Automotive Metal Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 113.59 Billion |

| Market Size (2031) | USD 145.32 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

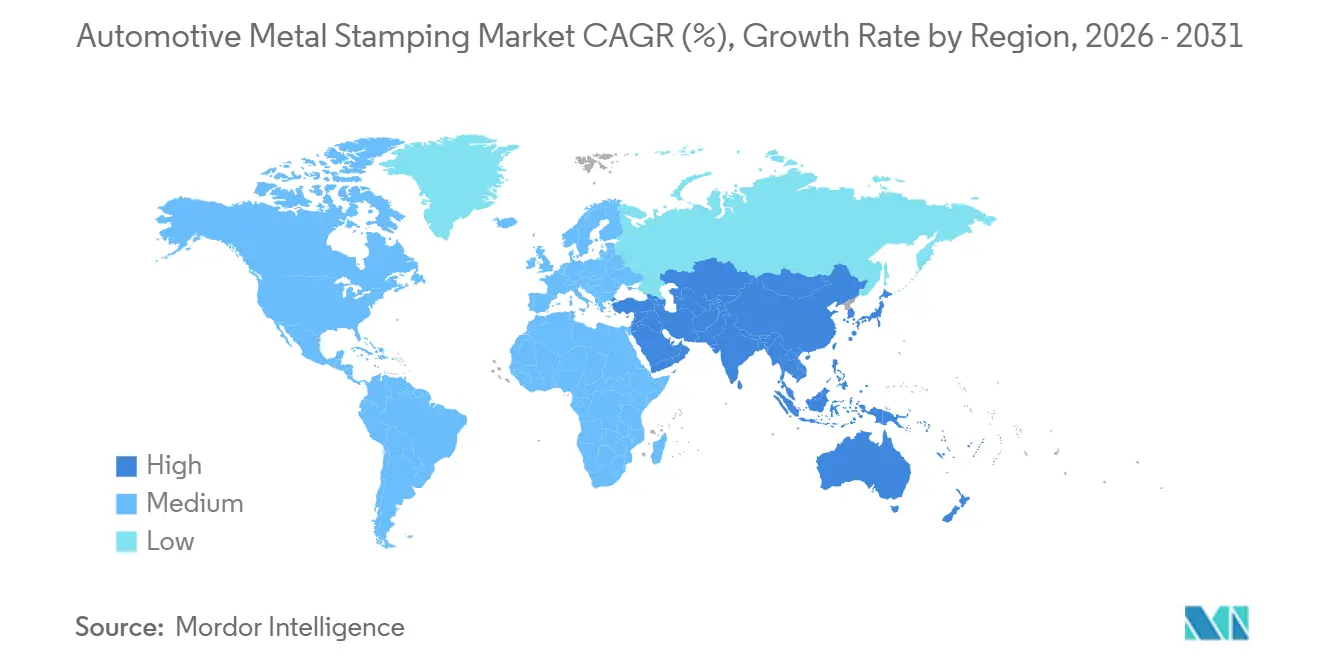

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Metal Stamping Market Analysis by Mordor Intelligence

The automotive metal stamping market size was valued at USD 108.13 billion in 2025 and estimated to grow from USD 113.59 billion in 2026 to reach USD 145.32 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). Rising vehicle electrification, lightweighting mandates, and a steady rebound in global automobile output keep the automotive metal stamping market resilient across passenger and commercial vehicle programs. Stamped parts underpin every modern body structure, battery enclosure, and chassis module, making the technology indispensable as OEMs juggle internal-combustion, hybrid, and battery-electric architectures. Material migration toward aluminum and advanced high-strength steel (AHSS) continues, but steel dominates in cost and supply-chain familiarity, allowing stampers to scale volumes quickly whenever production rebounds. Simultaneously, hot-stamping and servo-press upgrades let suppliers achieve thinner gauges and higher strengths without sacrificing dimensional integrity. Integrated digital twins, inline vision systems, and closed-loop controls are moving from pilot lines to mainstream operations as automakers demand zero-defect delivery and traceability to support over-the-air vehicle software updates.

Key Report Takeaways

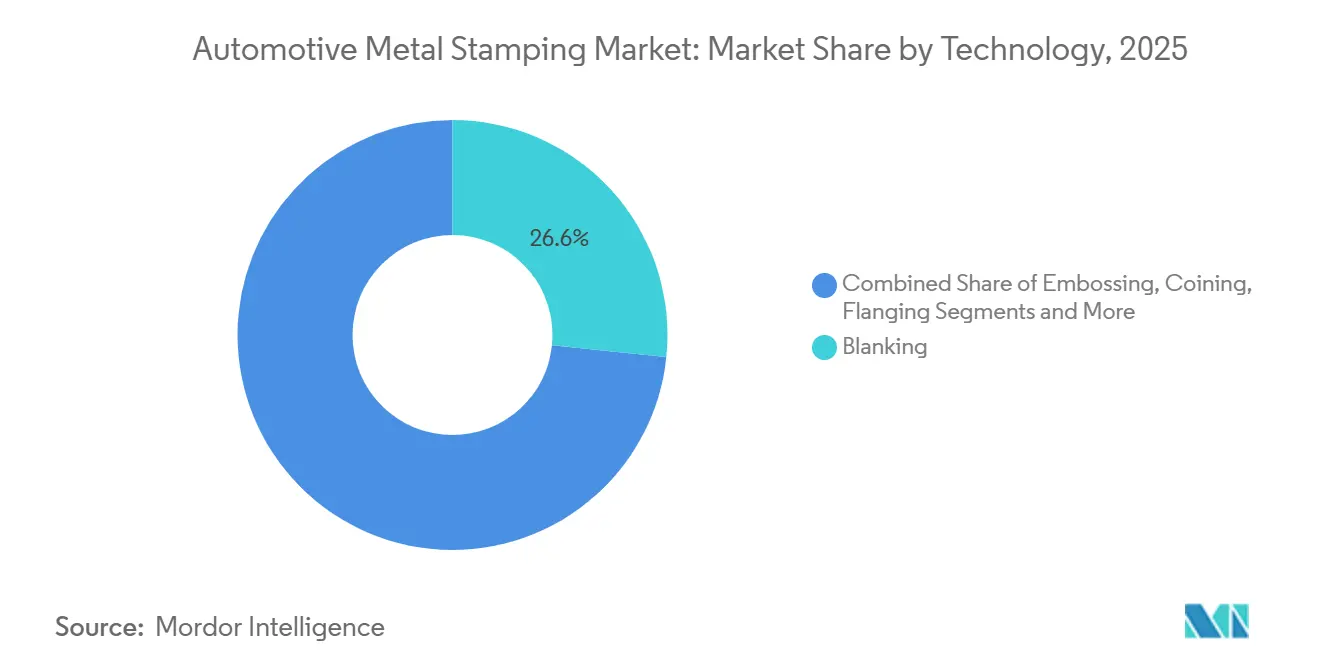

- By technology, blanking accounted for 26.64% of the automotive metal stamping revenue in 2025; embossing is forecast to post the fastest 5.11% CAGR from 2026 to 2031.

- By process, sheet metal forming accounted for 42.62% of the automotive metal stamping revenue in 2025; hot stamping is projected to expand at a 5.17% CAGR through 2031.

- By vehicle type, passenger cars accounted for 62.58% of the automotive metal stamping market share in 2025; light commercial vehicles are forecast to grow at a 5.12% CAGR through 2031.

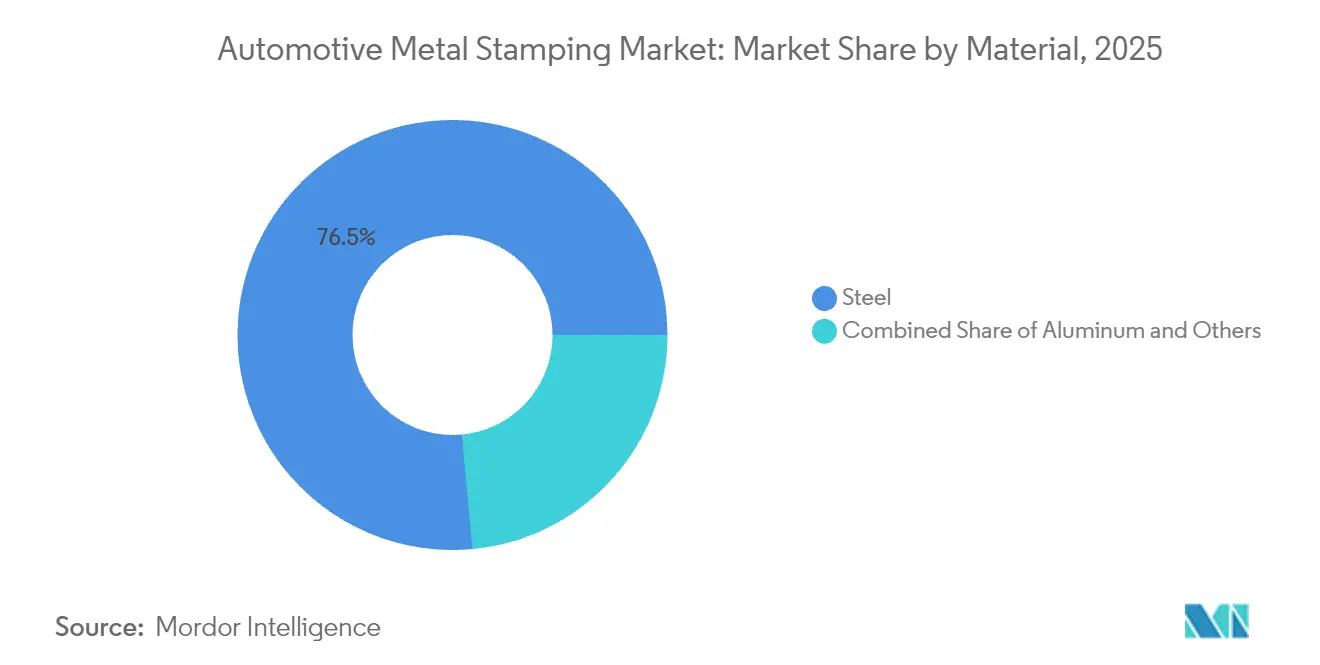

- By material, steel accounted for 76.48% of the automotive metal stamping market share in 2025; aluminum is the fastest-rising material with a 5.18% CAGR forecast to 2031.

- By application, body panels captured 45.96% of the automotive metal stamping market share in 2025; transmission and structural components are positioned for a 5.15% CAGR to 2031.

- By region, Asia-Pacific led the automotive metal stamping market with a 37.89% share in 2025; the region is on track to post the fastest 5.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Metal Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Automobile Production Rebound | +1.2% | Global, with concentration in Asia-Pacific and North America | Medium term (2-4 years) |

| Lightweighting Push For Better Fuel Economy | +1.0% | Global, with early adoption in Europe and North America | Long term (≥ 4 years) |

| Growth Of Hot-Stamped Battery Enclosures | +0.9% | Global, with early concentration in China, Europe, North America | Long term (≥ 4 years) |

| Rapid Recovery Of Chinese and Indian Auto Supply Chains | +0.8% | Asia-Pacific core, spill-over to global supply networks | Short term (≤ 2 years) |

| OEM Adoption Of Mega-Stamp Body Structures | +0.7% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Closed-Loop Digital Twins | +0.6% | Advanced manufacturing regions: Germany, Japan, South Korea, US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Automobile Production Rebound (Post-2025)

Global vehicle assemblies are climbing pre-pandemic peaks, prompting stampers to reopen idled presses and accelerate tool builds. Hyundai Steel’s planned Louisiana complex will deliver numerous automotive steel annually from 2029, cutting carbon intensity by three-fifths via electric-arc routes and positioning regional lines for higher electric-vehicle (EV) output [1]“Hyundai Steel to Build EAF-Based Integrated Plant in Louisiana,” Hyundai Steel, hyundaisteel.com. Capacity expansions illustrate how the automotive metal stamping market aligns capital spending with renewed OEM model launches. Suppliers can juggle AHSS, conventional grades, and aluminum blanks on the same servo press and win incremental orders as platforms diversify. Their flexibility shortens new-model lead times when OEMs request pilot lots for software-defined vehicles in smaller, more frequent batches.

Lightweighting Push for Better Fuel Economy & EV Range

Each kilogram removed from a vehicle lifts fleet fuel economy targets and lengthens EV range, so stampers now trial AHSS families that exceed 1.2 GPa while remaining cold-formable. ArcelorMittal and KIRCHHOFF Automotive validated Fortiform grades that surpass dual-phase steel bending metrics, enabling thinner gauges without extra draw-bead complexity [2]“Fortiform Ultra-High-Strength Steels for Lightweight Applications,” ArcelorMittal, arcelormittal.com. Down-gauged lids, closures, and reinforcement brackets created through such grades keep the automotive metal stamping market on course to supply lighter yet stronger parts. The transition forces shops to buy higher-tonnage servo presses and tailor-welded-blank lasers that marry dissimilar thicknesses inside one panel. Aluminum uptake runs parallel, so tier-ones must balance furnace lines for heat-treatable 6xxx alloys alongside pickling and galvanizing for AHSS sheets.

Rapid Recovery of Chinese & Indian Auto Supply Chains

New stamping lines across Guangzhou and Chennai absorb recovering domestic volumes while feeding export demand from joint-venture OEMs. SMS group’s second hot-dip galvanizing line for Angang Guangzhou Automotive Steel, due online in 2025 at 400,000 t/y, improves surface quality needed for Class-A exterior panels [3]“SMS to Supply Second HDG Line to Angang Guangzhou,” SMS group, sms-group.com. Local suppliers that now meet Japanese and European surface requirements secure long-term global sourcing contracts, anchoring the automotive metal stamping market in the Asia-Pacific. Multinationals hedge geopolitical risk by pairing Chinese partners with alternative Indian or ASEAN plants, deepening the regional pool of qualified stampers.

OEM Adoption of Mega-Stamp Body Structures

Mega-stamp cells compress 10-to-15 small pressings into a single deep draw, removing weld flanges and seam-sealers. BMW’s 2024 press shop in South Carolina houses servo presses rated for 18 strokes per minute and 10,000 panels per day, letting the automaker in-source large outer body sides while protecting proprietary geometries. Tier-ones that can fund 50,000 kN presses become strategic partners as other OEMs replicate the approach. Therefore, the automotive metal stamping market pivots toward fewer but larger part numbers, shifting revenue toward die design consultancy, in-plant line integration, and predictive maintenance services paid on uptime guarantees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Steel & Aluminum Prices | -0.8% | Global, with particular impact on cost-sensitive regions | Short term (≤ 2 years) |

| Shortage Of Skilled Tool-And-Die Makers | -0.6% | Advanced manufacturing regions: North America, Europe, Japan | Medium term (2-4 years) |

| High Cap-Ex | -0.4% | Global, with concentration in emerging markets | Long term (≥ 4 years) |

| Regional Metal Supply Disruptions | -0.3% | Supply-dependent regions: Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel & Aluminum Prices

Raw-material swings can erode thin margins because metal outlays exceed three-fifths of stamping costs. Tariff hikes on aluminum billet—US proposals indicate rates climbing exponentially—would ripple across blank suppliers and push tier-ones to renegotiate annual price clauses. Larger players hedge on commodity exchanges or lock multi-year offtake with mills, cushioning volatility. Smaller shops in the automotive metal stamping market face working-capital constraints, prompting joint procurement pools or consortia to gain leverage.

Shortage of Skilled Tool-and-Die Makers

An aging workforce and declining apprenticeship enrollment leave high-precision die sets without caretakers. Every unplanned die crash delays line start-ups, risking OEM penalties. Tier-ones, therefore, invest in simulation-driven try-outs, 5-axis machining centers with automated offset checks, and remote AR support so one master toolmaker can advise multiple sites. Automation of die spotting safeguards uptime, yet cannot fully replace tacit knowledge, keeping this restraint active through the decade.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Blanking Dominates Traditional Operations

Blanking captured 26.64% of the automotive metal stamping market share in 2025, underscoring its integral role in cutting sheet stock to net-shape blanks before downstream forming. This share illustrates how the automotive metal stamping market size still relies on high-speed mechanical presses for flat-pattern preparation. Continuous coil lines with inline surface inspection uphold the dimensional accuracy needed for outer panels. Embossing, although smaller, is registering the fastest 5.11% CAGR as design studios request textures that remove secondary decorative steps.

OEM requests for NVH damping ribs and stiffening beads lift embossing line orders. High-tonnage presses with programmable slide motions create deep patterns without thinning the base metal, meeting crashworthiness standards. As structures evolve toward fewer parts, embossing raises local stiffness, allowing gauge reduction. Consequently, capital outlays in servo-driven presses enable suppliers to toggle between blanking, coining, and light embossing, expanding service menus while retaining core blanking volumes. This approach keeps the automotive metal stamping market diversified but resilient.

By Process: Sheet-Metal Forming Leads Market Evolution

Sheet-metal forming accounted for 42.62% of the automotive metal stamping market share in 2025, underscoring that traditional progressive dies still dominate the market for high-volume inner panels and sub-assemblies. Automated coil feeds and quick-die-change carts maximize uptime, letting suppliers meet compressed model cycles. Hot-stamping trails in revenue but shows the strongest 5.17% CAGR, driven by EV crash-rail applications that require martensitic strengths near 1.5 GPa.

New furnaces with multi-zone quench control help prevent hydrogen embrittlement, and robotic vacuum transfer helps limit scale buildup. Tier-ones offering conventional and hot-stamping win platform bundles from OEM purchasing teams looking to rationalize supplier counts. Progressive-die and transfer-die systems remain essential for brackets and reinforcement plates. Still, servo-press retrofits lift, forming limits on AHSS sheets and illustrating the incremental technology migration sustaining the automotive metal stamping market.

By Vehicle Type: Passenger Cars Drive Volume Growth

Passenger cars generated 62.58% of the automotive metal stamping market share in 2025, reflecting global light-vehicle dominance and the breadth of stamped parts per unit—from roof bows to battery trays. Premium sedans and SUVs integrate mixed-material designs, blending aluminum doors with AHSS pillars, multiplying die set complexity yet locking in larger purchase orders. Light commercial vehicles (LCVs) are gaining steam at a 5.12% CAGR, propelled by e-commerce vans that require flat floors and underbody protection for skateboard EV platforms.

Tier-ones retool existing transfer presses to accommodate longer LCV side panels, leveraging shared tooling standards across fleet customers. Medium- and heavy-duty trucks remain a niche yet profitable segment, demanding thicker gauges and deeper draws for cab structures. Their lower annual volumes yield stable but limited additions to the automotive metal stamping market.

By Material: Steel Maintains Dominance Despite Aluminum Growth

Steel retained 76.48% of the automotive metal stamping market share in 2025 as galvannealed and AHSS grades balance cost, dent resistance, and weldability. Third-generation AHSS reaches 1.2 GPa tensile strength with elongation above 15%, letting designers shift weight out of sills, cross-members, and side-impact beams without abandoning existing spot-weld parameter windows. Aluminum is expanding at a 5.18% CAGR as EV OEMs prioritize range extension—doors, hoods, and closures migrate to 6xxx and 5xxx series sheets.

Press shops answer with lubricated blank feeds, dual-tension straighteners, and soft-touch grippers to avoid mar defects. Multimaterial adeptness thus defines competitive strength in the automotive metal stamping market, compelling even traditional steel houses to add dedicated aluminum bays or partner with coil coaters for pretreated stock.

By Application: Body Panels Lead Diverse Component Portfolio

Body panels accounted for 45.96% of the automotive metal stamping market share in 2025 because every passenger vehicle requires large-area exterior skins that drive stamping tonnage. Class-A surfaces necessitate ultra-clean press environments, automated part handlers, and precise die maintenance, embedding switching costs that favor incumbent suppliers. Transmission and structural components are on a 5.15% CAGR track, fueled by e-axle housings and cross-members with integrated cooling galleries.

EV propulsion packs add new brackets, shields, and tunnel sections to hold battery modules, widening the parts list addressed by stampers. Exhaust and chassis components stay relevant in internal combustion programs. Still, their share will ebb over time, making battery-pack and underbody shielding growth vital to the future revenue mix in the automotive metal stamping market.

Geography Analysis

Asia-Pacific commanded 37.89% of the automotive metal stamping market size in 2025 and is growing at a robust CAGR of 5.13% through 2031, aided by China’s restart of assembly lines and India’s policy-backed localization drives. Clusters around Shanghai, Guangzhou, Pune, and Chennai attract servo-press installations, enabling the production of AHSS roof rails and hot-stamped side sills for domestic EV models. Government incentives for new-energy vehicles ensure sustained tool-shop backlogs through the decade-end, bolstering the region's automotive metal stamping market presence.

North America maintains technology leadership through investments in smart-factory upgrades and near-shoring by Korean and Japanese steel majors. Hyundai Steel’s Louisiana plant will supply coil stock for southern assembly corridors, shortening logistics and lowering embodied carbon in stamped parts. U.S. and Mexican tier-ones adopt cloud-MES platforms to synchronize press uptime with OEM production sequencing, capturing penalty-avoidance bonuses while elevating service levels within the automotive metal stamping market.

Europe sustains an innovation edge despite high labor costs. Projects like thyssenkrupp Materials Processing Europe’s Stuttgart upgrade link IoT sensors to AI-driven process control, slashing scrap and raising predictive maintenance accuracy. Lightweighting directives under EU fleet targets channel R&D toward multi-material joining, reinforcing supplier know-how. South America, the Middle East, and Africa remain smaller contributors. Still, rising CKD assembly hubs usher in greenfield presses, particularly for pickup trucks and compact SUVs, setting the stage for future gains.

Competitive Landscape

Global tier-one players dominate the automotive metal stamping market, boasting a multi-continental presence. However, regional specialists continue to thrive, driven by constraints such as the just-in-time freight radius and the need for localized die maintenance. Companies like Magna International, Gestamp Automoción, and Shiloh Industries are clinching global platform awards by seamlessly integrating coil processing, pressing, and welding. Their strategy of bundling hot-stamped battery enclosures with traditional inner panels resonates with OEM purchasing teams, who are keen on reducing their supplier counts.

Mid-tier regional players differentiate through close engineering support and quick-response die repairs that international giants cannot match across all their plants. Several are piloting digital twin quality loops that guarantee 100 ppm defect rates—an achievement that opens doors to premium-brand programs. Disruptors exploit automation and advanced analytics; for instance, start-ups deploying multi-camera inline vision paired with cloud analytics secure zero-defect contracts for battery-tray stampings serving European luxury OEMs.

M&A activity remains selective: Standex’s February 2025 purchase of McStarlite adds aerospace-grade cold-draw capacity. Architect Equity’s acquisition of Gibbs Die Casting diversifies aluminum drivetrain castings, feeding stamped sub-assembly contracts. High press-line valuations and customer proximity requirements limit large-scale consolidation, so strategic partnerships around mega-stamp tooling and AI-driven maintenance emerge as preferred routes to capability expansion.

Automotive Metal Stamping Industry Leaders

Magna International Inc.

Shiloh Industries Inc.

Gestamp Automoción

Martinrea International

JBM Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Steel committed USD 5.8 billion to an electric-arc-furnace complex in Louisiana, aimed at producing 2.7 million t of automotive plates annually from 2029.

- March 2025: Techint Engineering & Construction won a USD 255 million contract to expand Vinton Steel’s Texas mill to 400,000 t/y using Tenova’s energy-efficient process.

- February 2025: Standex International acquired McStarlite Co. for USD 56.5 million, adding cold deep-draw expertise to its engineered products portfolio.

- February 2025: Architect Equity bought Gibbs Die Casting Corporation, enhancing precision aluminum capabilities for multi-energy powertrains.

Global Automotive Metal Stamping Market Report Scope

Automotive metal stamping is the manufacturing process of converting flat metal sheets into specific shapes. This process uses a stamping press and a range of metal-forming techniques, such as blanking, embossing, coining, flanging, bending, and others, to transform metal sheets into the desired shapes.

The Automotive Metal Stamping market is segmented by Technology, Process, Vehicle Type, and Geography. By Technology, the market is segmented into Blanking, Embossing, Coining, Flanging, Bending, and Other Technologies. By Process, the market is segmented into Roll Forming, Hot Stamping, Sheet Metal Forming, Metal Fabrication, and Other Processes. By Vehicle Type, the market is segmented into Passenger Cars and Commercial Vehicles. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Rest of the World. The report offers the market size in value (USD) and forecasts for all the above segments.

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Deep Drawing |

| Others |

| Roll Forming |

| Hot Stamping |

| Sheet-Metal Forming |

| Progressive-Die Stamping |

| Transfer-Die Stamping |

| Metal Fabrication |

| Others |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Steel |

| Aluminum |

| Others |

| Body Panels |

| Transmission and Structural Components |

| Exhaust Components |

| Chassis and Suspension Parts |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Technology | Blanking | |

| Embossing | ||

| Coining | ||

| Flanging | ||

| Bending | ||

| Deep Drawing | ||

| Others | ||

| By Process | Roll Forming | |

| Hot Stamping | ||

| Sheet-Metal Forming | ||

| Progressive-Die Stamping | ||

| Transfer-Die Stamping | ||

| Metal Fabrication | ||

| Others | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Material | Steel | |

| Aluminum | ||

| Others | ||

| By Application | Body Panels | |

| Transmission and Structural Components | ||

| Exhaust Components | ||

| Chassis and Suspension Parts | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the value of the automotive metal stamping market?

The Automotive Metal Stamping Market was valued at USD 108.13 billion in 2025 and estimated to grow from USD 113.59 billion in 2026 to reach USD 145.32 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031).

Which region leads to the demand for stamped automotive parts?

Asia-Pacific commands 37.89% revenue due to large-scale vehicle production in China and India alongside fast-growing EV programs.

Which stamping process is growing the fastest?

Hot-stamping is expected to post a 5.17% CAGR through 2031 as ultra-high-strength steel battery enclosures and safety components proliferate.

Why is the use of aluminum rising in automotive stamping?

Lightweighting goals for fuel economy and EV range push OEMs toward 6xxx and 5xxx series aluminum panels, driving a 5.18% CAGR in aluminum stamping revenue.

How are suppliers improving stamping quality?

Plants deploy digital twins and inline optical systems to predict defects in real time, reducing scrap by up to 40% and increasing on-time delivery.

What limits consolidation in the stamping sector?

High press-line capital needs plus OEM mandates for geographic proximity compel many producers to remain regional, yielding a moderate market-concentration score of 5.

Page last updated on: