Poland Cross-Border Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

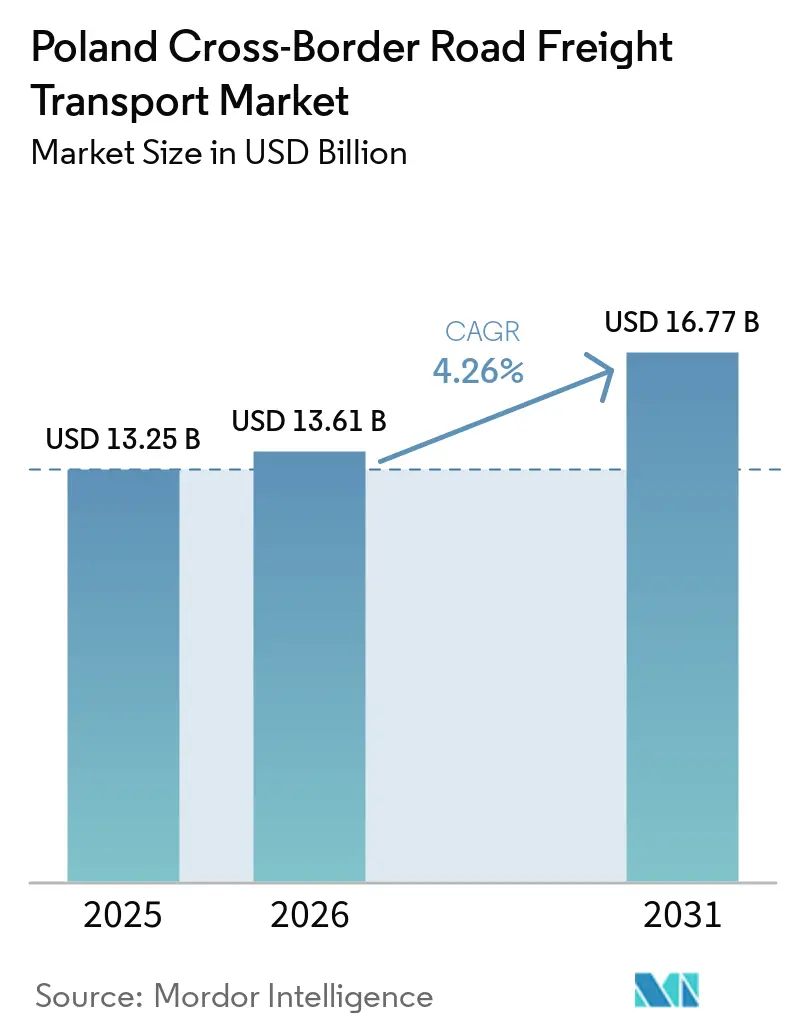

| Base Year Market Size (2025) | USD 13.25 Billion |

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 16.77 Billion |

| Growth Rate (2026 - 2031) | 4.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Poland Cross-Border Road Freight Transport Market Analysis by Mordor Intelligence

The Poland cross-border road freight transport market size is projected to expand from USD 13.25 billion in 2025 and USD 13.61 billion in 2026 to USD 16.77 billion by 2031, registering a CAGR of 4.26% between 2026 and 2031.

A strong trade pull from Germany, fresh EU funding for rail–road hubs, and surging digital-platform adoption are underpinning steady gains in the Poland cross-border road freight transport market, yet tight driver supply, rising German tolls, and cabotage compliance costs are tempering upside potential. Demand is shifting from bulk agriculture toward high-value electronics and pharmaceuticals, favoring containerized, temperature-controlled services. At the same time, near-shoring compresses average haul lengths, lifting less-than-truckload (LTL) and short-haul requirements. Consolidation momentum is accelerating after DSV’s takeover of Schenker, while platforms such as Trans.eu are squeezing legacy broker margins.[1]European Commission, “Poland–Germany Rail Freight Agreement 2025,” cinea.ec.europa.eu

Key Report Takeaways

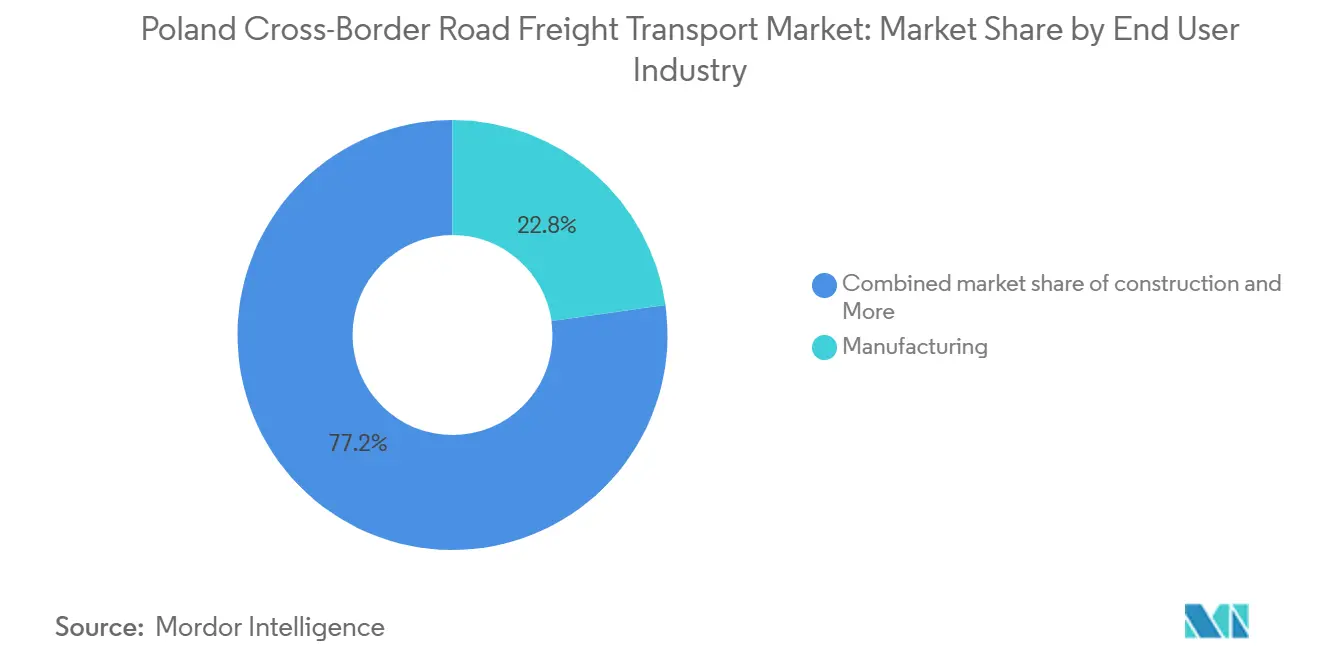

- By end user industry, manufacturing captured 22.78% of the Poland cross-border road freight transport market share in 2025, while wholesale and retail trade is projected to grow the fastest at a 4.91% CAGR to 2031.

- By truckload specification, full-truck-load held 78.61% of the Poland cross-border road freight transport market size in 2025, whereas less-than-truck-load (LTL) is poised for a 5.03% CAGR on the back of digital load-matching.

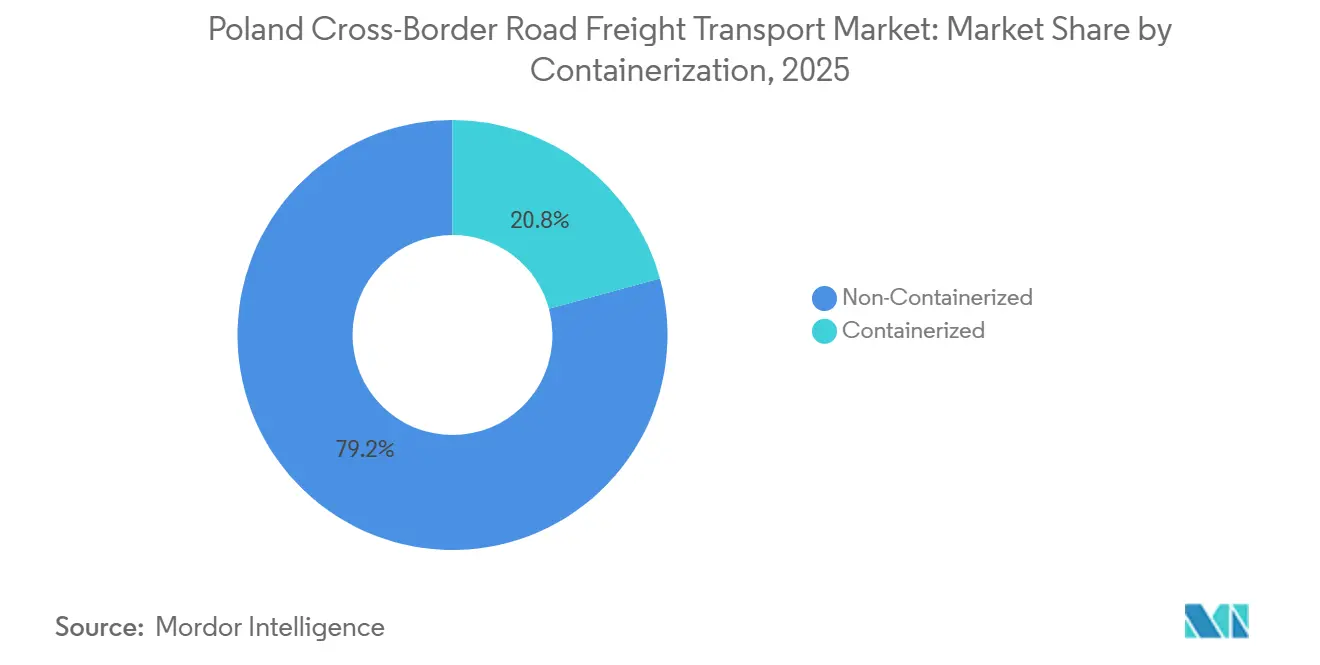

- By containerization, non-containerized freight made up 79.23% of the Poland cross-border road freight transport market share in 2025, yet containerized flows will expand at a 4.79% CAGR thanks to new intermodal terminals at Małaszewicze and Świnoujście.

- By distance, long-haul movements accounted for 62.47% of the Poland cross-border road freight transport market size in 2025; short-haul lanes are on track for a 5.08% CAGR as OEMs redraw supply radii to within 300 kilometers.

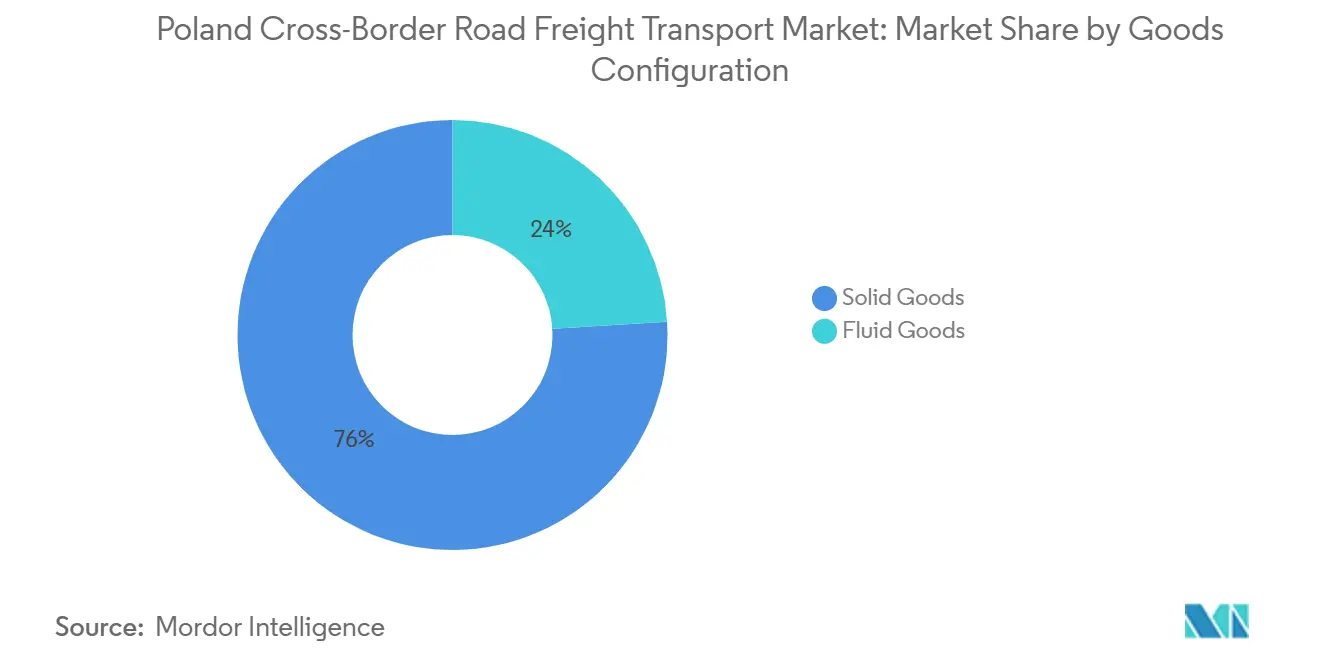

- By goods configuration, Solid Goods accounted for 75.98% of the Poland cross-border road freight transport market share in 2025, while fluid goods accounted for 4.74% and are expected to expand at a 4.74% CAGR.

- By tempreature control, Non-temperature controlled movements contributed 93.3% of the Poland cross-border road freight transport market size in 2025, temperature controlled are heading for a 4.87% CAGR.

- By country, Germany led with 35.66% of the Poland cross-border road freight transport market share in 2025; Ukraine is forecast to record the fastest 5.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Poland Cross-Border Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Re-routing of EU supply chains via the Poland–Germany corridor | +1.2% | Poland–Germany border, spillover to the Czech Republic and Slovakia | Medium term (2-4 years) |

| Near-shoring of Western OEMs to Poland & Czechia Republic | +1.1% | Polish and Czech production clusters | Medium term (2-4 years) |

| Post-2027 EU Mobility Package harmonization | +0.9% | EU-wide, concentrated enforcement in Germany, France, and Belgium | Long term (≥ 4 years) |

| Rapid uptake of digital freight platforms | +0.7% | Core Poland–Germany, –Netherlands, –Czech lanes | Short term (≤ 2 years) |

| Growth of temperature-controlled pharmaceutical exports | +0.5% | Poland to Germany, the Netherlands, Belgium, France, and the U.K. | Medium term (2-4 years) |

| EU funding for TEN-T border-crossing upgrades | +0.4% | Key Poland–Germany, –Ukraine nodes | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Re-Routing of EU Supply Chains via Poland-Germany Corridor

German CO₂ tolls that rose to EUR 200 per tonne (USD 220 per tonne) in 2024 pushed shippers to divert freight through Poland, where diesel remains 15-20 % cheaper, sustaining lane shifts that enlarge the Poland cross-border road freight transport market. New Warsaw–Berlin and Kraków–Wrocław–Berlin rail upgrades funded under the Connecting Europe Facility aim to add 25-30 % freight capacity by 2030, nudging 10-12% of road tonnage onto intermodal options. While pure road growth moderates, demand for first-mile and last-mile truck legs rises, particularly around Poznań and Wrocław rail terminals. DSV’s enlarged warehouse grid is well placed to capture this cross-docking flow. Overall, the corridor realignment lifts capacity utilization, lowers empty running, and supports steady rate growth.

Near-Shoring of Western OEMs to Poland & Czechia

Greenfield projects by Toyota, POSCO International, and others have injected more than USD 3 billion since 2024, shifting component flows from 600–800 kilometers down to nearly 250 kilometers. This densifies regional lanes and boosts LTL demand as factories call for sub-24-hour cycles. Raben answered with new terminals in Będzieszyn and Opole, each within 150 kilometers of major clusters. The trend underpins a healthy pipeline of short-haul revenue, even as long-haul exposure eases.

Post-2027 EU Mobility Package Harmonization

The active enforcement of the EU Mobility Package, which obliges trucks to return to base every eight weeks and grants drivers host-country wages for cross-trade and cabotage, continues to structurally alter the market. Consequently, Polish carriers face operating costs 8-12% higher than those of their competitors. However, investments in e-consignment notes (e-CMR) and geofencing mitigate this by cutting administrative paperwork by up to a third and reducing fine exposure. While countries such as Germany have intensified strict roadside checks via the BALM to enforce compliance, larger groups like Girteka and DSV absorb the regulatory burden through scale, whereas smaller fleets risk exiting international lanes. Over time, policy convergence narrows wage gaps but also pushes tech adoption, sustaining moderate positive momentum for the Poland cross-border road freight transport market.

Rapid Uptake of Digital Freight Platforms

Platforms such as Trans.eu and CargoON lowered empty-running on Poland–Germany lanes below 20 % in 2025, trimming spot prices 12-15 % and enlarging carrier margins. Their integration with EU wage-posting databases limits cabotage penalties, a key competitive edge. While the platform ecosystem processes millions of load offers monthly, its active user base of over 125,000 logistics professionals is heavily driven by Polish fleets, which account for roughly 40 % of transactions. Growth in predictive pricing and API links with major TMS vendors is expected to bring 60-65 % of all cross-border loads onto digital exchanges by 2031, cementing structural efficiencies in the Poland cross-border road freight transport market.

Restraints Impact Analysis*

| Restraints | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Driver shortage and ageing workforce | –0.8% | Poland and key Western EU partners | Short term (≤ 2 years) |

| Tightened cabotage and posting-of-workers rules | –0.6% | Poland–Germany, –France, –Belgium lanes | Medium term (2-4 years) |

| Border delays on the eastern frontier (Ukraine/Belarus) | –0.4% | Poland–Ukraine and Poland–Belarus crossings | Short term (≤ 2 years) |

| Rising tolls & CO₂ pricing on German Autobahn | –0.3% | Core Poland–Germany corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Driver Shortage and Ageing Workforce

Poland lacks 30,000 to 200,000 licensed truck drivers, and the workforce is aging rapidly, with the average driver nearing 50 years old and youth representation below 5%. Pay levels of USD 1,950–2,250 per month trail Western European offers by roughly a third, fuelling continuous out-migration.[2]European Parliament, “Written Question E-003456/2025: Driver Shortage,” europarl.europa.euFurthermore, visa delays limit essential third-country recruitment from Ukraine and beyond. Compounding these structural labor constraints, severe fuel price spikes in early 2026, which prompted emergency government price caps, have forced smaller, highly vulnerable fleets to idle trucks. Until automation or large-scale, state-sponsored training schemes mature, combined labor and operating cost pressures will cap capacity and slow growth in the Poland cross-border road freight transport market.

Tightened cabotage and posting-of-workers rules

From 2025 onward, Polish haulers face fines of USD 1,600–5,300 for exceeding three cabotage jobs in seven days or underpaying posted drivers. Compliance pushes costs up 8-12 %, eroding low-cost advantages. Bigger players offset the hit through technology and multi-country bases; smaller carriers may retreat to domestic work, squeezing international capacity and putting freight rates under pressure across the Poland cross-border road freight transport market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Commands, Retail Trade Rises

Manufacturing accounted for 22.78% of 2025 tonnage in the Poland cross-border road freight transport market as automotive and electronics plants fed German and Czech assembly lines. The wholesale and retail trade segment, buoyed by e-commerce’s 9.1% share of Polish retail, is the fastest-growing with a 4.91% CAGR forecast through 2031.[3]Polish Investment and Trade Agency, “Logistics Sector Overview,” paih.gov.pl

Online parcel specialists such as InPost, which operates more than 53,000 automated lockers, are driving higher LTL volumes, especially on the Germany and Netherlands lanes. Multitemperature capacity from Raben and Nagel-Group supports pharma and grocery inflows, while new electronics plants, such as Compal’s Czeladź site, spur demand for climate-controlled trucks within 300 kilometers. Altogether, retail freight is set to narrow the gap with manufacturing by the end of the outlook period, underpinning service diversification for carriers.

By Truckload Specification: FTL Dominance Meets Digital-LTL Surge

Full-truckload (FTL) shipments captured a commanding 78.61% of the Poland cross-border road freight transport market share in 2025, reflecting 22- to 24-tonne grain lots and dedicated auto-component runs that underpin high cube utilization. Average FTL stage lengths remain near 800 kilometers on Poland-Germany corridors, yet empty-running dropped below 20% in 2025 after widespread platform matching. DSV’s post-Schenker grid now groups multiple FTL departures per hour from Poznań and Wrocław, shrinking dwell times to under 12 hours.

Less-than-truckload (LTL) is on track for a 5.03% CAGR, the fastest in this category, thanks to CargoON’s AI bidding engine that lifts carrier win rates more than 20% on Dutch and Belgian lanes. Raben’s 10,000 m² Bedzieszyn terminal funnels 15–20 spoke depots into high-frequency trunk routes, lowering per-pallet costs by up to 25%. As near-shoring compresses shipment radii under 300 kilometers, mixed-size consignments multiply, pushing LTL’s share toward one-quarter of the Poland cross-border road freight transport industry by 2031.

By Containerization: Bulk Dominates, Intermodal Steps Up

Non-containerized freight represented 79.23% of the Poland cross-border road freight transport market size in 2025, driven by grain, timber, and prefabricated concrete streams loaded on curtain-siders or flatbeds. Average load weights of 22–24 tonnes and low value-to-weight ratios dissuade the use of containers. Yet the Yahodyn–Dorohusk and Małaszewicze terminals, expanded with Connecting Europe Facility funds, are lifting annual capacity by a combined 40%, aiming to permanently slice historically volatile border dwell times below 12 hours.

Consequently, containerized flows are projected to rise at a 4.79% CAGR through 2031, led by pharma reefers and electronics in 40-foot high-cubes. Compal Electronics started shipping ISO-sealed control modules to Czech plants in early 2026, cutting damage claims by 30% and ensuring 100% GDP compliance. Nagel-Group’s new 46,000 m² Poznan complex will dedicate eight dock doors specifically to temperature-controlled containers, reinforcing a corridor shift that supports higher yields per kilometer across the Poland cross-border road freight transport market.

By Distance: Long-Haul Holds Majority, Short-Haul Climbs

Long-haul lanes accounted for 62.47% of the Poland cross-border road freight transport market share in 2025, as fully loaded trailers shuttle for 24–36 hours to Germany, the Netherlands, and France under EU tachograph rest rules. Diesel-price arbitrage and heavy CO₂ tolls keep Polish haulers competitive despite 8–12% cost inflation on German roads. Short-haul traffic, defined here as under 300 kilometers, will climb at a 5.08% CAGR because OEM near-shoring pulls supply rings tighter.

New electronics nearshoring hubs, such as Compal’s Czeladź facility, generate high-frequency shuttle departures, each well below 250 kilometers, specifically serving nearby Czech and Slovak assembly lines. Rail investments that transfer trunk legs to intermodal loops simultaneously lift last-mile needs around Lodz and Wrocław terminals. Hence, Short-Haul’s weight could surpass one-third of the Poland cross-border road freight transport market share by 2031, even as absolute long-haul tonnage continues to grow.

By Goods Configuration: Solid Cargo Prevails, Fluids Create Premium Niche

Solid goods accounted for 75.98% of throughput in 2025, led by auto parts, packaged food, and steel components that fit standard 13.6-meter trailers. Construction demand linked to Ukrainian rebuilding funnels steady cement and rebar flows eastward, while consumer electronics ride back-haul slots westward, pushing average payload value up 8% year-on-year.

Fluid and temperature-sensitive goods are advancing at a 4.74% CAGR. Refineries in Gdansk and Płock dispatch diesel tankers westward under ADR protocols, while pharma shippers move mRNA vaccine concentrates at –70 °C via specialized deep-freeze medical logistics providers. Simultaneously, major networks like Nagel-Group and Raben have aggressively invested in active-refrigeration GDP-compliant trailer fleets for standard biopharma, earning up to 30% higher revenue per kilometer versus ambient loads. This premium segment is set to lift overall profitability for carriers active in the Poland cross-border road freight transport market.

By Temperature Control: Ambient Dominates, Cold Chain Accelerates

Non-temperature-controlled freight accounted for 93.3% of the Poland cross-border road freight transport market size in 2025, covering resilient automotive, electronics, and building materials lanes. Ambient goods tolerate swings of –10 °C to +30 °C, allowing simpler equipment and faster turnarounds.

Temperature-controlled loads, however, are on a 4.87% CAGR trajectory. Polish pharma exports relied on 2 °C-to-8 °C reefers and –20 °C freezers, while biologics increasingly demand –70 °C transit. To support this, major carriers are aggressively expanding their specialized footprints; Raben continues to scale its dedicated Fresh Logistics network across sites like Łomża, while GEODIS recently invested in a dedicated 2,600 m² GDP-compliant pharmaceutical hub at MLP Pruszków II to feed Western buyers. Driven by these investments, cold-chain fleet kilometers are set to double by 2031, steadily raising the value density of the Poland cross-border road freight transport industry

Geography Analysis

Germany held 35.66% of Poland's cross-border road freight transport market share in 2025, driven by steady automotive part shuttles and rising pharmaceutical exports that fill daily Poznań–Berlin and Wrocław–Leipzig lanes. The 2024 German CO₂ surcharge lifted road tolls to USD 0.15–0.56 per kilometer, nudging some long-haul cargo toward rail-road services yet leaving overall truck demand intact thanks to same-day delivery targets. Connecting Europe Facility upgrades on the Warsaw–Berlin and Kraków–Wrocław–Berlin corridors promise 25–30% extra rail capacity by 2030, but they also create new first- and last-mile work for Polish fleets. Large 13.6-meter trailers still depart every hour from hubs around Poznań, and empty running slipped below 20% in 2025 after Trans.eu load-matching went mainstream. Despite higher tolls, Germany is expected to maintain a low single-digit volume CAGR, driven by strong consumer demand and entrenched supplier relationships.

Czech Republic and Slovakia together accounted for roughly one-fifth of 2025 flows as near-shoring compressed component hauls to under 300 kilometers, enabling twice-daily shuttles that bypass driver overnight rests. The Katowice–Ostrava rail line, now under detailed design with EU funding, will cut Katowice–Prague truck equivalents by up to three hours and further spur short-haul moves around Łódź and Wrocław terminals. Ukraine is the fastest-growing lane with a 5.48% CAGR forecast through 2031 after the Yahodyn–Dorohusk upgrade raised annual capacity 40%. Reconstruction demand for cement, steel, and agricultural inputs is steering steady back-haul volumes, while the unified e-queue (eCherha) system, fully operational for trucks, attempts to keep historically volatile transit times more predictable. Belarus remains a niche at 3–5 % share because of sanctions and 24-hour customs checks that deter time-sensitive loads.[4]European Commission, “EU-Ukraine Solidarity Lanes,” ec.europa.eu

The Netherlands, BeThe lgium, and France together absorbed nearly one-quarter of westbound tonnage in 2025, led by Polish grain, packaged food, and generic drugs headed for Rotterdam and Antwerp distribution centers. Pharma reefers make profitable Poland–Belgium lanes, and Nagel-Group’s 2027 Poznań hub will shorten reload cycles to those markets. Scandinavian traffic rides northbound empty capacity, balancing network flows and limiting the impact of CO₂ toll hikes on rate volatility. Altogether, diversified geography keeps the Poland cross-border road freight transport market resilient against border shocks and single-country downturns.

Competitive Landscape

The market is moderately fragmented; the ten largest carriers account for just 35–40% of cross-border volume, leaving plenty of room for mid-tier fleets. DSV’s EUR 14.3 billion Schenker buyout in 2025 added 300,000 m² of Polish warehousing, and an extra 24,000 m² Łódź site coming online in 3Q 2026 will let the group bundle contract logistics with trunk haulage, a move aimed at locking in 12–15 % of Poland–Germany lanes. Girteka tapped USD 190 million in bank financing in 2025 to fund 8,000 new vehicles and rolled out a Carrier Advantage subcontractor scheme to secure headcount amid a 30,000–200,000 driver gap. Raben answered with new terminals in Będzieszyn and Opole that slash pallet-handling times by 25%, underscoring a race toward network density.

Digital platforms are reshaping pricing power. While Trans.eu processes millions of load offers for its 125,000 active users, CargoON’s AI tool explicitly boosts carrier win rates above 20 % on Dutch and Belgian lanes. Empty-running fell below 20% on Poland–Germany routes in 2025, lifting fleet utilization to historic highs. Smaller firms that lack API integration still depend on brokers and face 8–12 % margin pressure, making them prime targets for consolidation. Compliance technology is also decisive; operators that linked e-CMR and posting-of-workers databases cut cabotage fines one-third during 2025 roadside blitzes in Germany and France.

High-yield niches are driving the next strategy wave. Nagel-Group is pouring USD 60 million into a 46,000 m² multi-temperature complex in Poznań to win GDP-certified pharma contracts, while GEODIS recently fortified its footprint with a dedicated 2,600 m² GDP cold-chain hub at Pruszków II alongside wider ambient expansions. Raben and DSV each launched pilot fleets of Mercedes eActros battery trucks that enjoy German zero-emission toll exemptions through 2031, showing early total cost of ownership savings near 10% on sub-300-kilometer runs. With reconstruction work in Ukraine and electronics output in Czechia both climbing, carriers that blend cold-chain, digital dispatch, and short-haul electric units are set to outpace the broader Poland cross-border road freight transport market.

Poland Cross-Border Road Freight Transport Industry Leaders

DHL Supply Chain

Kuehne + Nagel

DSV A/S

Raben Group

GEODIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DSV advanced its target to finalize the DB Schenker integration by year-end, supported by a new 24,000 m² Łódź superhub aimed at lifting regional capacity by 40%.

- February 2026: Poland’s transport authorities unified border clearance procedures with Ukraine's e-queue system, a move projected to cut cross-border wait times by up to 10 hours.

- February 2026: DACHSER commenced operations at the transshipment terminal of its new Unna logistics center, a critical hub designed to tighten European and Poland–Germany delivery networks.

- November 2025: The European Commission cleared EUR 450 million (approx. USD 495 million) in state aid for Onsemi’s Czech SiC plant, securing supply chains for EV power modules.

Poland Cross-Border Road Freight Transport Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

| Containerized |

| Non-Containerized |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperature Controlled |

| Temperature Controlled |

| Germany |

| Czech Republic |

| Slovakia |

| Ukraine |

| Belarus |

| Rest of Europe |

| By End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| By Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| By Containerization | Containerized |

| Non-Containerized | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Country | Germany |

| Czech Republic | |

| Slovakia | |

| Ukraine | |

| Belarus | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Poland cross-border road freight transport market in 2026?

The Poland cross-border road freight transport market size stands at USD 13.61 billion in 2026 and is on course to reach USD 16.77 billion by 2031.

Which destination country accounts for the largest share of Poland's freight?

Germany held 35.66% of cross-border tonnage in 2025, driven by automotive and pharmaceutical flows.

What segment is growing fastest within the market?

Ukraine segment is projected to grow at 5.48% CAGR through 2031.

How will EU Mobility Package I affect Polish carriers?

Full enforcement from 2027 raises labor and routing costs by roughly 8-12%, pressuring small fleets while rewarding operators that invest in compliance technology.

Is cold-chain demand increasing in Poland’s cross-border freight?

Yes, temperature-controlled volumes are set to rise at 4.87% CAGR as pharmaceutical exports grow and biologics require 2 °C to –70 °C transit.

Page last updated on: