South Korea Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

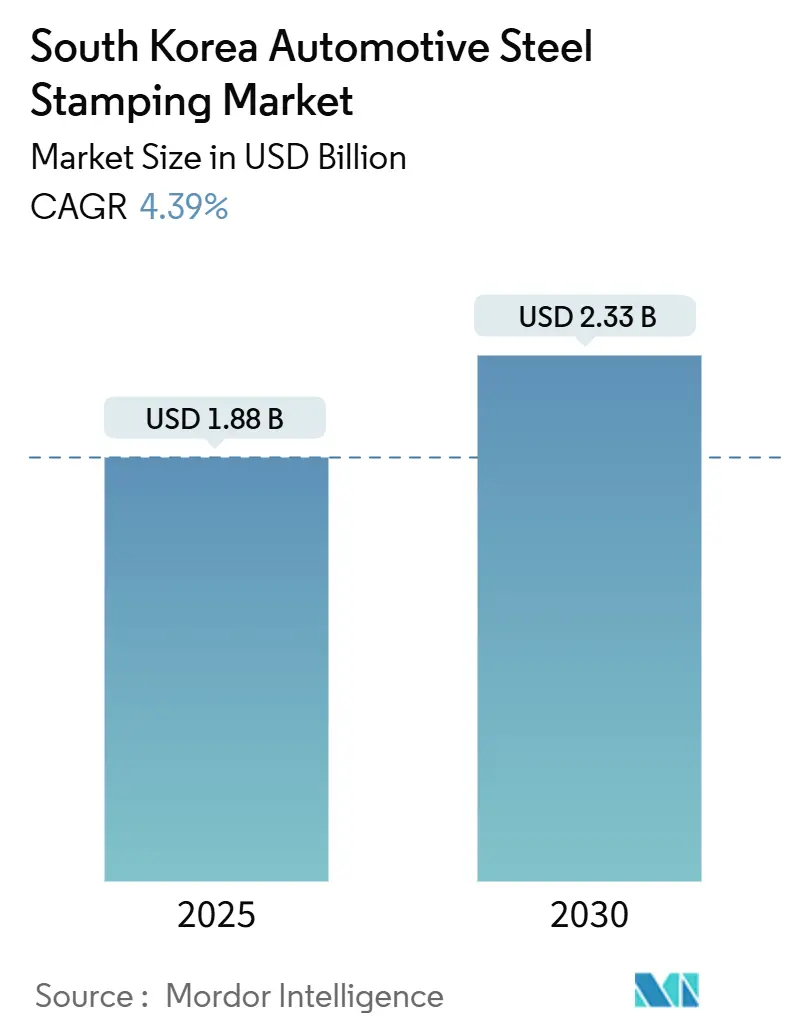

| Market Size (2025) | USD 1.88 Billion |

| Market Size (2030) | USD 2.33 Billion |

| Growth Rate (2025 - 2030) | 4.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Automotive Steel Stamping Market Analysis by Mordor Intelligence

The South Korea automotive steel stamping market size stands at USD 1.88 billion in 2025 and is forecast to reach USD 2.33 billion by 2030, expanding at a 4.39% CAGR during the period. This steady trajectory reflects regulatory pressure for lighter vehicles, the surging scale-up of electric-vehicle assembly, and government capital-expenditure incentives that promote low-carbon steel technologies. Market growth also mirrors the transition from volume-oriented output toward precision-engineered panels that differentiate local brands in export destinations. Competitive dynamics stay intense as vertically integrated steel groups battle specialist stampers able to exploit digital-twin press shops that cut scrap and compress development cycles.

Key Report Takeaways

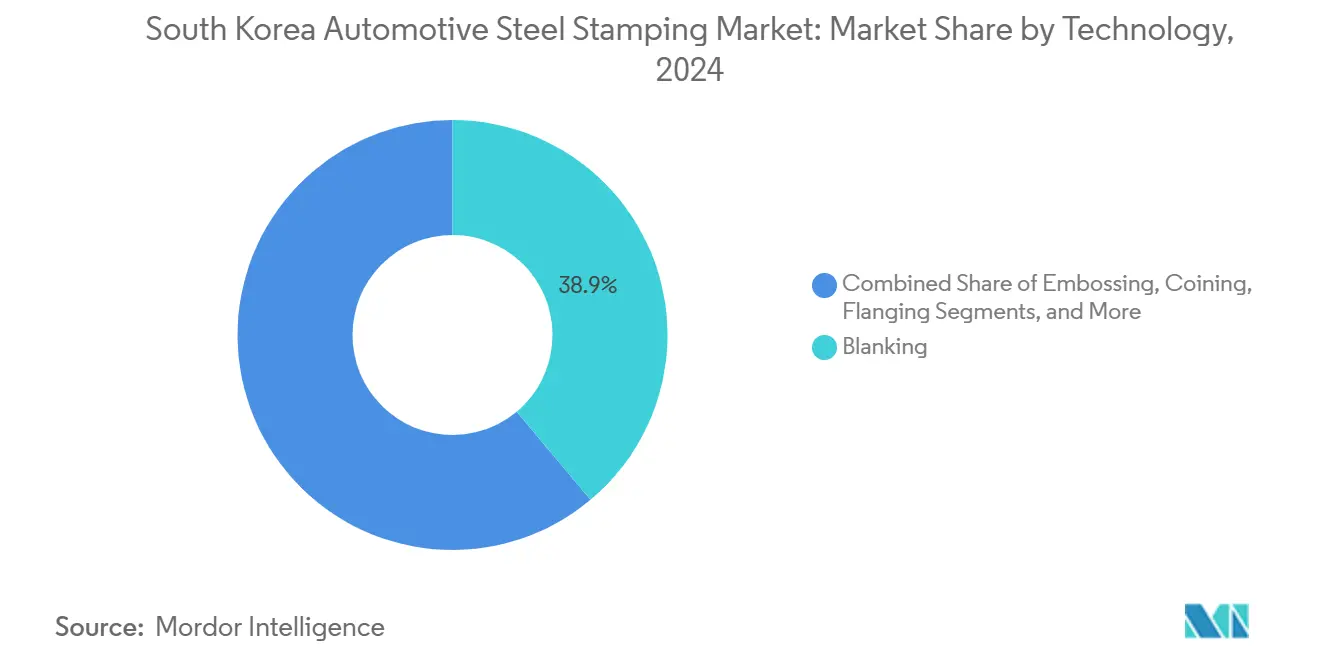

- By technology, blanking led with 38.91% of South Korea automotive steel stamping market share in 2024; flanging is projected to expand at a 5.85% CAGR through 2030.

- By process, hot stamping accounted for 46.25% of the South Korea automotive steel stamping market size in 2024, while roll forming recorded the fastest growth at 6.16% to 2030.

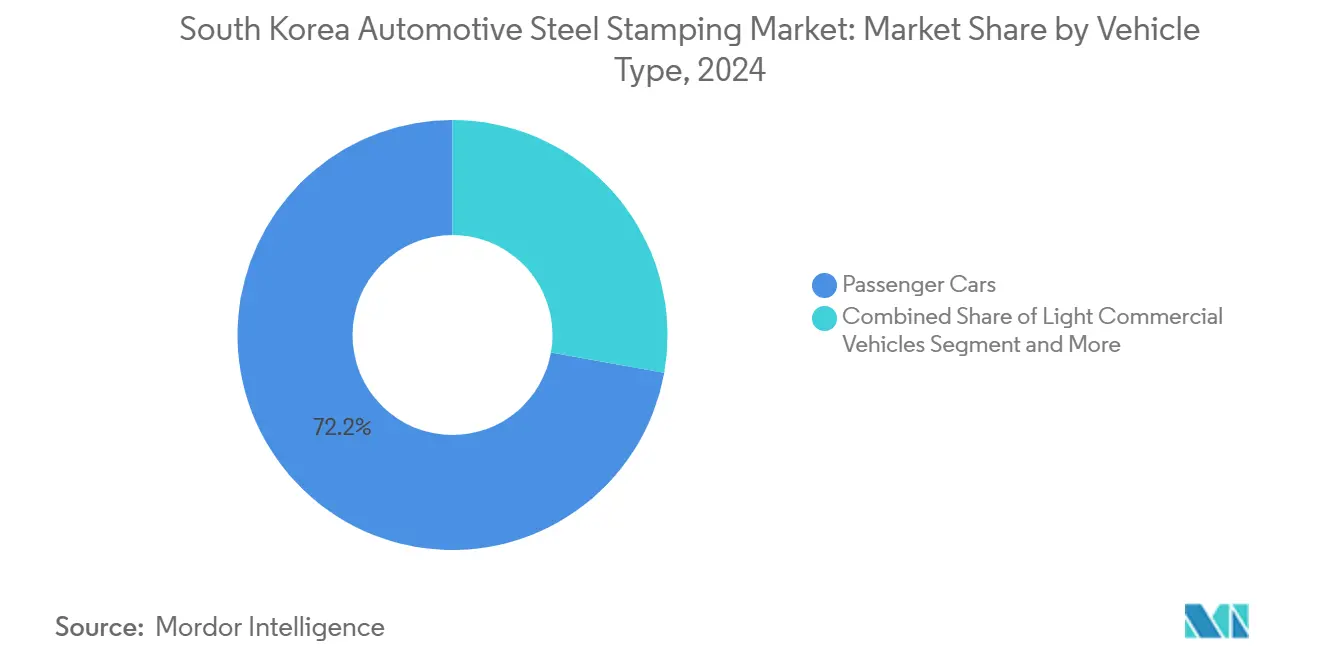

- By vehicle type, passenger cars held a 72.15% share of the South Korea automotive steel stamping market in 2024 and are advancing at a 5.13% CAGR over the forecast period.

- By propulsion, internal-combustion models commanded 78.33% of South Korea automotive steel stamping market size in 2024, whereas electric vehicles post a 6.73% CAGR outlook to 2030.

- By geography, the Seoul-Capital Area captured 30.51% revenue share in 2024; South-East Gyeongsang is set to grow the fastest at 4.96% CAGR through 2030.

South Korea Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight AHSS Demand to Meet CO₂/CAFE Norms | +1.2% | National; Seoul-Capital Area leads | Medium term (2-4 years) |

| Rapid Scale-up of EV Output and Battery Housings | +0.9% | South-East Gyeongsang and Central Clusters | Short term (≤ 2 years) |

| OEM Shift to Hot-Stamping for Crash Safety | +0.7% | National automotive corridors | Medium term (2-4 years) |

| Government “Future-Car” CAPEX Subsidies | +0.5% | Nationwide; boosted industrial zones | Long term (≥ 4 years) |

| Export-oriented Tier-1 Supply to ASEAN OEMs | +0.4% | Seoul-Capital and South-East export corridors | Medium term (2-4 years) |

| Digital-Twin Press-Shops that Cut Scrap | +0.3% | Early adopters in advanced plants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lightweight AHSS Demand Drives Regulatory Compliance

Corporate-average fuel-economy rules targeting fleet averages below 97 gCO₂/km push automakers toward third-generation AHSS grades that deliver 10% body-in-white mass savings without sacrificing crash performance [1]International Council on Clean Transportation, “South Korean Vehicle CO₂ Targets and Technology Pathways,” theicct.org. POSCO’s 1,500 MPa steels and Hyundai Steel’s HyECOsteel line illustrate how material innovation couples with stamping precision to secure both emissions compliance and structural integrity. OEM procurement teams now view lightweight stamping as a mandatory capability, reinforcing supplier investment in advanced die-design and simulation.

EV Production Scale-Up Transforms Component Architecture

Electric-vehicle assembly reached 268,785 units in 2023 and targets 4.83 million capacity by 2030, swapping 2,000 ICE parts for up to 800 EV-specific stampings centred on battery enclosures with tight tolerance and high energy-absorption needs [2]Hyundai Motor Group, “EV Production Strategy to 2030,” hyundaimotorgroup.com. Ulsan’s EV-only plant, on stream from late 2025, dedicates entire press lines to these functions, accelerating the shift of the South Korea automotive steel stamping market toward high-value, low-volume programs.

Hot-Stamping Adoption Enhances Crash Safety

B-pillars and door rings now require boron-steel hot-stamping that combines 22MnB5 chemistry with rapid quench to exceed 1,500 MPa tensile levels. Integrated simulation cuts part development from 18 to 12 months, tilting OEM sourcing toward suppliers with process depth across material, furnace, and tool optimization.

Government “Future-Car” Policy Accelerates Transformation

Cash grants up to 80% of project costs plus multiyear tax holidays lower payback hurdles for new hot-stamping and digitalized press-shops [3]Ministry of Economy & Finance, “Future-Car Support Measures,” chambers.com. Parallel green-steel pilots, although small today, signal long-term decarbonization funding that will ultimately influence buyer preference for low-emission stamped parts.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Tool-and-Die CAPEX, Long Payback | -0.8% | SMEs nationwide | Medium term (2-4 years) |

| Material Substitution by Aluminum and Plastics | -0.6% | Premium segments nationwide | Long term (≥ 4 years) |

| Shortage of Expert Die-Design Engineers | -0.4% | Advanced manufacturing regions | Long term (≥ 4 years) |

| Energy-Price Volatility on 24/7 Lines | -0.3% | Energy-intensive plants across the country | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High CAPEX Requirements Challenge Investment Economics

Major component programs can demand USD 10-15 million in tooling and 4-6-year paybacks, with hot-stamping lines doubling that outlay. Night-shift electricity tariffs partly relieve costs but complicate workforce scheduling.

Material Substitution Pressures Intensify

Gigacasting aluminum body sections, pioneered by global EV leaders, can replace 50-70% of stamped parts for specific models, prompting Korean stampers to push AHSS grades that meet weight and cost targets simultaneously.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Blanking Underpins Versatile Material Prep

Blanking held 38.91% of the South Korea automotive steel stamping market share in 2024, thanks to its universal role in sheet preparation, while flanging’s 5.85% CAGR to 2030 rides on EV battery housing edges that demand high sealing integrity. The South Korea automotive steel stamping market size, associated with blanking, therefore, remains the anchor revenue pool that funds broader technology upgrades. Suppliers refine servo-press controls for tighter dimensional tolerances, exploiting digital-twin feedback to minimize burr formation.

Flanging’s rise coincides with multi-step panel designs where battery packs interface with crash cages. Stampers invest in adaptive tooling that compensates for spring-back across mixed-material stack-ups. Embossing and coining niche applications cater to luxury interiors and sensor mounts, attracting premium pricing but limited volumes. Incremental forming, grouped under other technologies, shows promise for low-volume prototypes, yet requires software-heavy workflow integration that only tech-savvy firms can deliver.

By Process: Hot Stamping Dominates Safety-Critical Structures

Hot stamping delivered 46.25% of the 2024 South Korea automotive steel stamping market size, driven by OEM mandates for 1,500 MPa pillars and door rings. The South Korea automotive steel stamping market share of hot-stamped parts will edge higher as pedestrian-impact rules tighten. Iron-based blanks are heated above 900 °C, robotically transferred, pressed, and quenched in under 10 seconds, producing martensitic microstructures that slash weight while lifting energy absorption.

Roll forming’s 6.16% CAGR reflects flexible cross-section production from a single coil feed, supporting vehicle platform modularity. Conventional sheet-metal stamping survives in lower-stress panels yet faces margin erosion. Hybrid processes merging warm forming with partial heating emerge under other processes to create property gradients within a single component, balancing weight and local stiffness.

By Vehicle Type: Passenger Cars Drive Market Evolution

Passenger cars generated 72.15% of 2024 revenue, anchoring the South Korea automotive steel stamping market size with a 5.13% CAGR outlook that outpaces volume growth in the broader domestic vehicle parc. This dominance stems from dense model launches across compact and premium segments, each incorporating higher fractions of advanced high-strength steel panels and battery-ready floor assemblies that raise stamping content per unit. OEM styling refresh cycles averaging 4.5 years sustain tooling demand and feed continuous die-replacement contracts for leading press shops.

Light commercial vehicles follow as e-commerce growth sparks bespoke cargo-body designs requiring reinforced sidewalls and foldable step panels, though their share remains modest in the South Korea automotive steel stamping market hierarchy. Heavy trucks hold stable demand for chassis cross-members and cab rails, but face future electrification retrofits that will shift the mix toward battery-tray assemblies. Across segments, autonomous-driving sensor mounts and electromagnetic shielding brackets introduce new small-lot stampings, encouraging suppliers to install flexible, quick-change tooling and servo-press automation.

By Propulsion: ICE Dominance Faces EV Disruption

Internal-combustion platforms retained 78.33% of 2024 revenue, shielding near-term utilisation rates for legacy die-sets and giving the South Korea automotive steel stamping market size a dependable base while OEMs monetise sunk capital in engine-centric architectures. Typical ICE body structures employ more than 200 stamped components, including firewall reinforcements and exhaust-tunnel brackets, so even marginal production extensions translate into significant tonnage for steel service centres. Subsidy-fuelled fleet renewal programs that target outdated taxis and light trucks further stabilize cyclical order inflows.

Electric vehicles, though holding just 6.73% of 2024 revenue, post a 6.73% CAGR that will redefine press-shop workflows once dedicated Ulsan and Asan lines ramp in 2025-2026. Battery-housing decks, crash-guard cradles, and under-floor cooling plates together add 80-120 kg of high-precision stampings per car, demanding hot-stamping and roll-forming skills many ICE suppliers lack. Hybrid models act as transitional bridges, forcing plants to manage dual bill-of-material schedules and to schedule rapid die-changeovers that only servo-press platforms can accommodate.

Geography Analysis

Seoul-Capital Area retained 30.51% 2024 revenue on account of proximity to the headquarters of Hyundai, Kia and strategic Tier-1s. Design centres in the corridor favour agile suppliers that can machine prototype dies in days, then iterate via digital twins. Toolshops therefore cluster near academic partners whose metal-forming labs accelerate failure-mode analysis.

South-East Gyeongsang, anchored by Ulsan, posts the fastest 4.96% CAGR to 2030. An ecosystem of 300-plus auto suppliers generated USD 38 billion output in 2024, benefiting from port logistics that enable quick shipment of finished panels to ASEAN assembly plants. Local government tax offsets further pull new hot-stamping investment to the zone.

The central region supplies commercial-vehicle frames and service panels where cost efficiency overrules cutting-edge metallurgy. South-West Jeolla plays the export card, feeding Vietnam and Indonesia under duty-free regimes. Digital monitoring is shrinking the traditional penalty of geographic distance, allowing Gangwon and Jeju pilot plants to test low-carbon steel stamping powered by renewable energy.

Competitive Landscape

The South Korea automotive steel stamping market displays moderate consolidation. POSCO and Hyundai Steel exploit captive slab supply, integrated R&D, and customer financing to defend volume positions. Specialized players such as Gestamp Korea and Unipres Korea carve niches in battery-housing, aluminum-steel hybrid stampings, and digital-twin press shops that drive 90% scrap cuts. Capital thresholds exceeding USD 10 million per program discourage new entrants.

Strategic moves underscore diverging paths. POSCO pairs green-hydrogen steel with hot-stamping lines to offer low-carbon door rings to premium EV makers, while Hyundai Steel’s 2025 contract to supply GM Korea replaces China-sourced sheets, boosting local content. Gestamp is piloting servo-press retrofits that halve die-change time. Energy-price volatility, meanwhile, pressures smaller firms into night-only runs, pushing some into mergers or exits.

Government subsidies up to 80% of eligible CAPEX tilt the field toward domestic champions ready to file complex grant applications. Digitalization capability, not scale alone, now decides whether suppliers move up the value curve or stagnate as low-margin commodity panel vendors.

South Korea Automotive Steel Stamping Industry Leaders

POSCO

Hyundai Steel

Gestamp Korea

SeAH Steel

Dongkuk Steel Mill

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hyundai Steel to deliver 100,000 t of automotive steel sheets yearly to GM Korea after clearing quality certification, part of GM’s pivot away from China.

- November 2024: Hyundai Steel supplied hot-stamped high-strength cabin frames to Renault Korea Motors, extending its parts portfolio into safety-critical structures.

South Korea Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Electric Vehicle |

| Seoul-Capital Area |

| Central Region |

| South-East (Gyeongsang) |

| South-West (Jeolla) |

| Gangwon and Jeju |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric Vehicle | |

| By Geography | Seoul-Capital Area |

| Central Region | |

| South-East (Gyeongsang) | |

| South-West (Jeolla) | |

| Gangwon and Jeju |

Key Questions Answered in the Report

How big is the South Korea automotive steel stamping market in 2025?

The South Korea automotive steel stamping market size stands at USD 1.88 billion in 2025 and is projected to hit USD 2.33 billion by 2030.

What is the growth rate for automotive steel stamping in South Korea?

The market is forecast to expand at a 4.39% CAGR between 2025 and 2030, supported by EV component demand and government subsidies.

Which stamping process leads in South Korea?

Hot stamping holds 46.25% share due to its ability to produce ultra-high-strength safety parts exceeding 1,500 MPa.

Which region is expanding the fastest for stamping suppliers?

South-East Gyeongsang is expected to register a 4.96% CAGR through 2030 on the back of Ulsan’s EV-focused investments.

Page last updated on: