Saudi Arabia Cash Management Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

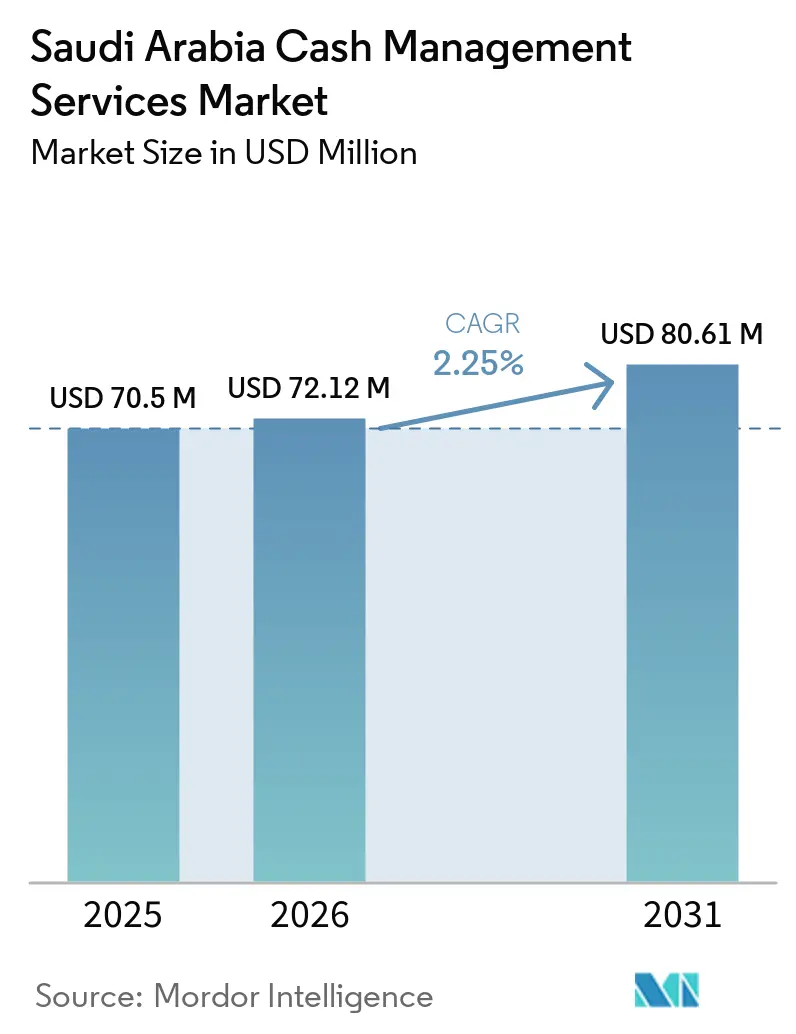

| Base Year Market Size (2025) | USD 70.5 Million |

| Market Size (2026) | USD 72.12 Million |

| Market Size (2031) | USD 80.61 Million |

| Growth Rate (2026 - 2031) | 2.25% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cash Management Services Market Analysis by Mordor Intelligence

The Saudi Arabia cash management services market size is projected to expand from USD 70.50 billion in 2025, USD 72.12 billion in 2026, to USD 80.61 billion by 2031, registering a CAGR of 2.25% between 2026 and 2031. Currency outside banks reached SAR 244.3 billion in Q2-2025, yet electronic‐payment penetration climbed to 79% of total transactions in 2024, prompting providers to migrate from volume-driven replenishment toward higher-margin smart-safe, forecasting and analytics products. ATM replenishment remains the largest revenue stream, but the acceleration of real-time payment rails compresses float income and forces operators to rethink route economics and working-capital models. Vision 2030 public-private partnerships are pushing ATM coverage deeper into rural governorates, generating temporary cash-surge arbitrage during Hajj and Umrah seasons while simultaneously sowing the seeds for wallet-based displacement of vault cash. Corporate treasurers are also consolidating liquidity positions: open-banking APIs and AI-driven forecasting now allow same-day sweeps, shrinking safety-stock buffers at bank branches and industrial sites. Against this backdrop, the Saudi Arabia cash management services market is navigating a delicate balance between safeguarding physical currency flows and monetizing digital liquidity insights.

Key Report Takeaways

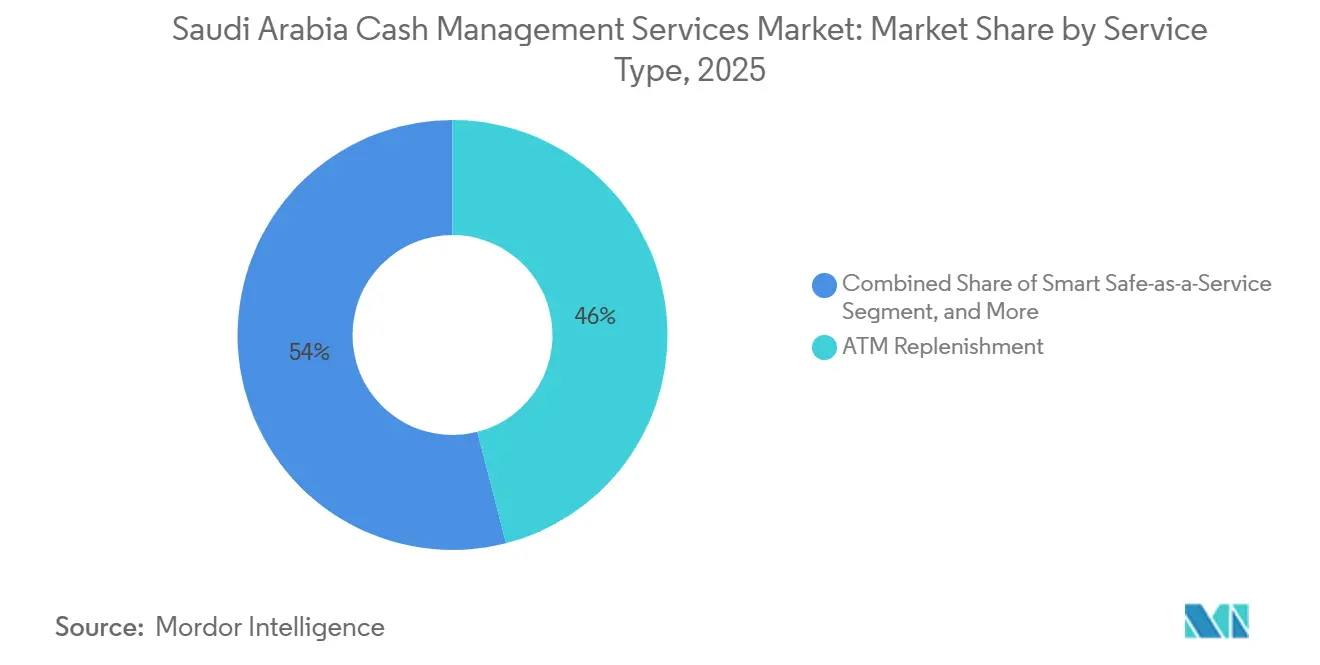

- By service type, ATM replenishment commanded 46% of 2025 revenue, while smart safe-as-a-service is forecast to post the fastest 2.48% CAGR through 2031.

- By end-user, banking and financial institutions held 33.5% share in 2025, whereas petrochemicals and industrial parks represent the quickest-expanding vertical at a 2.81% CAGR to 2031.

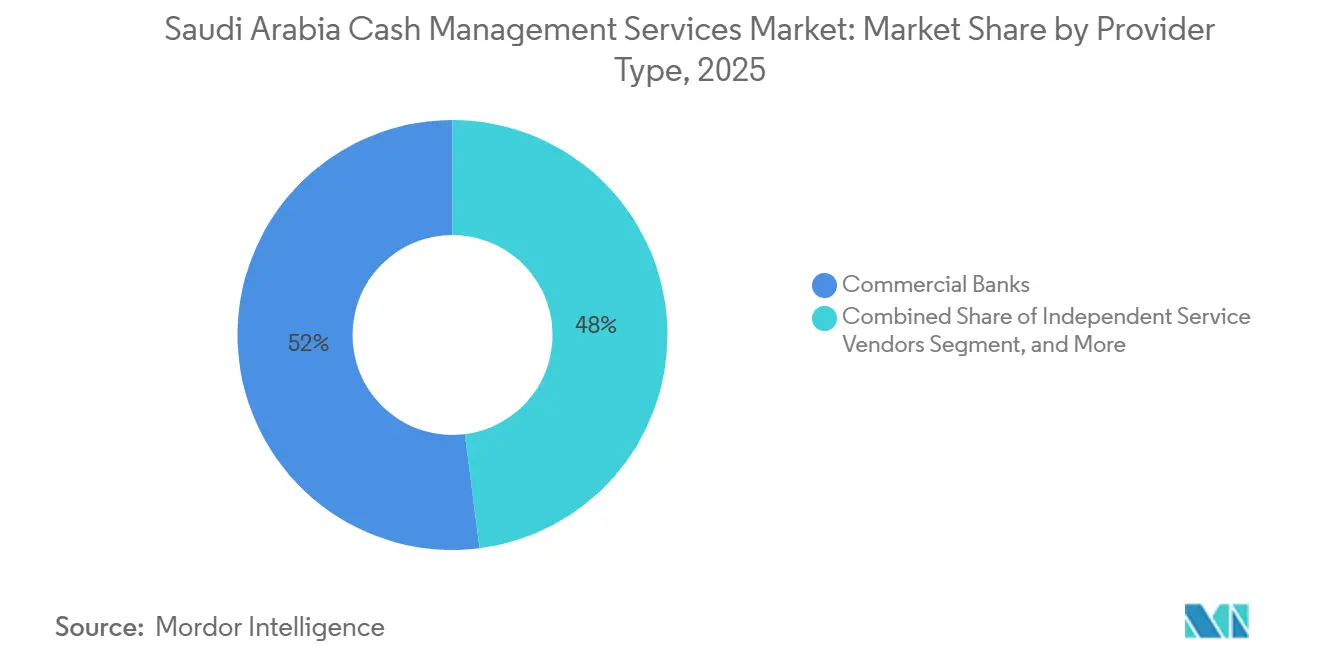

- By provider type, commercial banks led with 52% of 2025 sales, but independent service vendors are projected to accelerate at a 2.77% clip over the forecast horizon.

- By mode, outsourced models already account for 68% of spending and are advancing at a 2.96% CAGR, outpacing the in-house alternative.

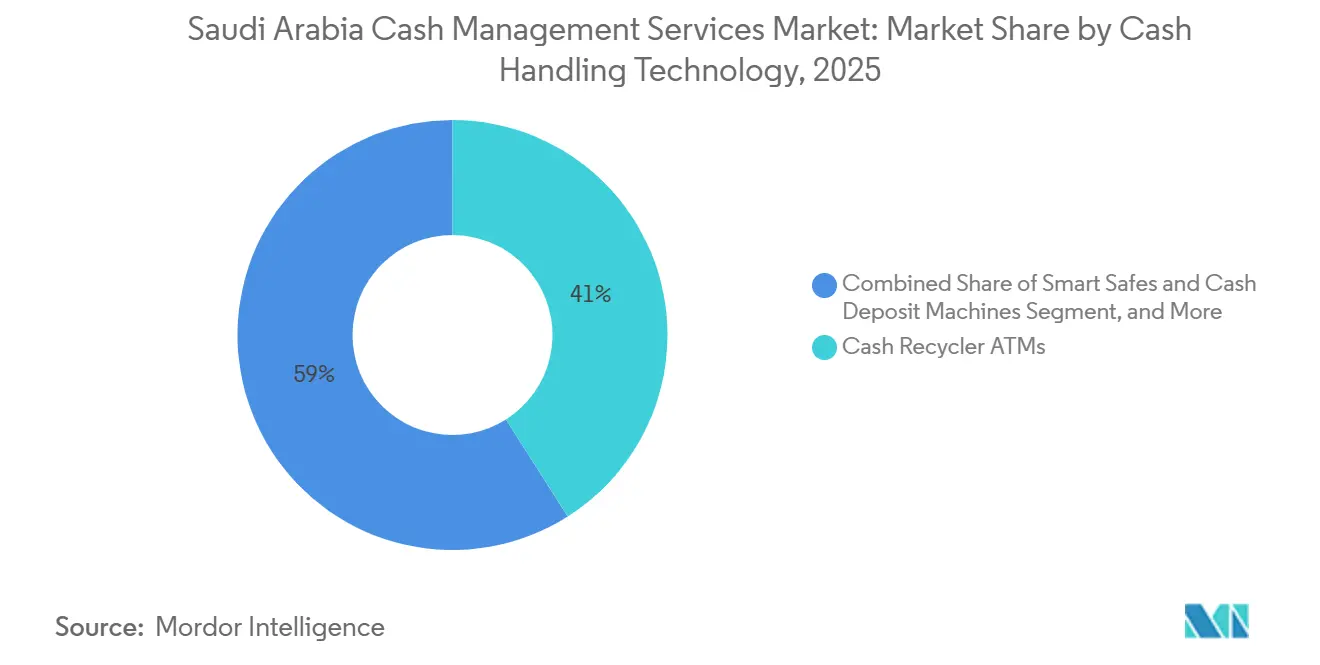

- By technology, cash recycler ATMs captured 41% share in 2025; smart safes and cash deposit machines are growing the fastest at 3.01% between 2026 and 2031.

- By cash-volume band, high-volume sites above SAR 5 million monthly processed 49% of 2025 value and are expanding at the segment-leading 3.22% rate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Saudi Arabia Cash Management Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Automation and Working Capital Optimisation | +0.60% | National, concentrated in Riyadh, Jeddah, Dammam financial hubs | Medium term (2-4 years) |

| Rising Debit and Credit Card Issuance Boosting Vault-Cash Velocity | +0.50% | National, with higher intensity in urban centers | Short term (≤ 2 years) |

| Rapid Adoption of AI-Driven Cash-Forecasting Platforms | +0.40% | National, early adopters in Tier-1 banks | Medium term (2-4 years) |

| Vision 2030 PPP Roll-outs Expanding Rural ATM Footprint | +0.30% | Rural governorates, Northern Border, Jazan, Najran | Long term (≥ 4 years) |

| Migration of Cash-Heavy Oil and Gas Payrolls to Smart-Safe Networks | +0.30% | Eastern Province industrial corridors, Yanbu, Jubail | Medium term (2-4 years) |

| Seasonal Hajj/Umrah Peaks Creating Predictable Cash-Surge Arbitrage | +0.20% | Makkah, Madinah, Jeddah gateway | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Automation and Working Capital Optimisation

Corporations are tightening liquidity controls, compressing days-sales-outstanding cycles and shifting cash management from an operational cost center to a strategic treasury lever.[1]PwC Middle East, “Working Capital Optimisation in the GCC,” pwc.com Automated reconciliation platforms now stream point-of-sale data into bank vault systems in near real time, slashing manual matching windows from two days to mere hours. Open-banking standards lower integration friction by exposing standardized payment-initiation and account-information APIs, which cuts onboarding expense and accelerates time to value. Commercial banks are responding by embedding cash-forecasting widgets within corporate portals, enabling CFOs to visualize projected cash positions and dial service levels accordingly. The margin upside for vendors comes from bundling analytics subscriptions alongside physical logistics, an approach that helps offset declining per-transaction fees as digital payments cannibalize cash volume. Treasury teams increasingly benchmark providers not only on pickup punctuality but also on forecast accuracy, making data fluency a must-have capability in the Saudi Arabia cash management services market.

Rising Debit and Credit Card Issuance Boosting Vault-Cash Velocity

Card penetration keeps rising, yet cash withdrawal counts remain lively in semi-urban provinces where merchant acceptance infrastructure trails consumer adoption. Each new cardholder effectively becomes both a digital spender in metropolitan malls and a cash user in peri-urban convenience outlets, thereby increasing the churn rate of banknote inventories. ATM operators must therefore maintain dense urban and semi-urban routes, absorbing higher per-stop costs but creating a moat of geographic scale that deters late entrants. International card acceptance also surges during tourism peaks, lifting withdrawal volumes even as e-commerce diverts in-store spending. The paradox sustains vault-cash velocity and buys incumbents time to pivot toward value-added technology layers inside the Saudi Arabia cash management services market.

Rapid Adoption of AI-Driven Cash-Forecasting Platforms

Banks are replacing heuristic refill schedules with predictive engines that ingest multivariate signals, transaction history, weather forecasts, event calendars, and mobility data to predict cash demand within a 5% error band. Cutting safety-stock buffers by a quarter unlocks idle capital, while shrinking emergency call-outs curbs fuel and labor expense. API-ready telemetry now streams directly from recyclers and smart safes into cloud dashboards, allowing dispatchers to resequence routes on an hourly cadence. Integration challenges persist because legacy note sorters often lack modern endpoints, forcing banks to deploy middleware layers, but the payoff in operating-expense relief continues to justify the transformation spend. As accuracy improves, treasury leaders treat forecast quality as a procurement KPI, shifting share toward providers that can prove algorithmic competence in the Saudi Arabia cash management services market.

Vision 2030 PPP Roll-outs Expanding Rural ATM Footprint

Government-sponsored projects aim to close the financial-inclusion gap by subsidizing ATM deployments in underserved districts where density lags by an order of magnitude. Solar-powered units and mobile-data backhauls reduce operating costs and align with sustainability commitments. Although rural machines yield lower per-unit revenue, multi-year service agreements with municipal councils guarantee minimum replenishment frequencies, de-risking capital outlays. Longer drive times and limited road infrastructure inflate logistics overhead, pushing operators to invest in dynamic scheduling algorithms and heavier-duty armored trucks. Vendors that master rural economics can tap fresh revenue pools and cement early-mover advantage before wallet-based solutions mature in these regions of the Saudi Arabia cash management services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Shift towards Non-Cash Payments | -0.70% | National, most pronounced in Riyadh, Jeddah metropolitan areas | Short term (≤ 2 years) |

| Rising Security-Compliance Costs under New SASO Rules | -0.40% | National, affecting all licensed CIT operators | Medium term (2-4 years) |

| Software Incompatibility and Skills Gaps during Network Expansions | -0.30% | National, concentrated in mid-tier banks and independent vendors | Medium term (2-4 years) |

| Tightening Cash-in-Transit Insurance Capacity and Premium Spikes | -0.20% | National, with spillover from global reinsurance markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift Towards Non-Cash Payments

Instant-payment rails, wallet apps and buy-now-pay-later platforms are eroding the transaction base that once justified dense ATM networks. Electronic payments already account for the majority of transaction counts, and the share is climbing, especially in retail categories such as groceries and fuel. E-commerce is compounding the drag by diverting consumer outlays away from cash-heavy brick-and-mortar lanes. Operators must therefore pivot from per-transaction pricing to subscription-style analytics offerings, but retraining sales teams to pitch treasury value rather than physical pickups is proving a cultural hurdle. The shift lowers route density, inflates per-stop costs and compresses the top line at a faster pace than opex can be taken out. Unless vendors diversify into software, their relevance inside the Saudi Arabia cash management services market risks steady decline.

Rising Security-Compliance Costs Under New SASO Rules

Biometric vault access, GPS telemetry, redundant storage sites and ISO certifications now form mandatory compliance baselines. Capital expenditures for vehicle retrofits, sensor arrays and control-room software have jumped, squeezing margins for smaller operators with thin balance sheets. Insurers, in parallel, demand evidence of upgraded controls before quoting premiums, heightening cost pressure. Consolidation is accelerating because sub-scale firms cannot amortize investments across wide route networks. For clients, higher compliance outlays translate into elevated service tariffs, potentially nudging cost-sensitive retailers to accelerate digital-payment migrations, thereby compounding demand risk for the Saudi Arabia cash management services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Smart Safes Edge Ahead as Replenishment Matures

The ATM replenishment category anchored 46% of 2025 revenue and remains the historical backbone of the Saudi Arabia cash management services market share. Growth, however, is decelerating as instant-payment systems trim withdrawal frequency, allowing banks to lengthen refill cycles and cut float inventory. Smart safe-as-a-service, while smaller in absolute terms, is widening fastest at a 2.48% CAGR because retail chains, petrochemical refineries and quick-service restaurants crave end-of-shift reconciliation without next-day bank runs.

Adopters receive provisional credit within hours, freeing working capital and reducing shrinkage. Providers meanwhile secure multi-year leasing contracts that bundle hardware, cloud dashboards and predictive algorithms, lifting average revenue per unit. Cash supply to bank branches and cash collection services still deliver meaningful volume, yet their trajectory slackens as branch rationalization and buy-now-pay-later uptake dilute depot-bound flows. Maintenance and managed-service lines look resilient because the installed base of recyclers and smart safes requires firmware updates and sensor calibration, ensuring a steady annuity stream in the Saudi Arabia cash management services market.

By End-User Industry: Petrochemicals Propel Near-Term Expansion

Banking and financial institutions contributed 33.5% of 2025 demand, but branch closures and wallet adoption cap their forward climb. Petrochemicals and industrial parks, in contrast, enjoy the strongest 2.81% CAGR because large continuous-process plants must reconcile shift wages on a rolling basis. Smart safes embedded inside refinery payroll offices eliminate manual counting and nighttime cash trucking, trimming security exposure while satisfying expatriate labor cash preferences.

Organized retail chains follow closely, leveraging recyclers to shrink cash drawers and improve in-store productivity, whereas unorganized retail lags due to fragmented ownership and hesitant credit relationships. Hospitality and government segments move in step with tourism mega-projects and wage-digitization mandates, respectively, each growing modestly yet consistently within the Saudi Arabia cash management services market size narrative.

By Provider Type: Independent Vendors Harvest API Agility

Commercial banks still controlled 52% of 2025 revenue through captive networks and cross-selling synergies. Yet their average growth trails because regulatory capital and digital priorities crowd out logistics investments. Independent service vendors, by contrast, pair RFID-sealed cash bags with cloud dashboards that interface directly with open-banking APIs, letting mid-tier banks outsource logistics while retaining client control. This agility fuels a 2.77% CAGR and steadily lifts vendors’ slice of the Saudi Arabia cash management services market size.

Cash-in-transit specialists occupy the middle ground: route density, insurance buying power and fleet resale value underpin reliable cash-flow generation, but organic acceleration stays muted without strong software differentiation. Hybrid partnerships are emerging wherein banks lend vault infrastructure while tech vendors handle forecasting code, combining regulatory reach with SaaS economics.

By Mode: Outsourcing Dominates Liability Transfer

Two-thirds of 2025 spending occurred under outsourced contracts, and that share is rising as corporates offload armored-truck liability, compliance overhead and cap-ex intensity. Insurance markets have hardened, with premiums up double digits since 2024, pushing treasurers to wrap risk inside vendor invoices rather than maintain stand-alone policies. Vendors respond by accepting full-liability clauses up to SAR 10 million, banking on route density and telematics to temper claim frequency.

In-house fleets persist only where security clearance or national-interest considerations trump cost, such as within petrochemical plants or state-owned utilities. Even there, co-managed arrangements that splice vendor forecasting software onto captive vaults are gaining acceptance, signaling a gradual migration toward asset-light models across the Saudi Arabia cash management services market.

By Cash Handling Technology: Recyclers Lead, Safes Surge

Cash recycler ATMs accounted for 41% of 2025 technology value, favored for their dual deposit-dispense function that halves refill frequency and credits customers within hours. Smart safes and cash deposit machines grow fastest at 3.01% because cellular modems, tamper sensors and ERP integrations allow retailers to lock tills in minutes and reconcile books before managers leave the store.

Banknote sorters and RFID bags serve as supporting infrastructure: sorters authenticate the polymer series launched in 2024, while sealed bags create immutable audit trails that reduce shrinkage and insurance cost. Dispense-only ATMs are on a slow retirement track as payment-security directives mandate EMV and contactless readiness, accelerating replacement cycles inside the Saudi Arabia cash management services market.

By Cash-Volume Band: High-Volume Sites Consolidate Gravity

Locations transacting above SAR 5 million per month contributed 49% of 2025 turnover and deliver the highest 3.22% CAGR. Mega-projects such as NEOM and the Red Sea tourism corridor compress workforce and visitor flows into dense clusters, making each service stop richly productive. Mid-volume nodes grow more slowly and face capital-expenditure pressure as regulators phase out non-secure machines. Low-volume rural ATMs remain strategically important for inclusion goals but increasingly rely on solar power, subsidy or mobile branches to cover cost of service.

Route planners therefore anchor schedules around high-volume venues and backfill spare capacity with secondary stops, a Pareto pattern that sharpens operational leverage across the Saudi Arabia cash management services market share landscape.

Geography Analysis

Riyadh, Jeddah and Dammam form the cash-intensive tripod that underpins roughly two-thirds of transactional value. Each hosts dense ATM arrays, corporate headquarters and Tier-1 data centers that feed vast streams of telemetry into forecasting engines. Urban wallets lead in digital adoption, yet the retail blend still features sufficient cash throughput to keep recycling networks profitable.

Central and Eastern provinces dominated by petrochemical and industrial estates supply the market’s most stable high-volume clients. Shift-based payrolls, temporary worker campuses and remote supply chains sustain predictable cash rhythms despite management efforts to digitize wage disbursement. Operators leverage these corridors to roll out networked smart safes, tapping high transaction densities to amortize hardware in under three years.

Northern Border, Jazan and Najran represent the developmental frontier. Vision 2030 subsidies and solar-powered ATM pilots aim to elevate inclusion, but route economics remain fragile due to long drive times and thin withdrawal counts. Armored-truck utilization therefore hinges on dynamic dispatch platforms that splice rural stops into metropolitan loops without breaching vault capacity or driver-hours ceilings. Mastery of such hybrid geography will separate scalable providers from niche incumbents within the Saudi Arabia cash management services market.[2]Alhamrani Universal, “ATM Network Statistics,” alhamrani.com

Competitive Landscape

Five firms Saudi Awwal Bank, Alhamrani Universal, ABANA, Sanid and Brink’s command about 60% of sector turnover, yielding a moderately concentrated field where both operational heft and digital capability matter. Commercial banks wield branch adjacencies and trust franchises to bundle cash management with foreign-exchange and trade-finance modules, fortifying relationship stickiness.

Pure-play cash-in-transit specialists concentrate on fleet telematics, insurance scale and 24-hour pickup guarantees, carving out mission-critical roles for high-volume retailers and ATM operators that value punctuality above all. Technology-focused disruptors, meanwhile, differentiate with AI-based cash-demand prediction and API integrations that let banks cut safety-stock buffers by a quarter. Sandboxing privileges from the central bank accelerate this software wedge, letting new entrants bypass legacy core systems.

Partnership alignments are becoming the norm: banks supply vault real estate and regulatory coverage, CIT firms manage transportation risk, and fintechs inject analytics that fine-tune route cadence. This interdependence, plus compliance cost inflation, propels selective consolidation. Overall, the Saudi Arabia cash management services market currently earns a concentration score of 6, reflecting a top-five share in the 60-70% band with meaningful but not prohibitive room for agile challengers.[3]Lloyd’s of London, “Cash-in-Transit Insurance Market Update 2024,” lloyds.com

Saudi Arabia Cash Management Services Industry Leaders

Saudi Awwal Bank (SAB)

ABANA Enterprises Group Company

Alhamrani Universal Company

Sanid (Saudi Financial Support Services Company)

Al Fareeq Security Services Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Saudi Arabia's Awwal Bank announced a USD 15 million AI-based overhaul of its cash management, projected to reduce costs by 25%.

- August 2025: NCR Corporation secured a USD 45 million contract to deploy 500 recycler ATMs nationwide.

- July 2025: G4S opened a USD 12 million hub in Jeddah, featuring hospitality-grade cash logistics.

- June 2025: SAMA issued new cybersecurity guidelines effective Jan 2026.

- May 2025: Loomis AB partnered with Finesse Global on AI-driven optimization services.

Saudi Arabia Cash Management Services Market Report Scope

The Saudi Arabia Cash Management Services Market Report is Segmented by Service Type (ATM Replenishment, Cash Collection and Processing, Cash Supply to Bank Branches, Maintenance and Managed Services, Smart Safe-as-a-Service), End-User Industry (Retail – Organised, Retail – Unorganised, Banking and Financial Institutions, Hospitality, Government and Public Sector, Petrochemicals and Industrial Parks), Provider Type (Commercial Banks, Cash-in-Transit Companies, Independent Service Vendors), Mode (Outsourced, In-house), Cash Handling Technology (Cash Recycler ATMs, Smart Safes and Cash Deposit Machines, Banknote Sorters and Validators, RFID-Based Sealed Cash Bags), and Cash Volume Band (High-Volume Sites, Mid-Volume Sites, Low-Volume Sites). The Market Forecasts are Provided in Terms of Value (USD).

| ATM Replenishment |

| Cash Collection and Processing |

| Cash Supply to Bank Branches |

| Maintenance and Managed Services |

| Smart Safe-as-a-Service |

| Retail - Organised |

| Retail - Unorganised |

| Banking and Financial Institutions |

| Hospitality |

| Government and Public Sector |

| Petrochemicals and Industrial Parks |

| Commercial Banks |

| Cash-in-Transit Companies |

| Independent Service Vendors / Technology Providers |

| Outsourced (Third-Party) |

| In-house (Self-service) |

| Cash Recycler ATMs |

| Smart Safes and Cash Deposit Machines |

| Banknote Sorters and Validators |

| RFID-Based Sealed Cash Bags |

| High-Volume Sites (More than SAR 5 mn / month) |

| Mid-Volume Sites (SAR 1-5 mn / month) |

| Low-Volume Sites (Less than SAR 1 mn / month) |

| By Service Type | ATM Replenishment |

| Cash Collection and Processing | |

| Cash Supply to Bank Branches | |

| Maintenance and Managed Services | |

| Smart Safe-as-a-Service | |

| By End-User Industry | Retail - Organised |

| Retail - Unorganised | |

| Banking and Financial Institutions | |

| Hospitality | |

| Government and Public Sector | |

| Petrochemicals and Industrial Parks | |

| By Provider Type | Commercial Banks |

| Cash-in-Transit Companies | |

| Independent Service Vendors / Technology Providers | |

| By Mode | Outsourced (Third-Party) |

| In-house (Self-service) | |

| By Cash Handling Technology | Cash Recycler ATMs |

| Smart Safes and Cash Deposit Machines | |

| Banknote Sorters and Validators | |

| RFID-Based Sealed Cash Bags | |

| By Cash Volume Band | High-Volume Sites (More than SAR 5 mn / month) |

| Mid-Volume Sites (SAR 1-5 mn / month) | |

| Low-Volume Sites (Less than SAR 1 mn / month) |

Key Questions Answered in the Report

How fast is cash demand expected to grow at industrial sites?

High-volume petrochemical and construction hubs show a 2.81% CAGR through 2031, the quickest among verticals.

Which technology is gaining ground with retailers?

Smart safes and cash deposit machines are expanding 3.01% annually as chains seek rapid provisional credit and theft reduction.

Why are independent vendors growing faster than banks?

API agility lets independents overlay forecasting software onto multiple banks, driving a 2.77% CAGR versus 2.0% for commercial banks.

What is driving outsourcing popularity among corporates?

Rising insurance rates and compliance costs push firms to shift liability to vendors, propelling outsourced contracts to 68% share.

How concentrated is provider competition?

The top five suppliers hold about 60% of revenue, placing market concentration at a moderate score of 6.

Page last updated on: