Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

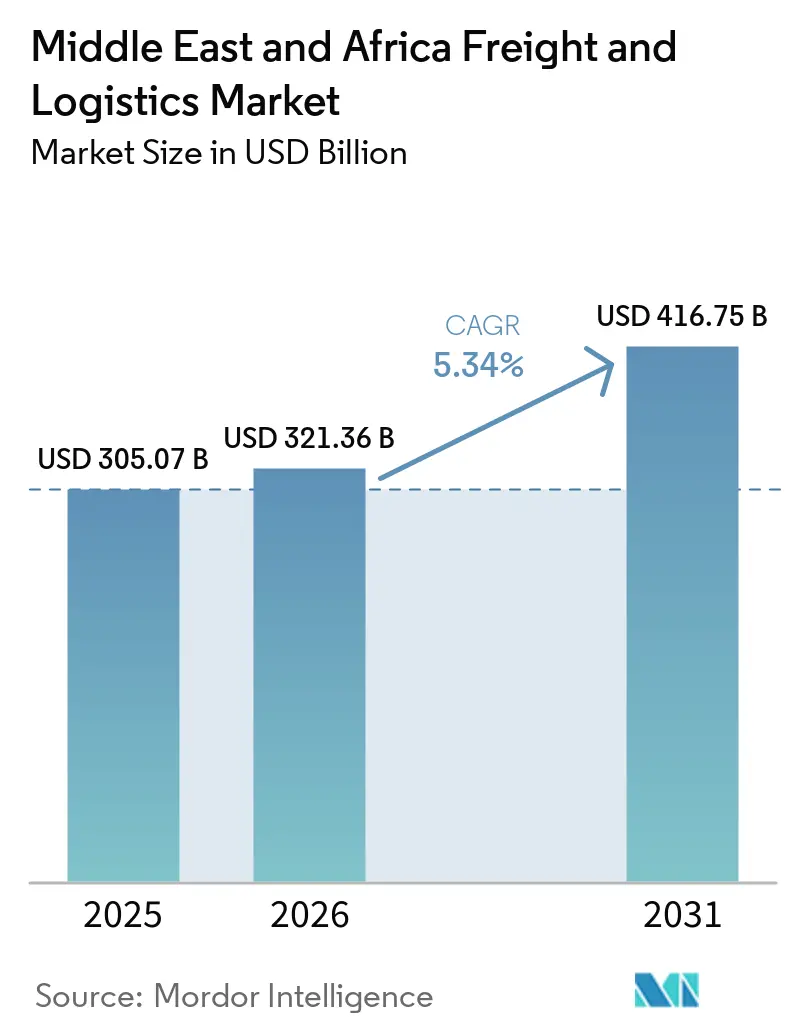

| Base Year Market Size (2025) | USD 305.07 Billion |

| Market Size (2026) | USD 321.36 Billion |

| Market Size (2031) | USD 416.75 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

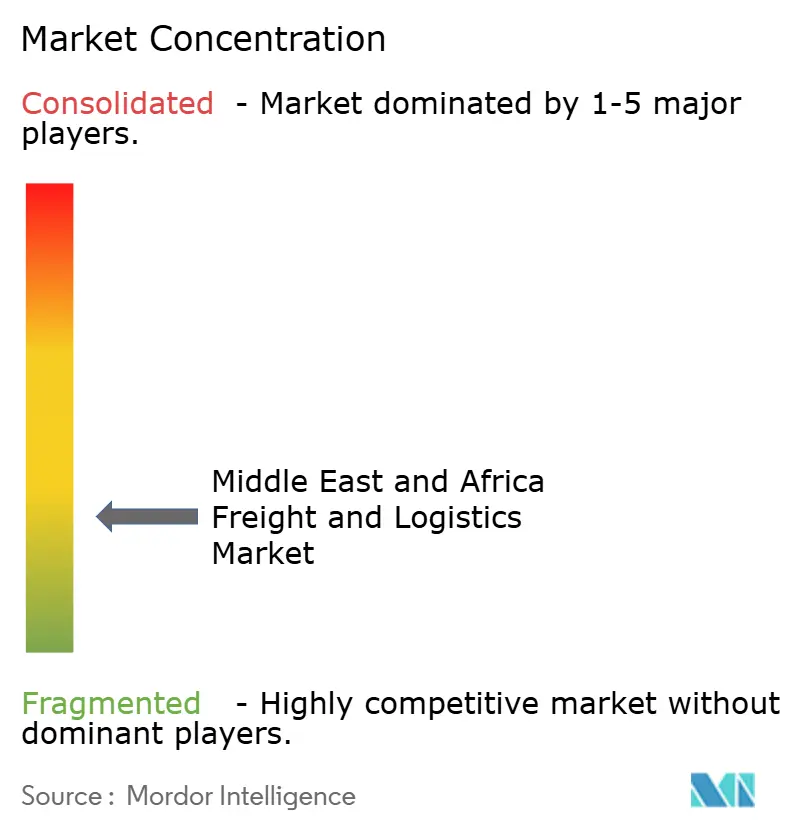

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East and Africa Freight and Logistics Market Analysis by Mordor Intelligence

Middle East And Africa Freight And Logistics Market size in 2026 is estimated at USD 321.36 billion, growing from 2025 value of USD 305.07 billion with 2031 projections showing USD 416.75 billion, growing at 5.34% CAGR over 2026-2031.

The growth outlook flows from the region’s pivotal position linking Asia, Europe, and Africa, combined with heavy infrastructure spending and permanent capacity upgrades triggered by Red Sea shipping disruptions. E-commerce expansion, the rollout of new multimodal corridors, and a surge in cold-chain demand strengthen baseline tonnage and yield per shipment. Sovereign wealth funds, free trade agreements, and digital freight platforms reinforce competitive intensity while mitigating geopolitical volatility. Operators that maximize network density, technology adoption, and sustainable practices are positioned to capture outsized returns.

Key Report Takeaways

- By logistics function, freight transport led with 59.21% of the Middle East and Africa freight and logistics market share in 2025, whereas courier, express, and parcel posted the fastest 5.57% CAGR to 2031.

- By courier, express, and parcel service type, domestic deliveries controlled 67.10% of the Middle East and Africa freight and logistics market size in 2025, while international services recorded the higher 5.63% CAGR through 2031.

- By freight forwarding mode, sea and inland waterways accounted for 52.84% of the Middle East and Africa freight and logistics market share in 2025, and the segment is projected to rise at a 5.62% CAGR between 2026 and 2031.

- By freight transport, road held 40.88% share of the Middle East and Africa freight and logistics market size in 2025; sea and inland waterways are forecast to expand at a 5.49% CAGR during the same period.

- By warehousing and storage type, non-temperature-controlled facilities dominated with 86.95% of the Middle East and Africa freight and logistics market share in 2025; temperature-controlled storage is advancing at a 5.54% CAGR to 2031.

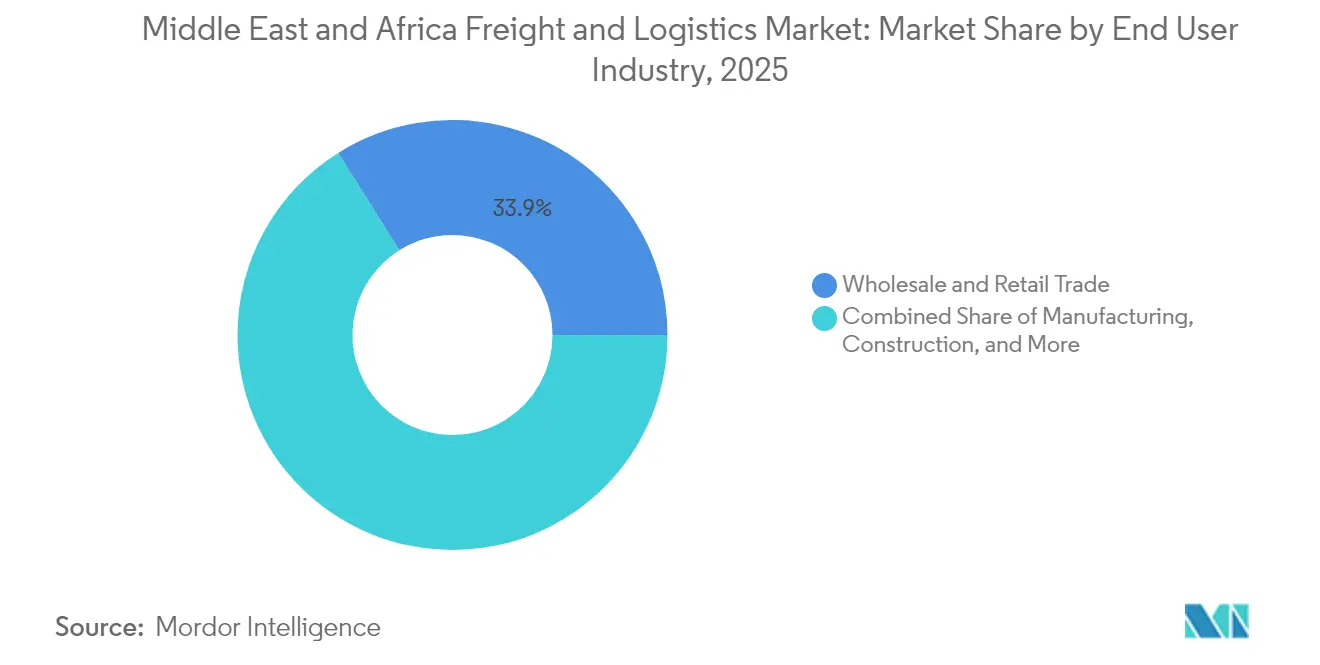

- By end-user industry, wholesale and retail trade captured 33.92% of 2025 revenue, whereas manufacturing is set to grow at a 5.58% CAGR through 2031.

- By geography, Saudi Arabia captured 6.84% of 2025 revenue, whereas United Arab Emirates is set to grow at a 5.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and Africa Freight and Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Boom and Cross-Border Retail | +1.2% | Global, with UAE and Saudi Arabia leading | Short term (≤ 2 years) |

| Mega-Investments in Multimodal Logistics Infrastructure | +1.8% | UAE, Saudi Arabia, Qatar, with spillover to Egypt and Nigeria | Medium term (2-4 years) |

| Growth of FTAs and Emerging Trade Corridors | +0.9% | Global, particularly AfCFTA members and GCC states | Long term (≥ 4 years) |

| Cold-Chain Demand for Pharma and Perishables | +0.7% | UAE, Saudi Arabia, South Africa, Nigeria | Medium term (2-4 years) |

| Warehouse Automation to Offset Labour Shortages | +0.6% | UAE, Saudi Arabia, Qatar, Kuwait | Short term (≤ 2 years) |

| Rapid Adoption of Digital Freight Platforms and Real-Time Visibility Tools | +0.5% | Global, with faster adoption in Gulf states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-commerce boom and cross-border retail

Cross-border e-commerce lifts last-mile shipment frequency, with domestic CEP covering 67.88% of traffic while international CEP advances at a 5.77% CAGR through 2030. Logistics providers are scaling automated sortation hubs and multi-carrier APIs that link Jebel Ali Port to Al Maktoum International Airport. Gulf operators deploy AI routing and collaborate with local universities to fill digital talent gaps. Omnichannel retailers demand integrated fulfillment that merges warehousing, click-and-collect, and door delivery, shifting volume toward express networks.

Mega-investments in multimodal logistics infrastructure

Saudi Arabia earmarked USD 133.3 billion for ports, airports, and railways through 2030, including Port of NEOM’s first fully automated cranes slated for 2026 launch[1]Reem Walid, “How Saudi Arabia is reshaping transportation infrastructure amid climate change challenges,” Arab News, arabnews.com. DP World’s USD 2.5 billion program and record USD 20 billion 2024 revenue signal deep private capital engagement. Automation and renewable energy integration compress dwell times and improve cost curves, reshaping transshipment competitiveness.

Cold-chain demand for pharma and perishables

Temperature-controlled warehousing grows at 5.69% CAGR, outstripping dry storage. Kuehne + Nagel strengthened South-South perishables lanes by acquiring Morgan Cargo, which moves 40,000 tons of air freight and 20,000 TEU of sea freight per year[2]Peter Shaw-Smith, “Kuehne+Nagel acquires South African freight forwarder,” Seatrade Maritime News, seatrade-maritime.com. GDP-compliant facilities, IoT sensors, and solar-powered chillers align with pharma guidelines and food security priorities across Africa and the Gulf.

Rapid adoption of digital freight platforms and real-time visibility tools

Dubai Customs’ blockchain pilot and Africa’s TWIN trade platform support paperless clearances[3]Dubai Customs, “Dubai Customs rolls out blockchain-enabled cross-border platform,” dubaicustoms.gov.ae. Kuehne + Nagel’s Seaexplorer maps vessel positions and port congestion in real time, supplying alternate routings during Bab el Mandeb disruptions. Predictive analytics and generative AI improve forecasting accuracy and cut administrative costs, rewarding asset-light digital intermediaries.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven Road, Rail and Port Infrastructure | -1.1% | Sub-Saharan Africa, with limited impact in Gulf states | Long term (≥ 4 years) |

| Complex Customs Rules and Border Delays | -0.8% | Global, particularly affecting cross-border trade | Medium term (2-4 years) |

| Red-Sea/Suez Chokepoint Disruptions | -0.6% | Global shipping routes, temporary but recurring | Short term (≤ 2 years) |

| Driver Shortages and Localisation Policies | -0.4% | Saudi Arabia, UAE, Qatar, Kuwait | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uneven road, rail, and port infrastructure

Infrastructure gaps raise logistics costs for landlocked African economies relying on coastal gateways. The African Development Bank cites road density disparities and underfunded common-user marine assets as persistent bottlenecks[4]African Development Bank, “State of Africa’s Infrastructure Report 2025,” afdb.org. PPP corridors and toll finance frameworks attract limited private capital outside mining routes. Concentrated capacity in a handful of hubs heightens vulnerability to weather or labor stoppages, stalling hinterland market penetration.

Red Sea/Suez chokepoint disruptions

Despite January 2025 cease-fire progress, Bab el Mandeb traffic stayed depressed, and insurers kept risk surcharges on transits. Diversions around the Cape of Good Hope raised global TEU-mile demand 21% in 2024, inflating rates and stretching vessel supply. Lines deploy sea-air mode shifts and inventory buffers, but security uncertainty still clouds long-range capacity planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing drives future growth

Wholesale and retail trade contributed 33.92% of 2025 revenue, while manufacturing posts the fastest 5.58% CAGR through 2031 as localization and industrial parks proliferate. Oil, gas, and mining logistics remain sizable, supported by commodity flows and energy security spending. Construction logistics taps infrastructure mega-projects, and agri-food shipments expand under food-security strategies.

Nigeria’s USD 20 billion Ogidigben industrial park underscores demand for specialized heavy-lift and project cargo services. Just-in-time production requires synchronized inbound material flows, elevating demand for real-time tracking and predictive inventory analytics

By Logistics Function: Express services drive market evolution

Freight transport retained 59.21% of the Middle East and Africa freight and logistics market in 2025, while courier, express, and parcel leads growth at 5.57% CAGR to 2031. Road-based bulk remains foundational, yet time-definite parcels capture e-commerce tailwinds. Freight forwarding and warehousing post steady gains, and temperature-controlled storage earns premium margins. Technology-driven value-added services under “other” activities scale quickly, feeding demand for end-to-end digital orchestration.

International integrators pledge nine-figure capex for hubs, whereas Aramex leverages ADQ backing to consolidate regional share. Robotics and AI inventory tools widen productivity differentials in Gulf warehouses, creating platforms that fuse parcel delivery, cross-dock, and forwarding under a single interface.

By Courier, Express, and Parcel: International growth outpaces domestic

Domestic CEP claimed a 67.10% share of the MEA freight and logistics market in 2025, yet international CEP grows at a 5.63% CAGR (2026-2031) as cross-border e-commerce and B2B emergency shipments rise. Mature domestic networks in the UAE and Saudi Arabia steer operators to build out pan-GCC and intra-African lanes. Customs complexity grants an edge to providers with automated clearance systems, which pre-file manifests and cut border dwell.

Network expansion needs dedicated gateways, bonded corridors, and regulatory partnerships. Successful CEP firms blend domestic market defense with cross-border scale, requiring heavy investment in compliance teams and digital documentation.

By Warehousing and Storage: Temperature control commands premium growth

Non-temperature-controlled sheds held 86.95% share in 2025, yet cold storage rises 5.54% CAGR (2026-2031) as pharma and perishables drive specialist demand. Renewable-powered chillers and IoT monitoring help operators meet GDP compliance and ESG targets. Automated storage and retrieval systems cut pick errors and labor costs across both facility types.

GCC governments bundle land, utilities, and customs incentives in logistics zones to lure third-party providers. Fulfillment centers evolve from static warehouses into micro-distribution nodes that combine storage, order processing, and last-mile dispatch under one roof.

By Freight Transport: Maritime routes gain despite road dominance

Road transport still held a 40.88% share of the MEA freight and logistics market in 2025, but sea and inland waterways registered a 5.49% CAGR (2026-2031), from expanded berths, deepwater drafts, and greenfield routes. Air freight serves critical spares and high-tech cargo; rail remains nascent outside South African and Moroccan grids. Pipeline logistics underpins energy flows, anchoring specialized midstream revenues.

DP World’s takeover of bp’s Southern Africa trucking arm demonstrates multimodal integration that links ports to inland depots. Performance-based truck combinations in mining reduce trips by 54% and fuel burn, while port-zone autonomous truck pilots test electric drayage in controlled environments.

By Freight Forwarding: Maritime services lead multimodal integration

Sea and inland waterways commanded a 52.84% share of the MEA freight and logistics market in 2025 and drive forwarding growth at a 5.62% CAGR through 2031, reflecting port modernization and alternative routing post-Red Sea disruptions. Air forwarding retains high-value niches, while road-rail forwarding supports mineral and industrial corridors. The Middle East and Africa freight and logistics market size for maritime forwarding is projected to widen as port throughput accelerates.

CEVA’s joint venture with Almajdouie secures Saudi regulatory know-how, while Kuehne + Nagel’s Morgan Cargo deal unlocks perishables pockets in East and Southern Africa. Digital marketplaces with real-time visibility, automated bills of lading, and predictive ETAs tighten customer retention.

Geography Analysis

Saudi Arabia held 6.84% of the Middle East and Africa freight and logistics market in 2025, anchored by Vision 2030 logistics clusters and USD 133.3 billion in multimodal capex. Automated cranes at the Port of NEOM and rail extensions cut dwell times and improve hinterland reach. Green hydrogen projects add specialized bulk movements and create export workflows that favor integrated supply-chain partners.

The United Arab Emirates matches Saudi growth at a 5.60% CAGR (2026-2031), leveraging Jebel Ali’s scale, Al Maktoum’s belly-hold capacity, and free-zone tax incentives. UAE entities have become Africa’s top investors, funneling capital into port concessions in Angola, Congo, and Egypt, thereby pulling African volumes back through Gulf hubs. Advanced digital trade platforms and favorable customs reforms accelerate clearance times, cementing Dubai’s role as a transshipment and fulfillment pivot.

Competitive Landscape

The MEA freight and logistics market exhibits fragmentation. International integrators—DHL, Kuehne + Nagel, DSV—vie with regional champions including Aramex, Gulf Agency Company, and Almajdouie. ADQ’s July 2025 acquisition of a controlling Aramex stake signals sovereign intent to create regional scale leaders.

Technology investments set leaders apart: DHL earmarked USD 570 million for Gulf automation, while Kuehne + Nagel’s Seaexplorer provides real-time disruption alerts. White-space persists in pharma cold chain, e-commerce fulfillment, and intra-African express lanes, where high compliance costs deter new entrants.

Strategic joint ventures couple local market access with global systems; CEVA-Almajdouie targets Saudi heavy industry, and DP World’s bp truck arm purchase links maritime and inland distribution. Smaller firms face pressure to merge or focus on niche verticals, such as dangerous-goods handling or reverse logistics.

Middle East and Africa Freight and Logistics Industry Leaders

DHL

Aramex

Gulf Agency Company (GAC)

RAK Logistics

Al-Futtaim Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: DHL committed over USD 570 million for Gulf network upgrades and e-commerce capacity to 2030.

- November 2024: Kuehne + Nagel began construction of a 23,000 m² e-commerce fulfillment and distribution center in Dubai’s EZDubai.

- November 2024: Rhenus opened a USD 23 million warehouse in South Africa, doubling its floor space to 28,000 m².

- October 2024: GFH signed terms with Gulf Warehousing Company to build 200,000 m² of Grade-A Saudi facilities across Riyadh, Jeddah, and Dammam.

Middle East and Africa Freight and Logistics Market Report Scope

Logistics is a part of supply chain management that deals with the efficient forward and reverse flow of goods, services, and related information from the point of origin to the point of consumption according to the needs of customers.

The Middle East and Africa Logistics Market is Segmented by function, by end-user, by country. By function the market is segmented by freight transport, freight forwarding, warehousing, and value-added services and other services by end user the market is segmented by manufacturing and automotive, oil and gas, mining, and quarrying, agriculture, fishing, and forestry, construction, distributive trade, healthcare and pharmaceutical, and other end users by country the market is segmented by United Arab Emirates, Saudi Arabia, Qatar, South Africa, Egypt, Morocco, Nigeria, and Rest of Middle-East and Africa. The report offers market sizes and forecasts for the market in value (USD) for all the segments.

By Logistics Function

| Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | ||

| Freight Forwarding | By Mode of Transport | Air |

| Sea and Inland Waterways | ||

| Others | ||

| Freight Transport | By Mode of Transport | Air |

| Rail | ||

| Road | ||

| Sea and Inland Waterways | ||

| Pipelines | ||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control |

| Temperatured Control | ||

| Other Services | ||

By End User Industry

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

By Geography

| United Arab Emirates |

| Saudi Arabia |

| Qatar |

| Oman |

| Kuwait |

| Nigeria |

| South Africa |

| Rest of Middle East and Africa |

| By Logistics Function | Courier, Express, and Parcel (CEP) | By Destination Type | Domestic |

| International | |||

| Freight Forwarding | By Mode of Transport | Air | |

| Sea and Inland Waterways | |||

| Others | |||

| Freight Transport | By Mode of Transport | Air | |

| Rail | |||

| Road | |||

| Sea and Inland Waterways | |||

| Pipelines | |||

| Warehousing and Storage | By Temperature Control | Non-Temperatured Control | |

| Temperatured Control | |||

| Other Services | |||

| By End User Industry | Agriculture, Fishing, and Forestry | ||

| Construction | |||

| Manufacturing | |||

| Oil and Gas, Mining and Quarrying | |||

| Wholesale and Retail Trade | |||

| Others | |||

| By Geography | United Arab Emirates | ||

| Saudi Arabia | |||

| Qatar | |||

| Oman | |||

| Kuwait | |||

| Nigeria | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current value of the Middle East and Africa freight and logistics market?

The market stands at USD 321.36 billion in 2026.

How fast is the market expected to grow by 2031?

It is projected to expand to USD 416.75 billion at a 5.34% CAGR.

Which logistics function is growing the quickest?

Courier, express, and parcel services are advancing at a 5.57% CAGR through 2031.

Which countries show the highest growth momentum?

The United Arab Emirates record a 5.60% CAGR from 2026 to 2031.

What segment offers the greatest future potential?

Manufacturing logistics leads with a 5.58% CAGR, driven by supply-chain localization and industrial diversification.

Which transport mode is gaining share despite road dominance?

Sea and inland waterways post the fastest 5.49% CAGR, buoyed by expanded port capacity and new routes.

Page last updated on: