Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 11.29 Billion |

| Market Size (2026) | USD 11.52 Billion |

| Market Size (2031) | USD 12.73 Billion |

| Growth Rate (2026 - 2031) | 2.03% CAGR |

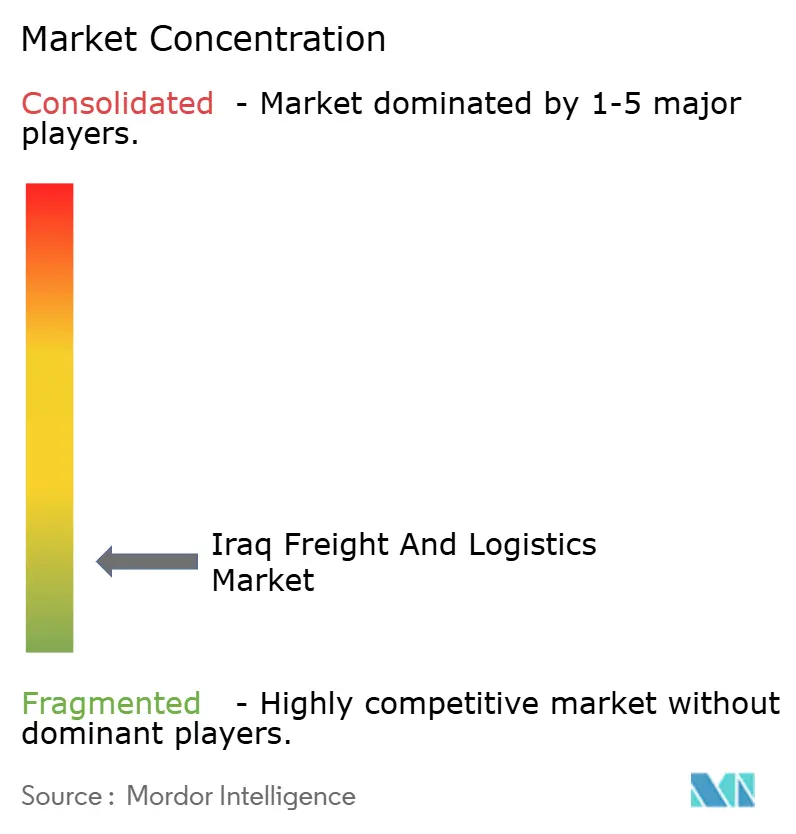

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Iraq Freight And Logistics Market Analysis by Mordor Intelligence

The Iraq freight and logistics market size is expected to grow from USD 11.29 billion in 2025 to USD 11.52 billion in 2026 and is forecast to reach USD 12.73 billion by 2031 at 2.03% CAGR over 2026-2031. This steady pace comes as the country moves from post-conflict recovery into a decisive infrastructure upgrade cycle. Large-scale projects such as the 1,200 km Development Road initiative and the deep-sea Al Faw Grand Port are widening trade corridors, while the nationwide roll-out of the ASYCUDAWorld customs platform is shortening clearance times. The oil sector anchors demand yet is broadening into retail e-commerce, humanitarian logistics, and temperature-controlled supply chains as investors respond to rising consumer spending, international aid flows, and food-security programs. Competitive rivalry is intensifying because foreign integrators are entering through joint ventures, while fleet modernisation, digital freight platforms, and multimodal hubs are reshaping service benchmarks within the Iraq freight and logistics market.

Key Report Takeaways

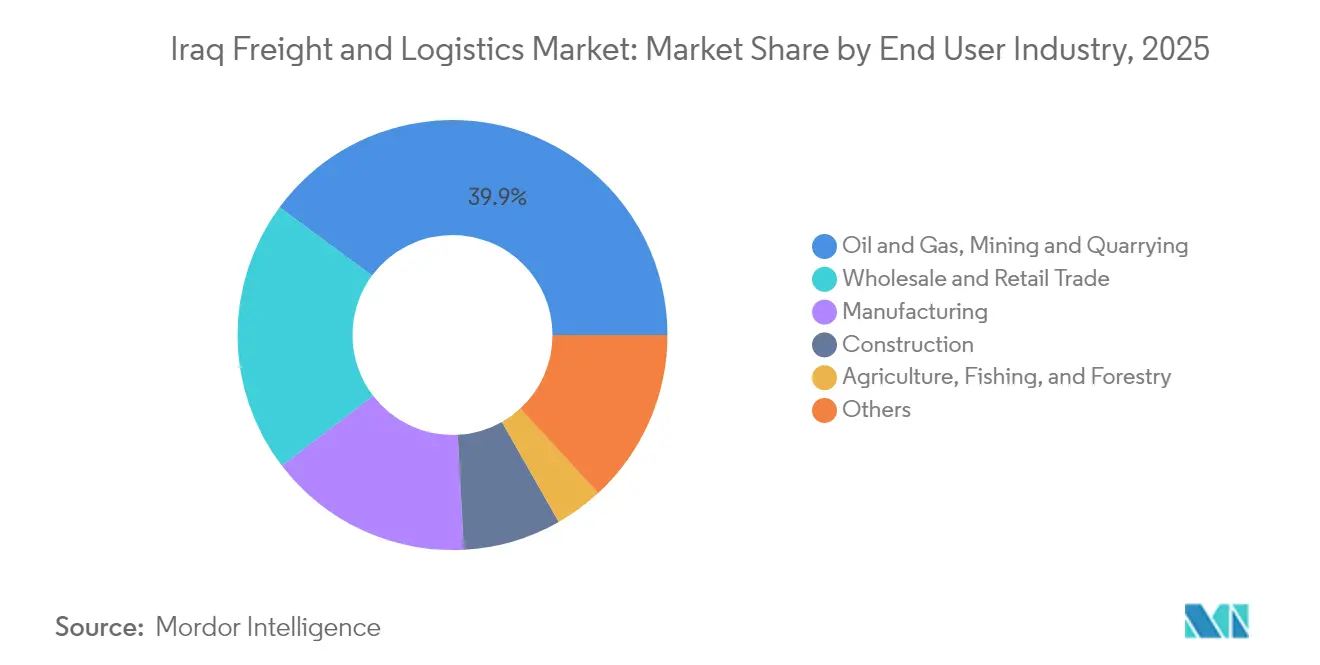

- By end user industry, oil and gas, mining, and quarrying held 39.88% of the Iraq freight and logistics market share in 2025, while wholesale and retail trade is projected to expand at a 2.16% CAGR between 2026-2031.

- By logistics function, freight transport led with 50.12% of the Iraq freight and logistics market size in 2025, whereas courier, express, and parcel (CEP) services are expected to record the fastest projected CAGR at 2.29% between 2026-2031.

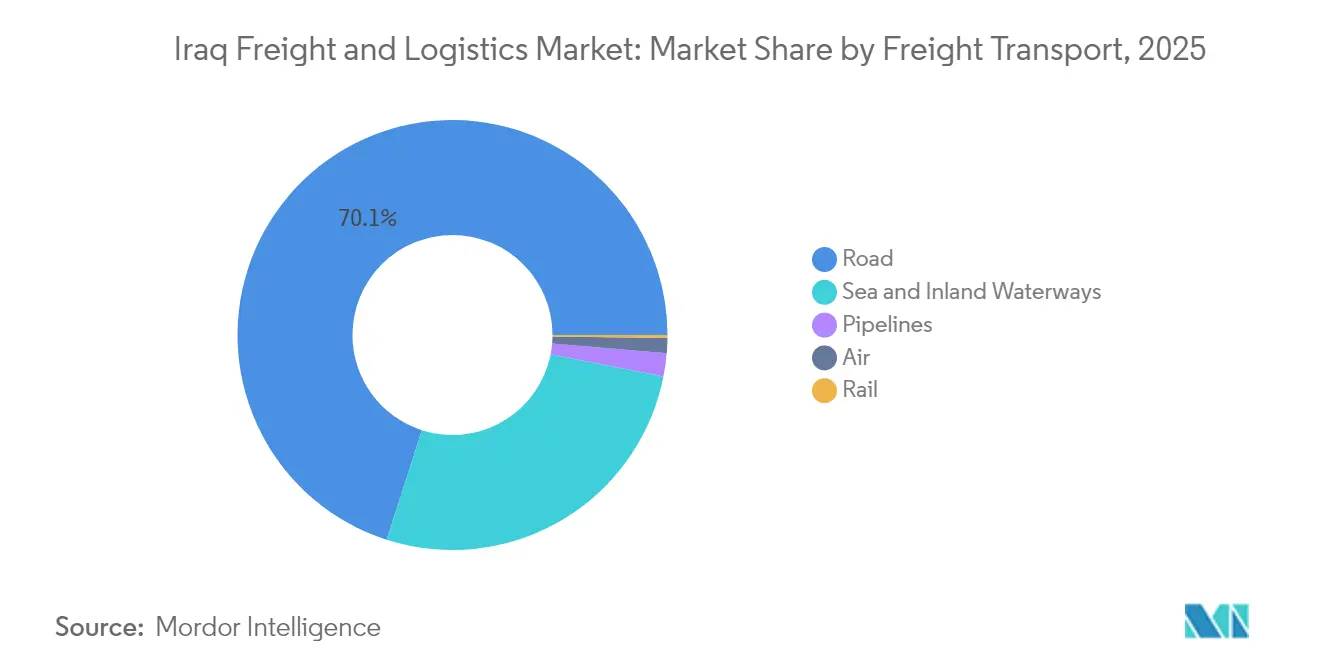

- By freight transport mode, road freight transport captured 70.05% revenue share in 2025; air freight transport is forecast to advance at a 3.52% CAGR between 2026-2031.

- By CEP service scope, domestic deliveries commanded a 65.11% revenue share in 2025, while international shipments are set to grow at a 2.39% CAGR between 2026-2031.

- By warehousing and storage type, non-temperature-controlled sites accounted for 91.95% revenue share in 2025; temperature-controlled space is expected to grow at a 2.24% CAGR between 2026-2031.

- By freight forwarding mode, sea and inland waterways commanded 73.56% revenue share in 2025, while air freight forwarding is projected to expand at a 3.14% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Iraq Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-ISIS oil-export rebound boosting road freight volumes | +0.8% | National, with concentration in southern oil fields and export routes to Basra | Medium term (2-4 years) |

| China–Iraq Belt-and-Road infrastructure investments accelerating multimodal connectivity | +0.6% | National, with focus on strategic corridors connecting to neighboring countries | Long term (≥ 4 years) |

| Basra deep-sea port expansion unlocking containerized trade in the country | +0.4% | Southern Iraq, with spillover effects nationwide | Medium term (2-4 years) |

| Retail and E-commerce growth in Baghdad driving urban last-mile networks | +0.3% | Urban centers, primarily Baghdad | Short term (≤ 2 years) |

| Digitization mandates by Iraqi customs ASYCUDA streamlining border clearance | +0.2% | National, with emphasis on major border crossings and ports | Short term (≤ 2 years) |

| Surge in humanitarian aid corridors via Kurdistan region raising 3PL demand | +0.1% | Kurdistan Region, with effects in northern Iraq | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Post-ISIS Oil-Export Rebound Boosting Road Freight Volumes

Crude oil exports account for 98.7% of Iraq’s merchandise shipments and 45.5% of GDP[1]Extractive Industries Transparency Initiative, “Validation of Iraq 2024,” eiti.org. Pipeline length reached 4,010 km by end-2024, with a further 1,155 km under construction, securing predictable flows from fields to Basra. The Sealine-3 offshore link will add 2 million barrels per day (bpd) capacity, lifting road transport demand for equipment haulage and workforce mobility. Logistics providers that field low-sulphur fuel trucks, GPS-tracked convoys, and heavy-lift trailers are winning service contracts from international oil companies. As upstream output rises, downstream petrochemical projects create backhauls that raise asset utilization and margins across the Iraq freight and logistics market.

China–Iraq Belt-and-Road Infrastructure Investments Accelerating Multimodal Connectivity

Chinese contractors signed about USD 9 billion of Iraq-based engineering work in 2024. Flagship schemes include a USD 8 billion refinery integrated with a dual-gauge rail spur, forming a backbone that aligns with the Development Road project. Freight capacity on the corridor is modeled to hit 40 million tons by 2050. Chinese EPC firms bring turnkey technology, trade credit, and rolling-stock packages that shorten execution cycles. Their presence also crowds in Gulf sovereign wealth funds eager to position Iraq as the trailer-to-Turkey alternative to the Suez route, raising long-haul container volumes through new inland depots.

Basra Deep-Sea Port Expansion Unlocking Containerized Trade

The Al Faw Grand Port spans 54 km² and will host 99 berths with 3.5 million TEU design capacity by 2025. Eleven global terminal operators are bidding for the concession, signaling confidence in Iraq’s reforms on tariffs and security vetting. Early works at the adjoining Basra Gateway Terminal already lifted vessel productivity records, proving demand elasticity once draft restrictions ease. The port’s rail and expressway interfaces will let shippers bypass congested Iranian or Kuwaiti gateways, further entrenching the Iraq freight and logistics market as a Gulf-to-Levant pivot.

Retail and E-commerce Growth in Baghdad Driving Urban Last-Mile Networks

Baghdad’s consumer-tech boom supports a projected 9.15% CAGR (2025-2030) in e-commerce, with turnover projected to reach USD 6.67 billion by 2030. Start-ups funded by the Iraqi Angel Investment Network (IAIN) are layering ride-hailing, quick commerce, and embedded finance onto single super-apps. The surge forces parcel operators to deploy micro-fulfilment hubs, electric scooters, and route-optimization algorithms suitable for narrow streets and variable security zones. Chains of pick-up points inside convenience stores are trimming failed-delivery rates, raising both speed and customer trust.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Informal levies at check-points significantly drive up transit costs | -0.5% | National, with concentration on major trade routes | Medium term (2-4 years) |

| Truck fleet obsolesce and fuel quality issues limiting delivery reliability | -0.4% | National, with acute impact in remote areas | Medium term (2-4 years) |

| Under-developed rail network curtailing bulk cargo diversification | -0.3% | National | Long term (≥ 4 years) |

| High cargo-insurance premiums being levied due to security risks | -0.2% | National, with higher impact in conflict-prone regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Informal Levies at Check-Points Significantly Drive Up Transit Costs

Checkpoint payments act as shadow tolls that inflate delivery prices and erode small-business margins[2]World Bank, “Trading Out of Fragility – Lessons from Iraq,” worldbank.org. The World Bank ties these frictions to Iraq’s fragile growth model, warning that competitiveness hinges on curbing rent-seeking. TIR accession promises an 80% cut in transit time and 38% cost savings, yet successful enforcement depends on broad security-sector reforms.

Truck Fleet Obsolescence and Fuel Quality Issues Limiting Delivery Reliability

Average truck age exceeds 15 years, and inconsistent diesel grades raise breakdown risks. The International Road Transport Union (IRU) calculates that modern fleets can trim operating costs by 20%[3]International Road Transport Union, “Road Transport: Iraq’s Engine for Growth,” iru.org. Contaminated fuel incidents reported in 2024 triggered emergency maintenance cycles that stranded cargo and drove contract penalties. Until fleet renewal credit lines and clean-fuel regulations tighten, the Iraq freight and logistics market faces reliability ceilings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Oil Drives Scale, Retail Sets the Pace

The oil, gas, mining, and quarrying segment captured a 39.88% share of the Iraq freight and logistics market in 2025. Pipeline extensions, crude oil gathering stations, and refinery upgrades produce heavy project cargo flows that anchor base volumes. Expanded export capacity under the Sealine-3 program supports new contracts for heavy-lift hauliers and rig-move specialists. At the same time, the wholesale and retail trade segment is on track for a 2.16% CAGR between 2026-2031 as rising disposable incomes spur product diversity and omnichannel shopping. This trend is pushing 3PLs to add cross-docking sites near Baghdad and to integrate cash-on-delivery reconciliation into transport management systems.

The manufacturing segment benefits from tariff relief on machine imports and the spread of industrial parks near Basra and Kirkuk. Cold-chain opportunities are opening in agriculture thanks to USAID-backed value-chain initiatives and a USD 112.5 million oil-seed crushing facility in Umm Qasr that will need dedicated grain-hoppers and silo services. Construction logistics mirror the USD 17 billion Development Road outlay, keeping demand high for concrete mixers, pre-cast beams, and oversized loads. As these verticals diversify, the Iraq freight and logistics market is evolving from a single-commodity backbone into a multi-sector ecosystem.

By Logistics Function: Freight Transport Commands the Revenue Pool

Freight transport supplied 50.12% of revenue share in 2025, underscoring its foundational role in the Iraq freight and logistics market. Road freight transport operations represent 70.05% of that pool because of route flexibility and minimal rail competition. The Ministry of Construction and Housing is resurfacing 4,000 km of highways, raising average speeds and lowering tyre wear. Courier, express, and parcel (CEP) services, though smaller, will expand fastest at a 2.29% CAGR (2026-2031) as e-commerce widens beyond Baghdad into Mosul and Basra.

Sea and inland waterways freight transport hold second-place status, supported by dredging at Umm Qasr and by Al Faw’s multi-berth roll-out. The warehousing and storage segment is moving from basic sheds to mezzanine-equipped distribution centers with WMS dashboards that track SKU velocity. Freight forwarders are bundling customs brokerage with cross-dock trans-loading under single‐window contracts that reassure multinationals new to Iraq.

By Courier, Express and Parcel: Domestic Dominance with International Upside

Domestic parcels held a 65.11% share of CEP turnover in the Iraq freight and logistics market in 2025, as Baghdad, Erbil, and Basra absorbed two-hour delivery services. Venture-funded apps are overlaying predictive ETA notifications and real-time chat with drivers to lift first-attempt success rates.

The international CEP segment is forecast to outpace domestic at a 2.39% CAGR (2026-2031), aided by simplified de-minimis thresholds and growing cross-border shopping among Iraq’s diaspora. DHL’s GoGreen Plus fuel-switch initiative resonates with multinationals that have science-based net-zero pledges, while Aramex-ZK’s 7,000 points-of-sale network offers cash deposit options crucial for customers without bank cards.

By Warehousing and Storage: Basic Sheds Give Way to Cold-Chain Nodes

Non-temperature-controlled stockrooms captured 91.95% segment revenue share in 2025, but multinational food and pharma firms are demanding Grade-A space with 24/7 power redundancy. The temperature-controlled warehousing is expected to grow fastest at a 2.24% CAGR (2026-2031), underpinned by dnata’s new 20,000 m² cargo complex in Erbil. Developers are installing solar-assisted chillers, racking systems certified to 50°C ambient loads, and warehouse management software that tracks humidity excursions in real time.

Location optimization models rank sites by proximity to highways, substations, and labor pools. As interest rates fall, local investors are syndicating real-estate investment trusts to fund multi-tenant distribution centers that offer modular chambers for frozen, chilled, and ambient goods. Public-private partnerships that bundle land grants with duty-free import of racking and forklift parts are accelerating the build-out.

By Freight Transport Mode: Road Rules, Air Gains Altitude

Road freight transport carried a 70.05% revenue share of freight transport segment in 2025, even as axle-load restrictions and checkpoint delays bite. Use of the TIR electronic pre-declaration portal is driving paperwork cuts that favour just-in-time deliveries. Air freight transport is set to achieve a 3.52% CAGR between 2026-2031 on the back of Baghdad International Airport upgrades financed by the International Finance Corporation. The Iraq freight and logistics market size for air cargo is projected to rise in tandem with pharmaceutical imports and high-value electronics, reinforcing the need for temperature-controlled ground handling.

Sea and inland waterway freight transport in terms of load moved (ton-km) enjoys a 67.89% share thanks to bulk-carrier traffic at Umm Qasr. Fast-track dredging and upgraded gantry cranes will lift throughput once customs e-gates sync with port community systems. Rail freight transport remains marginal, yet the 1,190 km dual line under the Development Road initiative promises modal shift for grain, cement, and steel coils when operational.

By Freight Forwarding: Maritime Heavyweight, Air the Sprinter

Sea and inland waterways freight forwarding represented 73.56% of freight forwarding revenue in the Iraq freight and logistics market in 2025. Al Faw’s milestone will anchor near-sourcing strategies for Gulf and East Mediterranean traders. BlackRock and MSC’s plan to manage Basra’s port estate is expected to inject performance-based KPIs typical of global terminal operators, raising crane productivity and shortening berth windows. Air freight forwarding is expected to log a 3.14% CAGR (2026-2031) because Baghdad and Erbil airports are adding perishable-handling cells and automated ULD storage. Forwarders that integrate cargo iQ milestones and electronic airway bills position themselves for premium shippers.

Multimodal solutions are nascent but expanding. Transport planners now model combined truck-barge-rail routings that bypass bottlenecks and lower carbon intensity. Tracking APIs channel event data back to ERP suites, letting importers automate purchase-order reconciliation and avoid demurrage shocks. These service bundles create stickiness and help freight intermediaries differentiate in a crowded Iraq freight and logistics market.

Geography Analysis

Southern Iraq dominates infrastructure and throughput because Basra anchors both crude oil exports and maritime imports. The Al Faw Grand Port’s USD 2.7 billion first phase, due online in 2025, will let 3.5 million TEU cycles flow directly to hinterland depots and on to Turkey via the new highway. The region also hosts pipeline manifolds, rig maintenance yards, and offshore fabrication sites, ensuring base-load volume for heavy-haul carriers. Specialized warehousing clusters near Umm Qasr are evolving into bonded logistics zones that offer investors deferred duty privileges and one-stop customs desks.

Baghdad forms the consumer nerve center, feeding demand for CEP, urban warehousing, and reverse logistics for e-commerce returns. The ASYCUDAWorld platform is live at the airport, boosting 2024 customs takings by 215%. Ongoing IFC-funded terminal renovations unlock cargo bays for wide-body freighters, while the city’s ring-road expansion lowers last-mile transit times to suburban fulfilment hubs. Service providers building omnichannel networks are locating cross-dock points within 15 km of shopper catchments to meet same-day promises and to reduce failed-delivery penalties across the Iraq freight and logistics market.

The Kurdistan Region benefits from relatively stable security, making Erbil a staging post for humanitarian convoys into Syria and Nineveh. dnata’s green-certified cargo complex will handle 100,000 tons per year, including temperature-sensitives. The regional government’s single-window permit portal offers quicker clearance than federal gateways, yet dual-customs regimes complicate corridor design. Integrating Kurdish and federal procedures remains critical for scaling the Development Road’s rail and highway extensions northward.

Regulatory Landscape

Iraq's freight and logistics regulatory environment is being tightened around trade facilitation and transit security, with the operational rollout of TIR for cross-border road transit and associated electronic pre-declaration processes providing the key anchor. The International Road Transport Union (IRU) reported that, following the operational launch on April 1, 2025, Iraq formalized requirements that make TIR a prerequisite for road transit goods, reinforcing sealed-movement controls and standardizing border documentation practices. At the same time, the nationwide customs digitization push using ASYCUDAWorld continues to shape compliance expectations at major gateways, while road freight operations are still governed by legacy frameworks such as Transport Law No. 80 of 1983 and axle-load instructions (Instruction No. 1 of 2015).

Value Chain Analysis

Iraq's freight and logistics value chain is centered on import and project cargo flows that feed domestic consumption and energy-sector demand. Maritime entry is concentrated in Basra province through Umm Qasr and the Al Faw Grand Port build-out, and onward distribution is predominantly by road due to limited rail penetration. Port and terminal operators, ocean carriers, and freight forwarders coordinate inbound container and bulk movements, which then pass through customs brokerage and inland trucking to Baghdad, Basra industrial zones, and northern consumption centers. Last-mile and returns logistics are increasingly organized around urban parcel networks as e-commerce expands beyond Baghdad. The chain also relies on specialized layers, including heavy-lift haulage for oil and infrastructure projects, bonded storage near ports, and temperature-controlled handling for food and pharmaceuticals.

Bottlenecks and value leakage tend to cluster at border and checkpoint interfaces, where documentation friction and informal levies can extend cycle times and reduce throughput. In this context, digitized customs and transit guarantees increasingly shape node economics. The IFC-backed expansion of Umm Qasr targets a lift in terminal handling capacity from 550,000 to 830,000 TEU (over 50% increase), while the World Bank's USD 900 million ITREC package focuses on rehabilitating Expressway 1 and constructing sections of Expressway 2, strengthening the trunk-road layer that links ports and border crossings to inland depots. With these upgrades progressing alongside Development Road planning, the value chain is shifting from a single-mode trucking dependence toward port-linked, corridor-oriented operating models that favor providers integrating port clearance, linehaul security, and distribution under one control structure.

Competitive Landscape

The Iraq freight and logistics market is highly fragmented, with regional champions, international integrators, and niche specialists competing on network coverage, security compliance, and digital transparency. Joint ventures such as Aramex-ZK blend international best practice with domestic route knowledge, accelerating nationwide branch roll-out without breaching foreign ownership caps. Global shipping lines, including MSC, CMA CGM, and Cosco, are positioning for terminal concessions at Al Faw, signaling that upstream port ownership is becoming a strategic lever.

Technology is a prime differentiator. Operators adopting telematics, warehouse management solutions, and API-based customer portals cut dwell times and improve shipment visibility. DHL’s MyDHL+ and My Global Trade Services pipelines offer exporters instant tariff look-ups and customs document checks, shrinking documentary error rates. Start-ups backed by angel syndicates deploy AI-based dispatching and cash-collection trip-cards to lift last-mile efficiency in Baghdad.

Consolidation is reshaping global league tables. DSV’s purchase of DB Schenker gives it the scale to bid for Iraq oil and gas EPC logistics contracts that demand multi-continent project cargo coverage. Meanwhile, 3PLs specializing in reefer movements or humanitarian aid are carving defensible niches by investing in ISO-certified processes and crisis-response protocols. White-space opportunities remain in integrated multimodal solutions and in contract logistics for agribusiness, healthcare and FMCG where modern inventory management is still nascent.

Iraq Freight And Logistics Industry Leaders

DHL Group

A.P. Moller – Maersk

GAC Group (Holdings), Ltd.

CMA CGM Group (Including CEVA Logistics)

Aramex

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is in port-linked, corridor-led logistics services built around Basra's gateway assets, where funded capacity actions create near-term whitespace for providers focused on throughput, reliability, and visibility. The IFC investment supporting Umm Qasr's expansion to 830,000 TEU, along with procurement of new ship-to-shore cranes and rubber-tyred gantries, points to demand for complementary services such as container freight stations, bonded warehousing, drayage pooling, and digital appointment systems that can reduce gate congestion. On the trade-lane side, new and expanded carrier offerings and corridors, including CMA CGM's Asia-to-northern Iraq connectivity via Turkiye and AD Ports Group's integrated corridor linking Khalifa Port to Umm Qasr for container and Ro-Ro cargo, widen the addressable market for end-to-end forwarding, inland distribution to Kurdistan cities, and cross-border consolidation.

Along the domestic backbone, road rehabilitation and governance programs support investment cases in fleet modernization, telematics, and performance-based maintenance services designed to address reliability constraints in Iraq's trucking-heavy modal split. The World Bank-approved USD 900 million ITREC financing for Expressway 1 rehabilitation and Expressway 2 sections provides an anchor for corridor-centric 3PL offerings such as scheduled linehauls, secure convoy management, and hub-and-spoke cross-docking located along improved expressways. There is also a parallel opportunity in intermodal and rail-enablement services tied to Development Road planning and related rail modernization initiatives, spanning engineering logistics, construction supply chains, and future inland depot operations that link port inflows to northern and cross-border trade lanes.

Recent Industry Developments

- July 2026: Gulftainer launched a dedicated feeder service via GT Lines linking Iraq's Umm Qasr with the UAE, using the Umm Qasr Logistics Centre as an operating node. The new service improves schedule options for Iraqi importers and exporters and strengthens the role of feeder networks in connecting Iraq to mainline services via Gulf hubs.

- March 2026: CMA CGM launched the Phoenician Service (PHOEX) to connect Asian trade lanes to northern Iraq via Mersin, Turkiye, with inland delivery options to Dohuk, Erbil, and Sulaymaniyah. The move expands carrier-led routing choices for cargo bound for the Kurdistan Region and supports growth in integrated sea-to-inland forwarding offerings.

- October 2024: Aramex partnered with ZK Holding to provide integrated courier, freight forwarding, and contract logistics across Iraq through a 7,000-point-of-sale network spanning 15 cities, with go-live planned for Q1 2025. This partnership broadened national reach for parcel acceptance and cash-based logistics transactions, supporting service coverage beyond major metros.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers paid freight and logistics services that move, store, and handle goods that flow into, within, and out of Iraq. It includes transport across road, rail, air, sea, and pipeline networks, plus related services that are billed as logistics revenue.

Scope exclusions: Passenger transport and purely in-house (captive) logistics activities are excluded where no invoiced service revenue is created.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the demand context and to anchor the model inputs to consistent public series that can be checked year over year. We typically review sources such as Iraq customs and trade statistics, port authority releases and throughput notes, civil aviation and airport traffic publications, central bank and national statistics releases, and global trade databases from international bodies such as UN agencies.

On top of that, we rely on company annual reports, investor presentations, reputable press coverage, and association websites to map service offerings and understand pricing movements. Where needed, paid subscriptions for company financials and intelligence, shipment-level import and export tracking, and a logistics supply chain and freight rate database are used to cross-check volumes and rate direction. The examples listed above are illustrative only, and many other sources were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions, especially around rate levels, mode mix, and how much of the spend sits in forwarding, transport, warehousing, and CEP. We spoke with a spread of logistics service providers, freight forwarders, transport operators, warehouse managers, and large shippers, and then we rechecked sensitive inputs with experts familiar with Iraq trade corridors and cross-border processes.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | APAC: 49% |

| Mid tier: 56% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 16% | Managers: 52% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where trade flows and domestic activity signals are used to reconstruct the addressable logistics spend that is actually billed in the country, and then the total is distributed across major service lines. To keep the totals realistic, the outputs are corroborated with selective bottom-up approximations, such as sampled rate-per-ton or rate-per-shipment checks, corridor-level sanity checks, and supplier revenue reasonableness tests where disclosures exist.

Key inputs that shape the model include import and export volumes by major commodity group, port and border throughput indicators, airport cargo handling trends, fuel cost direction as a pass-through driver for road freight pricing, and warehouse utilization signals in key commercial hubs. For forecasting, we use scenario analysis supported by expert views, where demand is linked to expected trade recovery, infrastructure project activity, and policy or security related frictions that can change transit times and costs. When bottom-up evidence is thin for smaller operators, gaps are handled using conservative penetration assumptions and service mix benchmarks that are reviewed in primary calls before finalizing the split.

Data Validation & Update Cycle

Validation happens in layers so the final number is not driven by one data series or one interview. We compare outputs against independent signals like trade values, port throughput direction, and corridor activity, and then anomalies are traced back to a specific assumption such as rate changes, mode shares, or one-off disruptions.

Before sign-off, the model and its drivers are reviewed by another analyst, and follow-up expert outreach is triggered when variances are outside the expected range. Reports are refreshed annually, and interim updates are made when material events affect trade flows, fuel costs, border operations, or capacity additions. Right before delivery, a fresh check is completed so clients receive the most current view available at that time.

Mordor Intelligence's Iraq Freight Logistics Market Study Market Size Compared Against Other Published Estimates

Published market sizes for Iraq freight and logistics do not always match because the service scope, the year used as the base, and the way rates are converted into USD can vary across studies. Differences also show up when one estimate leans more on optimistic trade growth, while another stays conservative due to corridor constraints and execution risks.

The main gap comes from whether captive fleets and in-house warehouse operations are counted as market revenue, and Mordor Intelligence counts only invoiced third-party logistics services, which keeps totals tied to outsourced spend rather than internal cost pools.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.52 B (2026) | |

| Global Consultancy A | USD 7.24 B (2024) | Uses an earlier base year and a different service framing, with sizing that appears more tightly tied to selected service types and a faster growth path, which can understate billed logistics revenue in later years when trade and rates normalize. |

| Industry Platform B | USD 7.69 B (2025) | Applies a lower monetization assumption for logistics spend and a shorter horizon, and the lower starting value suggests differences in what is treated as billable logistics services versus broader freight movement activity. |

The spread in the table is mostly explained by year choice, what gets counted as invoiced logistics services, and how pricing and currency timing are handled. By keeping the build tied to observable trade and throughput signals and then cross-checking with practical rate and service mix inputs from interviews, the final figure stays traceable to clear steps that can be repeated at each update.

Key Questions Answered in the Report

What is the current size of the Iraq freight and logistics market?

The Iraq freight and logistics market size stands at USD 11.52 billion in 2026 and is projected to reach USD 12.73 billion by 2031.

Which segment holds the largest market share today?

Freight transport leads with 50.12% of revenue, and within that road transport alone accounts for 70.05% of tonnage moved.

How fast is e-commerce growing in Iraq?

Online retail sales are expected to rise at 9.03% CAGR (2026-2031), lifting CEP demand and making Baghdad the core last-mile battleground.

What role will the Al Faw Grand Port play in future logistics flows?

Once operational in 2025, the port’s 3.5 million TEU capacity will position Iraq as a direct Gulf-Mediterranean gateway, shortening transit times versus the Suez route.

How does Iraq’s accession to the TIR system benefit shippers?

Electronic pre-declaration and sealed-container guarantees can trim cross-border journey time by up to 80% and cut costs by about 38%, improving reliability for regional trade corridors.

What are the main challenges facing fleet operators?

Ageing vehicles, variable fuel quality and informal checkpoint fees raise operating costs and limit the reliability of time-sensitive deliveries.

Page last updated on: