Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.46 Billion |

| Market Size (2026) | USD 28.49 Billion |

| Market Size (2031) | USD 34.29 Billion |

| Growth Rate (2026 - 2031) | 3.77% CAGR |

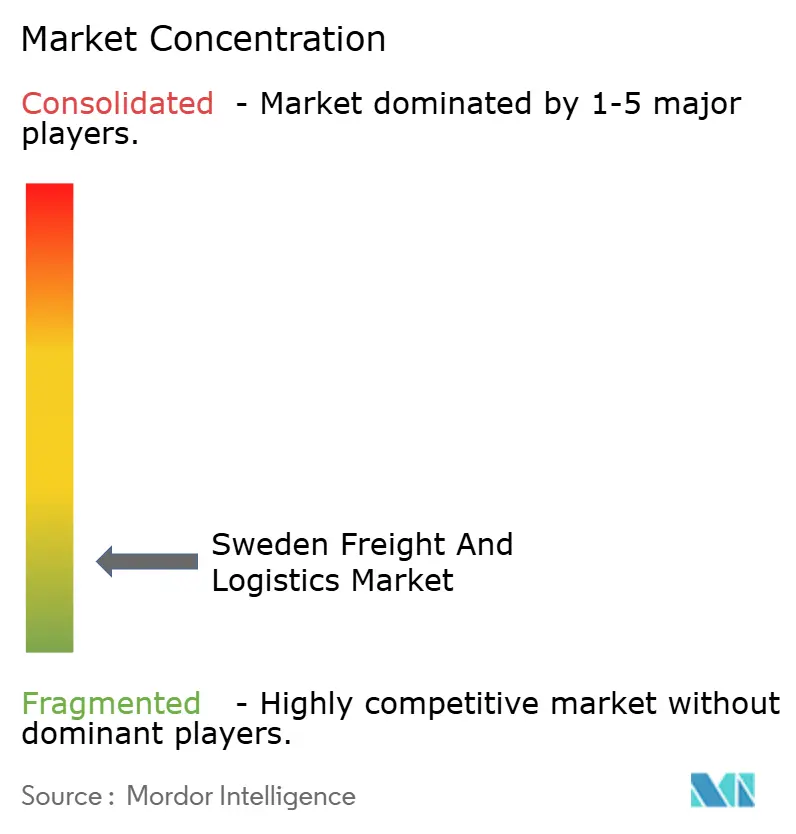

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Freight And Logistics Market Analysis by Mordor Intelligence

Sweden freight and logistics market size in 2026 is estimated at USD 28.49 billion, growing from 2025 value of USD 27.46 billion with 2031 projections showing USD 34.29 billion, growing at 3.77% CAGR over 2026-2031. The upswing stems from sustained infrastructure spending, accelerating electrification of heavy‐duty transport, and rapid adoption of warehouse automation. Robust trade links with the rest of Europe anchor demand, while the Port of Gothenburg’s capacity hike is drawing additional maritime flows. Air freight transport, although small, is advancing quickly on the back of high-value manufacturing exports and rising cross-border e-commerce parcels. Meanwhile, rail volumes are beginning to climb as carbon pricing tilts cargo away from roads, and a dense parcel locker network is easing last-mile constraints in major cities.

Key Report Takeaways

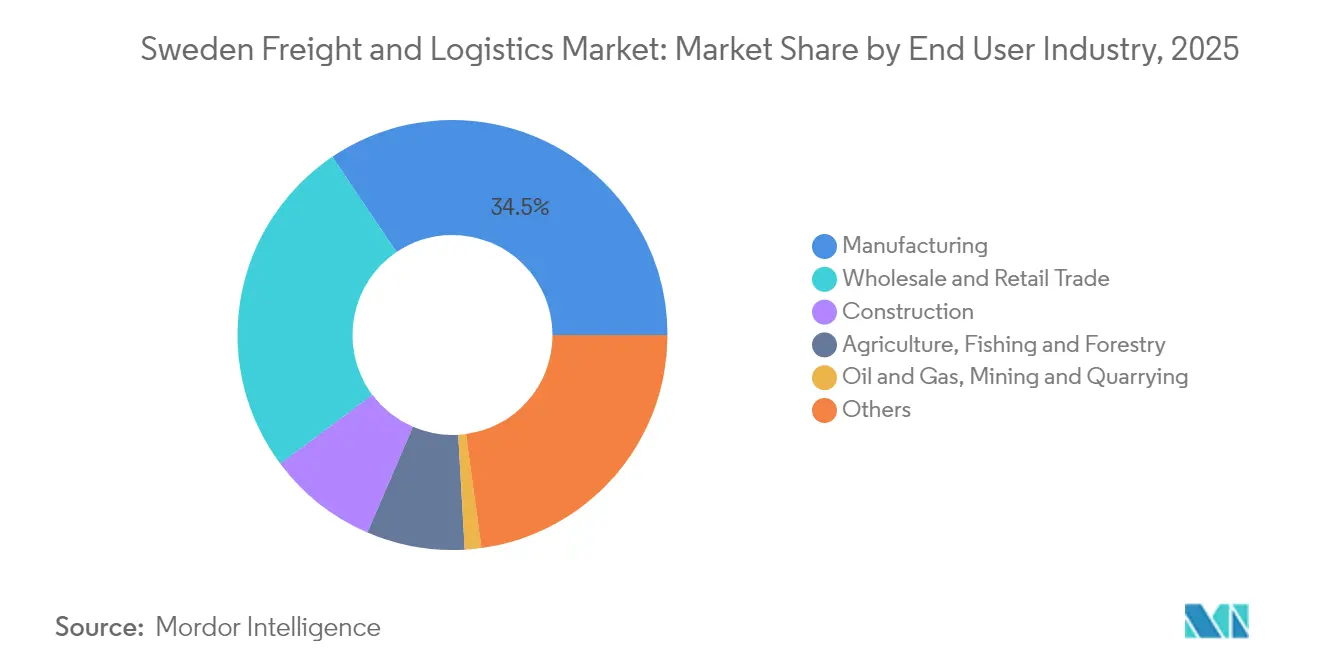

- By end user industry, manufacturing led with 34.45% of the Sweden freight and logistics market share in 2025, whereas wholesale and retail trade is forecast to post the strongest 4.02% CAGR between 2026-2031.

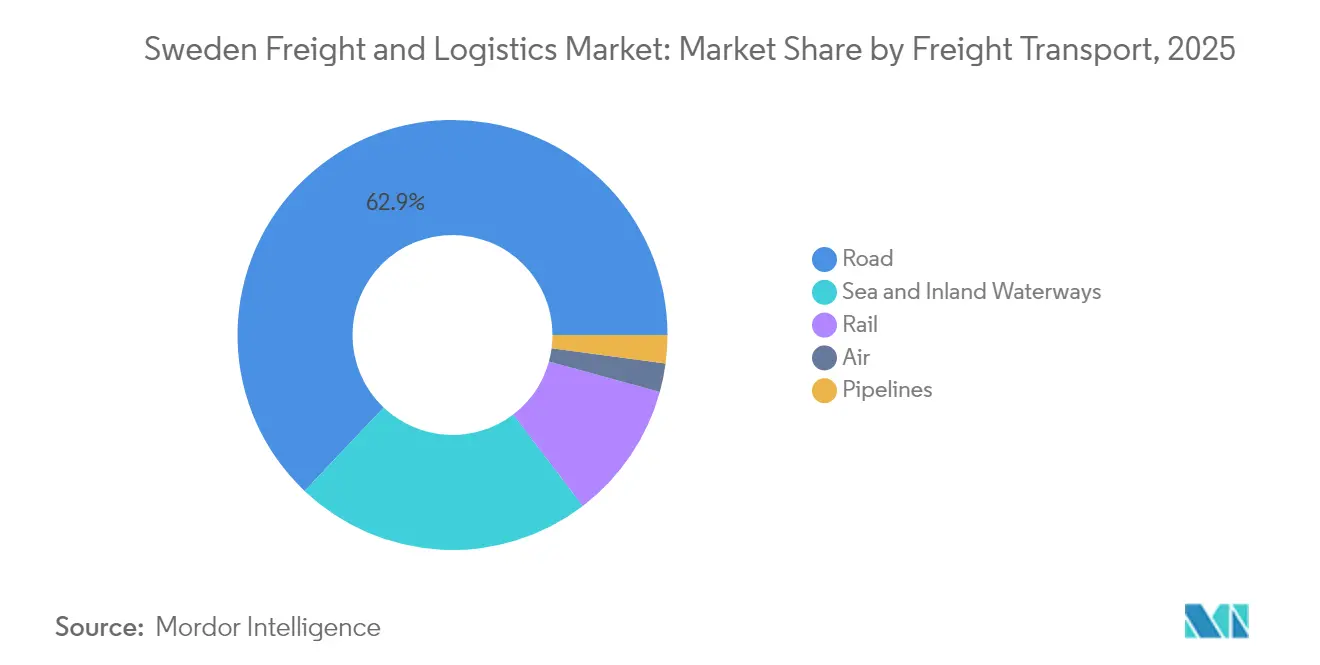

- By logistics function, the freight transport segment led with 62.95% of the Sweden freight and logistics market size in 2025; the courier, express, and parcel (CEP) segment is advancing fastest, with international CEP services expecting to grow at a 4.47% CAGR between 2026-2031.

- By freight transport mode, road freight held 62.92% revenue share in 2025, while air freight is projected to register the strongest 4.22% CAGR between 2026-2031.

- By CEP segment, domestic deliveries captured 63.40% revenue share in 2025; international CEP values are expected to grow at a 4.47% CAGR between 2026-2031.

- By warehousing and storage type, non-temperature-controlled accounted for 91.50% revenue share in 2025, whereas temperature-controlled space is forecast to expand at a 3.6% CAGR between 2026-2031.

- By freight forwarding service, sea and inland waterways dominated with 70.35% revenue share in 2025, and the expected fastest growth with CAGR of 3.98% between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government investments into green freight corridors and electrified road networks | +1.0% | National, with concentration along major highways E20 and E4 | Long term (≥ 4 years) |

| Expansion of Gothenburg port capacity to support export-oriented industries | +1.1% | Western Sweden, with spillover effects nationwide | Medium term (2-4 years) |

| Shift of cargo from road to rail driven by carbon taxation and EU Fit-for-55 policies | +0.8% | National, with emphasis on major freight corridors | Medium term (2-4 years) |

| Growing adoption of warehouse automation and robotics to offset labor shortages | +0.6% | Urban centers (Stockholm, Gothenburg, Malmo) | Medium term (2-4 years) |

| Digitalization of freight management and real-time visibility solutions | +0.5% | National, especially urban logistics | Short to medium term (1-4 years) |

| Surge in parcel volumes accelerating last-mile delivery demand across Sweden | +0.4% | National, with concentration in urban and suburban areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Investments into Green Freight Corridors and Electrified Road Networks

Sweden plans to electrify 2,000 km of high-traffic highways by 2030, including the world’s first permanent electric road on the E20 corridor[1]Euronews Staff, “Sweden Builds the World’s First Permanent Electrified Road,” euronews.com . Dynamic charging will shrink truck battery packs by up to 71%, cutting vehicle weight and cost. Because road freight transport held a 63.41% share of the freight transport segment in 2024, corridor electrification is set to reshape cost structures for long-haul operators and accelerate heavy-duty EV adoption.

Expansion of Gothenburg Port Capacity to Support Export-Oriented Industries

The Arendal 2 terminal, completed in 2024 at a cost of EUR 60 million (USD 66.21 million), adds 144,000 m² of quay and storage, lifting annual box handling well beyond the record 914,000 TEUs set in 2023. Rail track upgrades now enable 240 trains per day, triple the previous limit. The port’s deepened fairway broadens the vessel mix and anchors Sweden's freight and logistics market growth by supporting export-led manufacturers.

Shift of Cargo from Road to Rail Driven by Carbon Taxation and EU “Fit-for-55” Policies

The inclusion of shipping in the EU Emissions Trading System (ETS) and higher road user fees make rail more cost-competitive. Studies project marine fuel costs will rise 11-42% within the European Economic Area, encouraging shippers to channel higher-density cargo to rail. National greenhouse-gas reduction goals further underpin the pivot, although analysts caution that incentives must stay ahead of the decarbonizing road fleet.

Growing Adoption of Warehouse Automation and Robotics to Offset Labor Shortages

An inventory of 50 major retailers shows a marked shift toward goods-to-person systems, autonomous mobile robots, and digital twins, with automation intensity set to rise sharply by 2030. Staffing gaps, especially in aging rural districts, propel demand for automated storage and retrieval as operators safeguard service levels despite a projected 410,000 worker shortfall.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capacity constraints on key rail freight lines (Nordic Triangle) causing delays | -0.6% | Major rail corridors connecting Stockholm, Gothenburg, and Malmö | Medium term (2-4 years) |

| High logistics costs from long-haul distances and low back-haul utilization in north | -0.4% | Northern Sweden (Norrland region) | Long term (≥ 4 years) |

| Driver shortage exacerbated by aging workforce and restrictive migration rules | -0.3% | National, with greater impact in rural areas | Medium term (2-4 years) |

| Port strikes and labor-union disruptions affecting container throughput | -0.3% | Port cities (primarily Gothenburg) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capacity Constraints on Key Rail Freight Lines Causing Delays

Rail carries a significantly lower share of national freight, partly because the Nordic Triangle corridor lacks slots for rising cargo flows. The Malmbanan iron ore line suffered multiple derailments in 2023, halting trade for weeks. Although SEK 165 billion (USD 16.35 billion) has been earmarked for rail upgrades through 2033, industry groups argue the outlay falls short of the SEK 280 billion (USD 27.74 billion) needed to clear critical choke points[2]Swedish Transport Administration, “National Transport Infrastructure Plan 2022-2033,” trafikverket.se.

High Logistics Costs from Long-Haul Distances and Low Back-Haul Utilization in the North

Sparse density forces trucks to return empty on northern routes, pushing unit costs 25-40% above the national mean[3]OECD, “International Trade in the Wake of Multiple Shocks,” oecd.org . Transport makes up as much as 18% of production expenses for forestry and mining firms, reducing competitiveness until the Bothnian Corridor rail link is completed later next decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing Drives Logistics Demand

The manufacturing segment accounted for the largest share of around 34.45% in 2025 within the Sweden freight and logistics market. Automotive, machinery, and high-tech producers funnel considerable volumes through Gothenburg and intermodal depots, requiring time-defined, multimodal solutions. The wholesale and retail trade segment is expected to grow the fastest at 4.02% forecast CAGR (2026-2031), signalling that online retail’s parcel surges will steadily close the gap. Construction leans on bulk transport for cement, steel, and project cargo tied to the green-energy build-out. Agriculture, fishing, and forestry, strong pulp exports via Gothenburg kept flows resilient despite global price swings. Mining and energy underpin dedicated rail and port infrastructure in the North.

Growth prospects differ across verticals. Manufacturing continues to retool for electrified mobility and low-CO₂ metals, spurring demand for inbound battery cells and outbound finished vehicles. Wholesale and retail trade is leveraging parcel lockers and same-day services to sharpen customer propositions. Construction logistics gains from state funding for electrified highways and port expansions. Resource sectors depend on rail reliability; any disruption diverts high-tonnage ore back to road, stressing sustainability goals. Broadly, 8 in 10 Nordic consumers now weigh sustainability in purchasing, pressuring shippers across every vertical to decarbonize distribution.

By Logistics Function: Freight Transport Dominates While Courier, Express, and Parcel (CEP) Accelerates

Freight transport generated 62.95% of total revenues in Sweden freight and logistics market in 2025. Road freight transport remained king, handling short-haul pallets, groupage, and temperature-controlled food distribution. Sea and inland waterways freight transport benefited from direct Asia loops calling Gothenburg. Rail freight transport gained share where green-steel producers signed forward contracts for zero-carbon rail haulage. Air freight transport is small yet strategic for high-value electronics and urgent spares, expected to grow at a CAGR of 4.22% from 2026-2031. The CEP segment captured a significant revenue share of the total revenues on the strength of e-commerce and next-day cross-border offering. Freight forwarding is consolidating as global intermediaries acquire niche Scandinavian brokers to scale digital booking tools. The warehousing and storage segment is the hotbed of automation trials; non-temperature facilities dominate with a 91.50% segment share in 2025.

Margin trends vary. Road carriers face higher capital outlays as they electrify fleets, yet lower fuel and maintenance expenses offset some costs. Maritime lines must factor ETS charges, nudging them toward LNG, methanol, or biodiesel. Air cargo operators embed sustainable aviation fuel surcharges in Scandinavia’s largest gateways. Forwarders are merging to fund visibility platforms that can span every mode. Warehouse operators invest heavily in robotics, trading higher capex for labor savings and improved throughput.

By Courier, Express, and Parcel: E-commerce Reshapes Delivery Networks

In the CEP arena, domestic parcels accounted for 63.40% revenue share in 2025. International flows, though smaller, are forecast to outpace domestic at a 4.47% CAGR (2026-2031). E-commerce orders translated into 243 million parcels for PostNord alone in 2023, up 6% year on year. Consumers prize optionality: 59% want to select delivery mode, and parcel-locker preference climbed to 20% in 2023 from 5% four years earlier. Home delivery is still preferred by 68% of shoppers, but only 42% of merchants provide it, leaving white space for innovators.

Competition is fierce. PostNord commanded the highest segment share in 2023, trailed by DHL with the second-highest segment share. Deutsche Bahn/DB Schenker, UPS, and FedEx each hold low-single-digit portions. Consolidation looms: DSV’s 2025 takeover of DB Schenker broadens cross-border parcel capacity. Technology is decisive in the current market. PostNord’s AI-enhanced Rosersberg sorter lifts hourly throughput 70%, raising accuracy to 99.8%. Operators race to electrify last-mile vans to satisfy city clean-air mandates.

By Warehousing and Storage: Automation Transforms Operations

Non-temperature buildings accounted for 91.50% of the segment revenue share in 2025 as Sweden’s exports lean toward paper, machinery, and consumer goods. The sector’s Sweden freight and logistics market share for automated solutions is rising as retailers deploy goods-to-person technology to handle SKU proliferation. Average automation penetration is forecast to double by 2030. Case in point: a logistics property in Borås changed hands in 2024, prized for its AutoStore grid and 12-ton floor load.

Temperature-controlled warehousing, expected to grow at a CAGR of 3.6% (2026-2031), services pharmaceuticals and a thriving frozen-food sector. EQT’s acquisition of Constellation Cold Logistics underscores private equity’s appetite for temperature-controlled nodes. Operators upgrade to natural refrigerants and pursue BREEAM certifications to lock in multinational tenants that pledge science-based targets.

By Freight Transport Mode: Road Flexibility Meets Rail Sustainability

Road freight transport accounted for a 62.92% revenue share in 2025. Its reach across dispersed towns remains unmatched, particularly for perishables and home-delivery parcels. Road freight transport is expected to grow as charging corridors lower the total cost of ownership for battery electric trucks. Sea and inland waterways freight transport was anchored by Gothenburg’s deep-sea links and Stena Line’s Baltic ro-ro lanes. Rail freight transport could grow in value if capacity upgrades in the Nordic Triangle keep pace with demand. Air freight transport is expected to capture the strongest CAGR at 4.22% between 2026-2031, driven by semiconductor equipment and biotech shipments that value speed over cost.

Rail’s competitiveness hinges on infrastructure works funded under the SEK 165 billion (USD 16.35 billion) national plan. Shippers are ready to switch high-density cargo once block-train paths are guaranteed. Road hauliers plan to halve emissions by 2030 through a mix of electric and biogas fleets. Maritime operators prepare to pass through ETS costs, but also pilot green methanol bunkering. Air cargo’s growth remains tied to belly capacity on intercontinental passenger flights; schedule restoration following the pandemic is a tailwind.

By Freight Forwarding: Maritime Dominance Amid Modal Integration

Sea and Inland Waterways freight forwarding represented 70.35% revenue share in 2025, mirroring Sweden’s export profile of heavy and bulky goods. The Sweden freight and logistics market size for sea and inland waterways freight forwarding is forecast at a 3.98% CAGR from 2026-2031, helped by integrated digital platforms that stitch together sea and last-mile legs. Air freight forwarding caters to just-in-time supply chains in electronics and life sciences. The remaining covers customs clearance, project cargo, and supply-chain advisory.

Consolidation is brisk. Logwin bought Infranordic Shipping in late 2024 to fortify Scandinavian reach and integrate TMS solutions. Buyers seek scale to tap into real-time visibility, CO₂ tracking, and compliance modules. Forwarders also secure rail capacity blocks as a hedge against maritime ETS surcharges.

Geography Analysis

Western Sweden, anchored by Gothenburg, is the country’s foremost logistics gateway. The port handled 57% of national container throughput and logged 5% volume growth in H1 2024. Adjacent rail upgrades tripled daily train slots, connecting export-heavy clusters in Jonkoping and Vastra Gotaland. Ongoing fairway deepening accommodates larger LNG-ready vessels, reinforcing the Sweden freight and logistics market as an indispensable Nordic hub.

The Stockholm-Malaren basin hosts Sweden’s largest consumer catchment. Distribution centers around Eskilstuna and Vasteras support next-day parcel delivery across the capital region. Rising demand for choice drives investment in micro-fulfillment sites and parcel-locker grids. E-commerce players deploy AI demand-planning to minimize urban traffic peaks while preserving service promises. Proximity to Arlanda’s expanding cargo apron supports time-critical pharma and fashion imports destined for central Sweden boutiques.

The south, including Malmo, leverages the Oresund Bridge to funnel trade to Denmark and continental Europe. The Copenhagen-Malmo Port reported a 12% lift in cargo in 2023 and secured EUR 44 million (USD 48.56 million) in EU green port funding. Real-estate investors continue to add sustainable logistics parks near the E6 corridor, lured by demand for cross-border fulfillment. Skane’s horticulture exports generate back-haul for refrigerated trucks otherwise returning empty from northern markets.

Competitive Landscape

The Sweden freight and logistics market features a blend of global integrators and specialized regional operators. DSV’s USD 15.7 billion takeover of DB Schenker in April 2025 elevates the Danish group into the top tier of Nordic service providers and unlocks cost synergies of up to USD 770 million annually. PostNord remains one of the top CEP leaders; its digital-twin sorting platform boosts throughput 6-8% while trimming error rates, preserving its edge in a margin-tightening parcel market. DHL, another significant player in the market, showcased its green credentials by opening a solar-powered logistics center in Örebro in January 2025.

Regional challengers carve out niches. Bring targets full fossil-free parcel delivery by 2025 and already reports a 51% CO2 cut versus 2012 levels. Instabee leverages app-based aggregation to match deliveries with consumer schedules, chipping at incumbents’ urban share. Real-estate investors such as Storebrand and EQT funnel capital into automated and temperature-controlled warehouses, letting 3PLs scale without heavy balance-sheet strain.

Strategy pivots toward end-to-end control. A.P. Moller-Maersk’s USD 45 million omnichannel facility in Torsvik melds warehousing with contract logistics, aligning with its goal of sourcing half of group revenue from non-ocean services by 2030. Forwarders and carriers alike are bundling visibility, compliance, and sustainable-fuel options to retain multinational shippers tightening Scope 3 reporting.

Sweden Freight And Logistics Industry Leaders

DSV A/S (including DB Schenker)

DHL Group

PostNord (incl. PostNord Sverige AB)

A.P. Moller - Maersk (including Maersk Sverige AB)

Green Cargo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its EUR 14.22 billion (USD 15.69 billion) acquisition of DB Schenker, creating a USD 37 billion revenue logistics giant.

- March 2025: A.P. Moller-Maersk opened a 43,000 m² automated warehouse in Torsvik powered by 100% renewables.

- February 2025: PostNord commissioned a USD 65 million AI-driven sorter in Rosersberg, raising capacity to 40,000 parcels per hour.

- January 2025: DHL inaugurated a 25,000 m² BREEAM-Excellent logistics hub in Orebro featuring 1.2 GWh solar output.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Sweden's freight & logistics market as all paid revenues that arise when independent providers move goods inside, into, or out of Sweden by road, rail, sea, air, or pipeline and when they offer allied services such as freight forwarding, warehousing, CEP, and customs brokerage. The value pool therefore captures external spend only, not the internal costs of captive fleets or shipper-owned depots.

Scope exclusion: Passenger transport and purely in-house logistics operations are outside the frame.

Segmentation Overview

- By End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- By Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview carriers, 3PL managers, port officials, and large B2B shippers across Stockholm, Gothenburg, Malmö, and the iron-ore corridor. These conversations validate rate corridors, occupancy levels, emerging green-corridor premiums, and help us refine underlying cost and utilization assumptions before final triangulation.

Desk Research

We first map the demand base through Swedish Transport Administration traffic volumes, Statistics Sweden trade and production series, Eurostat modal splits, Port of Gothenburg throughput tables, and industry position papers from bodies such as Sveriges Åkeriföretag. Company filings, IPO prospectuses, and investor decks illuminate service yields and cost structures, while news flows retrieved via Dow Jones Factiva track tariff shifts and capacity expansions. Paid databases, D&B Hoovers for operator financials and Questel for patent activity around autonomous trucking, supply further granularity. The sources named illustrate our approach; many additional public and subscription datasets were reviewed for cross-checks.

Market-Sizing & Forecasting

A top-down model starts with Sweden's freight output (ton-km and SEK turnover) and reconstructs value by applying service-mix weights and average selling prices. Results are then compared with selective bottom-up roll-ups drawn from leading carrier revenues and sampled warehouse lease rates. Key variables include e-commerce parcel growth, rail modal-share shifts under Sweden's carbon tax, fuel indexation clauses, warehouse automation uptake, and average export container dwell times. Forecasts employ multivariate regression blended with scenario analysis to capture sensitivity to GDP, diesel prices, and EU Fit-for-55 policy milestones. Gaps in bottom-up coverage, especially in niche CEP routes, are bridged through interpolations agreed during primary interviews.

Data Validation & Update Cycle

Outputs pass a two-step analyst peer review, variance tests against independent trade statistics, and a senior sign-off. The database refreshes annually; interim updates are triggered when fuel prices, labor costs, or regulatory rulings move beyond preset thresholds.

Credibility of Our Sweden Freight And Logistics Baseline

Published estimates often diverge because firms pick different service baskets, convert currencies at varied dates, or refresh on uneven cadences.

Key gap drivers here include whether warehousing income is counted, how in-house fleet spend is treated, and if postal subsidies are folded into CEP totals. Our disciplined scope selection, yearly refresh, and dual-path validation mean stakeholders receive a stable, transparent baseline they can retrace.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 27.46 B (2025) | Mordor Intelligence | - |

| USD 42.0 B (2024) | Global Consultancy A | Bundles captive-fleet costs and government postal support |

| USD 3.8 B (2023) | Market Analytics B | Counts only road freight turnover; excludes forwarding & warehousing |

Taken together, the comparison shows that when overly broad costs are included or major functions are omitted, market values swing sharply. By anchoring estimates to externally verifiable freight flows and service revenues, Mordor Intelligence delivers a balanced, decision-ready view.

Key Questions Answered in the Report

How large is the Sweden freight and logistics market in 2026?

It stands at USD 28.49 billion and is projected to reach USD 34.29 billion by 2031, implying a 3.77% CAGR (2026-2031).

Which freight transport mode holds the biggest share?

Road haulage dominates with 62.92% share in 2025 thanks to flexible last-mile reach.

What is the fastest-growing segment under freight transport?

Air freight transport leads with an expected 4.22% CAGR between 2026 and 2031, driven by high-value exports and e-commerce.

Who are the top CEP players in Sweden?

PostNord leads with 34.10% market share, followed by DHL at 19.52% and Posten Bring.

How is electrification shaping freight transport?

Government plans to electrify 2,000 km of highways and dynamic-charging pilot roads are set to lower operating costs for heavy-duty EVs and cut emissions across long-haul corridors.

What challenges limit rail freight growth?

Capacity bottlenecks on the Nordic Triangle corridor and funding gaps in track upgrades delay modal shift from road to rail.

Page last updated on: