s Alexandria complex already operates a 3.1 million-ton Midrex DRI module fed by 6 million tons of pellets annually, illustrating the feed scale for low-carbon steelmaking. The national hydrogen roadmap requires more than three-fifths of Fe pellets, lifting the appetite for high-intensity grinding, reverse flotation, and magnetic separation lines. Financing channels under the EIB green-loan window shave interest costs on energy-efficient HPGRs and vertical roller mills, making these technologies integral to future iron-ore upgrades[2]“EGY-Green Industry Loan Facility,” European Investment Bank, eib.org .

Mandatory Local-Content Policy in Egypt’s 2024 Mining Law Amendments

Egypt’s 2024 Mining Law Amendments had already eased production-sharing rules, but the 2024 update moved the needle by prescribing minimum local content for machinery sourced under new concessions. OEMs such as Metso and FLSmidth are weighing knock-down kit assembly near the Suez Canal Economic Zone to beat tariff penalties and to qualify for royalty discounts. The policy also obliges miners to earmark part of revenue for local community projects, indirectly boosting spending on modular plants that can be relocated to remote concessions and later offered for SME use, reinforcing the circular deployment of equipment assets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Foreign-Currency Shortage Delaying L/Cs | -1.4% | National, acute in import-dependent regions | Short term (≤ 2 years) |

| Chronic Grid Instability Outside Cairo–Suez Industrial Corridor | -0.9% | Remote mining areas, Eastern Desert | Medium term (2-4 years) |

| Volatile Phosphate Export Taxes Reducing Investment Certainty | -0.8% | Upper Egypt, Western Desert phosphate zones | Medium term (2-4 years) |

| Water-Scarcity Regulations Limiting Wet-Processing Permits | -0.6% | Upper Egypt, desert mining areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Foreign-Currency Shortage Delaying L/Cs for Imported Heavy Equipment

Egypt tightened L/C rules in late 2024, freezing many inbound equipment consignments until the Central Bank exempted raw-material inputs in 2025. Spare-part vendors still queue weeks for currency, inflating lead times and forcing miners to cannibalize idle fleets. The USD 35 billion ADQ deal at Ras El-Hekma promises a liquidity boost. Still, FX reforms and pension-fund dollarization must land before import pipelines flow normally, prolonging a cautious capex stance among mid-tier producers.

Chronic Grid Instability Outside Cairo–Suez Industrial Corridor

Remote gold and phosphate camps operate on diesel gensets that cost triple the national tariff, making full automation uneconomic until micro-grid solar hybrids stabilize. Siemens added 14.4 GW from three combined-cycle plants, yet last-mile distribution upgrades lag, prompting miners to specify variable-frequency drives and dual-fuel burners for power flexibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mineral Mining Sector: Phosphate Core, Lithium Rising

The phosphate branch captured 34.37% of the Egyptian mineral processing equipment market 2024, catalyzed by the Golden Triangle’s billion-ton inventory and the Abu Tartour complex fast-track. Gold remains a close second on capex momentum from Sukari and new Eastern Desert deposits. Lithium is the standout growth pocket, posting a 6.67% segment CAGR as upstream explorers map spodumene veins near Wadi Ghadir. The Egyptian mineral processing equipment market size for lithium‐ready circuits could top by 2030 if a single commercial concentrator reaches nameplate. Iron-ore systems ride the hydrogen-steel roadmap, while bauxite, copper, and niche manganese projects form a long-tail that triggers modular demand spikes.

Stronger environment and health and safety compliance push each mineral stream toward finer grind sizes and selective flotation, favoring high-shear conditioners and column cells. Local fabricators are moving into phosphate dryer shells and gold elution columns, but complex components such as lithium calciner burners still depend on imports. This aligns with the local-content roadmap, which phases higher thresholds after 2028.

By Equipment Type: Crushers Ahead, Mills Moving Faster

Crushers accounted for 26.51% of the Egyptian mineral processing equipment market in 2024, reflecting the prevalence of surface bulk-ore operations. Yet mills and screens carry the top CAGR at 6.61% because downstream complexes need tighter liberation to meet export-grade specs. The Egyptian mineral processing equipment market share for hybrid HPGR–ball-mill layouts is rising as phosphate and iron-ore lines seek around one-fifths energy savings.

Conveying and material-handling skids gain traction inside the Suez logistics triangle that now hosts AD Ports’ multimodal terminals. Pumps, valves, and wet-classification gear sustain stable pull despite emerging dry-processing shifts because gold, phosphate, and silica plants still require water transport. Integrated vendors bundling digital SCADA, IIoT sensor kits, and predictive analytics enjoy up to 10% of bid-score premiums on EPC contracts.

By Mining Method: Surface Dominant, Underground Accelerating

Surface pits still constitute 73.29% of the Egyptian mineral processing equipment market size as of 2024, bolstered by shallow phosphate and ironstone horizons. However, underground lines exhibit a 6.59% CAGR on the back of deeper gold shoots and narrow vein copper zones. Underground payload size constraints favor compact jaw crushers, high-torque hoists, and split-feed chutes.

Battery-electric LHDs and emission-free ventilation packages are entering feasibility models, partly to tap EIB green finance. Surface fleets are trending toward autonomous haulage retrofits that reduce operator count by one-fifths, translating into higher demand for LiDAR‐equipped drill rigs and collision-avoidance-enabled primary crushers.

By Automation Level: Semi-Automated Leads, Full Automation Accelerating

Semi-automated circuits led the Egyptian mineral processing equipment market with 47.83% share in 2024 because PLC upgrades on legacy plants deliver quick productivity wins without wholesale rebuilds. Fully automated solutions post the fastest 6.77% CAGR because mine-to-mill integration underpins export contracts that mandate consistent product chemistry.

Hybrid sensor packages merging XRT sorting, online PSD analyzers, and AI-driven grind-control loops gradually replace human operator set-points. Manual operations persist in artisanal pits and pilot plants, but their share slips slightly by 2030 as training grants spread digital know-how, aligning with the government’s massive export target that hinges on volume and quality consistency.

Geography Analysis

Historically, Egypt’s mineral supply chain concentrates within the Cairo-Suez industrial corridor, where grid reliability, rail spurs, and export piers converge. The Eastern Desert forms the principal greenfield cluster as Sukari stabilizes 500,000-ounce production. Shalateen’s million-ounce discovery spurs joint ventures to install new crushing‐grinding trains along the Red Sea coast. Gulf capital inflows, such as AD Ports’ East Port Said zone, multiply warehousing and free-zone perks, drawing OEMs to pre-position spares near the Suez Canal.

Upper Egypt’s Qena governorate represents the most significant step-change in equipment consumption because the Abu Tartour complex demands end-to-end flowsheets from feeder breakers to phosphoric-acid evaporators. Water-scarcity rules tilt flowsheet design toward dry-beneficiation modules, and solar hybrid power rigs substitute for unstable grid supply outside the corridor. The Western Desert adds a future node with its planned phosphate and silica complexes. At the same time, New Alamein’s silicon plant will deploy specialist magnetic separators and fine-grind mills to process quartz sourced from 40 million tons of reserves.

Alexandria and the Suez Canal Economic Zone form the backbone for iron-ore pellets and hydrogen steel because Ezz Steel’s jetty unloads 6 million tons of pellets yearly, demonstrating bulk-handling volumes that justify high-throughput stacker-reclaimers and shiploaders. National Service Projects Organization’s marble and granite quarries at Beni Suef add a public-sector buyer that often bundles military logistics into procurement, giving local assemblers a foothold and raising transparency concerns over tendering.

Mordor Intelligence examines the mineral processing equipment market across diverse other regional markets as well, offering granular country-level perspectives for Morocco, South Africa, Brazil, Saudi Arabia, Australia, China, Canada, Germany, and France and more.

Competitive Landscape

The Egyptian mineral processing equipment market is moderately fragmented. FLSmidth posted just a percent above rise in mining service orders during 2024, yet logged a revenue dip as miners deferred mega orders amid currency shortages, signaling cautious expansion budgets[3]“Annual Report 2024,” FLSmidth, flsmidth.com . Metso's and Planet Positive, strengthening its hand on energy-efficient crushers and stirred-media mills prized by phosphate and gold complexes. Epiroc’s Q1 2025 orders climbed around one-fifth of its revenue from last year due to automation and battery equipment lines, even while civil construction cooled, suggesting that mining remains its core engine[4]“Interim Report Q1 2025,” Epiroc AB, epiroc.com .

Mandatory local-content thresholds push international brands toward Suez or Alexandria assembly hubs. FLSmidth is exploring a knock-down kit model with Egyptian Steel, Metso has signed a digital-services pilot with Centamin, and Weir Minerals is weighing expanding its Cairo pump refurbishment center. Regional challengers from Turkey and China offer a discount but face tighter vetting due to EU CBAM compliance and warranty concerns.

Service bundles, including performance-based maintenance contracts, gain traction as miners fight L/C delays that limit inventory stocking. OEMs can finance in Egyptian pounds or quote in EUR, under EIB climate-facility eco-loans, which hold a strategic edge. Automation vendors partnering with telcos on 5G private networks accelerate full-stack solutions that combine hardware, analytics, and telecom, an emerging differentiator as underground mines go digital.

Egypt Mineral Processing Equipment Industry Leaders

FLSmidth A/S

Metso Outotec

Sandvik AB

The Weir Group PLC

Komatsu Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AD Ports Group signed a 50-year concession with the Suez Canal Economic Zone to build the 20 km² KEZAD East Port Said industrial and logistics park, committing USD 120 million to Phase 1 for quays, warehouses, and utilities.

- July 2024: The European Investment Bank approved EUR 271 million in blended finance to help Egyptian industries curb pollution and enhance energy efficiency. EUR 135 million was earmarked for loans and a EUR 30 million EU grant, with mineral processing projects prioritized under the scheme.

Egypt Mineral Processing Equipment Market Report Scope

| Bauxite |

| Iron |

| Lithium |

| Phosphate |

| Gold |

| Others |

| Crushers |

| Feeders |

| Conveyors |

| Drills & Breakers |

| Mills & Screens |

| Pumps & Valves |

| Others |

| Surface Mining |

| Underground Mining |

| Manual |

| Semi-Automated |

| Fully Automated |

| By Mineral Mining Sector | Bauxite |

| Iron | |

| Lithium | |

| Phosphate | |

| Gold | |

| Others | |

| By Equipment Type | Crushers |

| Feeders | |

| Conveyors | |

| Drills & Breakers | |

| Mills & Screens | |

| Pumps & Valves | |

| Others | |

| By Mining Method | Surface Mining |

| Underground Mining | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated |

Key Questions Answered in the Report

How fast is equipment demand for mineral processing expanding in Egypt?

Demand is growing at a 6.54% CAGR between 2025 and 2030, taking the Egyptian mineral processing equipment market size from USD 0.11 billion to USD 0.15 billion.

Which mineral type uses the most processing equipment in Egypt?

Phosphate accounts for 34.37% of 2024 equipment revenue because of the Abu Tartour downstream complex and other value-added fertilizer projects.

What is the main obstacle to importing new processing machinery?

Short-term foreign-currency shortages delay letters of credit, lengthen delivery times, and raise financing costs for imported heavy equipment.

Where are greenfield projects driving new orders?

The principal greenfield hotspots are the Eastern Desert for gold, Upper Egypt’s Golden Triangle for phosphate, and the Suez Canal Economic Zone for multi-mineral hubs.

How is automation adoption evolving?

Semi-automated lines dominate now, but thoroughly fully automated circuits post the fastest 6.77% CAGR because miners seek higher recovery, lower labor exposure, and energy savings.

Which suppliers are currently the most active in Egypt?

FLSmidth, Metso, Sandvik, Epiroc, and Weir Minerals headline the market, with local assemblers entering under new local-content incentives.

Page last updated on: