UAE Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

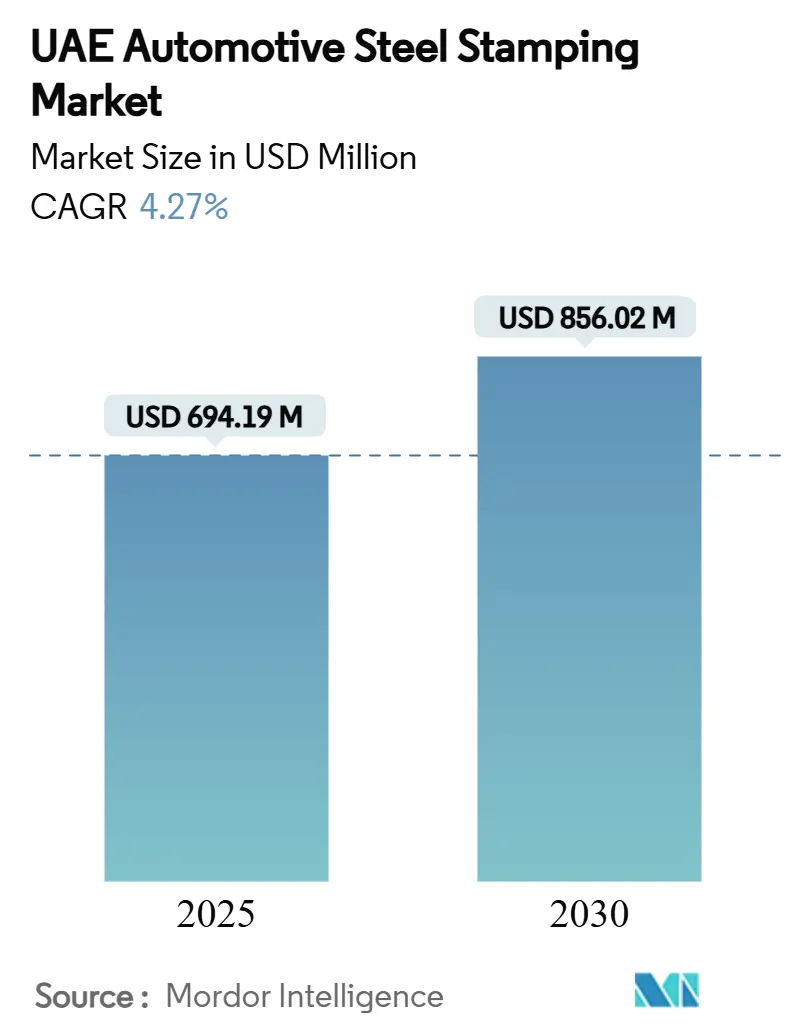

| Market Size (2025) | USD 694.19 Million |

| Market Size (2030) | USD 856.02 Million |

| Growth Rate (2025 - 2030) | 4.27% CAGR |

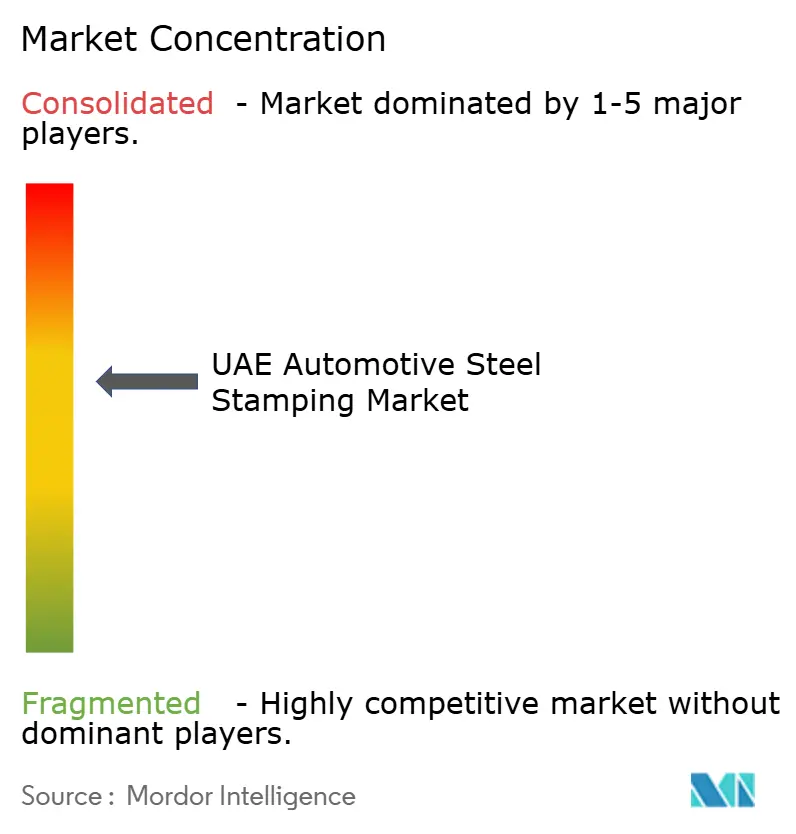

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

UAE Automotive Steel Stamping Market Analysis by Mordor Intelligence

The UAE automotive steel stamping market size is valued at USD 694.19 million in 2025 and is projected to reach USD 856.02 million by 2030, registering a 4.27% CAGR during the forecast period. This expansion mirrors the country’s widening industrial base, the government’s Operation 300 bn agenda, and rising electrification targets that require stronger yet lighter body-in-white parts. Demand pivots on advanced high-strength steel (AHSS) components that balance weight and crash safety, while new gigafactory investments and an expanding free-zone network keep international suppliers engaged. Etihad Rail’s 900 km corridor cuts logistics costs for coils and finished parts, increasing just-in-time efficiency for tier-1 stampers. At the same time, electricity tariffs and limited passenger-vehicle assembly temper competitiveness against Asian supply hubs. However, fresh industrial financing and targeted tax holidays continue to make the UAE automotive steel stamping market an increasingly attractive site for high-value forming operations.

Key Report Takeaways

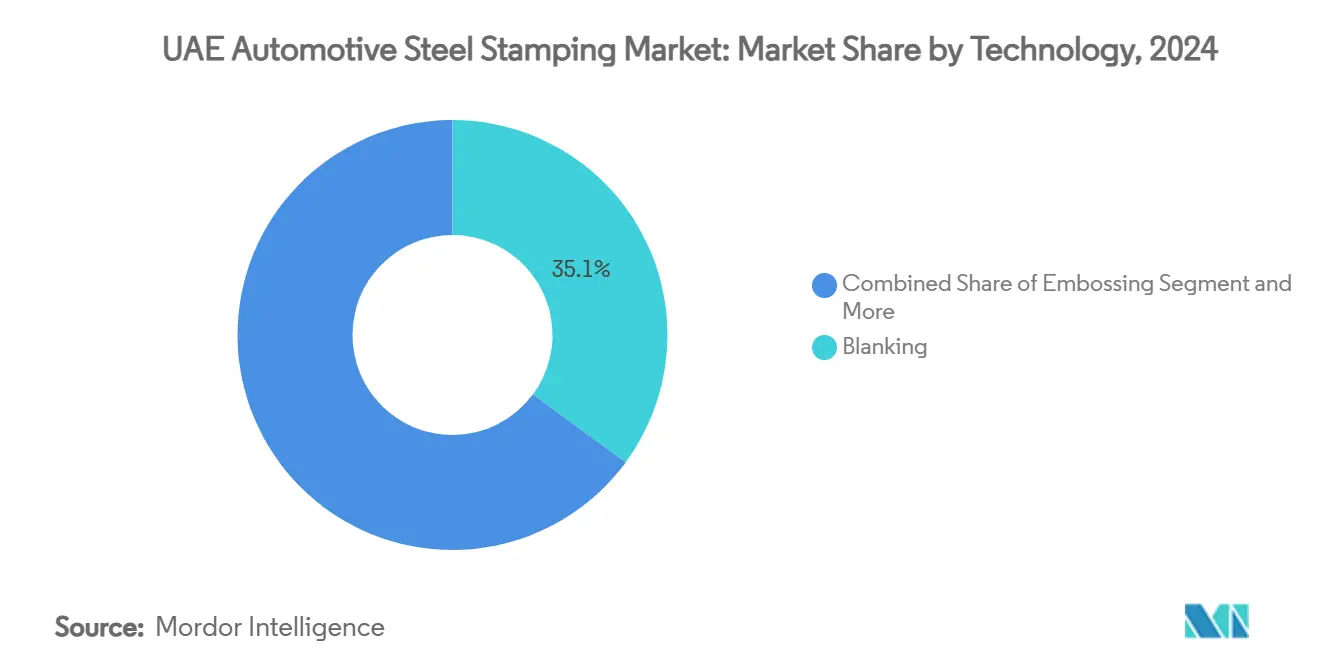

- By technology, blanking led with 35.14% of the UAE automotive steel stamping market share in 2024, while hot-stamped AHSS is forecast to rise at a 9.92% CAGR through 2030.

- By process, hot stamping captured 38.27% of the UAE automotive steel stamping market in 2024 and is advancing at a 9.87% CAGR to 2030.

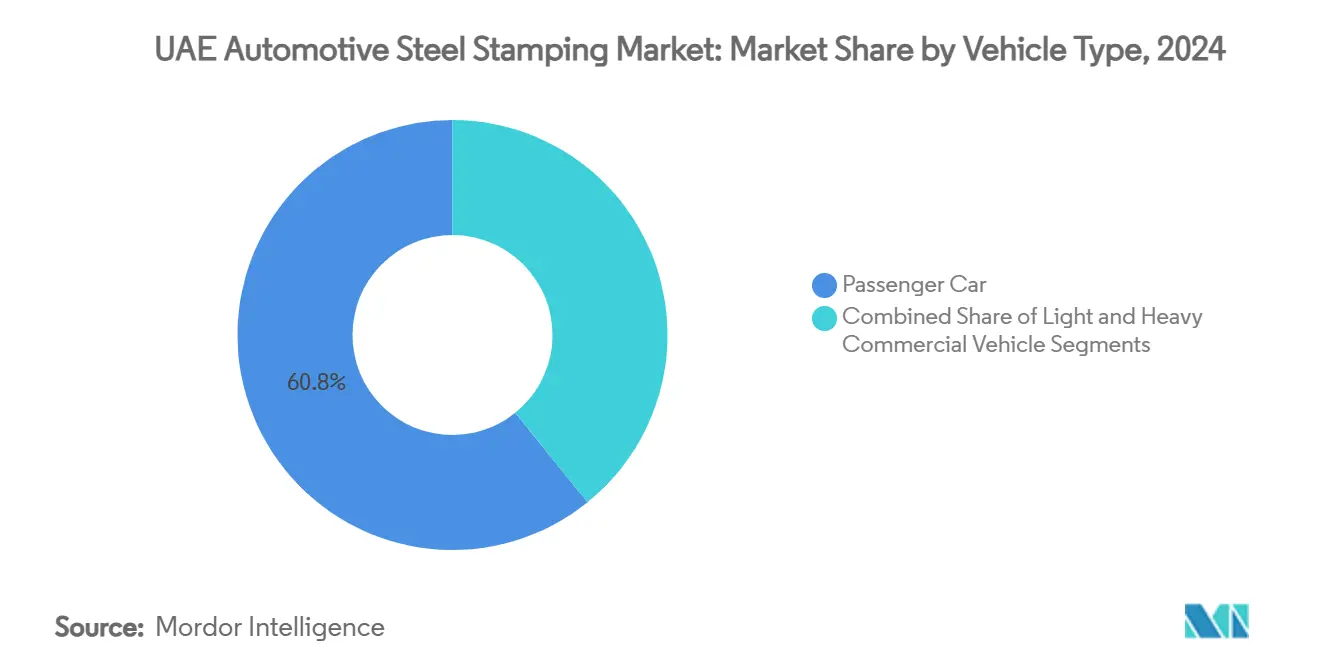

- By vehicle type, passenger cars accounted for 60.84% of the UAE automotive steel stamping market size in 2024, and the electric-passenger subsegment is expanding at an 11.63% CAGR through 2030.

- By propulsion, internal combustion platforms still held 71.78% of the UAE automotive steel stamping market share in 2024, whereas electric vehicle stampings are surging at a 19.12% CAGR to 2030.

- By geography, Abu Dhabi retained 45.92% of the UAE automotive steel stamping market share in 2024; Dubai is growing fastest at a 12.08% CAGR through 2030.

UAE Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight Vehicle Demand | +1.2% | Global, with concentration in Abu Dhabi and Dubai | Medium term (2–4 years) |

| EV Incentives Boosting Adoption | +0.8% | National, with early gains in Abu Dhabi, Dubai | Short term (≤ 2 years) |

| Etihad Rail Enabling JIT Stamping | +0.6% | National, connecting all emirates | Long term (≥ 4 years) |

| Tax Holidays for Local Stamping | +0.4% | Dubai, Sharjah, and Northern Emirates | Medium term (2–4 years) |

| Localized EV Battery-Pack Enclosures | +0.7% | Abu Dhabi core, spill-over to Dubai | Medium term (2–4 years) |

| Safety Norms Driving Hot-Stamped AHSS | +0.5% | National compliance requirement | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Lightweight, Fuel-Efficient Vehicles

The automotive industry's weight reduction imperative is fundamentally altering steel stamping specifications, with advanced high-strength steels now achieving tensile strengths up to 2,040 MPa while enabling 40% weight reductions in crash components. This transformation extends beyond traditional lightweighting to encompass electric vehicle applications, where steel accounts for significant emissions in EV production and every kilogram saved translates to extended battery range. The UAE's position as a regional hub for automotive parts trade, with significant re-exports to neighboring countries, amplifies the impact of these specifications changes across the broader GCC market. Hot stamping technology, which transforms steel into ultra-high strength martensite with intensities around 1,500 MPa, is becoming the preferred method for producing complex geometries while maintaining dimensional accuracy[1]"The Research and Development of Hot Stamping Forming Technology and Production Line in View of High Strength Steel Plate," Scientific.Net, scientific.net.. The process allows manufacturers to achieve minimal springback and excellent formability, critical factors for producing EV battery protection systems and structural components that meet both safety and efficiency requirements.

Government Incentives Accelerating EV Adoption

The UAE's National Electric Vehicles Policy, implemented in 2023, establishes a comprehensive framework targeting a 20% reduction in transport sector energy consumption by 2050 while promoting industrial growth in the EV ecosystem[2]"The National Electric Vehicles Policy," Ministry of Energy and Infrastructure, uaelegislation.gov.ae.. This policy framework extends beyond consumer incentives to encompass manufacturing support, with the government targeting 70,000 charging points by 2030 and encouraging local assembly of electric vehicles under the Make it in the Emirates initiative. The policy's industrial focus creates direct demand for specialized steel stamping capabilities, particularly for EV-specific components like battery enclosures, thermal management systems, and lightweight structural elements. Abu Dhabi's commitment to establishing a USD 2.72 billion manufacturing investment plan, targeting 13,600 skilled jobs by 2031, specifically emphasizes transportation sector development. The convergence of EV adoption incentives with manufacturing support creates a multiplier effect, where consumer demand drives local production requirements, which in turn necessitates advanced steel stamping capabilities for components that traditional ICE vehicles do not require.

Etihad Rail Logistics Corridor Enabling JIT Stamping Supply

The Etihad Rail network's transformation of UAE logistics fundamentally alters the economics of steel stamping operations by enabling just-in-time supply chains that reduce working capital requirements and inventory costs. The 900 km network connects key industrial centers from Saudi Arabia to Oman, with freight services projected to handle 60 million tons by 2030, creating unprecedented opportunities for integrated supply chain optimization. This infrastructure advantage becomes particularly significant for automotive steel stamping, where raw material costs represent 60-70% of total production expenses and inventory carrying costs can substantially impact competitiveness. The rail network's partnership with companies like Al Jazeera Steel Products demonstrates the practical application of this infrastructure, with agreements to transport up to 15,000 tons of freight while reducing reliance on road transport. For stamping operations, this connectivity enables synchronization with steel coil deliveries from Emirates Steel Arkan's facilities while facilitating finished component distribution across the GCC region. The rail network's integration with port facilities and free zones creates a logistics ecosystem that can compete with established automotive manufacturing clusters in Asia and Europe.

Free-Zone Tax Holidays for Local Stamping Plants

Dubai's 2025 Executive Council Resolution enabling free zone entities to expand into mainland operations represents a paradigm shift in UAE manufacturing economics, allowing companies to leverage tax advantages while accessing broader market opportunities[3]"Dubai's Game-Changer: New Executive Council Resolution Unlocks Mainland Access for Free Zone Companies," cms-lawnow.com.. This regulatory evolution addresses a longstanding constraint where free zone manufacturers faced limitations in serving domestic markets, forcing them to choose between tax efficiency and market access. For automotive steel stamping operations, this change enables companies to establish production facilities in tax-advantaged zones while serving both local assembly operations and export markets without regulatory barriers. The resolution's requirement for separate financial records and compliance with local regulations creates operational complexity but preserves the fundamental economic advantages that make UAE manufacturing competitive. KEZAD Group's expansion, including a 51,015 sqm metals facility lease with Ducab Metals Business, demonstrates how free zone operators are positioning for this regulatory shift. The timing coincides with global automotive supply chain diversification trends, where OEMs seek to reduce concentration risk by establishing alternative supplier bases outside traditional manufacturing centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Vehicle Assembly Base | -1.1% | National, particularly affecting export dependency | Long term (≥ 4 years) |

| High Power & Decarbonization Costs | -0.7% | National, with higher impact in Dubai and Northern Emirates | Medium term (2–4 years) |

| Die-Making Skill Shortages | -0.4% | National, concentrated in technical manufacturing zones | Medium term (2–4 years) |

| Imported Coil Steel Dependence | -0.3% | National, affecting all production centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Vehicle-Assembly Base

The UAE's automotive manufacturing ecosystem remains constrained by minimal local vehicle assembly capacity, with production primarily limited to commercial vehicles through companies like Ashok Leyland and specialized applications rather than mass-market passenger vehicles. This structural limitation forces steel stamping operations to depend heavily on export markets and aftermarket demand, creating vulnerability to regional economic fluctuations and trade policy changes. The absence of major OEM assembly plants means local stamping companies cannot leverage the economies of scale and technical collaboration that typically develop around automotive manufacturing clusters. While the UAE's strategic position enables significant re-exports to neighboring countries, this model inherently limits the development of sophisticated stamping capabilities that require close integration with vehicle design and production processes. The challenge becomes more acute as global automotive supply chains increasingly emphasize regional integration and just-in-time manufacturing, where proximity to final assembly operations provides competitive advantages that pure trading relationships cannot replicate.

High Electricity Tariffs and Decarbonization Compliance Costs

Industrial electricity costs in the UAE present a significant competitiveness challenge for energy-intensive steel stamping operations, particularly as global decarbonization mandates require investments in cleaner production technologies. The UAE's industrial sector faces mounting pressure to achieve net-zero targets by 2050, with companies like Emirates Steel Arkan committing to operate with 45% less carbon emissions through clean energy adoption. For steel stamping operations, this transition requires substantial capital investments in energy-efficient equipment and renewable energy systems, costs that must be absorbed while maintaining price competitiveness against suppliers in markets with lower energy costs. The challenge intensifies as automotive OEMs increasingly mandate low-carbon steel in their supply chains, requiring stamping operations to source materials from suppliers with verified emissions reductions. European industrial electrification studies indicate that up to 78% of industrial energy use could be electrified, but the transition requires robust electricity storage systems and infrastructure investments that add to operational complexity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Blanking Dominates While Hot-Stamped AHSS Accelerates

Blanking technology commands 35.14% market share in 2024, reflecting its fundamental role in producing basic automotive components across all vehicle types and applications. The technology's dominance stems from its versatility in processing various steel grades and thicknesses, making it essential for both traditional ICE vehicles and emerging EV applications. However, hot-stamped AHSS represents the fastest-growing technology segment at 9.92% CAGR through 2030, driven by automotive lightweighting mandates and safety requirements that demand ultra-high strength components. This growth differential illustrates the market's evolution toward more sophisticated manufacturing processes that can achieve the complex geometries and material properties required for modern vehicle designs.

Embossing and coining technologies serve specialized applications in decorative and functional components, maintaining steady demand but limited growth potential as automotive design trends favor cleaner, more minimalist aesthetics. Flanging operations remain critical for structural components and assembly interfaces, particularly in EV battery pack construction where precise dimensional tolerances are essential for thermal management and safety systems. Bending technologies continue to evolve with advances in servo-electric press systems that provide greater precision and energy efficiency compared to traditional hydraulic systems. The technology segmentation reflects broader industry trends toward process consolidation, where manufacturers seek to reduce tooling complexity and cycle times through integrated forming operations that combine multiple traditional processes into single-step solutions.

By Process: Hot Stamping Leads Innovation Drive

Hot stamping processes capture 38.27% market share in 2024 and maintain the highest growth rate at 9.87% CAGR, positioning this technology as the cornerstone of advanced automotive steel stamping in the UAE. The process's ability to produce components with tensile strengths exceeding 1,500 MPa while maintaining formability makes it indispensable for safety-critical applications like A-pillars, B-pillars, and door frames that must withstand crash loads while minimizing weight. Recent developments in low-temperature hot stamping technologies address productivity concerns by reducing energy requirements and cycle times, making the process more economically viable for medium-volume applications. The UAE's adoption of hot stamping aligns with global automotive trends, where manufacturers like Honda achieved 41-pound weight reductions in the Acura RDX through increased use of ultra-high-strength steel components.

Roll forming and sheet-metal forming processes serve complementary roles in producing longer components and complex three-dimensional shapes that cannot be efficiently manufactured through stamping operations. Metal fabrication encompasses welding, joining, and assembly operations that integrate stamped components into larger assemblies, particularly important for EV battery enclosures where multiple stamped components must be precisely assembled to ensure thermal and electrical safety. The process segmentation reflects the industry's movement toward integrated manufacturing cells where multiple forming operations are combined to reduce material handling and improve dimensional consistency. Strata's partnership with Pilatus to manufacture hot press parts in the UAE demonstrates the technology transfer occurring as international aerospace and automotive companies establish local production capabilities.

By Vehicle Type: Passenger Cars Drive Volume While Commercial Vehicles Show Promise

The passenger car segment maintains 60.84% market share in 2024, reflecting the UAE's vehicle fleet composition, where passenger vehicles represent approximately 80% of total registrations. However, the electric passenger car subsegment emerges as the fastest-growing category at 11.63% CAGR, significantly outpacing traditional passenger vehicle growth as the UAE implements policies targeting 25% autonomous transportation by 2030. This growth trajectory creates distinct requirements for steel stamping operations, as electric passenger vehicles require specialized components for battery protection, thermal management, and structural reinforcement that differ substantially from ICE vehicle specifications. Light commercial vehicles represent a growing opportunity as e-commerce expansion and last-mile delivery services drive demand for urban delivery vehicles, many of which are transitioning to electric powertrains to comply with urban emissions regulations.

Heavy commercial vehicles maintain steady demand driven by construction and logistics activities, but face increasing pressure to adopt alternative powertrains as the UAE pursues its net-zero objectives. The Etihad Rail network's development creates specific opportunities for specialized rail transport vehicles and maintenance equipment that require custom steel stamping solutions. Companies like Changan Automobile's 51% growth in the MEA region, with new models like the DEEPAL S07 electric vehicle, demonstrate the market's shift toward electrified platforms that require different stamping capabilities. The vehicle type segmentation increasingly reflects powertrain considerations rather than traditional size categories, as electric vehicle architectures enable new design approaches that blur conventional distinctions between passenger and commercial vehicle platforms.

By Propulsion: ICE Dominance Faces EV Disruption

Internal combustion engine vehicles command 71.78% market share in 2024, but this dominance faces systematic erosion as electric vehicle adoption accelerates at 19.12% CAGR through 2030. The growth differential reflects the UAE's strategic commitment to electrification, with government policies targeting 50% of commercial vehicles to be electric by 2050 and infrastructure investments supporting 70,000 charging points by 2030. This transition creates fundamentally different requirements for steel stamping operations, as EV platforms require components for battery protection, electromagnetic shielding, and thermal management that have no equivalent in ICE vehicles. The UAE's National Electric Vehicles Policy provides a regulatory framework and incentives that accelerate this transition while creating opportunities for local manufacturing of EV-specific components.

The propulsion segmentation reveals the market's bifurcation into declining traditional applications and rapidly expanding electrified segments that require new manufacturing capabilities. ICE vehicle stamping operations face margin pressure as volumes decline and competition intensifies, while EV component stamping commands premium pricing due to technical complexity and a limited supplier base. Lucid Motors' expansion in the UAE, with showrooms and service centers in Dubai, exemplifies how luxury EV manufacturers are establishing a regional presence and potentially creating demand for local component supply. The transition timeline suggests that stamping operations must develop capabilities for both propulsion types during the forecast period, requiring flexible manufacturing systems that can adapt to changing product mix requirements as the market evolves.

Geography Analysis

Abu Dhabi’s dominance stems from 3.5 million ton upstream capacity that now operates on 80% clean energy, supporting OEM mandates for low-carbon steel. Multimodal corridors knit KEZAD to Khalifa Port and Etihad Rail yards, cutting door-to-quay trucking by 30 %. ADNOC’s commitment to source AED 90 billion of industrial inputs locally by 2030 further underwrites volume visibility for stampers aligned with its vendor lists.

Dubai’s growth accelerates as free-zone borders blur. The emirate’s decision to allow dual mainland licensing lets Jebel Ali-based presses serve UAE dealer networks without intermediaries, expanding order books while preserving zero-tax status. Logistics trifecta—port, airport, and rail spur—supports 24-hour coil inflow and finished-part escalation to GCC plants. With a deep engineering labour pool, Dubai attracts technology-intensive cell manufacturers keen to capitalise on expanding charging infrastructure.

Although smaller, Sharjah and the Northern Emirates offer strategic niches: cost-effective land, access to Emirates Road arteries, and tailored incentives for SME tooling shops. Ras Al Khaimah’s low-carbon cement cluster augments vehicle-related metals work, while Fujairah’s deep-water port opens an Indian-Ocean route that bypasses Hormuz chokepoints, appealing to Asian coil suppliers looking for alternate Gulf gateways.

Competitive Landscape

Competition in the UAE automotive steel stamping market is moderately fragmented. Emirates Steel Arkan leverages raw-steel integration and 16 production plants to supply coil tailored for advanced hot stamping, strengthening its bargaining position with tier-1 customers. Strategic patterns emphasize technology transfer, local partnership development, and supply chain integration as companies seek to balance cost competitiveness with technical sophistication required for modern automotive applications.

The market's evolution toward electrification creates opportunities for companies that can develop capabilities in electromagnetic shielding, thermal management components, and battery protection systems that require manufacturing approaches different from traditional automotive stamping applications. Emerging disruptors include companies leveraging digital manufacturing technologies and sustainable production methods to serve the growing segment of environmentally conscious automotive OEMs seeking to reduce supply chain emissions.

Strategic moves focus on sustainability and localisation. Emirates Steel Arkan rebranded to EMSTEEL, promising 45% emission cuts by 2030 and EUR 200 million capex for direct-reduction furnaces. Mashreq Bank’s extra AED 1 billion credit window promotes automation upgrades among SME press shops. Global EV newcomers, such as Lucid Motors, install showroom-assembly hybrids in Dubai, signalling future localisation of low-volume stampings

UAE Automotive Steel Stamping Industry Leaders

-

Emirates Steel Arkan (EMSTEEL)

-

Dana Steel UAE

-

Oasis Metal Mfg.

-

Al Ghurair Iron & Steel

-

Automech Steel Industries LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Emirates Steel Arkan completed its rebranding to EMSTEEL, emphasizing operational transformation and worldwide expansion while maintaining 16 plants with 3.5 million mt steel capacity and 4.6 million mt cement capacity, exporting to over 70 markets. The company committed to supporting UAE's Net Zero by 2050 initiative with 80% clean energy operations.

- July 2024: Mashreq Bank allocated additional AED 1 billion in financing for UAE industrial companies to boost investment attractiveness, aligning with the Make it in the Emirates initiative and supporting technological transformation in manufacturing sectors including metal industries.

UAE Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet-Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Car |

| Light Commercial Vehicle |

| Heavy Commercial Vehicle |

| Internal Combustion Engine (ICE) |

| Electric Vehicle (EV) |

| Abu Dhabi |

| Dubai |

| Sharjah and Northern Emirates |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet-Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicle | |

| Heavy Commercial Vehicle | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric Vehicle (EV) | |

| By Emirate | Abu Dhabi |

| Dubai | |

| Sharjah and Northern Emirates |

Key Questions Answered in the Report

How large is the UAE automotive steel stamping market in 2025?

The UAE automotive steel stamping market size stands at USD 694.19 million in 2025.

What CAGR is forecast for UAE automotive steel stamping through 2030?

The market is projected to grow at a 4.27% CAGR from 2025 to 2030.

Which technology segment is expanding fastest in UAE stamping?

Hot-stamped AHSS components are advancing at a 9.92% CAGR due to lightweighting and safety mandates.

Why is Abu Dhabi the leading emirate for automotive steel stamping?

Abu Dhabi offers upstream coil supply from Emirates Steel Arkan and industrial zones with rail-port integration, giving it 45.92% market share.

How will electrification influence UAE stamp-shop demand?

EV adoption, rising at a 19.12% CAGR, lifts demand for battery-enclosure and under-body stampings, reshaping tool and material requirements.

What infrastructure project supports just-in-time stamping logistics?

The 900 km Etihad Rail freight network enables rapid coil and finished-part movement across the federation, cutting inventory costs.

Page last updated on: