Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

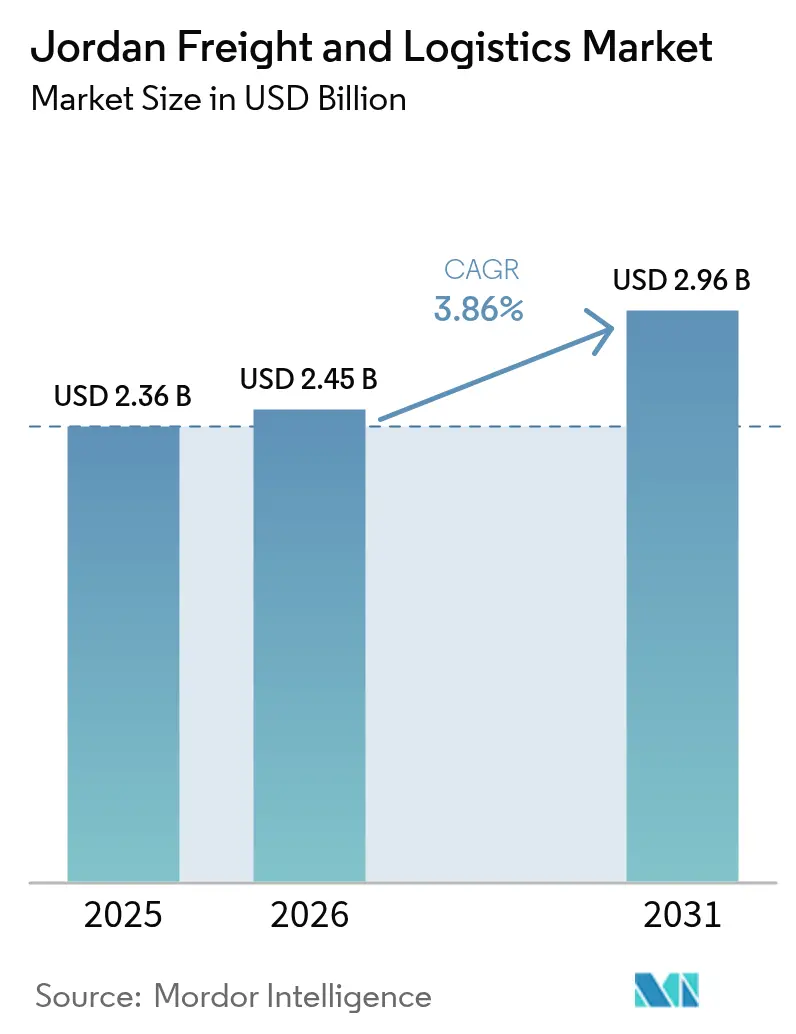

| Base Year Market Size (2025) | USD 2.36 Billion |

| Market Size (2026) | USD 2.45 Billion |

| Market Size (2031) | USD 2.96 Billion |

| Growth Rate (2026 - 2031) | 3.86% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jordan Freight And Logistics Market Analysis by Mordor Intelligence

The Jordan freight and logistics market size is expected to grow from USD 2.36 billion in 2025 to USD 2.45 billion in 2026 and is forecast to reach USD 2.96 billion by 2031 at 3.86% CAGR over 2026-2031. Rising Gulf investment, steady manufacturing output, and steady e-commerce adoption keep freight volumes expanding even as regional shipping lanes realign. Public–private partnerships under the Economic Modernization Vision channel USD 2.3 billion into roads, rail, and port upgrades, anchoring Jordan’s role as a transit gateway for cargo moving between Asia, the Levant, and the Gulf. Container diversions caused by Red Sea disruptions are funneling additional throughput through Aqaba Port, while airport cold-chain expansions lift the share of high-value perishables and pharmaceuticals. Digital freight platforms, government vehicle-tracking mandates, and 960 automated public services collectively improve shipment visibility, reduce empty back-haul ratios, and reinforce the Jordan freight and logistics market as a regional reliability hedge.

Key Report Takeaways

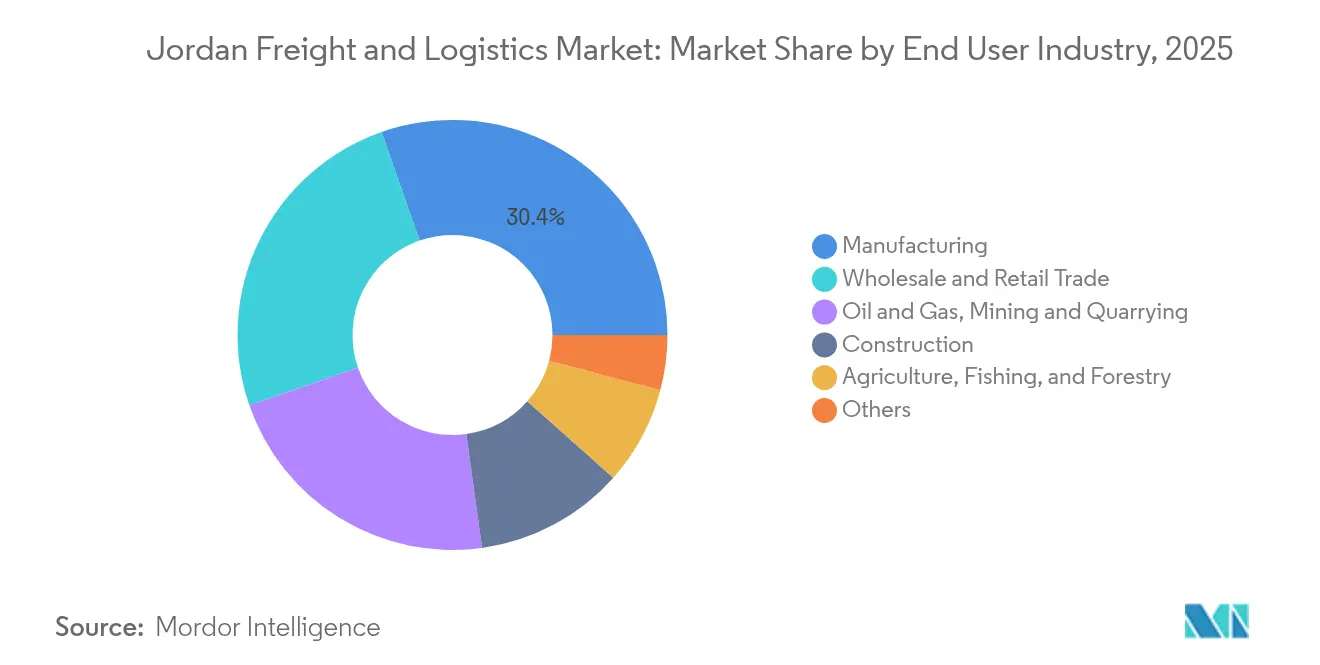

- By end user industry, manufacturing generated 30.35% of the Jordan freight and logistics market share in 2025, while wholesale and retail trade is projected to expand at a 4.18% CAGR between 2026 and 2031.

- By logistics function, freight transport led with 53.55% of the Jordan freight and logistics market size in 2025, while courier, express, and parcel (CEP) posted the fastest projected CAGR at 4.55% between 2026 and 2031.

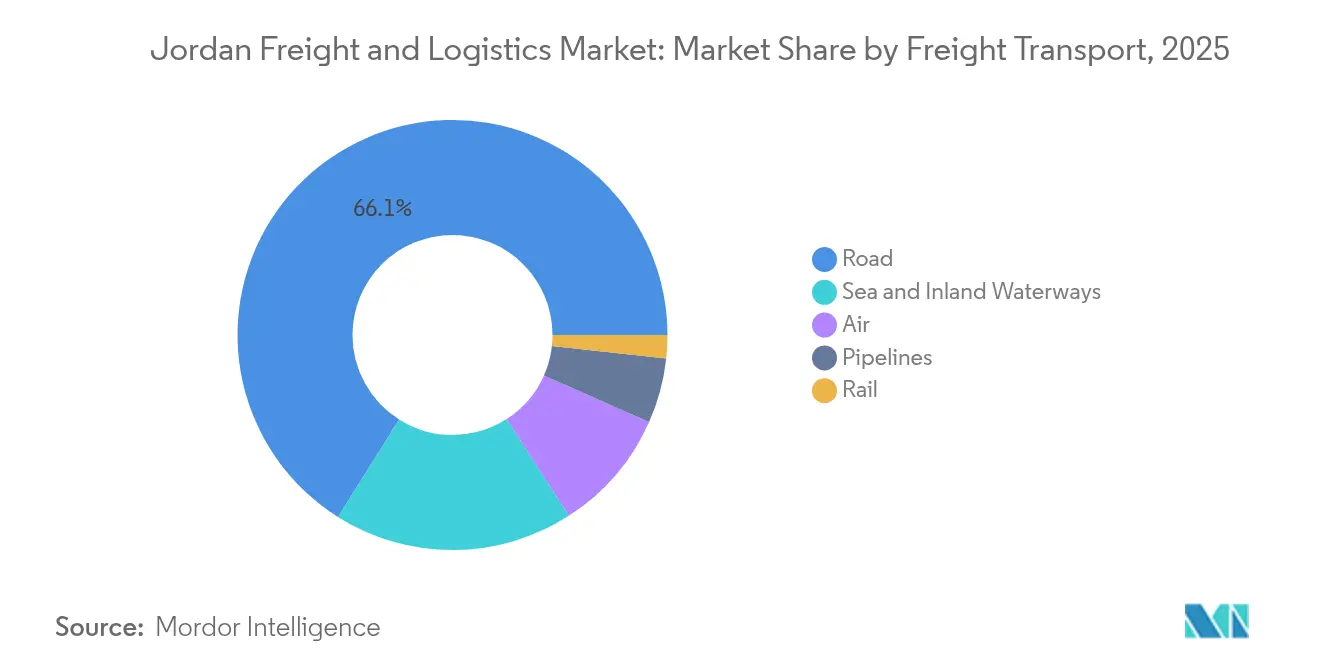

- By freight transport mode, road freight transport captured 66.05% revenue share in 2025; air freight transport is projected to advance at a 5.02% CAGR between 2026 and 2031.

- By CEP segment, domestic services held 64.85% revenue share in 2025, whereas international CEP is forecast to climb at a 4.71% CAGR between 2026 and 2031.

- By warehousing and storage, non-temperature controlled facilities accounted for 91.88% of the revenue share in 2025; temperature controlled space records the highest segment CAGR (2026-2031) at 4.55%.

- By freight forwarding mode, sea and inland waterways freight forwarding commanded 67.95% revenue share in 2025, and air freight forwarding shows the quickest projected 4.46% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Jordan Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Jordan allocates USD 2.3 billion for logistics CapEx under economic modernization vision 2023-25 | +0.8% | National, focused on the Amman–Aqaba corridor | Medium term (2-4 years) |

| Aqaba port in Jordan sees a significant surge in container throughput, bolstered by the impending GCC rail link | +0.6% | Southern Jordan, extending to GCC markets | Long term (≥ 4 years) |

| EU near-shored cargo volume routed through Jordan sees a considerable increase | +0.5% | National, emphasis on northern trade routes | Short term (≤ 2 years) |

| Queen Alia airport in Jordan sees a significant surge in air-reefer exports for pharma and fresh produce | +0.4% | Central Jordan, global export reach | Medium term (2-4 years) |

| Rising government regulatory reforms and trade facilitation initiatives | +0.4% | National, with border crossing focus | Medium term (2-4 years) |

| Accelerated adoption of digital freight platforms e.g., Trella | +0.3% | National, urban concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Jordan Allocates USD 2.3 Billion for Logistics CapEx under the Economic Modernization Vision

Capital commitments across 344 projects fund modern roads, a north–south rail spine, and first-mile digitization for customs clearances. The program integrates private finance to accelerate design–build cycles and targets one million youth job placements by 2033. A dedicated freight line between Aqaba and Maan will remove heavy trucks from key highway segments, cut fuel burn, and allow 25-car unit trains to haul minerals and containers. Expanded truck rest areas, weigh-in-motion sensors, and smart tolling are set to trim journey times on the Amman Ring Road. Early macro signals already show national exports up 8.1% year-on-year in February 2025, while FDI climbed 3.7% in 2024, underscoring the Vision’s near-term stimulus.

Aqaba Port Sees Higher Throughput, Boosted by the Future GCC Rail Link

The three-berth container terminal now works with larger Post-Panamax vessels after recent quay dredging and yard automation upgrades[1]Jordan Logistics Cluster, “Aqaba Port Factsheet,” lca.logcluster.org. With Suez Canal volumes down 82% during security incidents, carriers repositioned strings to Aqaba, swelling import flows to Jordan and re-export cargo to Saudi Arabia and Iraq. Planned rail interoperability will connect the port to the 2,177 km GCC network engineered to shift up to 31 million tons annually, unlocking long-haul, low-carbon inland corridors. Maersk alone has invested USD 300 million since 2006 and targets a 70% cut in terminal emissions by 2030.

Queen Alia Airport Captures High-Value Cold-Chain Exports

Pharmaceuticals and fresh produce benefit from new apron-side cool rooms, GDP-certified handling, and upgraded reefers. The Cool Up program backs technology retrofits and technician training that lift temperature-compliance rates above 98%[2]Cool Up Programme, “Cold-Chain Retrofit Case Studies,” coolupprogramme.org. Etihad Cargo doubled its regional cool-chain lift, while WDA(H)-licensed forwarders such as Aramex ensure audit trails that satisfy EU Good Distribution Practice for vaccines. Ongoing USAID support for IoT sensor deployment lets customs and shippers scan real-time temperature logs, reducing claims and deepening exporter confidence.

EU Near-Shored Cargo Volume Through Jordan Jumps

Retailers and automotive OEMs seeking swift replenishment now truck containers from Haifa and Aqaba across Jordan to Gulf free zones, trimming door-to-door times by as much as 10 days. Jordan’s road network ranks 35th globally for competitiveness and supports 40-ton semitrailers on multilane highways. Customs fee waivers and 5% corporate income tax inside investment zones reinforce Jordan’s draw as an inflation-hedge hub for European shippers. Automated single-window customs clearance, live in 2025, now clears compliant consignments in under two hours, supporting the Jordan freight and logistics market in absorbing redirected European orders.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outside Amman, Jordan, most warehousing facilities lack temperature control | -0.4% | Rural and secondary urban areas | Medium term (2-4 years) |

| At Al-Omari, the median border dwell time stands at 22 hours, significantly higher than the GCC average of 6 hours | -0.3% | Northern border with Syria | Short term (≤ 2 years) |

| Rail freight accounts for a significantly smaller share of the national ton-km | -0.2% | Nationwide rail network | Long term (≥ 4 years) |

| Agri trucks face a high dead-head ratio on back-hauls due to water scarcity | -0.2% | Agricultural regions, especially Jordan Valley | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Outside Amman, Most Warehousing Stock Lacks Temperature Control

Less than 8% of nationwide space meets GDP-level cold-chain specifications, leaving a service gap for pharmaceuticals, dairy, and floriculture exports. Rural growers often move produce 200 km to Amman for pre-cooling, adding costs and spoilage risk. Cool Up pilot projects are installing solar-powered ammonia CO₂ systems in Mafraq and Irbid, yet network-wide rollout remains years away. The government has earmarked part of the USD 2.3 billion logistics fund for cold-room grants, but land pricing and fragmented ownership slow site aggregation.

Border Dwell Time at Al-Omari Remains Four Times the GCC Average

Trucks queue for security inspections, veterinary checks, and paper manifests, turning the northern crossing into a chronic bottleneck that erodes Jordan’s hub credentials. Each extra hour of waiting inflates operating costs by USD 27 per truck, research by the Ministry of Transport shows[3]Ministry of Transport, “National Transport Strategy 2025,” mot.gov.jo. Planned biometric driver cards and pre-arrival data lodgment are expected to cut hold-ups, but the capital works for extra inspection bays will not finish before 2027. High perishables risk forces exporters to reroute via Saudi entry points, diverting potential traffic away from the Jordan freight and logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Leads Logistics Demand

Manufacturing produced 30.35% of logistics revenue in 2025, with chemicals, textiles, and potash processors moving high-frequency loads. Bonded factories in Qualified Industrial Zones exploit duty-free access to the United States, creating steady container flows. Wholesale and retail trade grows at 4.18% CAGR (2026-2031) as omnichannel grocers push regional store penetration and same-day click-and-collect.

Energy projects and civil infrastructure sustain bulky inbound shipments of turbines, steel, and cement. Potash miners near the Dead Sea dispatch 2.5 million tons annually to Asian fertilizer markets via Aqaba, underpinning demand for covered bulk wagons once rail goes live. Agricultural co-operatives, meanwhile, rely on reefer trucks to reach Saudi buyers, although water scarcity keeps back-haul ratios elevated.

By Logistics Function: Freight Transport Dominates Market Structure

Freight Transport generated 53.55% of 2025 revenue, confirming its pivotal role in the Jordan freight and logistics market. General cargo, break-bulk fertilizers, and containerized consumer goods feed stable lane density between Aqaba, Amman, and the Iraqi border. The segment benefits from continuous highway resurfacing and GPS-based weight compliance that limit axle damage and extend fleet life. CEP, though smaller, scales quickly with smartphone adoption and a youthful online shopper base that exceeded 75% of Jordanian internet users in 2024. Digital booking portals bundle transport, customs, and last-mile options, shrinking lead times and boosting pickup density across urban rings.

The Jordan freight and logistics market sees value-added warehousing and freight forwarding integrating more tightly with transport operators to secure end-to-end contracts for big-box retailers. Supply-chain orchestration platforms such as Trella enhance load matching and cut empty mileage. Government tax rebates on Euro 5 trucks sweeten fleet renewal economics and underpin the 3.86% freight and logistics market CAGR (2026-2031). CEP companies ride e-commerce peaks by offering subscription lockers and evening deliveries, while traditional 3PLs tap spare van capacity to penetrate small-parcel flows.

By Courier, Express, and Parcel (CEP): Domestic Services Lead Market Penetration

Domestic CEP accounted for 64.85% of revenue share in 2025, propelled by dense drops inside Greater Amman and Irbid. Same-day services, once a premium add-on, now cover more than half of intra-city orders after vehicle routing algorithms lifted stop counts per van. International parcels grow more briskly at a 4.71% CAGR (2026-2031) as MSMEs export craft wear to Europe under preferential rules of origin. Aggregated return-management hubs in Zarqa pool reverse flows, driving down per-item handling costs.

Cross-border shoppers benefit from live duty calculators and flat-rate clearance fees that the customs single window rolled out in 2025. Major CEP players adopt smart lockers at gas stations, raising first-attempt delivery success above 96%. Blockchain verification for high-value items reduces fraud, reinforcing consumer trust and supporting the Jordan freight and logistics market.

By Warehousing and Storage: Non-Temperature Facilities Dominate Infrastructure

Non-temperature controlled warehouses represented 91.88% of revenue share in 2025, reflecting the historical tilt toward durable consumer goods, garments, and mechanical parts. Such sites cluster along Amman’s Airport Road and the Sahab industrial estate, leveraging six-lane access and high dock density. Temperature controlled space, though only 8.12% in 2025, expands at a 4.55% CAGR (2026-2031) as pharmaceutical majors re-shore regional distribution hubs to Jordan’s free zones.

Demand for 2–8°C rooms outpaces construction as vaccine producers and supermarket chains lock in multi-year leases. Developers retrofit idle sites with insulated panels and trans-critical CO₂ systems, taking advantage of Jordan’s solar abundance to cap energy bills. Cold-room investments also unlock fresh export lanes for strawberries and cherries routed by air to Gulf supermarkets within 24 hours.

By Freight Transport: Road Infrastructure Drives Modal Dominance

Road freight transport commanded 66.05% of segment share in 2025, anchoring the Jordan freight and logistics market on a backbone of 7,000 km of paved highways. Fleet telemetry and a government tracking mandate allow carriers to optimize routing and curb fuel wastage. The 5.02% CAGR (2026-2031) projected for air freight transport reflects expanded cool-chain lift and new weekly pharma charters from Queen Alia Airport into Frankfurt and Singapore. Sea and inland waterways, served by Aqaba, handle heavyweights such as autos and grains, while pipelines continue to move crude and refined products to refinery gates.

The upcoming GCC railway spur promises to recalibrate modal economics by shifting long-haul containers and bulk moves from road to steel wheel. Shippers eye a 30% cost reduction once 1,200-meter-long trains link Aqaba to the Saudi border. Until commissioning, the road remains indispensable for farm-to-port hauls, cement and potash distribution, and aid shipments to Syria. Air freight’s weight share stays minor, yet its value share rises as Jordanians shop cross-border fashion and time-critical medical spare parts.

By Freight Forwarding: Sea and Inland Waterways Routes Leverage Port Connectivity

Sea and inland waterways freight forwarding secured 67.95% of 2025 revenue share, mirroring Aqaba’s status as Jordan’s sole deep-water gateway. Maersk and CMA CGM deploy feeders to Jeddah and Port Said, enabling weekly transshipment cycles. The Jordan freight and logistics market expects air freight forwarding to lift margins faster at 4.46% CAGR (2026-2031) as semiconductor tooling, dialysis consumables, and aerospace spare parts transit through Queen Alia.

Forwarders embed emission dashboards to help shippers compare mode-wise carbon footprints, a feature winning bids from European retailers facing Scope 3 reporting mandates. Rail forwarding remains nascent, but feasibility studies plan roll-on/roll-off wagons that let trucks drive onto flat cars for the Aqaba–Amman trip, shaving five hours off transit.

Geography Analysis

The Amman-Aqaba corridor funnels a majority of national freight, supported by six-lane highways, double-stack container yards, and a steady pipeline of donor-funded upgrades. Gulf investors have placed USD 4 billion on the Amman Stock Exchange since 2020, signaling confidence in the corridor’s continued throughput growth. Expansion of Aqaba Container Terminal creates 500,000 m² of paved stacking ground, enabling the Jordan freight and logistics market to accommodate greater transshipment volumes should Red Sea insecurity persist.

Northern gateways lag. At Al-Omari, 22-hour dwell times suppress traffic toward Syria, and refrigerated haulers often reroute via Al Mudawara to dodge delays. Grain silos at Irbid and Mafraq require better last-mile roads to absorb future rail-to-road handovers. USAID-funded weigh-in-motion sensors are now being installed, a first step toward harmonizing axle standards with GCC neighbours.

Secondary cities such as Zarqa, Karak, and Salt witness rising demand for 3PL services as retail chains spread warehouse spokes beyond the capital. Yet land scarcity and zoning rules keep new builds slow. Mobile cargo apps now link rural drivers with city shippers, improving load factors and incorporating these peripheries into the Jordan freight and logistics market. Once the GCC rail spur is commissioned, planners anticipate dry ports in Mafraq and Ma’an, accelerating hinterland development and balancing today’s corridor concentration.

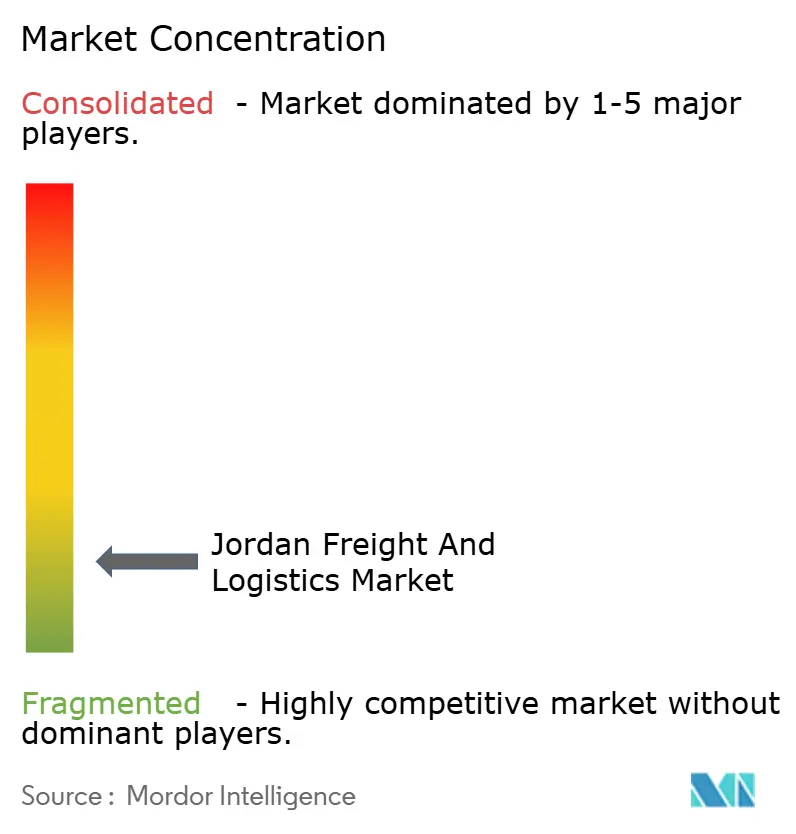

Competitive Landscape

Competition remains fragmented despite the presence of global integrators. Multinationals leverage standardized IT and procurement muscle, while domestic fleets of fewer than 50 trucks still dominate primary haulage corridors. Scale is changing: the April 2025 acquisition of DB Schenker by DSV unites roughly 160,000 employees under one banner, raising the service ceiling for complex aerospace and life-science contracts. Local champions respond by forming asset-light alliances, pooling yards, and sharing customs brokers to retain their share.

Partnerships between global and regional specialists grow. CEVA and Almajdouie’s Saudi JV combines CEVA’s network tools with 2,000 regional tractors, allowing through-billing for Riyadh–Amman milk runs. Jordanian SMEs concentrate on last-mile niches, serving remote villages and offering cash-on-delivery, a must-have option for 55% of e-commerce shoppers in 2024. Market entrants with cold-chain expertise find white-space as only a handful of facilities outside Amman meet GDP certification.

Technology adoption separates leaders from laggards. Major forwarders deploy predictive ETA engines that ingest border wait-time data. Smaller fleets tap shared telematics subscriptions, gaining compliance without large CAPEX. Sustainability credentials also win business; Maersk’s target to cut terminal CO₂ by 70% resonates with European shippers seeking low-carbon corridors. Such differentiated offerings support a vibrant Jordan freight and logistics market even as consolidation progresses.

Jordan Freight And Logistics Industry Leaders

Aramex (Including Aslas)

Naouri Group

DHL Group

A.P. Moller - Maersk

GAC Group (Holdings), Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Aramex partnered with Sprinklr to automate 99% of customer service cases and save over 1 million agent hours annually, enhancing last-mile efficiency.

- April 2025: DHL Group signed an MoU with Temu to provide multimodal solutions that assist Middle East SMEs in compliant cross-border trade.

- March 2025: UPS launched UPS Global Checkout, leveraging AI to calculate duties and taxes upfront for shoppers in 43 countries.

- November 2024: CEVA Logistics unveiled the FORPLANET sub-brand to accelerate its path to net-zero emissions by 2050.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Jordan's freight and logistics market as all paid domestic and international movement, storage, and allied handling of merchandise carried by road, rail, air, sea, pipelines, and integrated express networks, together with third-party warehousing and freight forwarding services. According to Mordor Intelligence, values capture gross revenue generated within Jordan's borders from transport, storage, and value-added logistics activities delivered by licensed providers.

Scope exclusion: Private in-house transport fleets that do not charge an explicit fee are outside the market.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed road hauliers, air-cargo handlers at Queen Alia, free-zone warehouse operators in Aqaba, and procurement heads at manufacturing exporters across Amman, Irbid, and Zarqa. These discussions validated rate movements, typical load factors, and service mix shifts, and helped fine-tune our assumptions around cross-border traffic with Saudi Arabia and Iraq.

Desk Research

We begin with structured scans of reputable open data such as the Department of Statistics Jordan trade tables, Ministry of Transport annual bulletins, Aqaba Development Corporation cargo throughput data, and UN COMTRADE shipment records. Macro drivers, GDP by sector, manufacturing output, fuel excise, and e-commerce adoption are benchmarked through World Bank Open Data, IMF Article IV reports, and OECD country notes. Company filings, tender announcements, and reputable press feeds on Dow Jones Factiva complement these public statistics. Paid sources, notably D&B Hoovers for carrier financials and Aviation Week for air-cargo slot metrics, enrich provider-level insights. The sources listed illustrate our secondary foundation; many additional references supported variable checks and narrative refinement.

Market-Sizing & Forecasting

We apply a top-down reconstruction that starts with official freight volume by mode, multiplies it by calibrated average revenue per ton-kilometer, and then layers in warehousing and CEP revenue using penetration-rate-based demand pools. Selective bottom-up roll-ups of leading carriers' turnovers and sampled contract rates cross-check totals. Key variables include truck border crossings, container dwell time at Aqaba, per-capita e-commerce parcels, diesel price trajectory, and planned logistics-park capacity. A multivariate regression linking these drivers to historical revenue underpins the forecast, while scenario analysis tests sensitivity to corridor-rail deployment slippage. Data gaps, especially for informal last-mile players, are bridged through ratio-based imputation anchored to verified peer benchmarks.

Data Validation & Update Cycle

Outputs pass three-layer review: automated outlier flags, senior-analyst variance checks, and lead-author sign-off. We refresh models annually and issue interim updates when policy shifts or large-scale investments materially alter assumptions. Clients receive a final consistency sweep before publication.

Why Mordor's Jordan Freight And Logistics Baseline Earns Trust

Published numbers often diverge because firms pick differing service baskets, base years, and conversion factors. Our disciplined scope setting, refresh cadence, and dual-check modelling make the differences transparent, not puzzling.

Key gap drivers include whether courier revenue is bundled with warehousing, how informal trucking turnover is estimated, and the exchange rate vintage applied at conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.36 billion (2025) | Mordor Intelligence | - |

| USD 2.50 billion (2024) | Regional Consultancy A | Counts landlord warehousing rents and free-zone port fees |

| USD 0.55 billion (2024) | Global Consultancy B | Uses carrier financials only; excludes forwarding margins and CEP revenue |

These contrasts show that when scope is either too broad or too narrow, totals shift significantly. Mordor's balanced middle path, grounded in verifiable trade flows and cross-checked pricing, gives decision-makers a dependable, reproducible baseline.

Key Questions Answered in the Report

What is the current value of the Jordan freight and logistics market?

The market is valued at USD 2.45 billion in 2026 and is projected to rise to USD 2.96 billion by 2031.

Which segment holds the largest Jordan freight and logistics market share?

Freight Transport leads, accounting for 53.55% of overall revenue in 2025.

Which freight transport mode is expected to grow the fastest?

Air freight transport is forecast to register the highest 5.02% CAGR between 2026 and 2031, driven by pharmaceuticals and perishables.

How will the GCC railway affect Jordan’s logistics sector?

The 2,177 km network will create a cost-efficient rail option for 31 million t of freight annually, easing road congestion and lowering shipping costs.

Why is temperature-controlled warehousing a growth area?

Rising pharmaceutical output and perishable exports require GDP-compliant cold rooms; current share of the segment is only 8.12% as of 2025, spurring new builds.

What digital initiatives are improving logistics efficiency in Jordan?

A 960-service government single window, vehicle-tracking mandates, and blockchain-enabled courier chains are cutting border delays and enhancing shipment transparency.

Page last updated on: