Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

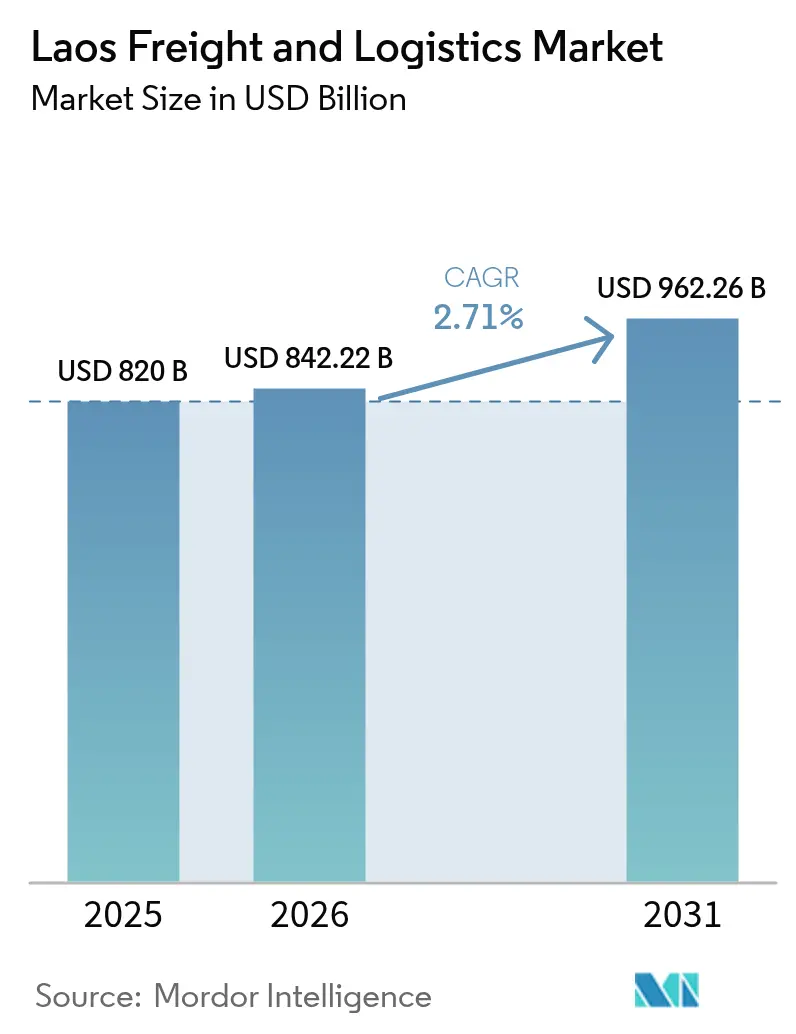

| Base Year Market Size (2025) | USD 820 Billion |

| Market Size (2026) | USD 842.22 Billion |

| Market Size (2031) | USD 962.26 Billion |

| Growth Rate (2026 - 2031) | 2.71% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Laos Freight And Logistics Market Analysis by Mordor Intelligence

Laos freight and logistics market size in 2026 is estimated at USD 842.22 million, growing from 2025 value of USD 820 million with 2031 projections showing USD 962.26 million, growing at 2.71% CAGR over 2026-2031. This steady trajectory reflects rising cross-border trade volumes, the modal shift created by the China-Laos Railway, and policy measures that streamline customs processing. Infrastructure upgrades funded under China’s Belt and Road Initiative, digitized customs declarations that already handled 15,000 filings in H1 2025, and e-commerce parcelization are lowering transit times and enlarging addressable demand. Intensifying interest from third-country manufacturers pursuing Thailand-plus-one diversification is stimulating premium air-freight demand and accelerating special-economic-zone warehousing. Competitive dynamics remain fragmented as global integrators acquire scale while domestic operators leverage regulatory familiarity and last-mile reach to defend niche positions.

Key Report Takeaways

- By logistics function, freight transport captured 70.20% of the Laos freight and logistics market share in 2025; courier, express, and parcel (CEP) is expected to grow at the fastest 4.06% CAGR between 2026-2031.

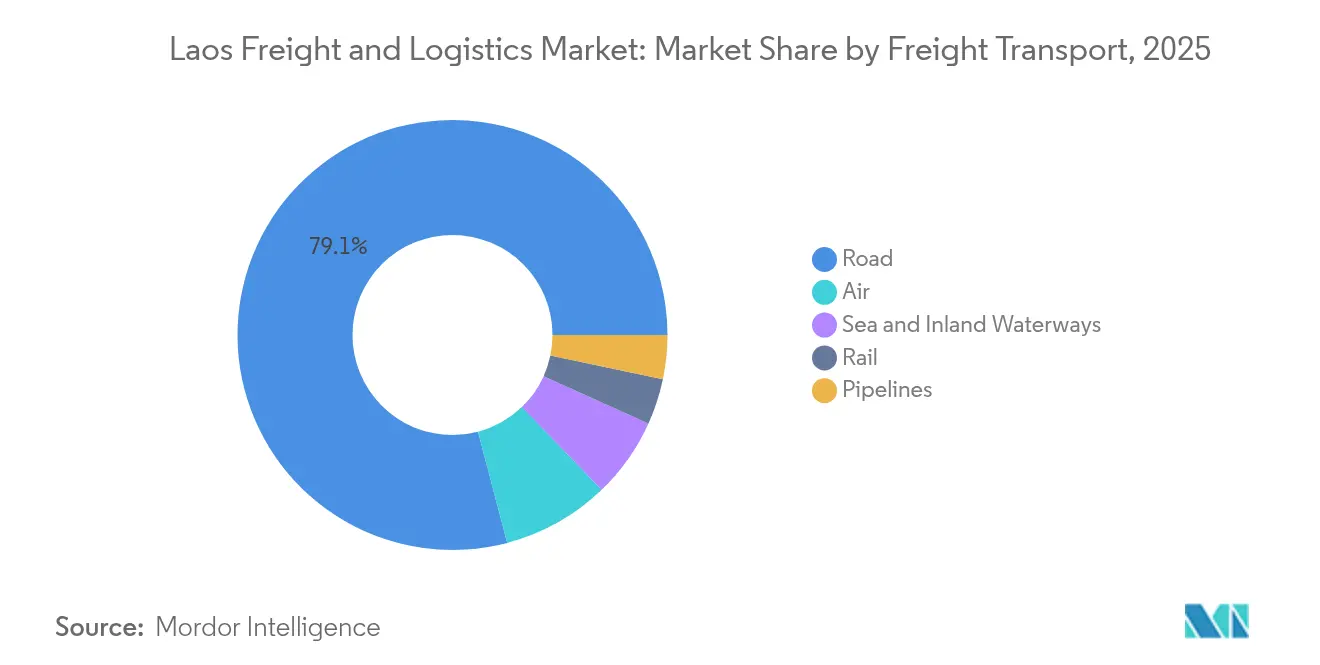

- By freight transport, road freight transport held 79.10% revenue share in 2025, while air freight transport is projected to expand at a 4.02% CAGR between 2026-2031.

- By end user industry, wholesale and retail trade commanded 34.10% of the Laos freight and logistics market size in 2025; manufacturing is expected to advance at a 2.83% CAGR between 2026-2031.

- By CEP type, domestic parcels represented a 66.70% revenue share in 2025, whereas international parcels are forecast to grow at a 4.01% CAGR between 2026-2031.

- By warehousing and storage, non-temperature-controlled facilities accounted for 91.40% revenue share in 2025, and temperature-controlled capacity is expected to rise at a 2.58% CAGR between 2026-2031.

- By freight forwarding, air freight forwarding accounted for 36.50% revenue share in 2025 and is expected to lead growth with a 3.88% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Laos Freight And Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Belt and Road rail freight is driving growth spillover into Laos | +0.8% | National, with concentrated gains in Vientiane, Luang Prabang, Boten | Medium term (2-4 years) |

| Rapid growth in E-commerce is boosting cross-border parcel volumes | +0.6% | National, early adoption in urban centers and border zones | Short term (≤ 2 years) |

| Cold chain incentives in the Savan-Seno SEZ are drawing new logistics investment | +0.3% | Southern provinces, spillover to the Vietnam corridor | Long term (≥ 4 years) |

| Digital freight platforms are expanding along the China-Laos railway | +0.5% | National rail network, extending to Thailand connections | Medium term (2-4 years) |

| ASEAN-wide cabotage relaxation is strengthening barge trade on the Mekong | +0.2% | Mekong basin provinces, cross-border waterway routes | Long term (≥ 4 years) |

| The Laos-Vietnam expressway is spurring development of a major petrochemical corridor | +0.4% | Eastern provinces, Vientiane to the Vietnam border | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Belt-And-Road Rail-Freight Spill-Over to Laos

Rail freight volumes on the 422 km China-Laos Railway climbed 326% in 2024 relative to pre-opening baselines, lifting container throughput to 1.29 million t and compressing Kunming-Vientiane transit times from 2–3 days to 10–12 hours. Faster services enable Laos to intermediate a slice of the USD 975 billion China-ASEAN merchandise flow and generate new transshipment income[1]"ASEAN-China Trade Statistics 2024," ASEAN Secretariat, asean.org. Automated border clearance at Boten and Vientiane has cut paperwork cycles from 4–6 hours to under 90 minutes. Follow-on feeder-road upgrades and inland-dry-port projects are extending the network’s reach into agricultural catchments and urban retail hubs, bolstering door-to-door reliability. These dynamics collectively contribute to the forecast CAGR by driving modal shift from road to rail.

Rapid E-Commerce Parcellation of Cross-Border Trade

Cross-border platforms processed USD 904.61 million in gross merchandise value during 2025, more than doubling volumes handled two years earlier as shoppers demand faster delivery windows and tighter tracking. Domestic CEP already holds 67.15% of parcel flows, yet the international leg is expected to scale at 4.28% CAGR as customs digitization eases micro-shipment clearance. Supply-chain actors are investing in automated sortation centers and blockchain-enabled provenance tools that satisfy premium buyers of specialty foods. Digital freight marketplaces such as 360TRUCK fill backhauls and compress empty-run ratios by up to 18%. As parcel density rises, last-mile operators in Vientiane and Savannakhet gain pricing power and widen service portfolios to include returns management and same-day delivery.

Savan-Seno SEZ Cold-Chain Incentives

Tax holidays, duty exemptions, and subsidized land leases inside Savan-Seno have catalyzed the installation of multi-temperature warehouses and cross-docking platforms, a prerequisite for scaling agro-processing and pharmaceutical assembly. Cold-store throughput is projected to rise 17% annually through 2028, chipping in to boost the national CAGR[2]"Study on Capacity Development for Economic Zones in Border Areas," Asian Development Bank, adb.org. Access to the East-West Economic Corridor ensures time-critical exports reach Vietnamese seaports within 10 hours, mitigating landlocked cost disadvantages. Incentives stipulate compliance with Hazard Analysis and Critical Control Point (HACCP) protocols, elevating food-safety standards and widening market access to Japanese and European buyers. The scheme is also attracting third-party logistics specialists that bundle bonded storage, value-added labeling, and quick-freeze services into integrated contracts.

China-Laos Railway Digital-Freight Platforms

The railway’s end-to-end digital stack mixes IoT sensors, GPS devices, and electronic data interchange with seaports at Laem Chabang and Vung Ang. Real-time visibility supports dynamic slot-pricing that has lifted load factors in the first full year of operation. Predictive-maintenance algorithms cut unplanned wagon downtime by 23%, enabling 99.2% on-time dispatch and anchoring just-in-time manufacturing flows. Exporters gain automated bill-of-lading issuance and pre-arrival customs filings, shrinking document lead times from two days to under four hours. These productivity accelerants jointly expand national cargo-handling capacity without commensurate capital outlay, delivering a lift to CAGR forecasts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High unofficial border fees remain a significant barrier for businesses | -0.4% | All border crossings, especially Thailand and Vietnam corridors | Short term (≤ 2 years) |

| Limited bonded warehouse capacity is restricting efficient supply chain operations | -0.3% | National, concentrated in Vientiane and Savannakhet | Medium term (2-4 years) |

| Extreme seasonal swings in Mekong river levels impact reliable waterway transport | -0.2% | Mekong basin provinces | Long term (≥ 4 years) |

| A shortage of truck drivers, partly due to outward migration, is straining fleet capacity | -0.3% | National, most acute on rural and border routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Unofficial Border Fees

Informal payments ranging from USD 50–200 per truck inflate logistics costs by 8–12% versus official tariffs and erode Laos’s route competitiveness[3]"Border Management Modernization," World Bank Group, worldbank.org. SMEs lack leverage to negotiate with local agents and are disproportionately affected, stalling inclusive trade participation. A national single-window and e-payment portal aims to curtail cash transactions, but uptake remains uneven across remote crossings. Persistent opacity risks re-routing of regional flows through Thailand or Vietnam despite longer physical distances, dragging the forecast CAGR down until systemic fixes materialize.

Limited Bonded-Warehouse Capacity

With only 50,000 m² of bonded space, mostly non-temperature-controlled, importers often must clear goods immediately, tying up working capital and constraining just-in-time models[4]"Greater Mekong Subregion: Capacity Development for Economic Zones in Border Areas," Asian Development Bank, adb.org. Pharmaceutical and chemical consignments face additional hurdles because compliant cold rooms are scarce, forcing rerouting through Bangkok or Ho Chi Minh City. Land-acquisition complexities and multi-agency permits slow expansion, suppressing value-added logistics revenue and subtracting from potential CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Drives Future Growth

Manufacturing’s 2.83% CAGR (2026-2031) cements its status as the fastest-expanding customer set within the Laos freight and logistics market, even though wholesale and retail trade retains the largest 34.10% slice of 2025 revenue. Duty-exempt raw-material imports, coupled with preferential cross-border clearance on railway corridors, make Laos an appealing Thailand-plus-one location. Food-processing plants and light-electronics assemblers lean heavily on temperature-controlled inbound flows and outbound premium-air services. Segment growth is also buoyed by agro-industrial clusters in Savannakhet that capitalize on proximity to Vietnamese ports. The Laos freight and logistics market size attributable to manufacturing-linked cargo is deepening modal diversification as firms add bonded warehousing and value-added packaging.

Meanwhile, agriculture, fishing, and forestry supply stable base volumes that hinge on Mekong barge reliability and cold-chain stewardship. Construction remains cyclical, tracking highway and Petro-Chemical corridor outlays. Oil, gas, mining, and quarrying contribute niche yet high-margin flows, aided by pipeline tie-ins and specialized rail wagons. Service-sector logistics, grouped under “Others,” grow modestly but introduce higher handling requirements for medical and high-tech equipment. As manufacturing scales, integrated service contracts that blend freight, customs brokerage, and sub-assembly emerge, elevating 3PL penetration across the Laos freight and logistics market.

By Logistics Function: CEP Accelerates Amid Transport Dominance

Freight transport generated 70.20% of the Laos freight and logistics market share in 2025, illustrating that cargo movement remains the central pillar of the Laos freight and logistics market. Road freight transport fleets facilitate flexible door-to-door delivery, while rail captures heavier loads and cross-border containers. CEP’s 4.06% CAGR (2026-2031) stems from consumer e-commerce and SME online exports, prompting investment in automated sorters and address-verification software. Warehousing and storage, although smaller, underpins rising contract-logistics uptake, with non-temperature space accounting for 91.40% of capacity. Freight forwarding orchestrates multimodal journeys and secures space on constrained international flights, and its air freight forwarding sub-segment is expected to ride a 3.88% CAGR (2026-2031). Altogether, these complementary functions fuel service bundling that increases stickiness and average-revenue-per-shipment.

CEP operators pioneer data-driven route optimization, allowing 2-day delivery between Vientiane and Bangkok, and same-day service for intra-city consignments. Digital freight platforms aggregate spot demand, trimming empty backhauls, and reducing carbon footprints. As Shipper-of-Record responsibilities deepen, forwarders broaden customs-compliance suites, while warehouse managers add kitting, light assembly, and reverse-logistics services. This functional diversification positions the Laos freight and logistics market to capture value beyond pure transportation, expanding contractual tenures and margin opportunities.

By Courier, Express, and Parcel: International Growth Outpaces Domestic Base

Domestic parcels dominated at 66.70% revenue share in 2025, thanks to urban consumption and rising smartphone penetration, which fuels online shopping. Yet international CEPs’ 4.01% CAGR (2026-2031) reflects streamlined customs APIs and railway-enabled 48-hour transit to Kunming. Cross-border sellers use fulfillment centers in Savannakhet to pool inventory destined for Thailand, Vietnam, and Cambodia. Shipping APIs automatically generate region-specific duty invoices, enhancing buyer transparency. The Laos freight and logistics market size for international CEP is growing, narrowing the domestic-international gap.

Rural delivery remains costly due to scattered settlements and road quality, spurring trials of drone drop-points and communal parcel lockers. International express providers partner with local firms for last-mile execution while focusing on cross-border line-haul reliability. Enhanced visibility, supported by QR-code scanning and bilingual status updates, boosts customer satisfaction. The connection between domestic density and international volume helps operators balance network loads and sustain investment in route-planning technologies.

By Warehousing and Storage: Temperature Control Expansion Accelerates

Non-temperature controlled space underpinned 91.40% of 2025 revenue, but temperature controlled warehousing enjoys a 2.58% CAGR (2026-2031) as pharmaceuticals, dairy, and frozen seafood volumes rise. SEZ incentives slash import duties on chillers, while power-backup mandates ensure 99.5% uptime. The Laos freight and logistics market size for cold storage is forecast to grow by 2031, narrowing the infrastructure deficit. IoT probes feed real-time temperature and humidity to dashboards, enabling proactive maintenance and regulatory compliance.

Investors increasingly prefer modular, expandable cold-store designs to match demand without overshooting capacity. Training focuses on hazard prevention, ammonia handling, and energy-efficiency best practices. Bundling cold warehousing with specialized trucking and customs brokerage yields integrated cold-chain corridors that improve shelf life and reduce product loss. As service quality rises, exporters gain access to higher-margin markets with stringent cold-chain requirements.

By Freight Transport: Road freight transport Dominance Faces Modal Competition

Road freight transport commanded a 79.10% share in 2025 but confronts eroding dominance as rail and air carve niche superiority on cost or speed metrics. Air freight transport’s 4.02% CAGR (2026-2031) springs from manufacturer demand for just-in-time parts, and the modal shift boosts Laos' freight and logistics market efficiency. Rail’s uplift is founded on predictable schedules and integrated customs, while inland waterways retain importance for cost-sensitive heavy cargo despite seasonal constraints. Pipelines handle petroleum products, freeing road capacity during peak drilling campaigns.

Hauliers upgrade to Euro IV engines and install telematics for fuel optimization. Road-rail transfer yards in Boten and Thanaleng shorten long-haul trucking distances by 220 km on north-south corridors. Electronic tolling and weight-in-motion sensors reduce checkpoint congestion and limit overloading. Although road’s relative share decays, total tonnage hauled will still increase owing to overall market growth, maintaining asset-utilization and driver-demand profiles.

By Freight Forwarding: Air Freight Forwarding Leads Growth and Share

Air freight forwarding controlled a 36.50% revenue share in 2025, underpinned by Wattay International Airport upgrades that doubled cargo-terminal throughput capacity. Time-critical electronics, fashion samples, and perishables underpin the expected 3.88% CAGR (2026-2031), while sea-inland waterways forwarding caters to bulk commodities at lower price points. Others, including project cargo and multimodal coordination, provide high-skill revenue streams with lower volume but higher yield. The Laos freight and logistics industry increasingly depends on forwarders to aggregate small-lot exports into unit-load devices and negotiate slot allocations during peak seasons.

Digital booking portals integrate schedule, tariff, and document management, cutting quote-to-book cycles from 24 hours to under 30 minutes. Forwarders diversify into supply-chain finance by advancing freight charges against confirmed letters of credit, easing cash flow for SMEs. Training programs aligned with IATA Dangerous Goods Regulations expand the talent pool and lift service compliance. Airside cold-chain corridors link temperature-controlled warehouses directly to apron stands, shortening tarmac exposure and supporting pharmaceutical volume growth.

Geography Analysis

Northern provinces leverage the China-Laos Railway to tap Kunming’s manufacturing supply chains and distribute Chinese consumer goods southward within 24 hours, lowering historic overland lead times by nearly three-quarters. Vientiane anchors national logistics with its concentration of warehouses, CEP sortation centers, and regulatory agencies, enabling seamless multimodal hand-offs. The Laos freight and logistics market size tied to the central corridor is projected to rise at a 3.04% CAGR as distribution networks densify.

Southern hubs such as Savannakhet and Champasak ride the East-West Economic Corridor to connect Thai and Vietnamese ports, offering exporters two ocean gateways within a day’s trucking. The Savan-Seno SEZ multiplies its cold-chain footprint, attracting seafood processors that shorten door-to-quay intervals for high-value frozen shrimp. Eastern provinces anticipate expressway connectivity to Vung Ang Port, which will slash transit times for containers headed to North American and European routes by bypassing congested regional hubs.

Mekong-side provinces capitalize on relaxed cabotage to ferry rice, cement, and timber on low-cost barges when water levels permit, with multimodal yards facilitating road transfers during dry spells. Border checkpoints with Thailand and Vietnam remain sensitive to unofficial fees, but digitized manifests are reducing face-to-face interactions and harmonizing duty assessments. Collectively, geographic diversification mitigates single-route disruption risks, broadens modal choice, and supports balanced development across Laos freight and logistics market sub-regions.

Regulatory Landscape

Freight and logistics oversight in Laos primarily involves the Ministry of Public Works and Transport (MPWT), working with the Ministry of Industry and Commerce for trade procedures and the Ministry of Finance for customs and duties. A key 2024 anchor is the Decree on Dry Port No. 298/GOL (June 5, 2024), which sets principles for managing, monitoring, and inspecting dry port operations and positions dry ports to integrate with regional transport networks.

Cross-border execution is being tightened through digitization and compliance controls. An MPWT instruction issued in April 2024 mandated the Cross-Border Transport Management (CBTM) system for freight, container, and document tracking, including guarantee requirements for foreign transport vehicles. Truck load compliance is anchored by MPWT Decision No. 9393/MPWT (April 13, 2023), which governs maximum truck weights and requires inspection at weight stations. In 2026, the National Trade and Transport Facilitation Committee (NTTFC) continued the operational rollout of its Trade and Transport Facilitation Roadmap 2025-2030 through dissemination tied to Decision No. 001/NTTFC (January 9, 2026), reinforcing efforts to standardize procedures across corridors and border points.

Value Chain Analysis

The Laos freight and logistics value chain is shaped by shipper demand (wholesale and retail trade, manufacturing, and agriculture), origin consolidation and first-mile trucking, multimodal line-haul (road, rail, air, and inland waterways), and destination-side distribution and CEP. Corridor infrastructure and node performance drive service outcomes: the China-Laos Railway and hubs such as Thanaleng Dry Port act as backbone assets for containerized and cross-border cargo, while road networks remain the dominant connector for door-to-door movements and feeder legs into rail terminals and border checkpoints.

Value capture is concentrated in cross-border forwarding, customs brokerage and documentation, and node-based handling (dry ports, freight stations, and warehouses), with bottlenecks often arising at handoff interfaces. The report highlights pain points including reload requirements between Thanaleng Dry Port and the Vientiane South Freight Station, limited competition in some station services, and inconsistent documentation processes that increase dwell time. On network development, large connectivity projects are expanding the chain upstream and downstream, including the March 2026 concession agreement for the Thakhek to Mu Gia section of the Laos-Vietnam Railway and the April 2026 MOU for feasibility studies on Sections 2 and 3 of the Vientiane-Boten Expressway, alongside ongoing rehabilitation of National Road 2 to strengthen Thailand-Laos-Vietnam corridors. Node-level partnerships linked to Thanaleng Dry Port are also being used to plug gaps in port interfacing, systems, and service design.

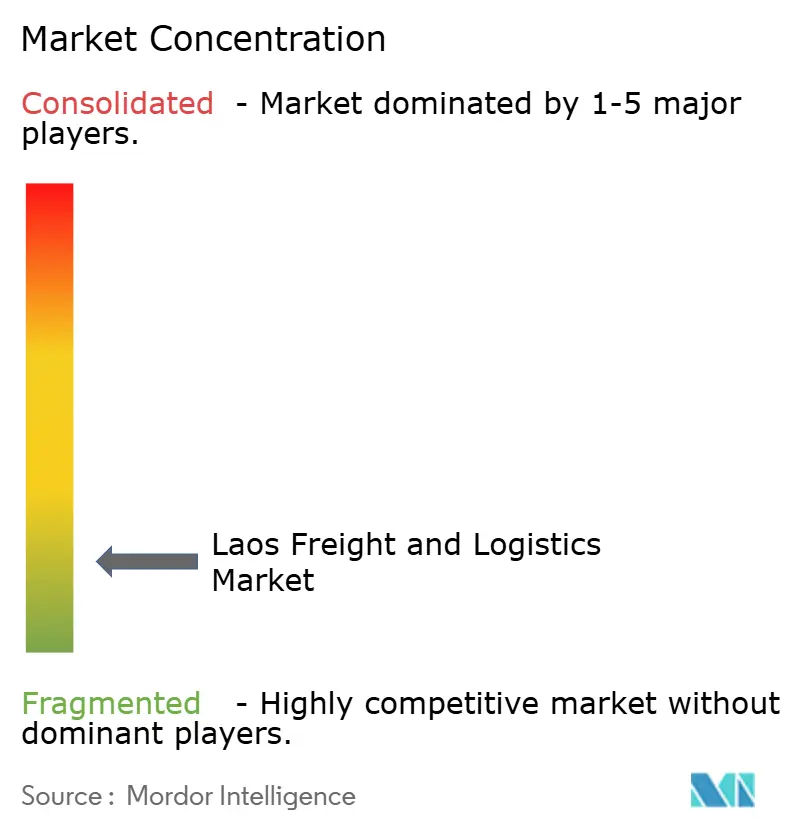

Competitive Landscape

The competitive field is moderately fragmented. Global integrators such as DSV, DHL, and CMA CGM push scale advantages in air-sea forwarding, contract logistics, and digital visibility, while local firms like Geotrans Logistics and Sayfon Logistics retain last-mile resilience and border-procedure expertise. Following DSV’s USD 15.8 billion acquisition of DB Schenker in April 2025, the combined entity commands unparalleled capacity buying power and unified digital freight platforms, raising competitive intensity. DHL’s AI-driven optimization suite trims Laos-regional transit times by 15-20%, setting new benchmarks in express reliability.

DP World’s entry via the Savan Logistics acquisition signals a push into inland-dry-port management, enabling end-to-end visibility from Chinese factories to sea-port quays. CMA CGM’s partnership with Google embeds predictive analytics into scheduling, underscoring a tech-led arms race. Local operators respond by partnering with fintechs to provide cash-on-delivery settlement and micro-insurance for SMEs. Strategic moves focus on warehouse automation, cold-chain expansion, and multimodal connectivity to defend share in the growing Laos freight and logistics market.

Market entrants face barriers in capital-intensive cold-storage and in navigating multilingual regulatory regimes. However, niches exist in hazardous-materials handling, reverse logistics, and outsourced trade-compliance advisory. Cross-border e-commerce and rail-enabled regional consolidation lanes are poised to yield new service blueprints, ensuring an evolving competitive tapestry.

Laos Freight And Logistics Industry Leaders

-

China Merchants Group - cmhk (Including Sinotrans, Ltd.)

-

DHL Group

-

CMA CGM Group (Including CEVA Logistics)

-

DSV A/S (Including DB Schenker)

-

Linfox Pty, Ltd. (Owned by Fox Group)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity set is consolidating around trade facilitation execution and corridor-linked, multimodal services that reduce border friction and improve shipment visibility. The Trade and Transport Facilitation Roadmap 2025-2030, disseminated by the NTTFC in February 2026, supports programs to integrate multimodal transport systems and digitize trade information via the Lao PDR Trade Portal, creating whitespace for forwarders, 3PLs, and technology providers to operationalize e-documentation, tracking, and compliant cross-border processes. With customs digitization already handling 15,000 filings in H1 2025 (as referenced in the report context), operators that combine brokerage, payments, and data exchange into a single workflow have room to win SME and e-commerce volumes.

Infrastructure-linked capacity additions and new nodes broaden addressable demand beyond pure trucking. In June 2026, MPWT commenced the Boten Station expansion and renovation project on the Lao section of the China-Laos Railway, aligning with the observed rise in rail-enabled cross-border cargo and supporting higher-frequency rail logistics products. The March 2026 concession for the Thakhek-Mu Gia rail link toward Vietnam and ongoing National Road 2 rehabilitation under the Southeast Asia Regional Economic Corridor and Connectivity project expand land-bridge options to Vietnamese seaports and Thai gateways. This supports opportunities in inland container depots, bonded warehousing (notably constrained at around 50,000 m2 in current capacity per the report context), and cold-chain compliant storage in incentive-providing zones such as Savan-Seno. Service providers that can package rail-road transfers, temperature-controlled handling, and corridor-specific compliance, including CBTM adoption, have a practical path to capture higher-value contracts tied to manufacturing and time-sensitive trade.

Recent Industry Developments

- June 2026: The Ministry of Public Works and Transport (MPWT) officially commenced the expansion and renovation project at Boten Station on the Lao section of the China-Laos Railway. Added node capacity at a primary border rail gateway supports higher throughput and strengthens rail-linked multimodal offerings across north-south corridors.

- April 2025: DSV completed its acquisition of DB Schenker for USD 15.8 billion, creating a larger global forwarding and contract-logistics platform with deeper scale in Southeast Asia lanes serving Laos. The deal increased competitive pressure on local forwarders and raised the benchmark for integrated digital visibility and capacity procurement.

- August 2024: DHL Group rolled out an AI-powered supply-chain optimization platform across Southeast Asia, including Laos-linked express and forwarding operations. Faster planning and network optimization improved service reliability on cross-border routes, reinforcing CEP differentiation as e-commerce parcel volumes increased.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the Laos freight and logistics market is defined as the value of services used to move, store, and handle goods within Laos and across its borders. This includes transport, forwarding, warehousing, and parcel logistics.

Scope exclusions: Passenger transport, pure tourism mobility, and standalone construction of transport infrastructure are excluded from this market sizing.

Segmentation Overview

-

End User Industry

- Agriculture, Fishing, and Forestry

- Construction

- Manufacturing

- Oil and Gas, Mining and Quarrying

- Wholesale and Retail Trade

- Others

-

Logistics Function

-

Courier, Express, and Parcel (CEP)

-

By Destination Type

- Domestic

- International

-

By Destination Type

-

Freight Forwarding

-

By Mode of Transport

- Air

- Sea and Inland Waterways

- Others

-

By Mode of Transport

-

Freight Transport

-

By Mode of Transport

- Air

- Pipelines

- Rail

- Road

- Sea and Inland Waterways

-

By Mode of Transport

-

Warehousing and Storage

-

By Temperature Control

- Non-Temperature Controlled

- Temperature Controlled

-

By Temperature Control

- Other Services

-

Courier, Express, and Parcel (CEP)

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clear demand picture for Laos, since logistics activity is tied to trade, production, and consumption. We rely on public statistics and official references such as Laos customs and trade publications, ASEAN trade and transport releases, the World Bank logistics and trade indicators, IMF macro series for GDP and inflation, and UN Comtrade style trade-flow datasets where they are available by product and partner country.

We also review supporting sources such as transport ministry notes and corridor updates, border and dry port announcements, and airport and rail disclosures when they contain freight-relevant details. Company filings, investor presentations, and credible press coverage are used to understand service mix shifts, price direction, and operational constraints. For added structure, paid subscriptions are used only for items like company financials and intelligence, shipment-level import and export records, and freight rate and logistics supply chain databases, which help tighten assumptions that cannot be fully observed in public series. The sources mentioned here are illustrative only, and we checked many other public and paid references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what desk sources cannot settle cleanly, especially price movement, modal mix, and where cross-border services are booked and recognized. We speak with logistics providers, freight forwarders, warehousing operators, and shippers across main corridors, then we re-check assumptions with trade and industry experts across APAC, EMEA, and the Americas who track regional flows into and out of Laos.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 15% | Managers: 54% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down build that reconstructs the service demand pool from Laos trade and production signals, then allocates it across logistics functions and modes based on validated shares. To keep the totals realistic, bottom-up approximations are used as checks, such as sampled price per ton-km times estimated volumes on key lanes, warehouse space utilization times average storage rates, and selected operator revenue benchmarks where disclosures are available.

The model uses practical inputs that can be reviewed and repeated, including import and export values and mix, corridor and border throughput indicators, road and rail freight activity signals (including the rail corridor effect), fuel and labor cost inflation, and observed pricing changes in forwarding and warehousing contracts. Where data is missing, gaps are handled with proxy indicators like trade value by partner, known seasonality from agriculture shipments, and conservative utilization ranges, which are then challenged through interviews.

For forecasting, we use scenario analysis with a light multivariate regression layer on the main demand drivers, and align assumptions to what experts expect for trade growth, infrastructure usage, and cost pass-through. When a forecast year looks out of line with the activity indicators, we revisit the build and adjust the shares and price paths before finalizing the series.

Data Validation & Update Cycle

Validation is done through triangulation across multiple signals, so the final number does not rely on any single dataset. We compare outputs against independent checks such as trade growth direction, modal capacity additions, and observed price movements, then investigate any large jumps that do not match these signals.

Before sign-off, the model and assumptions go through multi-step analyst review, and follow-up calls are triggered when an estimate sits outside the expected range shared by respondents. Reports are refreshed annually, and interim updates are made when major events occur, such as policy changes at borders, large infrastructure openings, or sharp cost shocks. Right before delivery, a fresh data pass is completed so clients receive the latest updated view.

Mordor Intelligence's Laos Freight and Logistics Market Size Compared With Other Published Estimates

Published market sizes for Laos freight and logistics do not always match, and that is usually because each publisher draws the service scope differently and uses different activity indicators and pricing logic. Even when the country is the same, the base year and the treatment of cross-border services can shift the total by a wide amount.

Some published figures bundle a wider transport and logistics universe and extend the forecast window with faster price and volume assumptions, which can lift the starting value. In the Mordor Intelligence model, totals are limited to the defined logistics functions and modes in Laos and are tied back to trade-linked demand signals for the 2025 base year before the 2026 to 2031 forecast is applied.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.82 B (2025) | |

| Global Publisher A | USD 1.89 B (2026) | Uses a later base reference year and a broader ecosystem definition that explicitly includes items like customs brokerage and 3PL as core scope, and then applies a longer high-growth runway through 2035, which tends to raise the implied starting level. |

| Industry Portal B | USD 17.96 B (2025) | Appears to present a much wider national logistics industry value that likely mixes in adjacent transport and service spending beyond freight logistics, and the sizing logic is not transparent on how cross-border billing, inflation, and currency timing are handled. |

The spread in the table is mainly explained by scope width and base-year choices, followed by how price growth and cross-border services are treated in the build. By keeping the service definition explicit and checking the totals against trade and corridor activity, the final estimate stays traceable to clear variables and can be reproduced with the same steps.

Key Questions Answered in the Report

How big is the Laos freight and logistics market in 2026?

It is valued at USD 842.22 million with a forecast to reach USD 962.26 million by 2031.

Which logistics function generates the most revenue?

Freight transport leads, holding 70.20% of 2025 revenue.

What segment is growing fastest?

Courier, express, and parcel posts an expected 4.06% CAGR between 2026-2031.

How important is the China-Laos Railway?

It cut Kunming-Vientiane freight time to 10–12 hours and lifted rail volumes 326% in 2024, underpinning modal shift.

Where are cold-chain investments concentrated?

The Savan-Seno Special Economic Zone hosts most new temperature-controlled capacity.

Are unofficial border fees still a problem?

Yes, informal charges add 8–12% to cross-border road costs, though digital customs reforms aim to curb them.

Page last updated on: