US Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

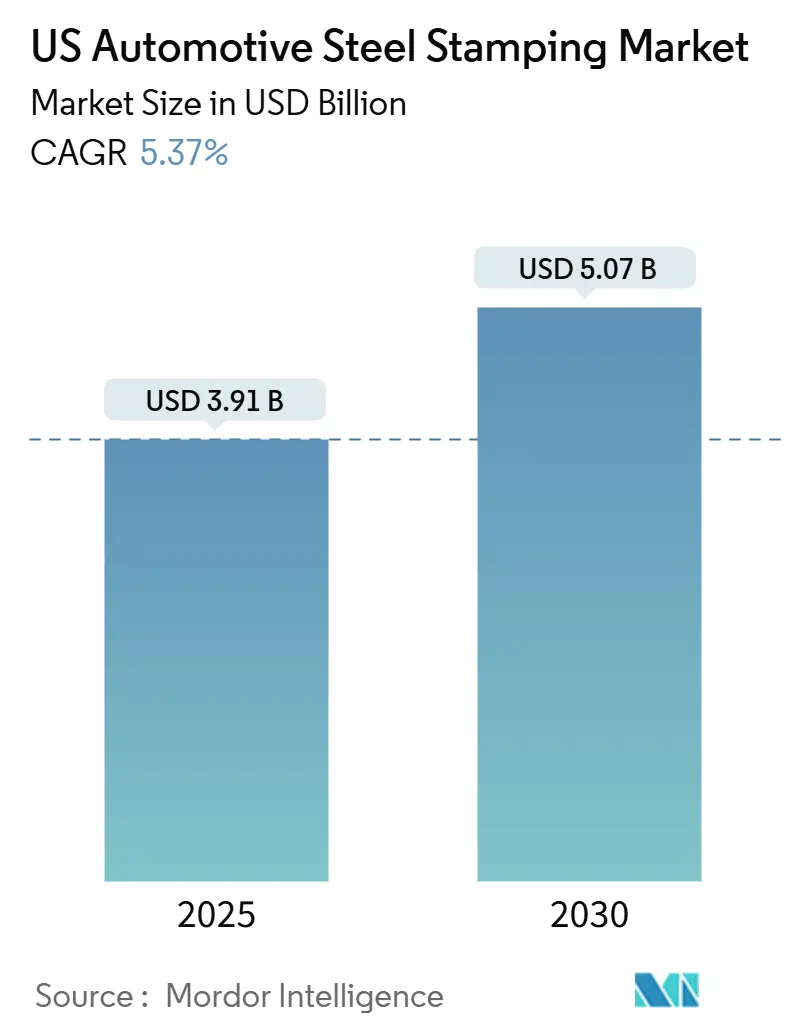

| Market Size (2025) | USD 3.91 Billion |

| Market Size (2030) | USD 5.07 Billion |

| Growth Rate (2025 - 2030) | 5.37% CAGR |

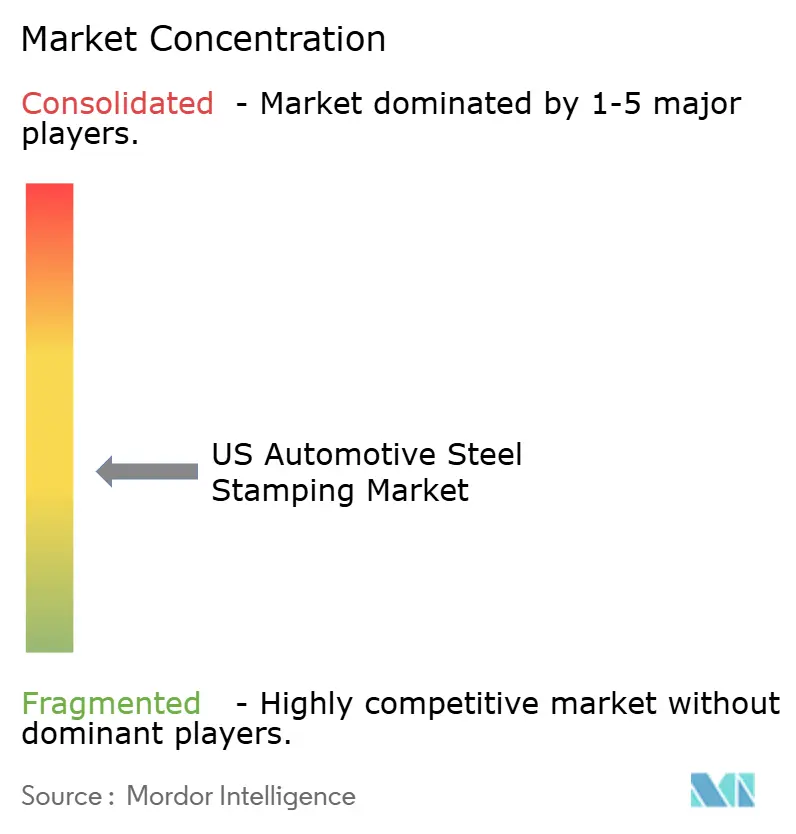

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Automotive Steel Stamping Market Analysis by Mordor Intelligence

The US Automotive Steel Stamping Market size is estimated at USD 3.91 billion in 2025, and is expected to reach USD 5.07 billion by 2030, at a CAGR of 5.37% during the forecast period (2025-2030). The positive outlook is tied to stricter Corporate Average Fuel Economy rules that push automakers toward advanced high-strength steels, growing demand for domestic content under supply-chain localization programs, and steady rebounds in vehicle production volumes. Hot stamping commands more than two-fifths of current revenue because it supports complex geometries for crash-critical parts. At the same time, blanking remains the most widely used technology and is an essential first step for nearly all parts. Suppliers with servo-press capacity, numerical simulation know-how, and proximity to new Southern assembly plants are well positioned to capture incremental orders. Steel’s favorable cost-to-weight ratio versus aluminum preserves its relevance even as Tesla and other firms experiment with gigacasting, and this cost edge is expected to sustain mainstream demand across both internal-combustion and battery-electric vehicle lines.

Key Report Takeaways

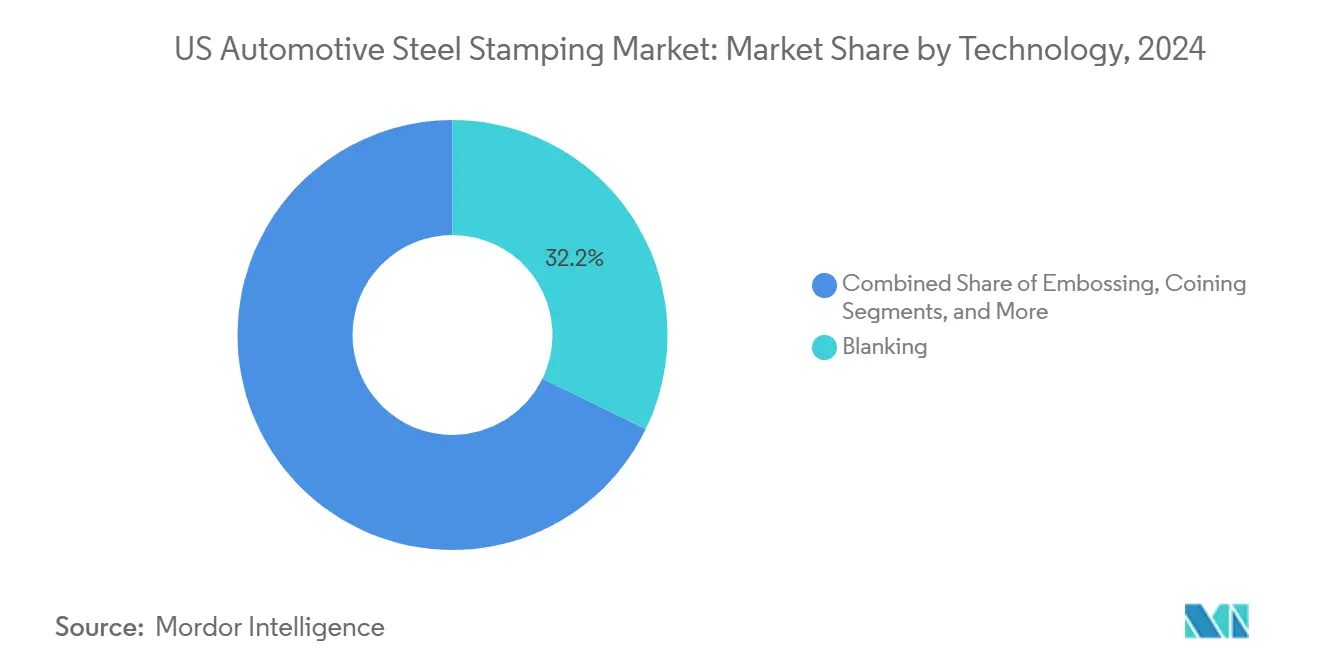

- By technology, blanking led with 32.17% revenue share in 2024, whereas embossing is projected to grow at 5.41% CAGR through 2030.

- By process, hot stamping accounted for 28.73% of the US automotive steel stamping market share in 2024 and is forecast to expand at a 5.57% CAGR to 2030.

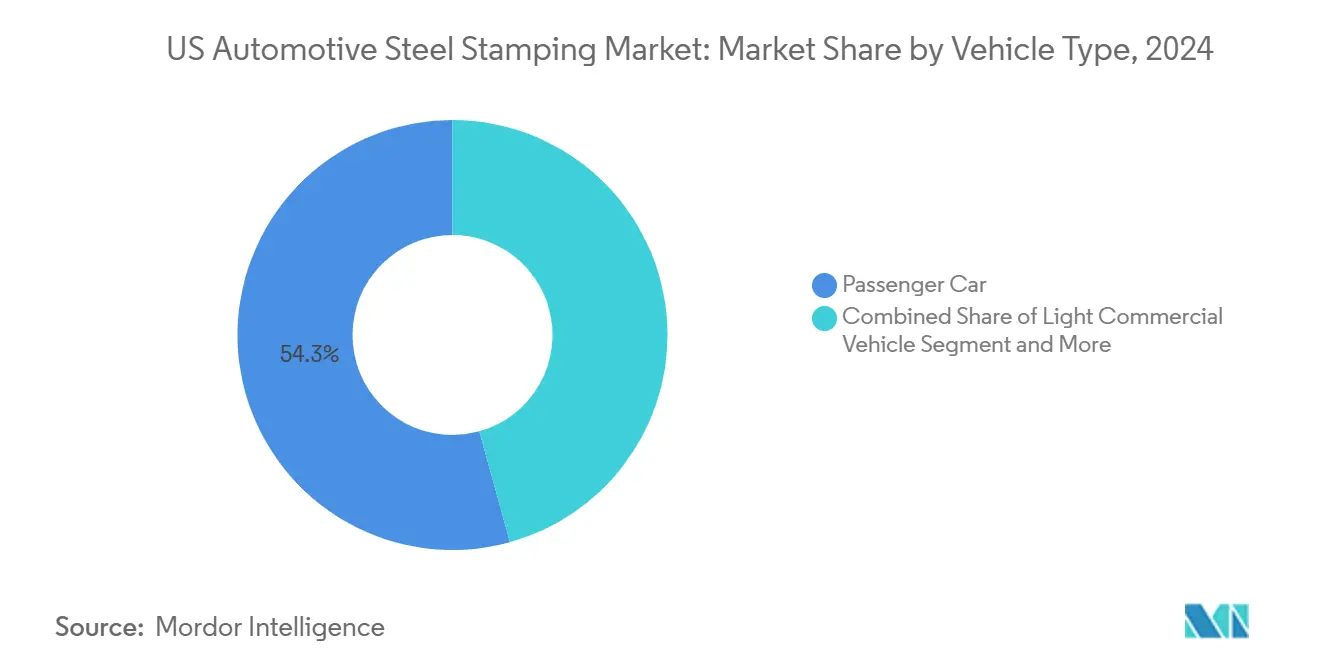

- By vehicle type, passenger cars retained a 54.26% share in 2024; light commercial vehicles show the highest projected CAGR at 5.45% through 2030.

- By propulsion, internal combustion platforms held a 64.11% share in 2024, but electric-vehicle applications are advancing at a 5.84% CAGR during the same horizon.

US Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| OEM lightweighting mandates | +1.1% | National, concentrated in Michigan, Ohio, Indiana | Medium term (2-4 years) |

| Rapid adoption of advanced & ultra-high-strength steels | +0.9% | Global, with early adoption in premium vehicle segments | Medium term (2-4 years) |

| Rising U.S. vehicle production | +0.8% | National, with emphasis on Southern manufacturing corridors | Short term (≤ 2 years) |

| Surging electric-vehicle (EV) body panel | +0.7% | California, Texas, Michigan, with spillover to Southeast | Long term (≥ 4 years) |

| Servo-press upgrades enabling complex geometries | +0.6% | Manufacturing hubs in Midwest and Southeast | Medium term (2-4 years) |

| Domestic re-shoring of metal parts | +0.4% | National, with concentration in traditional automotive states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

OEM Lightweighting Mandates for Higher CAFÉ Targets

The U.S. Department of Energy calls for around half of body-structure weight reduction by 2025 and around three-fifths by 2050. Automakers specify third-generation advanced high-strength steels with tensile strengths above 1,500 MPa for pillars, rockers, and battery enclosures. ArcelorMittal’s Fortiform® trials with KIRCHHOFF Automotive show that these steels cut component mass while keeping formability, and EPA technical assessments find that AHSS can lower overall vehicle mass by up to 26%. Stamping suppliers are investing in servo-presses and predictive forming simulation to handle tighter tolerances, which favors plants already AHSS-capable. The compressed regulatory window intensifies competition among firms offering validated die sets for such grades.

Rapid Adoption of Advanced & Ultra-High-Strength Steels (AHSS/UHSS)

According to recent SAE analysis, nine of the ten vehicles with the highest high-strength-steel utilization are electric. ThyssenKrupp will deliver low-carbon AHSS to Volkswagen from its 2027 direct-reduction plant, tying decarbonization goals to material innovation. These grades spring back more than mild steel, so suppliers deploy finite-element modeling and tailored die coatings to reach dimensional accuracy. Automakers view steel as cost-attractive versus aluminum for crash structures, and they are willing to pay premiums for CO₂-reduced grades to meet Scope 3 targets. This combination of safety, cost, and sustainability supports steady AHSS penetration over the forecast horizon.

Rising U.S. Vehicle Production Rebound Post-Pandemic

Inflation Reduction Act incentives exceed half a trillion for domestic EV manufacturing[1]“Investor Presentation 2024,” Magna International, magna.com. Honda’s CAD 15 billion Canadian EV value-chain plan and BMW’s EUR 800 million (USD 872 million) expansion in San Luis Potosí illustrate capacity growth that lifts demand for stamped steel. The production rebound favors suppliers with existing OEM relationships and quality certifications such as IATF 16949. Southern greenfield assembly plants, including Hyundai-Kia and Mazda-Toyota ventures, shift procurement geographies, so stamping firms with new facilities in Alabama, Tennessee, and Texas gain proximity advantages.

Surging Electric-Vehicle Body-Panel Demand

Gestamp reports that EV-specific components already contribute around two-fifths of its global sales, underscoring the rapid transformation of part portfolios[2] “2024 Annual Report,” Gestamp North America, gestamp.com . Battery housings, underbody shields, and side-impact beams require tighter tolerances and multi-material joining. SIMPAC’s CX servo-press line targets these parts, showing how equipment makers tailor motions for single-stroke deep draws. EV architectures locate mass centrally, so side rails and cross-members handle load paths different from ICE designs, dictating new blank shapes and die designs. Stamping firms that can prototype quickly for evolving battery sizes enjoy an edge with fast-moving EV startups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steel-price volatility | -0.6% | National, with acute impact on smaller suppliers | Short term (≤ 2 years) |

| Material substitution toward aluminum & composites | -0.5% | National, with concentration in EV manufacturing hubs | Long term (≥ 4 years) |

| High upfront capex | -0.4% | National, particularly affecting mid-tier suppliers | Medium term (2-4 years) |

| Skilled tool-and-die labor shortages | -0.3% | National, with acute impact in traditional manufacturing regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Steel-Price Volatility Compressing Supplier Margins

Hot-rolled coil averaged around a thousand USD per ton during 2024 swings, squeezing firms with thin working-capital buffers. Europe’s demand slumped slightly in Q1 2024, creating a global oversupply that spilled into North America. Large Tier 1 stampers secure multi-year contracts; smaller suppliers rely on spot buys and suffer margin erosion when coil prices spike. Some resort to value-stream mapping to cut internal waste, but many lack the negotiation power to recoup surcharges from OEM customers. Persistent volatility fuels consolidation as financially stronger groups acquire distressed niche shops to broaden plant footprints.

High Upfront Capex for Progressive-Die Tooling

Complex progressive dies demand more than a million USD before a single part ships, and AHSS coils elevate die-steel and coating costs by up to 30%. Wilson Tool’s purchase of PASS Stanztechnik reflects the need for scale to amortize precision grinding, wire-EDM, and laser-hardening systems. OEMs press for shorter development loops, and suppliers respond with 3-D-printed prototype dies and modular inserts. Even so, capital hurdles deter entrants, reinforcing incumbents that own in-house die-making and refurbishment shops.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Blanking Leads Complex-Geometry Demand

Blanking generated the most significant revenue contribution of 32.17% in 2024 within the US automotive steel stamping market. Its dominance stems from being the universal first step that converts coil into precise blanks for every downstream operation. Volumetric growth parallels vehicle builds, so blanking volume curves align with OEM schedules. Yet blanking firms still differentiate by integrating optical inspection and high-speed servo feeders that cut takt times. Embossing, although smaller, is the fastest-growing at a 5.41% CAGR because EV battery covers and side-impact beams need local stiffening ribs. Suppliers that master embossing on 1,200 MPa steels without thinning possess an attractive niche.

The remaining methods—bending, flanging, coining, and emerging hydroforming—see steady but slower uptake as they serve legacy brackets, seat tracks, and mount points. Hydroforming appears in prototype skateboard frames, but volumes stay low. Flanging remains vital for weld-flange preparation on outer panels, while coining ensures tight flatness on gasket surfaces. Automation, sensor feedback, and quick-change conveyors form key investment themes that keep each technology class competitive.

By Process: Hot Stamping Dominates Premium Applications

Hot stamping captured 28.73% share in 2024 and also delivers the top growth rate of 5.57% CAGR, reflecting its dual capability to shape and quench ultra-high-strength boron steel in one cycle. This capability satisfies stringent IIHS side-impact and roof-crush targets. Light-commercial makers adopt hot-stamped A-pillars and door rings to cut weight and increase payload, supporting uptake beyond premium sedans. Roll forming holds a reliable base for rocker panels, yet volume migration to hot stamping slowly erodes its share. Traditional sheet-metal cold stamping remains critical for outer skin parts, but its CAGR lags as aluminum hang-on panels gain ground.

Sheet-metal fabrication houses integrate welding cells to assemble bracket substructures, creating one-stop modules. Incremental forming, a still-experimental category, shows promise for service-parts runs and bespoke luxury models. Suppliers that bundle laser trimming with hot forming win business on intricate patchweld blanks, underscoring the role of auxiliary processes.

By Vehicle Type: Commercial Segments Drive Growth

Passenger cars accounted for 54.26% revenue in 2024, due to higher unit output and a complex skin-panel mix. Model refresh cycles every four to five years, keeping tool orders predictable. Light commercial vehicles, however, are pacing at a 5.45% CAGR through 2030, driven by e-commerce parcel vans and urban last-mile fleets. EV-only panel vans like BrightDrop Zevo implement stamped steel underbody enclosures, lifting content per vehicle. Heavy trucks use thicker gauge AHSS for frame cross-members; volumes lag light segments, yet part weight raises dollar revenue per unit.

Fleet electrification policies at firms like Amazon and USPS accelerate demand for lightweight commercial van structures. Stamping suppliers respond with dedicated die sets for large sliding-door apertures and reinforced floor pans. Passenger-car stampers hedge by adding commercial vehicle work cells to diversify order books.

By Propulsion: EV Transition Accelerates Steel Innovation

Internal combustion platforms still account for 64.11% of 2024 revenue, but electric-vehicle stamping lines expand at a 5.84% CAGR as OEMs swap engine bays for battery cages. EV underbody shield panels need deep draws and multiple emboss patterns for crash energy absorption; hot stamping serves this niche. Battery enclosures sport mix-metal architectures; steel top covers attach to aluminum trays via self-pierce rivets.

Hybrid powertrains add battery cradles alongside ICE mounts, increasing mixed-material joining demand. Stamping firms develop tool coatings that resist galling on coated aluminum blanks when mixed lines run short changeovers. Suppliers that stay propulsion-agnostic build fixtures for both ICE tunnel reinforcements and EV edge beams and maintain plant utilization during the transition.

Geography Analysis

Midwestern states such as Michigan, Ohio, and Indiana continue to anchor over half of the total volumes within the US automotive steel stamping market, leveraging dense supplier networks and proximity to legacy assembly plants. Detroit Three OEMs rely on these clusters for rapid engineering liaison and just-in-sequence deliveries. Yet land constraints and higher labor costs motivate new capacity to gravitate toward the Southeast. Alabama and Tennessee plants by Hyundai, Kia, and Volkswagen attract stamping satellites prioritizing lower utility tariffs and modern logistics links.

Texas now hosts Tesla’s Gigafactory in Austin, creating fresh pull for high-tonnage press lines that stamp large body-side outer blanks. Suppliers nearby benefit from state training grants and highway connectivity to Mexican maquiladoras. California’s regulatory reach influences tool specification nationally as its ZEV mandate spreads to other states; local R&D centers in Palo Alto and Fremont help refine prototype battery housings before full-scale stamping occurs elsewhere.

The Great Lakes still command unmatched die-making skills, so complex progressive dies often originate in Chicago or Detroit before production transfers to Southern press shops. Cross-state shipping remains viable because dies move once, while daily panel logistics favor co-location. This blended model underpins current investment patterns and keeps the US automotive steel stamping market resilient across shifting regional cost structures.

Competitive Landscape

Competition remains fragmented; the top five firms accounted for less than two-fifths of 2024 revenue, leaving ample scope for mid-tier specialists. Gestamp deepened its Midwest footprint with a 580-employee Michigan expansion that adds servo-press lines for EV side-ring parts. Magna International ramped a greenfield Arizona site to serve Lucid Motors, blending stamping with e-Beam welding for lightweight closures. ThyssenKrupp Automotive Technology posted EUR 7.5 billion (USD 8.21 billion) in 2024 sales despite inflation headwinds, evidencing scale resilience.

Regional suppliers differentiate with quick-turn die-repair services and low-volume prototype support for new EV entrants. Servo-press ownership is a rising barrier because AHSS blanks demand variable velocity profiles. Firms without such capability often partner on tier-two, relinquishing direct OEM contracts. Consolidation gathers pace as larger groups scoop up distressed tool shops to secure supply and Intellectual Property around die coatings.

Vertical integration shapes strategy: Hyundai Steel’s Louisiana mill connects upstream coil casting to downstream stamping, promising price stability. Nippon Steel’s purchase of US Steel creates the second-largest global steel producer, expected to supply captive R&D for new AHSS grades. Stamping houses with strategic steel alliances will likely secure coil allocations during market tightness, a critical edge over independents.[3]“Acquisition of US Steel,” Nippon Steel Corporation, nipponsteel.com

US Automotive Steel Stamping Industry Leaders

Gestamp Automoción

Magna International (Cosma)

Tower International

Shiloh Industries

Martinrea International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hyundai Steel unveiled a USD 5.8 billion plan for an EAF-based integrated mill in Louisiana to produce 2.7 million t of automotive sheet annually starting 2029.

- February 2025: ArcelorMittal committed USD 1.2 billion to build a non-grain-oriented electrical-steel facility in Alabama with 150,000 t yearly capacity for EV motor cores.

US Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet-Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Car |

| Light Commercial Vehicle |

| Medium and Heavy Commercial Vehicle |

| Internal-Combustion Engine (ICE) |

| Electric Vehicle (EV) |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet-Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicle | |

| Medium and Heavy Commercial Vehicle | |

| By Propulsion | Internal-Combustion Engine (ICE) |

| Electric Vehicle (EV) |

Key Questions Answered in the Report

What is the value of the US automotive steel stamping market in 2025?

It is valued at USD 3.91 billion with a projected rise to USD 5.07 billion by 2030.

Which stamping process shows the fastest growth through 2030?

Hot stamping posts the highest CAGR at 5.57% because it combines forming and quenching for ultra-high-strength parts.

Why are electric vehicles boosting demand for stamped steel parts?

EVs need battery enclosures, underbody shields, and side-impact structures that rely on advanced high-strength steel for safety and weight savings.

How will the reshoring trend influence US suppliers?

Domestic steel mills such as Hyundai’s Louisiana site reduce tariff exposure and transport costs, favoring local stamping plants with quick delivery.

What challenges do smaller stamping firms face?

They struggle with steel-price volatility and the USD 1–5 million upfront cost of progressive dies, which constrains cash flow and limits growth.

Which states offer the strongest growth outlook for stamping capacity?

Alabama, Tennessee, and Texas lead growth due to new OEM assembly plants and supportive economic-development incentives.

Page last updated on: