Logistics

30th MayUnlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

The Morocco Freight and Logistics Market Report is Segmented by Logistics Function (Courier Express and Parcel, Freight Forwarding, Freight Transport, Warehousing and Storage, Other Services), End User Industry (Agriculture Fishing and Forestry, Construction, Manufacturing, Oil and Gas Mining and Quarrying, Wholesale and Retail Trade, Others). The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

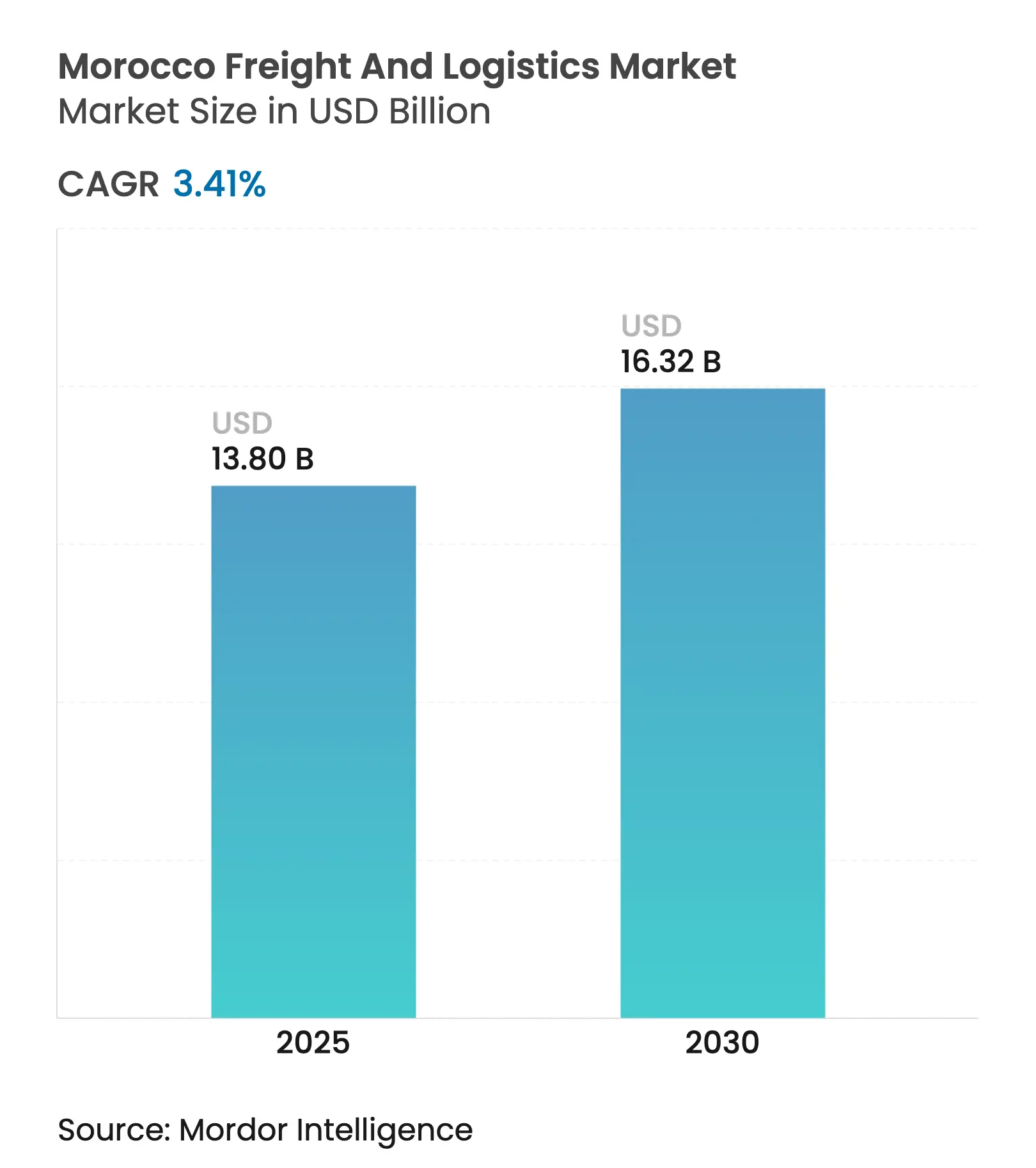

| Market Size (2025) | USD 13.80 Billion |

| Market Size (2030) | USD 16.32 Billion |

| Growth Rate (2025 - 2030) | 3.41 % CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Morocco’s advantageous location between Europe and West Africa, combined with infrastructure spending that has exceeded USD 15 billion since 2010, continues to attract manufacturing investment, stimulate multimodal integration, and reinforce the country’s role as a cross-continental gateway. Consistent gains in automotive exports, the roll-out of new free-trade zones, and customs digitalization reforms underpin steady demand for freight forwarding, warehousing, and last-mile services. Meanwhile, modal diversification toward sea and inland waterways is strengthening port–hinterland connectivity, and accelerating adoption of logistics technology is improving visibility and asset utilization. Medium-term growth opportunities concentrate in parcel logistics, temperature-controlled storage, and integrated port–rail solutions that support Morocco’s ascendant export-oriented manufacturing base.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

E-commerce and B2C parcel growth E-commerce and B2C parcel growth | +0.8% | Casablanca–Rabat corridor | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Casablanca–Rabat corridor | Impact Timeline:Medium term (2-4 years) |

Port and free-zone investment Port and free-zone investment | +0.6% | Tangier-Tetouan-Al Hoceima, Oriental | Long term (≥ 4 years) | |||

Africa–Europe trade-corridor integration Africa–Europe trade-corridor integration | +0.5% | National, focus on northern ports | Long term (≥ 4 years) | |||

Automotive OEM near-shoring Automotive OEM near-shoring | +0.4% | Tangier–Kenitra industrial axis | Medium term (2-4 years) | |||

Renewable-energy supply-chain localization Renewable-energy supply-chain localization | +0.3% | Ouarzazate, coastal wind zones | Long term (≥ 4 years) | |||

Logistics-tech start-ups & customs digitization Logistics-tech start-ups & customs digitization | +0.2% | Major ports & industrial zones | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Surge in E-commerce and B2C Parcel Volumes

Rapid digital-commerce uptake raised online card transactions to 14.3 million in 2024, lifting parcel density in the Casablanca–Rabat urban corridor and spurring capital flows into automated sortation hubs. New digital payment products are reducing the historic reliance on cash-on-delivery, improving failed-delivery ratios and encouraging investment in micro-fulfillment centers. Global platforms entering Morocco freight and logistics market are requesting end-to-end visibility and reverse-logistics capabilities, motivating 3PLs to deploy track-and-trace and route-optimization tools. These technology upgrades help operators cut urban delivery times, improve asset utilization, and scale capacity during seasonal peaks. Multinational CEP players are therefore deepening Moroccan partnerships to capture share in a segment growing faster than overall GDP[1]“Morocco – Infrastructure,” U.S. Commercial Service, privacyshield.gov.

Government Investment in Ports and Free Zones

The 2030 National Port Strategy earmarks USD 7.5 billion for upgrades across 27 ports, accelerating hinterland connectivity and lowering vessel turnaround times. Anchor projects such as Nador West Med are pairing deep-water berths with 600-hectare industrial zones financed by EUR 110 million (USD 121.40 million) from the EBRD, illustrating the state’s cluster-based approach. Dakhla Atlantic Port, budgeted at USD 1.7 billion, will open a new Atlantic gateway for Sahel trade, reinforcing Morocco freight and logistics market as a regional transshipment hub. Expanded capacity raises container throughput, encourages value-adding activities such as pre-assembly and packaging, and stimulates demand for inland transport to newly established free-trade zones[2]“Digital Morocco 2030 Strategy,” Digital Watch Observatory,dig.watch.

Integration into Africa–Europe Trade Corridors

Inclusion of Tanger Med and Casablanca in the U.S. Container Security Initiative enhances Morocco’s perception as a secure transit node, widening customer bases among trans-Atlantic shippers. Cross-border projects, including the Smara–Bir Moghrein corridor with Mauritania, are cutting transit time for mineral exports, supporting bilateral volume growth. Automotive supply chains already ship 536,000 finished vehicles to Europe, demonstrating corridor efficiency and cementing the Morocco freight and logistics market’s role in near-shoring strategies. These developments create network effects: larger volumes attract more carriers, which lower rates and further boost trade flows.

Automotive OEM Near-shoring Boosting JIT Demand

Vehicle output reached 570,000 units in 2024, translating into complex intra-Morocco flows of parts and finished vehicles that necessitate digital control towers and time-definite services. Renault’s real-time monitoring platform exemplifies data-driven orchestration that minimizes stock-outs. The upcoming USD 6.5 billion EV-battery gigafactory near Kenitra will add hazardous-materials logistics and controlled-temperature storage requirements, expanding service scope for specialized freight forwarders. As OEMs push higher localization rates, tier-1 suppliers establish nearby plants, intensifying domestic freight volumes and anchoring contract-logistics growth.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile fuel and energy prices Volatile fuel and energy prices | −0.4% | National, higher on long-haul road routes | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:−0.4% | Geographic Relevance:National, higher on long-haul road routes | Impact Timeline:Short term (≤ 2 years) |

Fragmented road-transport sector Fragmented road-transport sector | −0.3% | National, rural and inter-city corridors | Medium term (2-4 years) | |||

Insufficient cold-chain capacity Insufficient cold-chain capacity | −0.2% | Agricultural export regions | Medium term (2-4 years) | |||

Limited rail-freight capacity & gaps Limited rail-freight capacity & gaps | −0.2% | Inland industrial zones | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Fuel and Energy Prices

Diesel costs climbed to 11.26 MAD per liter in June 2025, squeezing margins for operators responsible for 85% of non-phosphate freight movements. Subsidy phase-outs pass price swings directly to haulers, forcing frequent rate renegotiations and encouraging modal shift discussions. Short-term hedging remains limited, so smaller firms struggle to forecast costs accurately, driving fleet rationalization and encouraging consolidation in the Morocco freight and logistics market[3]“Morocco’s Long Road Toward Economic Transformation,” Carnegie Endowment, carnegieendowment.org.

Fragmented Road-Transport Sector

Thousands of micro-fleets lack telematics, have limited access to bank financing, and operate older trucks that raise maintenance and fuel costs, translating into lower reliability and higher emissions. Such fragmentation complicates adoption of common digital platforms and weakens Morocco freight and logistics market efficiency. The government’s plan to professionalize drivers and introduce mandatory fleet-tracking could catalyze consolidation, though the timeline extends beyond 2027.

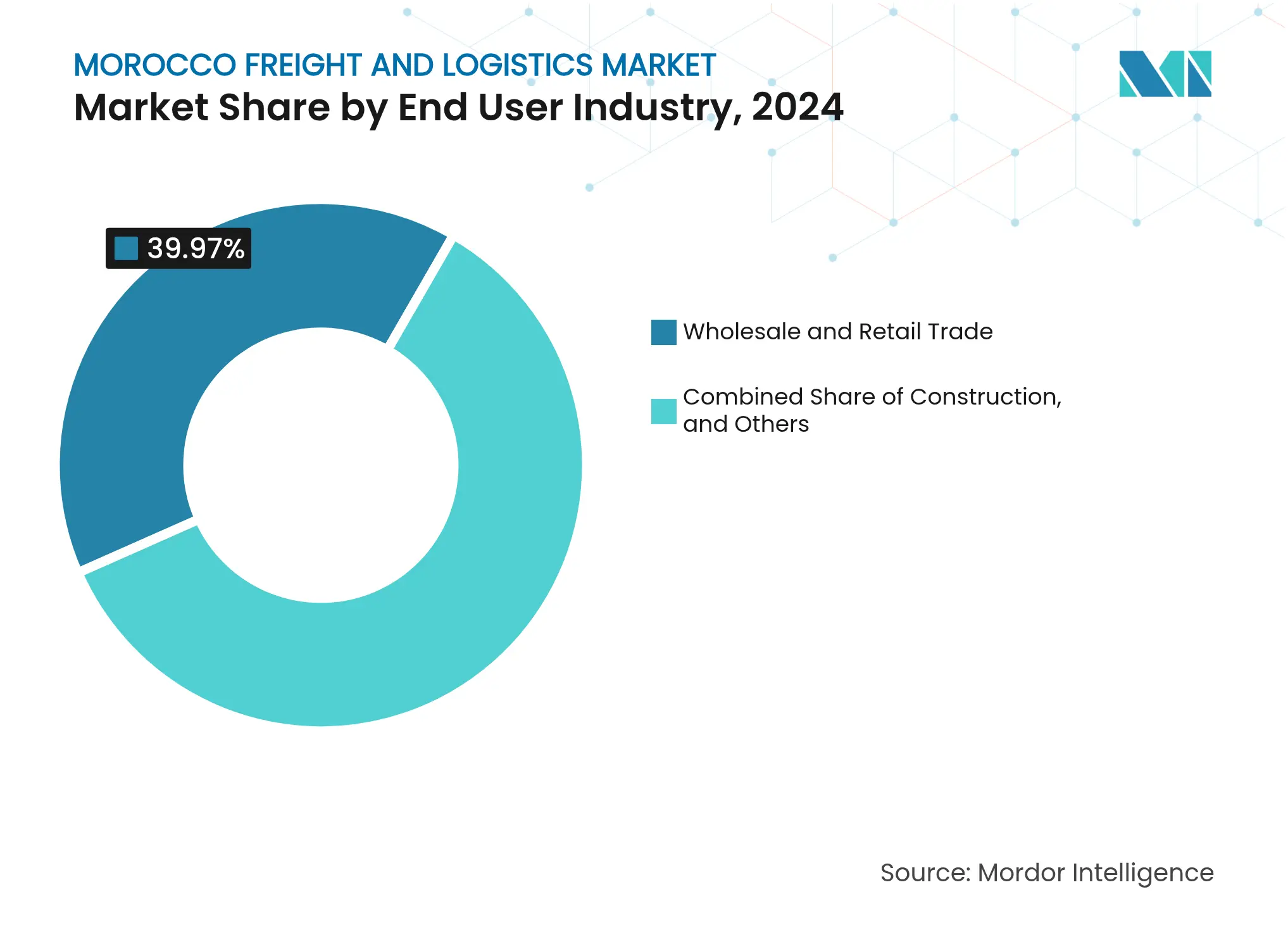

By End User Industry: Wholesale Trade Leadership Reflects Economic Diversification

Wholesale and Retail Trade captured 39.97% of 2024 demand—the largest slice of the Morocco freight and logistics market size—and is projected to post a 4.26% CAGR on the back of modern grocery formats and omnichannel expansion. Manufacturing ranks second, lifted by automotive, aerospace, and electronics clusters that require synchronized inbound flows and export dispatches.

Agriculture, Fishing, and Forestry continue to rely on fast, temperature-controlled links to European buyers, while Oil and Gas, Mining, and Quarrying hinge on bulk handling for phosphates and energy inputs. Construction logistics remains brisk as rail, port, and urban projects advance. Emerging domains such as logistics tech and specialized industrial services round out a broadening customer base, underscoring the Morocco freight and logistics industry’s role in economic modernization.

Note: Segment shares of all individual segments available upon report purchase

By Logistics Function: Freight Transport Dominance Drives Modal Integration

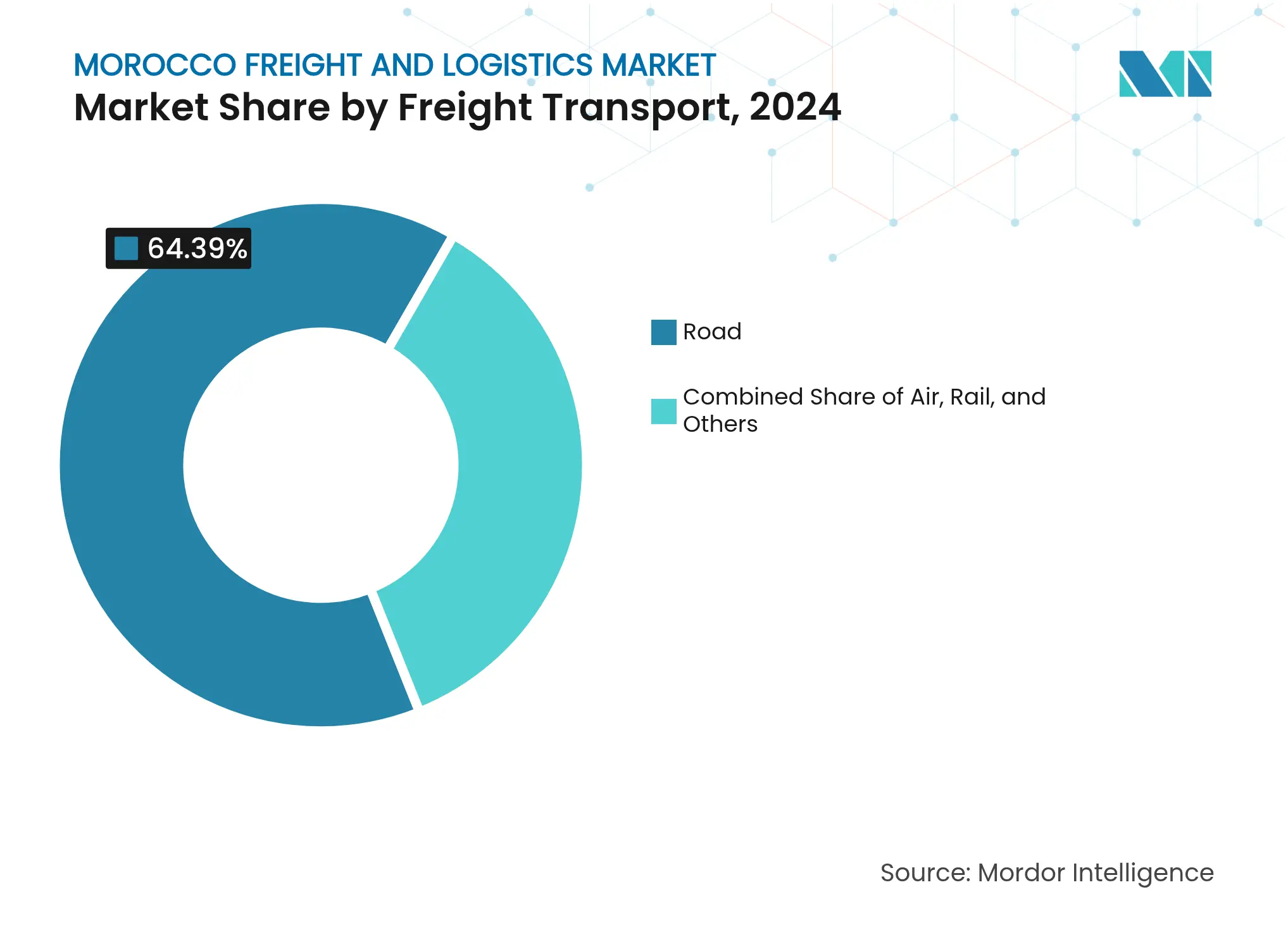

Freight Transport generated 73.26% of the Morocco freight and logistics market share in 2024, underscoring the country’s export-oriented economy and the prevalence of bulk cargo. Inside this function, road services handled 64.39% of volumes, supported by a highway grid that already stretches 1,800 kilometers and is slated to reach 3,000 kilometers by 2030. Sea and inland-waterway operations are picking up momentum, expanding at a 3.99% CAGR from 2025 to 2030 as new berths come onstream at Tanger Med and Nador West Med. Rail moves significant phosphate and automotive flows yet remains capacity-constrained when compared with maritime alternatives.

Modal diversification is reshaping service portfolios across the Morocco freight and logistics market. Courier, Express, and Parcel activities grow fastest at a 3.80% CAGR, buoyed by e-commerce demand and digital-payment adoption. Warehousing is shifting toward multi-temperature sites as providers such as Socamar add cold rooms for produce exporters. Freight Forwarding gains from Morocco’s trade-corridor role by coordinating customs and multimodal links, while technology-driven “Other Services” deliver tracking, analytics, and inventory visibility that many shippers now expect.

By Courier, Express, and Parcel (CEP): Domestic Volumes Drive E-commerce Transformation

Domestic parcels represented 66.22% of CEP traffic in 2024, reflecting the clustering of online spending in Casablanca, Rabat, and other large cities. Cross-border volumes are smaller today, yet international CEP exhibits the stronger 3.88% CAGR through 2030 as Moroccan merchants plug into European and African platforms. Online card payments reached 14.3 million in 2024, easing reliance on cash on delivery and supporting tighter delivery windows.

Network upgrades mirror these trends. Global integrators add sortation hubs near ports and airports to capture two-day Europe service, while domestic operators widen reach into secondary cities. Reverse logistics for returns, refrigerated delivery for pharmaceuticals, and same-day options in metropolitan areas are emerging as premium add-ons. Customs-clearance proficiency is now a must-have for providers that want to scale international parcel flows inside the Morocco freight and logistics industry.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Warehousing and Storage: Temperature Control Drives Premium Growth

Non-temperature-controlled space accounted for 89.22% of warehouse capacity in 2024, serving textiles, consumer goods, and automotive parts. Temperature-controlled facilities, although small, show the quickest 4.23% CAGR thanks to booming horticultural exports that demand uninterrupted cold chains.

Specialists such as Socamar are adding new chambers and backup power to meet European phytosanitary rules. International 3PLs integrate refrigerated transport, bonded storage, and value-added packaging to offer end-to-end cold-chain solutions. Persistent supply gaps invite private investment in energy-efficient designs and skilled technicians, themes central to future competitiveness in the Morocco freight and logistics market.

By Freight Transport: Road Dominance Faces Maritime Competition

Road haulage retained 64.39% of freight moves in 2024, reflecting a flexible network that will gain another 2,100 miles of expressway and 1,300 miles of highway by 2030 under a USD 9.6 billion program. This share anchors domestic distribution and just-in-time manufacturing feeds.

Yet sea and inland-waterway transport is the growth story, advancing at a 3.99% CAGR as expanded container yards shorten vessel wait times. Rail investments under the USD 37 billion Rail Morocco 2040 scheme promise future relief, but single-track stretches and passenger-train priorities still curb freight slots today. Operators diversifying into LNG trucks, biofuels, and route-optimization software position for rising sustainability requirements across the Morocco freight and logistics market.

Note: Segment shares of all individual segments available upon report purchase

By Freight Forwarding: Maritime Services Lead Multimodal Integration

Sea and inland-waterway forwarding held 71.22% of 2024 revenue and is forecast to grow at 4.11% CAGR through 2030, powered by Tanger Med’s 8.61 million TEUs and a 13.4% annual throughput rise. Air forwarding, though smaller, secures high-value cargo such as electronics and perishables by leveraging new cold-chain zones at Casablanca and Marrakech airports.

The sector is consolidating as multinationals ally with local brokers to navigate documentation and PortNet digital processes. CMA CGM’s joint venture at Nador West Med illustrates a push toward integrated port-to-inland service backed by real-time data platforms. Niche forwarders prosper in project cargo, dangerous goods, and tailor-made supply-chain solutions, rounding out a diverse Morocco freight and logistics market.

Northern regions led by Tangier-Tetouan-Al Hoceima draw the largest freight volumes owing to Tanger Med’s 8.61 million TEU throughput in 2024. High-frequency feeder services to European ports combine with integrated industrial parks to create a dense logistics ecosystem that concentrates third-party warehousing and freight-forwarding activity. Casablanca-Settat retains its role as Morocco’s commercial nucleus, leveraging the country’s busiest general-cargo port and a robust manufacturing base to anchor national distribution networks.

The Oriental region is accelerating on the back of Nador West Med, financed partly by EUR 110 million (USD 121.40 million) from the EBRD, which is fostering new metal-processing and agrifood clusters adjacent to the port. Southern provinces such as Dakhla-Oued Ed-Dahab have emerged as the fastest-growing territory, supported by the USD 1.7 billion Dakhla Atlantic Port and cross-border corridors that shorten Mauritanian iron-ore transit. Inland regions profit from highway and future rail extensions that will link 43 cities by 2040, providing hinterland access for export industries located away from the coast.

Souss-Massa stands out for agricultural exports, handling roughly 85% of Morocco’s tomato shipments, necessitating investment in cold storage, fumigation, and reefer trucking. Climate-resilience measures, including desalination plants and renewable-power microgrids, gain prominence in coastal areas to safeguard port operations against water stress. Together, these geographic shifts reinforce the Morocco freight and logistics market’s national integration while positioning it as an indispensable node in Africa–Europe value chains.

Oil and Gas, Mining, and Quarrying Segment in Morocco Freight and Logistics Market

The oil and gas, mining, and quarrying segment is experiencing robust growth in the Morocco freight and logistics market, with an expected growth rate of approximately 8% during 2024-2029. This growth is primarily driven by Morocco's position as one of the world's leading producers of high-quality phosphate, contributing significantly to the country's export earnings. The segment's expansion is further supported by recent discoveries of natural gas deposits across various regions, including Kenitra, Essaouira, Guersif, Zag, Boudnib, and Missour. The government's initiatives to develop domestic natural gas infrastructure, including plans for pipeline projects and floating storage and regasification units, are creating substantial opportunities for logistics service providers. The mining sector's strategic importance is emphasized by the government's vision to triple the sector's turnover, driving increased demand for specialized logistics services, including sea freight and air freight solutions.

Remaining Segments in Morocco Freight and Logistics Market

The remaining segments in the market include construction, distributive trade (wholesale and retail), and healthcare and pharmaceutical sectors, each contributing uniquely to the market dynamics. The construction segment benefits from ongoing infrastructure development projects and government initiatives for urban development. The distributive trade segment is being transformed by the rapid growth of e-commerce and digital retail platforms, requiring sophisticated logistics solutions. The healthcare and pharmaceutical segment, though smaller in market share, is experiencing significant transformation due to Morocco's ambitions to become a regional hub for pharmaceutical manufacturing and distribution. These segments collectively create a diverse demand profile for logistics services, ranging from specialized medical supply chain solutions to large-scale construction material transportation. The role of contract logistics is increasingly vital in managing these complex supply chain requirements.

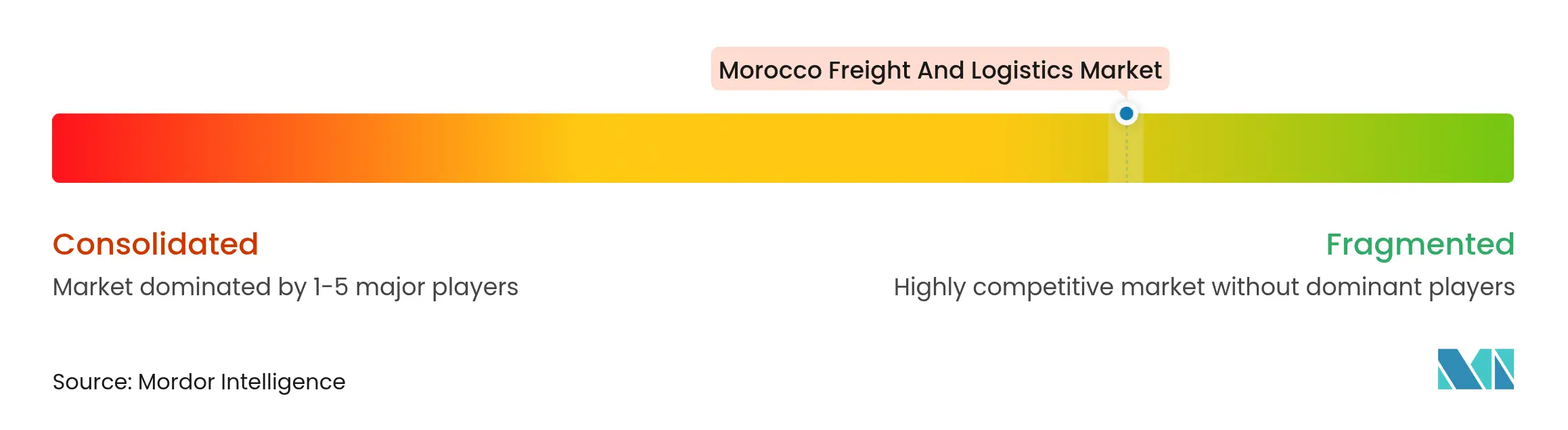

Market Concentration

The Morocco freight and logistics market remains moderately fragmented, though vertical integration is intensifying as global carriers partner with state-owned entities. CMA CGM and Marsa Maroc’s joint venture to operate half of the Nador West Med container terminal exemplifies alignment between ocean carriers and port authorities to secure capacity and end-to-end control. Maersk and Hapag-Lloyd maintain dedicated services to Tanger Med, while DHL and DSV continue expanding contract-logistics footprints inside free-trade zones.

Road haulage shows the highest operator count, yet rising compliance costs and digital-tracking mandates encourage consolidation; larger fleets leverage telematics to cut fuel burn and optimize asset turns. ONCF’s rail-freight unit is courting private-sector partners to co-develop terminals along high-speed corridors, hinting at future modal diversification. Technology investments—such as warehouse-management systems, automated guided vehicles, and AI-driven demand forecasts—differentiate service quality and underpin premium pricing.

Sustainability initiatives are moving from pilot to procurement clauses: Tanger Med’s EUR 400 million (USD 441.45 million) truck-terminal upgrade includes renewable-energy KPIs tied to IFC financing, and carriers test biofuel blends on Atlantic routes. Cold-chain specialists are eyeing solar-powered refrigeration to reduce operating costs. Overall, customer demand for transparency, reliability, and environmental stewardship is shaping competitive dynamics in the Morocco freight and logistics industry.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size and Growth Forecasts

6. Competitive Landscape

7. Market Opportunities and Future Outlook

Freight and logistics refer to the transportation of goods through air, rail, and roadways. The logistics process is defined as the planning, implementation, and control of an efficient, effective flow and storage of goods, services, or related information from the point of origin to the point of consumption.

A complete background analysis of the Moroccan logistics market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The Moroccan logistics market is segmented by function (freight transport [road, shipping and inland water, air, and rail], freight forwarding, warehousing, value-added services, and other services) and end-user (manufacturing and automotive; oil and gas, mining, and quarrying; construction, distributive trade (wholesale and retail); healthcare and pharmaceutical, and other end users (chemicals, telecommunications, etc). The report offers market size and forecasts for all the above segments in value (USD).

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

Wealth Management Intelligence for the Middle East

4 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.