Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 15.14 Billion |

| Market Size (2026) | USD 15.35 Billion |

| Market Size (2031) | USD 16.43 Billion |

| Growth Rate (2026 - 2031) | 1.37% CAGR |

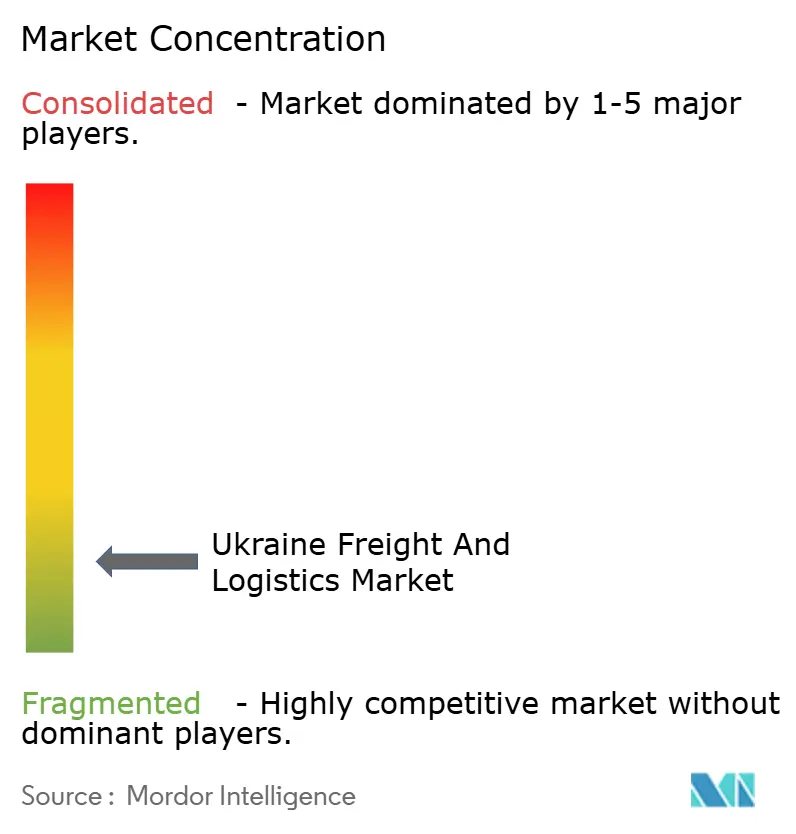

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ukraine Freight And Logistics Market Analysis by Mordor Intelligence

The Ukraine freight and logistics market size is expected to grow from USD 15.14 billion in 2025 to USD 15.35 billion in 2026 and is forecast to reach USD 16.43 billion by 2031 at 1.37% CAGR over 2026-2031. Recovered volumes on rail corridors, the reopening of Black Sea lanes, and streamlined EU border procedures underpin this muted yet steady expansion. Freight flows are progressively shifting westward, driven by permit-free road access to the EU, while reconstruction outlays are lifting domestic haulage and warehousing demand. Stabilized war-risk insurance rates, supported by the Unity facility, continue to ease operating costs for shippers. Meanwhile, the government’s Great Construction program and EU-backed Solidarity Lanes are anchoring long-term investment in multimodal infrastructure.

Key Report Takeaways

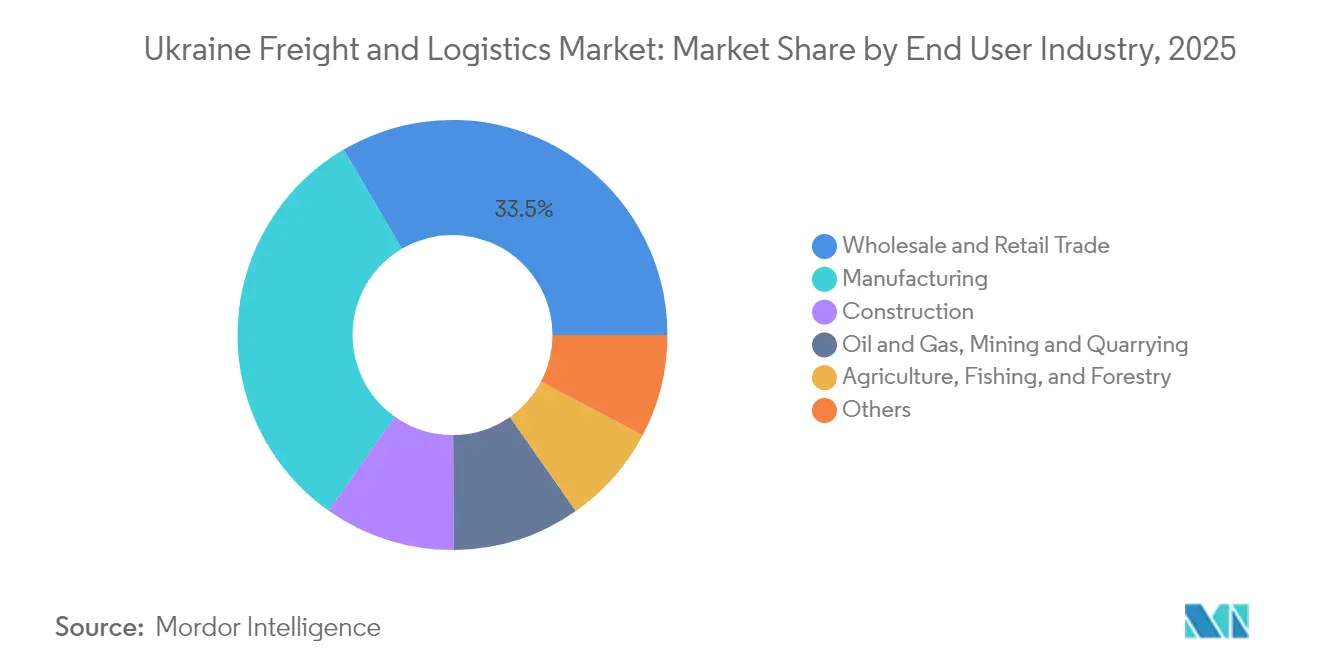

- By end user industry, wholesale and retail trade led with 33.45% of the Ukraine freight and logistics market size in 2025; manufacturing shows the fastest projected growth at 1.56% CAGR between 2026-2031.

- By logistics function, freight transport held 73.78% of the Ukraine freight and logistics market share in 2025, while courier, express, and parcel (CEP) services are projected to grow at a 1.59% CAGR between 2026-2031.

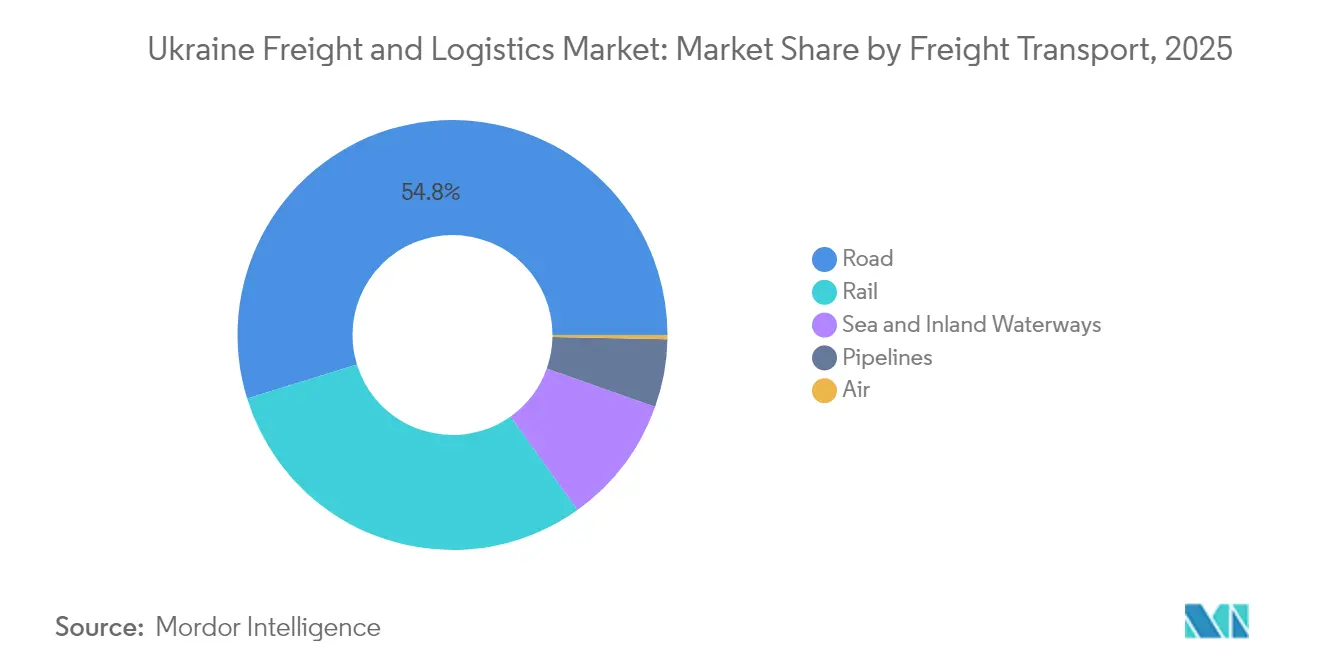

- By freight transport, road freight transport captured 54.78% of revenue share in 2025; sea and inland waterways freight transport are set to expand at a 1.82% CAGR between 2026–2031.

- By CEP destination, domestic routes accounted for 67.72% of revenue share in 2025, yet international services are poised for a 1.66% CAGR between 2026-2031.

- By warehousing and storage, non-temperature controlled facilities dominated with 91.55% revenue share in 2025, while temperature controlled space is set to advance at a 1.31% CAGR between 2026-2031.

- By freight forwarding mode, sea and inland waterways freight forwarding commanded 77.82% of 2025 revenue and are forecast to grow at 1.73% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ukraine Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-Ukraine trade realignment boosting west-bound road freight | +0.4% | Western Ukraine, EU border regions | Medium term (2–4 years) |

| Solidarity Lanes multimodal export corridors accelerating intermodal uptake | +0.3% | EU-Ukraine corridors | Short term (≤ 2 years) |

| Government Great Construction program reviving domestic haulage demand | +0.2% | National | Long term (≥ 4 years) |

| Surge in grain maritime corridor volumes witnessed post-Black Sea Grain Initiative 2.0 | +0.3% | Black Sea region, Danube ports | Medium term (2–4 years) |

| Warehouse space shortage observed in Kyiv and Odesa spawning build-to-suit boom | +0.2% | Kyiv, Odesa metros | Short term (≤ 2 years) |

| EU accession preparation is driving regulatory compliance and infrastructure standardization | +0.2% | National, with priority on EU border corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU-Ukraine Trade Realignment Boosting West-Bound Road Freight

Permit-free bilateral road haulage introduced in 2022 lifted Ukrainian exports to the EU by 42% and imports by 37% within a year. Monthly outbound loads now surpass 300,000 tons, redirecting flows from Black Sea routes to western crossings. Expanded lanes at border posts cut wagon queues that once stretched to 30 days, and Romania’s fast-tracked Moldova Highway is shortening transit to Baltic and Adriatic ports. EU support through 2025 locks this shift into the long-term structure of the Ukraine freight and logistics market.

Solidarity Lanes Multimodal Export Corridors Accelerating Intermodal Uptake

Since May 2022, these corridors have handled 157 million tons of cargo, equal to EUR 180 billion (USD 198.65 billion) in trade value, and now carry 87% of Ukraine’s imports and 52% of its non-agricultural exports. The European Commission’s EUR 2 billion (USD 2.20 billion) infrastructure envelope is unclogging rail, road, and Danube links, while digital platforms give shippers end-to-end visibility[1]European Commission, “Solidarity Lanes: Two Years On,” transport.ec.europa.eu. As the lanes mesh with the TEN-T backbone, they cement Ukraine’s status as a transit bridge and expand the addressable base of the Ukraine freight and logistics market.

Government “Great Construction” Program Reviving Domestic Haulage Demand

The 2025 transport budget allocates USD 7.37 billion to rebuild roads, bridges, and European-gauge lines[2]World Bank Group, “Ukraine Rapid Damage and Needs Assessment,” worldbank.org. Over 2,000 km of highways have already reopened, spurring heavy-bulk moves of cement, steel, and aggregates. A 63,000 m² dry store and 21,000 m² cold store nearing completion in Lviv underline strong private follow-on capital[3]President of Ukraine, “Head of State Visits Construction of Lviv Logistics Hub,” president.gov.ua. Continuous project flow secures a multi-year freight pipeline that stabilizes the Ukraine freight and logistics market.

Surge in Grain Maritime Corridor Volumes Witnessed Post-Black Sea Grain Initiative 2.0

Self-secured sea lanes restored grain exports to nearly 30 million tons a year, attracting liner calls amounting to 25.1 million deadweight tons (DWT) in Q1 2024. Black Sea ports now process 80% of total exports versus 69% in 2022, after operators such as Nibulon upgraded terminals. Re-enabled ocean legs rekindle forwarder confidence and elevate the maritime component of the Ukraine freight and logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ukraine's handling capacity diminishes as war-related destruction targets bridges, depots, and port berths | -0.3% | East and South | Medium term (2–4 years) |

| EU bilateral permit caps throttling cross-border trucking capacity | -0.2% | West | Short term (≤ 2 years) |

| High war-risk insurance premiums inflating freight rates | -0.2% | Black Sea | Short term (≤ 2 years) |

| Persistent driver out, migration to EU labor markets creating shortages | -0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ukraine’s Handling Capacity Diminishes as Destruction Targets Transport Assets

Direct infrastructure losses top USD 176 billion, of which transportation represents USD 78 billion. Strikes have hit 126 rail stations, 500 km of track, and critical berths at Chornomorsk, shrinking daily throughput and forcing costlier detours. Although Ukrainian Railways regularly restores links within weeks, repetitive damage erodes the systemic buffer, limiting upside for the Ukrainian freight and logistics market.

EU Bilateral Permit Caps Throttling Cross-Border Trucking Capacity

Temporary caps on special heavy-haul permits continue to create sporadic shortages at Polish and Slovak gates, stretching dwell times during seasonal surges. While Brussels reviews quota ceilings, forwarders shift excess to rail, pressuring wagon availability and rates. Persistent administrative frictions weigh on the short-term trajectory of the Ukraine freight and logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Wholesale Trade Leads Diversified Demand Base

Wholesale and retail trade held 33.45% of 2025 revenue, reflecting Ukraine’s swelling consumer rebound and restock push. Manufacturing, projected at a 1.56% CAGR (2026-2031), accelerates as EU near-shoring programs trigger equipment imports and parts exports. Agriculture continues to supply high tide volumes, while construction freight remains pronounced until at least 2027. Such a blend cushions market swings and cements a balanced demand canvas for the Ukraine freight and logistics market.

International OEMs co-locating plants around Lviv and Rivne rely on bonded warehouses and just-in-time feeds, raising the share of contractual logistics revenues. The resulting sophistication nudges local operators toward quality certifications, ISO 9001, GDP pharma protocols, that match EU peer standards and unlock higher fee tiers.

By Logistics Function: Freight Transport Anchors Market Foundation

Freight transport accounted for 73.78% of the Ukraine freight and logistics market share in 2025, reflecting the country’s heavy exposure to bulk agricultural and reconstruction cargo. The Ukraine freight and logistics market size for Freight Transport is projected to edge up in line with the overall 1.37% CAGR (2026-2031) as restored corridors lift export tonnage. CEP services, though smaller, ride surging e-commerce volumes and expanded international routes, showing the strongest growth at 1.59% CAGR (2026-2031). Freight forwarding and warehousing, and storage continue to formalize, spurred by EU customs alignment and digital visibility mandates. Private operators such as Nova Poshta doubled 2024 capital budgets, while Ukrainian Railways’ variable-gauge bogies cut two-hour border swaps to minutes, sharpening intermodal competitiveness.

Second, the segment is expanding its value chain depth. Shippers are increasingly outsourcing load planning, customs brokerage, and last-mile delivery, pushing local firms to add integrated offerings. Foreign carriers enter through joint ventures, seeking partner knowledge on security protocols and domestic road permits. Over the outlook, diversified service menus position Ukrainian providers to match EU 3PL standards, embedding them deeper into continental supply chains.

By Courier, Express, and Parcel (CEP): International Services Accelerate Cross-Border Integration

Domestic parcels made up 67.72% of 2025 CEP revenue, driven by reconstruction supplies and everyday consumer deliveries. International shipments, however, show a higher 1.66% CAGR between 2026-2031 as EU duty suspensions and marketplace links escalate B2C exports. Nova Poshta’s Khmelnytsky terminal sorts 8,500 parcels an hour and feeds a 200-country partner network, illustrating scale economies in outbound flows. Lower de-minimis thresholds in the EU push Ukrainian sellers to use professional brokers, deepening parcel logistics sophistication within the Ukraine freight and logistics market.

The e-commerce surge ripples through to value-added services like cash-on-delivery handling, returns processing, and customs prep. Providers bundle these extras to defend their margins against price-centric rivals. Over time, international CEP margins are set to narrow, yet volumes should keep the segment growing faster than the broader Ukraine freight and logistics industry.

By Warehousing and Storage: Cold Chain Infrastructure Drives Premium Growth

Non-temperature controlled still occupy 91.55% of segment revenue in 2025, but market vacancy sits below 3% in Kyiv and Odesa. Temperature-controlled capacity is rising at a 1.31% CAGR (2026-2031), fed by stringent EU food safety rules and the rebound of pharmaceutical imports. Developers now add backup generators and IoT sensors by default, guarding perishables from power disruptions. The Ukraine freight and logistics market size for cold storage gains a further lift from multinational grocers that require HACCP-compliant distribution hubs.

Rental spreads remain wide: chilled space in Kyiv commands USD 9 per m² a month versus USD 5 per m² for dry. Landlords thus prefer mixed-use parks, layering higher-yield cold rooms atop bulk racking. This premium niche will keep drawing inward FDI, especially as agribusiness exporters chase value retention through processed goods.

By Freight Transport: Road Networks Drive Modal Integration

Road freight transport held 54.78% of revenue in 2025, underpinned by flexibility and abundant 3.2-ton pickups that bridge fractured rail links. Sea and Inland Waterways, helped by reopened Black Sea lanes, are forecast to climb at 1.82% CAGR (2026-2031), the fastest across modes. The Ukraine freight and logistics market size for maritime legs is buoyed by reduced war-risk premiums following the Unity cover and steady grain off-take commitments. Rail remains vital for bulk ores but suffers from strike damage; European-gauge rollouts should recapture part of the lost share beyond 2026.

Cost convergence is evident; 2024 road spot prices averaged USD 0.110 per ton-km, only three times rail’s USD 0.029 per ton-km, yet faster amid dynamic lane closures. Logistics planners increasingly select hybrid rail-road runs—loaders dispatch north-south by wagon and finish the final 120 km by truck, to balance cost and reliability. Such blending underscores a future in which the Ukraine freight and logistics market optimizes mode selection rather than relying on single-channel dominance.

By Freight Forwarding: Maritime Corridors Dominate International Trade

Sea and inland waterways freight forwarding represented 77.82% of forwarding revenue in 2025 and are on course for a 1.73% CAGR between 2026-2031. The Ukraine freight and logistics market benefits from the Unity insurance program that slashes premium add-ons on Black Sea sailings. Forwarders package through bills that link Danube barges, deep-sea feeders, and west-bound rail shuttles. Air forwarding lags given airspace limits, though niche charters continue for high-tech spares.

Market leaders invest in blockchain-backed document flows, cutting dwell time at Constanța by 18 hours per consignment. Customs e-seal pilots on Poland lanes further compress cycle times, signaling a tech-centred arms race that will re-rank forwarders based on digital enablement rather than asset count.

Geography Analysis

Kyiv remains the single-largest logistics node, orchestrating domestic replenishment and serving as the nerve center for intermodal dispatch. Its ring road depots feed most population clusters within 24 hours, anchoring national distribution efficiency. Western provinces, Lviv, Volyn, Zakarpattia, have gained weight as entry doors to the EU; road and rail links funnel 60% of outbound tonnage through these crossings in 2025. The West’s relative security draws new warehouses, redundant data centers, and customer service hubs, insulating supply chains from frontline risk.

The Odesa region safeguards maritime capacity. Port output in 2024 rose 77%, handling 133,000 TEU and restoring 80% of 2021 throughput despite sporadic missile alerts. Danube delta upgrades, financed under the Solidarity Lanes plan, broaden draft limits and enable barges to bypass mined coastal lanes. Eastern oblasts, though damaged, witness gradual rail reopenings that revive metallurgical shipments toward EU steel mills, yet capacity there remains below half of 2021 levels.

Regional policy favors multimodal nodes that knit road, rail, and river. Rivne’s planned tri-modal park will slot 12 daily broad-gauge trains into EU truck fleets, slicing transit to Polish ports by 30 hours. Such hubs accelerate the geographic pivot of the Ukraine freight and logistics market toward European-facing corridors and away from legacy east-west pipelines.

Regulatory Landscape

Ukraine’s freight and logistics regulation is being reshaped by EU integration and wartime continuity measures. A key anchor is the EU-Ukraine road transport liberalization (permit-free regime) introduced in 2022 and extended through March 31, 2027, which continues to shape cross-border trucking flows and compliance expectations at western crossings.

Customs and border administration is moving toward EU-aligned authorizations and digital controls. The State Customs Service completed a mandatory transition to a new authorization regime for customs brokerage and temporary storage warehousing, with legacy permits expiring on April 19, 2026. In May 2026, the Cabinet of Ministers approved a draft new Customs Code aligned with EU customs legislation for submission to the Verkhovna Rada, reinforcing a shift toward electronic document exchange, risk-based controls, and expanded post-clearance audit practices for compliant operators.

Value Chain Analysis

Ukraine’s freight and logistics value chain is anchored by shippers in agriculture, manufacturing, construction materials, and wholesale and retail trade, moving through forwarders and 3PLs into multimodal corridors that increasingly prioritize western land borders and Danube/Black Sea gateways. Core operating links include domestic road distribution, rail trunk haul (particularly for bulk and export flows), port and river terminals for international legs, and warehousing that supports consolidation, customs procedures, and last-mile delivery. Air cargo remains constrained, which amplifies the role of road-rail-sea combinations and border checkpoint performance.

On the service-provider layer, integrated operators and distributors such as UVK (warehousing), TEUS (rail/sea/road integration), AFINA Group (FMCG distribution), and Ekol Logistics (cross-border services) support linehaul, cross-dock, and contract logistics, while agribusiness exporters such as Nibulon remain central to Danube-oriented export logistics. Investment and capacity formation is increasingly routed through state-led PPP and concession mechanisms for critical nodes: in June 2026, the Ministry for Development of Communities and Territories presented a pipeline of transport PPP projects at URC 2026 (about USD 5 billion) and advanced concession work for Chornomorsk terminals, indicating that terminal operators, financiers, and EPC partners are becoming more structurally embedded in the market’s upstream capacity supply.

Competitive Landscape

Competition remains fragmented; however, the top five operators together hold a significant revenue share. Domestic champions such as Nova Poshta, Ukrposhta, and Ukrainian Railways compete alongside multinationals Raben, Maersk, and DB Schenker. The fight has moved from price to resilience; customers prize guaranteed lift capacity, live-tracking, and war-risk mitigation. Leaders responded by embedding satellite-linked fleet monitors, redundant border depots, and pooled marine insurance.

Technology is a prime differentiator. Ukrainian Railways introduced automatic gauge-changing wheelsets that remove border bogie swaps, saving eight hours per train and raising competitiveness on Kyiv–Katowice lanes[4]Ukrainian Railways, “Variable Gauge Wheelset Deployment Update,” railwaygazette.com. Nova Poshta’s robotics-driven Khmelnytsky terminal cuts parcel touchpoints to two, halving sort errors. Strategic tie-ups abound: Raben partnered with a local 3PL for cross-dock control at Lviv, while Maersk opened a block-train service from Odesa to Prague, bundling customs under a single invoice.

Foreign entrants prefer asset-light models, joint ventures, and agency tie-ups to hedge operational risk. Access to Unity-backed insurance presents a key moat; providers able to secure cover win volumes otherwise priced off the water. Over 2025–2030, further consolidation is likely as operators seek scale to amortize compliance costs and fund digital capex, steadily professionalizing the Ukraine freight and logistics market.

Ukraine Freight And Logistics Industry Leaders

Ukrainian Railways (Ukrzaliznytsia)

NOVA Group (Nova Post LLC)

Ukrposhta

DSV A/S (incl. DB Schenker)

A.P. Moller – Maersk

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunity formation is concentrated around EU corridor integration, border capacity, and port-linked concessions, where public frameworks are already defined. In June 2026, the Government presented a portfolio of 15 priority transport PPP projects at URC 2026 (about USD 5 billion), including port and corridor assets, which expands the near-term addressable pipeline for developers, terminal operators, and asset-light logistics providers that can structure long-tenor operating models. The concession concept for the Chornomorsk ferry terminal was also presented with a 35-year term and at least USD 40 million investment target, creating a clear entry route for Ro-Ro, intermodal, and project-cargo logistics ecosystems.

A second opportunity set is centered on border and compliance enablement, where programs and platforms are being institutionalized. The DREAM platform is being used as a mandatory digital backbone for public investment project management, opening whitespace for contractors and logistics firms to integrate reporting, traceability, and execution controls into infrastructure and corridor operations. On the hard-infrastructure side, modernization of the M-09 Ternopil-Lviv-Rava-Ruska road corridor with EBRD support, alongside a June 2026 memorandum for a EUR 120 million border infrastructure development project (Border Crossing Points, Tranche A) for 2027-2029 implementation, signals continued demand for cross-dock capacity, bonded warehousing, yard management, and EU-facing linehaul services in western Ukraine.

Recent Industry Developments

- July 2026: Ukrzaliznytsia reported a 17.8% increase in grain cargo transportation in the first half of 2026 versus the same period of 2025. The higher rail grain throughput supports corridor reliability for exporters and increases the focus on wagon availability, border transshipment capacity, and intermodal planning across western crossings.

- June 2026: Nova Post announced plans to open around 300 new parcel acceptance and delivery points in Poland during 2026, materially expanding its cross-border network footprint. The move strengthens Ukraine-EU parcel connectivity and increases competitive pressure on international CEP lanes, particularly for returns handling, customs-prepared shipments, and fulfillment-linked delivery options.

- May 2026: The Cabinet of Ministers of Ukraine approved the draft new Customs Code of Ukraine aligned with EU customs legislation for submission to the Verkhovna Rada. This advances a multi-year shift toward EU-compatible procedures and IT-driven control, pushing forwarders, brokers, and warehouse operators to invest in electronic workflows, risk-based compliance, and post-clearance audit readiness.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Ukraine freight and logistics market is counted as the revenues earned from transporting and handling goods within Ukraine across freight modes and logistics services. This includes forwarding, warehousing, and contract logistics that directly support cargo movement.

Scope exclusions: We exclude passenger transport, construction spending for logistics infrastructure, and purely retail postal services.

Segmentation Overview

- End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

- Logistics Function

- Courier, Express, and Parcel (CEP)

- By Destination Type

- Domestic

- International

- By Destination Type

- Freight Forwarding

- By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

- By Mode of Transport

- Freight Transport

- By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

- By Mode of Transport

- Warehousing and Storage

- By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

- By Temperature Control

- Other Services

- Courier, Express, and Parcel (CEP)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to understand how Ukraine cargo flows behave and to set guardrails for the model before interviews were run. We referenced public sources such as the State Statistics Service of Ukraine (transport output and freight turnover), Ukrzaliznytsia releases for rail freight signals, Ukraine Sea Ports Authority port throughput updates, State Customs Service trade statistics, and Eurostat cross border transport indicators that capture rerouted volumes.

To translate these indicators into market value, we also reviewed company filings and investor presentations of logistics operators and infrastructure owners, association publications, and reputable press coverage of corridor shifts and capacity constraints. For cost and pricing context, selected paid subscriptions were used for logistics supply chain and freight rate benchmarks, plus shipment-level trade checks. Patent databases were used lightly to track logistics digitalization signals. This list is not exhaustive, and additional sources were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of cargo is served by organized logistics providers, how pricing is reset under volatile fuel and insurance conditions, and which routes are actually used for cross border movements. We spoke with a mix of carriers, freight forwarders, warehouse operators, customs related service firms, and large shippers across agriculture, metals, retail, and industrial goods. Coverage was balanced across Ukraine focused operators and cross border decision makers in nearby EU corridors.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 16% | APAC: 39% |

| Mid tier: 50% | Functional/Unit leaders: 30% | EMEA: 34% |

| Smaller Players: 21% | Managers: 54% | Americas: 27% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where national freight activity and trade flow indicators are reconstructed into a payable demand pool for logistics services in Ukraine. Inputs typically include freight ton-km trends, port and inland terminal throughput, cross border export and import mix, rail versus road share shifts, and price markers such as fuel-linked trucking tariffs and storage rates, which are normalized to current USD.

After the demand pool is formed, we corroborate results with selective bottom-up approximations, such as sampled carrier and 3PL revenue benchmarks, lane-based rate checks, and volume times average price logic for warehousing and forwarding, to confirm the order of magnitude. Where company coverage is incomplete, we handle gaps through penetration assumptions by mode and service type, and we stress test those assumptions through interviews. Forecasts are built using scenario analysis, with assumptions for trade recovery, corridor stability, capacity availability, and cost pass-through to keep the growth path realistic under different operating conditions.

Data Validation & Update Cycle

Model outputs are checked against independent signals so large swings do not pass without explanation. These include transport output indices, customs trade direction changes, and throughput series for ports and rail. If a variance looks unusual, we review the drivers, revisit the assumptions, and trigger targeted follow ups with interviewees to confirm whether a structural change occurred or a temporary shock is being overread.

Before sign-off, a second analyst reviews calculations, unit conversions, and currency timing to reduce avoidable errors. Reports are refreshed annually, and interim updates are made when material events shift routes, capacity, or costs. Before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Ukraine Freight and Logistics Market Size Versus Other Published Estimates

Published market sizes for Ukraine freight and logistics often differ because each publisher chooses a different service perimeter, pricing basis, and treatment of war-time volatility in volumes and exchange rates. Some estimates align more closely with a transport-output proxy, while others try to capture the full paid logistics ecosystem, which naturally changes the headline value.

A common gap driver is whether courier and parcel, contract warehousing, and forwarding fees are counted within the same market or kept separate, and whether revenues are counted only when earned inside Ukraine or also when billed by offshore entities for the same move. Some sources also lean on fixed pre-war mode shares or long-run averages, which can miss the impact of corridor rerouting and insurance and fuel surcharges, and their refresh cadence can lag fast changes. In this study, the broader external scope often includes adjacent postal and infrastructure spend, while Mordor Intelligence limits the value to service revenues tied to cargo movement, including forwarding, CEP, and third-party warehousing, with current-USD normalization and re-checks against throughput signals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.14 B (2025) | |

| Regional Consultancy A | USD 13.90 B (2026) | Often modeled from freight transport output only, which can undercount forwarding margins and contract warehousing revenues, and it may apply conservative pricing resets that lag fuel and risk surcharges. |

| Trade Journal B | USD 18.20 B (2025) | Tends to use a broader definition that folds in adjacent postal or infrastructure-related spending, and it can overstate value when corridor disruption premiums are not separated from true logistics service revenues. |

The spread across the table mainly comes from what is treated as paid logistics service revenue versus adjacent spending, and how quickly pricing and route changes are reflected. By anchoring the estimate to observable freight activity signals and then sanity-checking with operator economics, the final number remains traceable to clear steps and practical inputs that can be revisited each refresh.

Key Questions Answered in the Report

What is the current value of the Ukraine freight and logistics market?

The Ukraine freight and logistics market is valued at USD 15.35 billion in 2026 and is projected to reach USD 16.43 billion by 2031.

Which logistics function holds the largest market share?

Freight Transport dominates with 73.78% of the Ukraine freight and logistics market share in 2025.

Why are Sea and Inland Waterways the fastest-growing freight transport mode?

Reopened Black Sea lanes, reduced war-risk premiums, and rising grain exports support a 1.82% CAGR (2026-2031) for maritime and inland waterway transport.

How is EU integration affecting Ukrainian logistics?

Permit-free road access, Solidarity Lanes funding, and EU standard-gauge rail upgrades are realigning freight westward and embedding Ukraine into European supply chains.

What segments show the strongest future growth?

Courier, Express, and Parcel (CEP) services and temperature-controlled warehousing lead segment growth, driven by e-commerce expansion and stricter EU food-safety requirements.

How are war-risk insurance premiums influencing freight costs?

The Unity facility now covers all non-military cargo, trimming premiums and allowing Ukrainian shippers to price ocean and road moves closer to pre-war levels.

Page last updated on: