Texas Freight And Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 139.19 Billion |

| Market Size (2026) | USD 144.23 Billion |

| Market Size (2031) | USD 172.24 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Texas Freight And Logistics Market Analysis by Mordor Intelligence

The Texas Freight And Logistics Market size was valued at USD 139.19 billion in 2025 and estimated to grow from USD 144.23 billion in 2026 to reach USD 172.24 billion by 2031, at a CAGR of 3.62% during the forecast period (2026-2031).

The steady climb of the market rests on the state’s role as the United States’ primary gateway to Mexico, where surging cross-border trade aligns with accelerating nearshoring activity. Semiconductor fabrication megaprojects, renewable-energy buildouts, and an expansive e-commerce fulfillment network amplify freight flows across road, rail, air, sea, and pipeline assets, stabilizing demand even as individual sectors fluctuate. The Texas freight and logistics market benefits from government incentives under the CHIPS Act and Inflation Reduction Act, which add long-term project visibility for heavy-haul carriers supporting oversized cargo moves. Moderate competitive intensity persists because 20 national and regional players address a wide set of niche demands, from temperature-controlled warehousing to AI-enabled cross-border brokerage. Structural headwinds—chiefly truck-parking shortages on the I-35 and I-10 corridors, intermodal rail pinch-points in Houston and Dallas-Fort Worth, and hurricane-driven Gulf Coast disruptions—temper growth but do not derail the broader expansion trajectory.

Key Report Takeaways

- By logistics function, freight transport led with 61.85% revenue share in 2025; freight forwarding is projected to expand at a 3.87% CAGR through 2031.

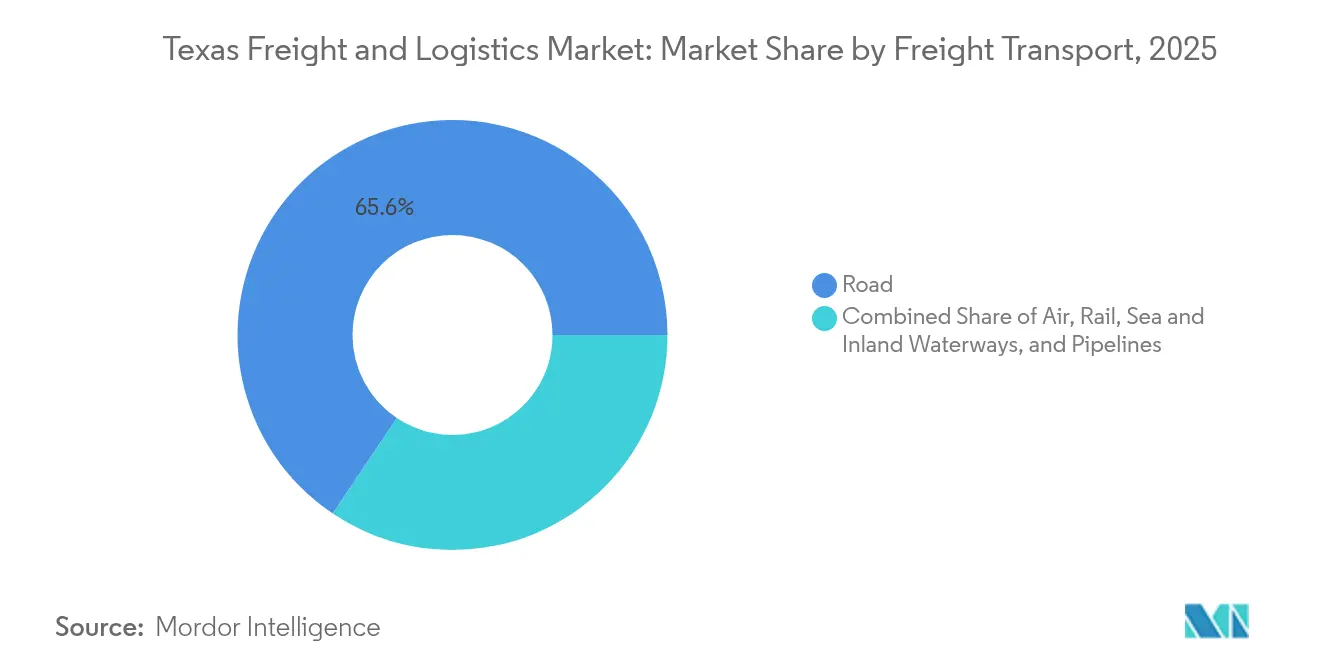

- By freight transport mode, road accounted for 65.60% of the Texas freight and logistics market share in 2025, while air freight exhibits the fastest 4.02% CAGR outlook.

- By CEP destination, domestic shipments held 87.12% share of the Texas freight and logistics market size in 2025; international CEP is expected to grow at a 4.16% CAGR to 2031.

- By warehousing temperature control, non-temperature facilities captured 73.55% of the Texas freight and logistics market size in 2025, whereas temperature-controlled space is advancing at a 4.05% CAGR through 2031.

- By freight forwarding mode, air services commanded 42.62% of segment revenue in 2025 and are forecast to post a 4.09% CAGR to 2031.

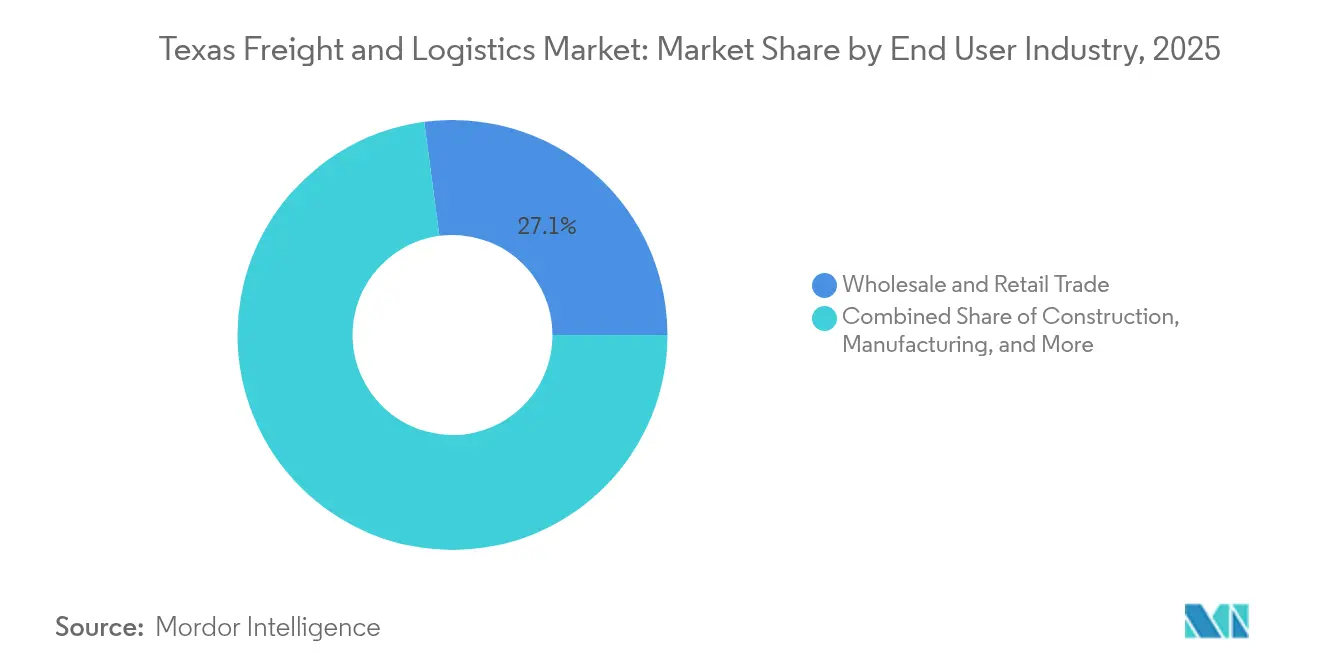

- By end user, wholesale and retail trade held 27.10% of the Texas freight and logistics market share in 2025 and is growing the fastest at a 4.32% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Texas Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment boom | +0.8% | Dallas–Fort Worth, Houston, Austin metros | Medium term (2-4 years) |

| Near-shoring flows from Mexico | +0.9% | South Texas border regions, I-35 corridor | Short term (≤ 2 years) |

| Energy-transition oversized cargo | +0.6% | Gulf Coast petrochemical corridor, East Texas | Long term (≥ 4 years) |

| Connected-freight corridor tech pilots | +0.4% | Dallas–Houston–San Antonio triangle | Medium term (2-4 years) |

| Rapid warehouse automation | +0.5% | Major metro distribution centers statewide | Short term (≤ 2 years) |

| Federal CHIPS/IRA semiconductor subsidies | +0.7% | Austin–San Antonio corridor | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Fulfillment Boom Reshaping Distribution Footprints

Amazon’s statewide rollout of large-package delivery capabilities signals a decisive shift toward handling bulkier items that dominate e-commerce growth[1]Karen Hao, “Amazon Expands Large-Package Delivery Network,” Reuters, reuters.com. Texas distribution centers are reconfiguring dock space and adopting automated sortation to process furniture, appliances, and home-improvement goods more efficiently. Cold-storage landlords are retrofitting facilities for rapid grocery fulfillment as online food orders climb. Robotics providers report double-digit throughput gains when AI-driven inventory systems replace manual picking, accelerating turnover rates in key Dallas-Fort Worth and Houston submarkets. These productivity improvements reinforce Texas freight and logistics market competitiveness by compressing delivery windows and reducing labor costs.

Near-shoring Flows from Mexico Boosting Cross-Border Truckload

Mexico surpassed China as America’s top trade partner, driving a sharp rise in truck crossings at Laredo, Pharr, and El Paso[2]David Luhnow, “Mexico Becomes America’s Top Trade Partner,” Wall Street Journal, wsj.com. Automotive and electronics parts now traverse the I-35 corridor at volumes that strain existing rest-area and bridge capacity. To preserve cycle times, brokers deploy predictive analytics to pre-clear customs data and schedule off-peak staging. Carriers with bilingual dispatch teams and C-TPAT certifications gain an edge in winning multiyear contracts from nearshoring manufacturers. These developments elevate the strategic importance of the Texas freight and logistics market for nationwide supply-chain managers seeking resilient regional networks.

Energy Transition Investments Spiking Oversized Cargo

ExxonMobil, Occidental, and other majors are channeling billions into blue hydrogen, carbon capture, and wind projects along the Gulf Coast, each requiring modules that weigh hundreds of tons[3]Jennifer A. Dlouhy, “ExxonMobil Plans USD 20 Billion Low-Carbon Investment,” Bloomberg, bloomberg.com. Heavy-haul specialists secure premium rates to navigate route surveys, bridge engineering approvals, and night-move escorts across rural highways. Concurrent pipeline and compressor-station construction stimulates steady demand for specialized trailers and rigging crews. Permitting reforms by state agencies compress project timelines, leading shippers to lock in multi-year capacity with carriers that possess demonstrated compliance records. The Texas freight and logistics market, therefore, benefits from a distinct oversized-cargo revenue stream insulated from broader economic cycles.

Connected-Freight Corridor Tech Pilots Improving Asset Turns

TxDOT’s Connected and Automated Transportation initiative outfits the Dallas–Houston–San Antonio triangle with roadside sensors and vehicle-to-infrastructure communications[4]Texas Department of Transportation, “Connected and Automated Transportation Studies,” txdot.gov. Real-time routing updates trim peak-hour delays for truck fleets, while predictive maintenance alerts reduce unscheduled downtimes. Early field data show faster average speeds on pilot segments, enabling carriers to squeeze an extra weekly turn from long-haul tractors. Shippers reward that reliability with volume commitments, reinforcing the competitive standing of digitally enabled operators within the Texas freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Severe truck-parking deficit | –0.6% | I-35 Laredo–Dallas; I-10 El Paso–Houston | Short term (≤ 2 years) |

| Rail capacity pinch-points | –0.4% | Houston Ship Channel; Dallas-Fort Worth | Medium term (2-4 years) |

| Gulf-Coast extreme-weather disruptions | –0.5% | Houston metro, Gulf petrochemical corridor | Long term (≥ 4 years) |

| Driver and warehouse labor shortages | –0.3% | Rural counties and smaller metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Severe Truck-Parking Deficit Along I-35 and I-10 Corridors

Truck stops on the Laredo-to-Dallas stretch operate at over 100% of design capacity during peak evenings, forcing drivers to stage on highway shoulders. Lost time securing legal parking erodes productivity and inflates detention costs. Hours-of-service limits, unchanged since the pandemic, magnify the operational hit when safe parking is scarce. State grants for new rest-area construction remain years away from delivery, meaning carriers must bake larger time buffers into schedules—an inefficiency that drags on the Texas freight and logistics market CAGR.

Gulf-Coast Extreme-Weather Disruptions Raising Insurance and Re-Routing Costs

Hurricane Beryl shuttered the Houston Ship Channel for four days in 2024 and cut electricity to distribution centers serving half the Gulf region. Insurers subsequently boosted premiums for warehouses inside the storm-surge zone. Carriers now pre-plan hurricane detours that add hundreds of miles to lanes connecting petrochemical exporters with Midwest buyers. These cost spikes weigh on competitiveness for operators anchored to Gulf infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale and Retail Trade Drives Dual Leadership

Wholesale and retail trade captured 27.10% of the Texas freight and logistics market size in 2025 and is posting the highest 4.32% CAGR (2026-2031). Expansion of mega-fulfillment centers by both Amazon and traditional big-box retailers positions Texas as a national inventory staging point.

Manufacturing ranks second as semiconductor, aerospace, and machinery makers increase output destined for domestic and export customers. Energy extraction and processing remain core, but diversification into renewables tilts freight mix toward oversized turbines and hydrogen modules. Construction logistics stay robust on industrial capex cycles, while agricultural exports of beef, cotton, and grains sustain a meaningful baseline of specialized reefer and bulk freight.

By Logistics Function: Freight Transport Anchors Market Leadership

Freight transport generated 61.85% of the Texas freight and logistics market size in 2025, underscoring the state’s function as a continental transit hub linking Mexican factories, Gulf Coast refineries, and inland consumption centers. Robust intermodal connectivity enables carriers to shift seamlessly among road, rail, and waterway options, supporting commodity flows ranging from refined fuels to retail merchandise. Established 3PLs leverage economies of scale to lock in contract rates, while specialized heavy-haul operators capture premiums on equipment destined for semiconductor fabs and hydrogen plants.

The outlook through 2031 shows freight forwarding expanding at a 3.87% CAGR as nearshoring raises demand for customs brokerage, trade-compliance consulting, and multimodal coordination. Courier, express, and parcel (CEP) specialists face intensifying competition from retailer-controlled delivery networks, pushing them to differentiate via regional sort-center density and real-time visibility. Warehousing and storage providers use automation to trim operating ratios, while value-added “other services” such as sustainability audits and supply-chain risk modeling gain traction among ESG-focused shippers.

By Courier, Express, and Parcel Destination: Domestic Shipments Drive Volume

Domestic CEP dominated with an 87.12% share of the Texas freight and logistics market size in 2025, reflecting proximity to population clusters across the southern and central United States. Same-day and next-day expectations pressure carriers to densify micro-fulfillment nodes in Austin and San Antonio for rapid regional deliveries.

International CEP lanes exhibit a 4.16% CAGR (2026-2031) outlook as ship-from-Mexico replenishment strategies mature. Cross-border e-commerce parcels cross at Laredo and Brownsville under streamlined Section 321 rules, favoring brokers that offer embedded customs data tools. The large-package subsector grows faster than small parcel as furniture, appliances, and fitness equipment subscriptions accelerate, compelling CEP leaders to invest in oversized sortation systems.

By Warehousing and Storage Temperature Control: Automation Reshapes Non-Temperature Operations

Non-temperature warehouses held 73.55% of the Texas freight and logistics market size in 2025, servicing electronics, automotive, and general merchandise inventories. Robotics deployments trim labor hours per unit moved, elevating throughput and shrinkage control.

Temperature-controlled facilities, while a smaller slice, post a 4.05% CAGR (2026-2031) as pharmaceutical and grocery categories demand near-perfect cold-chain integrity. Americold’s newly acquired Houston site deploys mobile racking and AS/RS cranes, doubling pallet density relative to conventional configurations. FDA and USDA rules raise the compliance bar, presenting hurdles for new entrants but reinforcing value capture for incumbent cold-chain specialists.

By Freight Transport Mode: Road Dominance Faces Modal-Shift Pressures

Road carriers retained 65.60% of the Texas freight and logistics market share in 2025, buoyed by the flexibility required for last-mile delivery, cross-border trucking, and petrochemical drayage. Consistent lane density along the I-35 spine supports favorable backhaul ratios that keep rates competitive with rail on trips under 500 miles.

Air freight, although just a mid-single-digit slice of volume, leads modal growth at a 4.02% CAGR (2026-2031) as semiconductor component flows and next-day e-commerce transactions speed up. Railroads battle terminal congestion despite continuous capital outlays, while the Houston Ship Channel’s widening elevates barge and container volumes. Pipeline mileage for carbon dioxide expands quietly, supporting CCS projects that diversify the Texas freight and logistics market revenue base.

By Freight Forwarding Mode: Air Services Lead Growth Despite Constraints

Air freight forwarding secured 42.62% of forwarding revenue in 2025 and is tracking a 4.09% CAGR through 2031. Semiconductor fabs time equipment arrivals to tight construction milestones, paying a premium for dedicated-charter services.

Sea and inland waterways forwarding revolves around the Port of Houston’s petrochemical export dominance and growing container trade. Capacity bottlenecks at major Texas airports occasionally divert time-critical shipments through secondary hubs such as San Antonio, illustrating the nimbleness required of forwarders to sustain service levels in the Texas freight and logistics market.

Geography Analysis

The Texas Triangle—anchored by Dallas–Fort Worth, Houston, and San Antonio—concentrates 70% of the state population and the majority of logistics infrastructure, ensuring dense lane networks that reduce empty-mile rates. Dallas–Fort Worth’s dual Class I rail access and central location make it the hub for nationwide less-than-truckload consolidation, while Houston’s petrochemical complex feeds bulk and container exports through an expanding ship channel dredge project. State traffic initiatives apply connected-corridor technology to synchronize freight flows among these metros, bolstering the Texas freight and logistics market’s national role.

Border counties such as Webb, Hidalgo, and El Paso channel surging near-shoring volumes, with Laredo alone handling a sizable share of the U.S.-Mexico truck trade. Bridge expansions and unified cargo pre-inspection programs shorten border dwell, yet truck-parking deficits and limited dray staging space persist. The Rio Grande Valley increasingly hosts cross-dock facilities that transfer freight between Mexican and U.S. carriers under mirrored regulatory frameworks, cementing the region’s place in the Texas freight and logistics industry.

Competitive Landscape

The Texas freight and logistics market hosts major operators spanning trucking, warehousing, forwarding, parcel, and integrated solutions. National parcel giants FedEx and UPS deploy hub reallocations and ground-network redesigns to accommodate large-package growth, with FedEx’s Network 2.0 revamp cutting redundant handoffs and trimming delivery lead times. Asset-heavy truckload carriers J.B. Hunt, Schneider, and Werner layer brokerage and final-mile services onto traditional line-haul competencies to capture broader wallet share.

Regional specialists such as Texas Logistic & Fulfillment Service leverage local zoning knowledge to secure permits for oversized moves faster than national rivals, carving defensible niches in semiconductor and energy transition projects. Brokerage disruptors like Arrive Logistics and Redwood Logistics harness AI-driven load-matching engines to reduce empty miles and enhance predictive ETAs, appealing to shippers seeking real-time visibility.

M&A remains a strategic lever; DSV’s USD 14.9 billion pickup of DB Schenker intensifies scale economies, especially in cross-border forwarding. Cold-chain consolidation proceeds as Americold and Lineage Logistics acquire temperature-controlled warehouses in Houston and San Antonio to secure pharmaceutical and grocery contracts. Patent filings in autonomous yard tractors and warehouse robotics by incumbents and startups alike hint at a technology arms race poised to redefine cost structures across the Texas freight and logistics market.

Texas Freight And Logistics Industry Leaders

FedEx Corporation

UPS Inc.

Total Quality Logistics

Schneider

Penske Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: C.H. Robinson unveiled predictive analytics-driven cross-border freight services to compress border dwell times.

- April 2025: DSV finalized its USD 14.9 billion acquisition of DB Schenker, expanding contract logistics capacity statewide.

- March 2025: Americold purchased a Houston cold-storage facility featuring high-density automation to serve pharmaceutical and e-grocery clients.

- January 2025: Total Quality Logistics opened an 8,754-square-foot Fort Worth office to deepen brokerage coverage in North Texas.

Texas Freight And Logistics Market Report Scope

Freight and logistics refer to the transportation of goods in the domestic and international markets via various modes, including air, rail, and roadways. A complete background analysis of the Texas Freight and Logistics Market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact is included in this report.

The Texas Freight and Logistics Market are segmented By Function (Freight Transport, Freight Forwarding, Warehousing, and Value-Added Services) and By End User (Construction, Oil and Gas and Quarrying, Agriculture, Fishing, & Forestry, Manufacturing and Automotive, Distributive Trade, and Other End Users). The report offers market size and forecast values (USD billion) for all the above segments.

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Pipelines | ||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control |

| Temperatured Control | ||

| Other Services | ||

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Pipelines | |||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control | |

| Temperatured Control | |||

| Other Services | |||

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

Key Questions Answered in the Report

What is the current value of the Texas freight and logistics market?

The Texas freight and logistics market size stands at USD 144.23 billion in 2026.

How fast is the market expected to grow through 2031?

It is forecast to expand at a 3.62% CAGR, reaching USD 172.24 billion by 2031.

Which logistics function holds the largest share?

Freight transport led with 61.85% of 2025 revenue.

What end-user segment is growing the fastest?

Wholesale and retail trade is advancing at a 4.32% CAGR through 2031.

How are semiconductor projects influencing logistics demand?

CHIPS Act-backed fabs in Taylor and Sherman require specialized air and heavy-haul moves, boosting premium freight services.

What major challenge could limit trucking efficiency in Texas?

Severe truck-parking deficits along I-35 and I-10 constrain driver productivity and lengthen delivery times.

Page last updated on: