North America Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

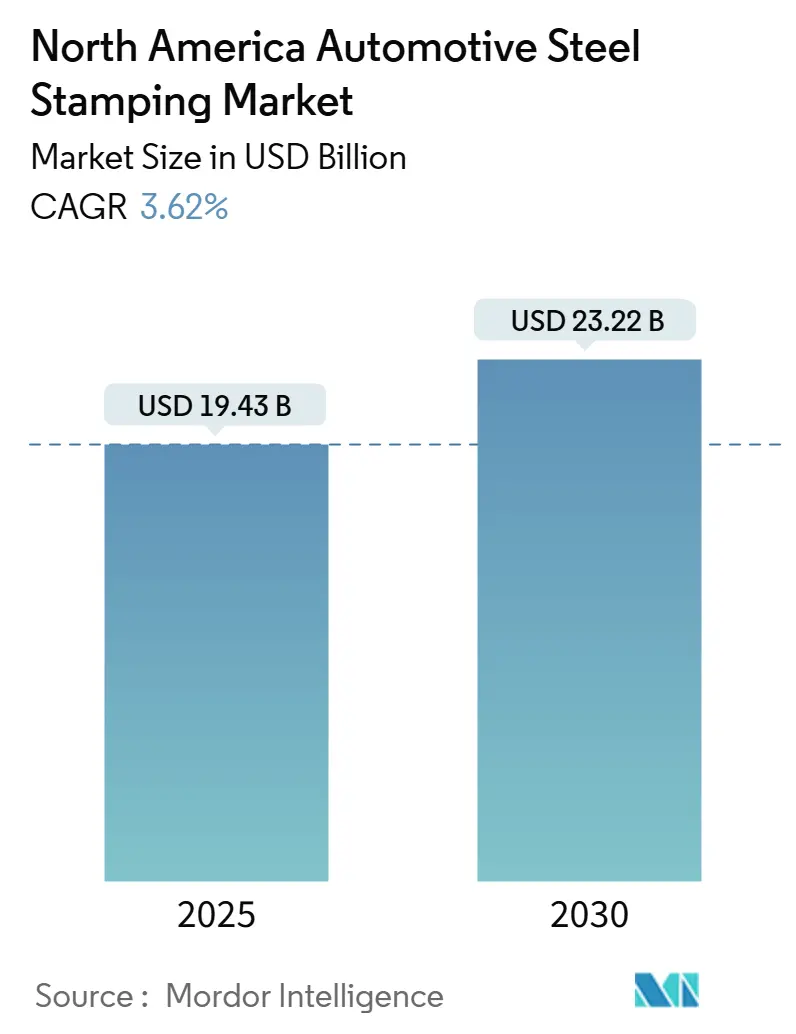

| Market Size (2025) | USD 19.43 Billion |

| Market Size (2030) | USD 23.22 Billion |

| Growth Rate (2025 - 2030) | 3.62% CAGR |

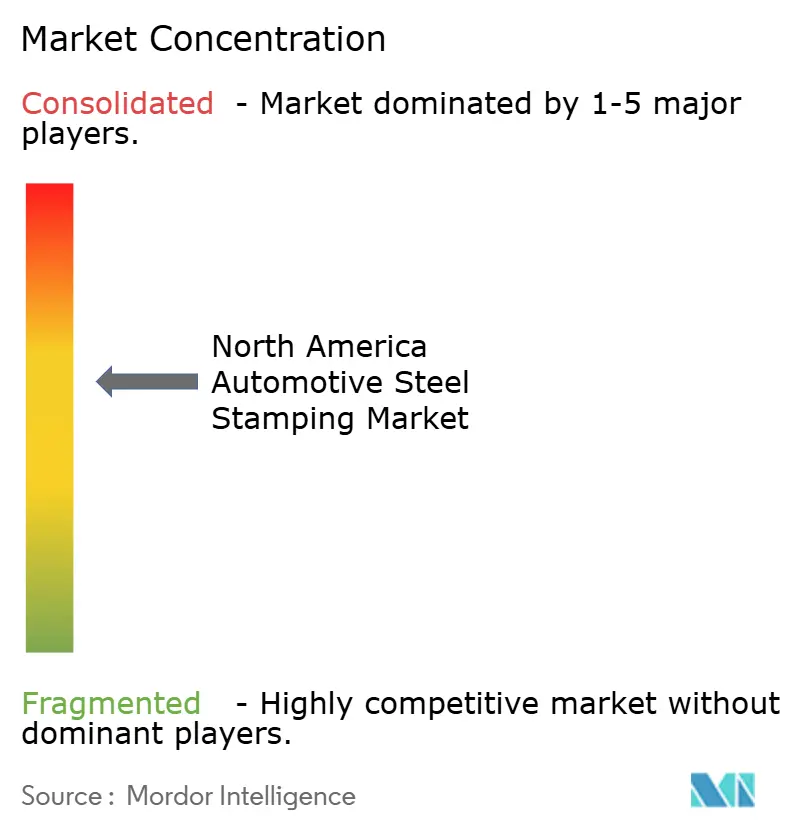

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Automotive Steel Stamping Market Analysis by Mordor Intelligence

The North America automotive steel stamping market reached USD 19.43 billion in 2025 and is projected to grow at a 3.62% CAGR, lifting the North America automotive steel stamping market size to USD 23.22 billion by 2030. Tighter USMCA regional-content rules, ongoing lightweighting programs, and automation upgrades support this measured expansion even as aluminum gigacasting presents competitive pressure. Steel keeps a leading 57% share of average vehicle construction because advanced high-strength grades can meet crash, cost, and sustainability targets more readily than alternative materials. Investment momentum is robust: new electric-arc furnaces, servo press lines, and integrated press shops shorten supply chains and reinforce the North America automotive steel stamping market against global volatility. Demand tailwinds strengthen further as on-shoring of battery-pack enclosures accelerates under Inflation Reduction Act content rules, giving regional suppliers a decisive cost-and-logistics edge.

Key Report Takeaways

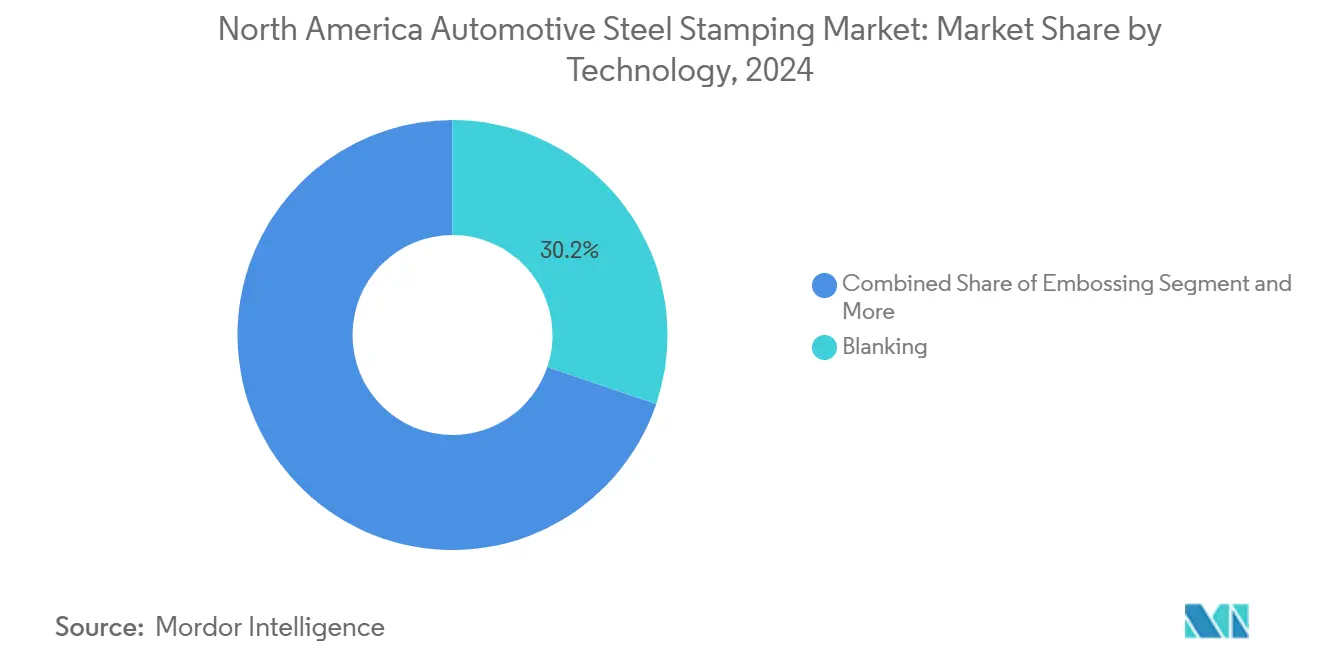

- By technology, blanking contributed 30.23% of the North America automotive steel stamping market size in 2024 and other technologies are projected to rise at a 5.07% CAGR to 2030.

- By process, sheet-metal forming held 35.12% of 2024 revenue, whereas hot stamping is set to post the fastest 8.04% CAGR over the forecast window.

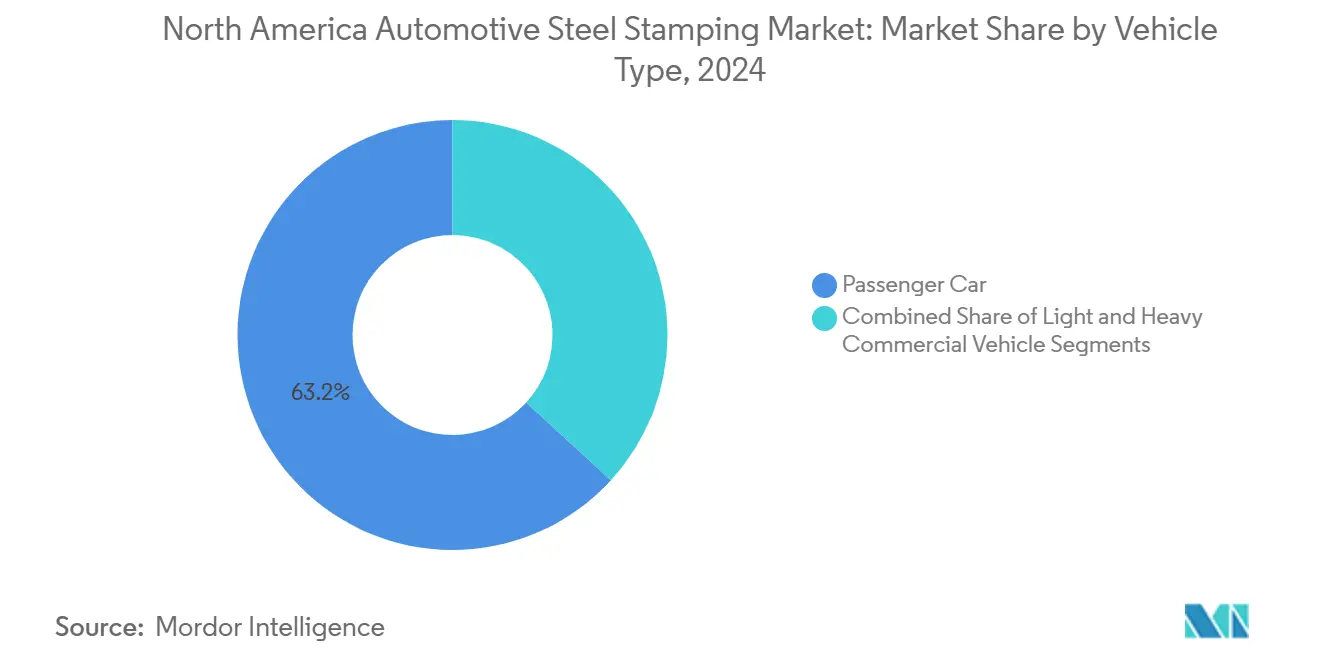

- By vehicle type, passenger cars accounted for 63.17% of 2024 value, yet light commercial vehicles will advance at a 5.03% CAGR to 2030.

- By propulsion, internal-combustion vehicles retained a 72.36% share in 2024, and electric vehicles will register the highest 14.18% CAGR through 2030.

- By geography, the United States commanded 68.42% of the North America automotive steel stamping market share in 2024, while Mexico is forecast to expand at a 4.53% CAGR through 2030.

North America Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound in North American Light-Vehicle Production | +0.8% | United States and Canada, spillover to Mexico | Short term (≤ 2 years) |

| OEM Demand for AHSS/UHSS Stampings | +1.2% | Global, with concentration in US and Mexico | Medium term (2-4 years) |

| USMCA Rules Favoring Local Suppliers | +0.9% | North America, particularly US-Mexico corridor | Long term (≥ 4 years) |

| Automation Reducing Stamping Costs | +0.4% | United States and Canada manufacturing hubs | Medium term (2-4 years) |

| On-Shoring for IRA Compliance | +0.6% | United States, early gains in Michigan, Ohio, Tennessee | Medium term (2-4 years) |

| EV Megastamping Demand Replacing Gigacasting | +0.3% | North America, concentrated in EV production centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in North-American Light-Vehicle Production Rebound Post-Pandemic

North American light vehicle production reached 15.7 million units in 2024, marking a recovery trajectory that directly correlates with stamping demand as each vehicle requires approximately 200-300 stamped components. The rebound accelerates through supply chain normalization and inventory restocking, with automakers like GM and Ford resuming full production schedules after pandemic-induced disruptions. Steel consumption in the automotive sector shows resilience, with Cleveland-Cliffs reporting 26% of steel sales directly to automotive markets in Q2 2025, highlighting the sector's recovery momentum. This production surge creates multiplier effects for stamping suppliers, as increased vehicle assembly drives proportional demand for body panels, structural components, and safety-critical parts. The recovery pattern suggests sustained growth through 2026, with projections indicating 16.1 million units annually, supporting the stamping industry's capacity utilization improvements.

OEM Lightweighting Push Spurring Demand for AHSS and UHSS Stampings

Corporate Average Fuel Economy (CAFE) standards mandate 2% annual increases for passenger cars through 2031, compelling automakers to adopt advanced materials that reduce vehicle weight while maintaining structural integrity. AHSS and UHSS enable weight reductions up to 25% in body structures compared to conventional steel, with tensile strengths reaching 1,500-2,000 MPa through hot stamping processes. ArcelorMittal's Multi Part Integration technology demonstrates cost advantages over aluminum die-casting while achieving similar weight savings, positioning steel stamping as the preferred solution for mass production vehicles. The lightweighting imperative intensifies with electric vehicle adoption, where every kilogram saved in body structure translates to extended battery range and reduced material costs. Advanced steel grades like Fortiform® enable cold stamping of ultra-high-strength components, expanding design flexibility while maintaining manufacturing efficiency.

Tighter USMCA Regional-Content Rules Favoring Local Steel Stampers

The USMCA's 75% regional value content requirement, recently elevated to 85% through executive order with plans for 90% by 2026, fundamentally reshapes automotive supply chains by mandating local sourcing[1]"Trump Raises USMCA Auto Content Rule to 85%," Mexico Business News, mexicobusiness.news.. Steel and aluminum procurement rules require 70% North American sourcing, creating competitive advantages for regional stamping suppliers while imposing 25% tariffs on non-compliant imports[2]"The United States-Mexico-Canada Agreement (USMCA)," ustr.gov.. This regulatory framework drives USD 34 billion in new automotive investments and 76,000 jobs over 5 years, with stamping operations benefiting from proximity requirements and supply chain localization mandates. Labor Value Content rules requiring 40-45% high-wage manufacturing further incentivize domestic stamping operations, as automakers seek compliant suppliers to avoid tariff penalties. The regulatory tightening creates barriers for Asian suppliers while expanding market opportunities for established North American stampers with existing OEM relationships.

Automation Investments Lowering Per-Part Cost in Stamping Presses

BMW's USD 200 million press shop investment in Spartanburg demonstrates the industry's commitment to automation, featuring servo technology and advanced robotics that improve part quality while reducing cycle times. Martinrea's acquisition of 3,000-ton and 1,600-ton presses with variable speed capabilities exemplifies how tier-1 suppliers leverage automation to enhance throughput and quality control[3]"Tier 1 masters massive stampings with 3,000-tonne press," The fabricator, thefabricator.com. . SIMPAC's CX Series stamping press, specifically engineered for electric vehicle applications, incorporates AI-driven quality control and predictive maintenance systems that reduce downtime and improve operational efficiency. These automation investments enable stampers to compete with low-cost regions while maintaining quality standards required for safety-critical automotive components. The technology adoption cycle accelerates as suppliers seek to offset labor cost increases and improve competitiveness against emerging manufacturing technologies like gigacasting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flat-Steel Price Volatility | -0.7% | United States and Canada, moderate impact in Mexico | Short term (≤ 2 years) |

| Slower BEV Adoption | -0.5% | North America, concentrated in premium EV segments | Medium term (2-4 years) |

| OEM Cost-Down Pressure on Tier-1s | -0.4% | United States and Canada, especially Tier-1 supplier base | Medium to long term (2–4+ yrs) |

| Substitution by Aluminum and Composites | -0.2% | Global, pronounced in lightweight and EV applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in North-American Flat-Steel Prices

Steel price volatility reached critical levels in 2024, with hot-rolled coil prices fluctuating between USD 800-1,000 per ton, creating margin pressure for stamping suppliers who typically operate on 3-6 month pricing contracts while facing immediate material cost changes. Trade case proceedings against coated steel imports from multiple countries introduce additional uncertainty, with potential duties affecting domestic pricing dynamics and supplier competitiveness. Raw material cost inflation, energy price fluctuations, and geopolitical tensions contribute to pricing instability, with steel representing 60-70% of stamping production costs. Stamping suppliers implement risk management strategies including long-term contracts, inventory optimization, and material substitution, yet price volatility remains a persistent challenge affecting profitability and investment planning. The volatility particularly impacts smaller suppliers lacking hedging capabilities and negotiating power with steel mills.

Slower-Than-Expected BEV Adoption Curbing Incremental Stamping Volumes

Battery electric vehicle penetration rates lag initial projections, with industry forecasts adjusting BEV market share to 20-30% by 2030 compared to earlier estimates of 40-50%, directly impacting incremental stamping demand for EV-specific components. Consumer resistance to higher EV prices, charging infrastructure limitations, and range anxiety contribute to adoption delays, with automakers like Ford reducing EV production plans and shifting focus to hybrid powertrains. The slower transition affects battery enclosure stamping demand, where each EV requires specialized structural components worth USD 500-800 per vehicle in stamping content. Magna's Q2 2024 results reflect this challenge, with lower-than-expected EV volumes impacting assembly operations and component demand. Stamping suppliers must balance capacity investments for EV components while maintaining ICE production capabilities during the extended transition period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Automation Drives Blanking Dominance

Blanking technology commands 30.23% market share in 2024, reflecting its fundamental role in creating initial workpieces for subsequent forming operations across all vehicle platforms. The segment's dominance stems from its versatility in processing both conventional and advanced high-strength steels, with modern blanking lines capable of handling material thicknesses from 0.5mm to 6mm while maintaining tight tolerances. Other technologies segment accelerates at 5.07% CAGR from 2025-2030, driven by innovations in coining, flanging, and specialized forming processes that enable complex geometries required for EV battery enclosures and structural components. Embossing operations gain traction for lightweighting applications, creating strategic stiffening patterns that reduce material usage while maintaining structural integrity.

Bending processes experience steady demand from chassis and suspension component production, while coining technology finds niche applications in precision components requiring exact dimensional control. The evolution of technology mix reflects automakers' shift toward integrated manufacturing approaches, where multiple forming operations combine within single press lines to reduce handling and improve quality consistency. Advanced simulation tools like ESI's BM-Stamp enable stampers to optimize process parameters and reduce trial-and-error development cycles, supporting the adoption of complex forming technologies across the industry.

By Process: Hot Stamping Revolutionizes Strength Requirements

Hot stamping technology surges at 8.04% CAGR from 2025-2030, transforming ultra-high-strength steel production through controlled heating and quenching processes that achieve tensile strengths exceeding 1,500 MPa. Sheet-metal forming maintains 35.12% market share in 2024, encompassing traditional deep drawing and progressive die operations that form complex body panels and structural components. The process segment's evolution reflects automakers' increasing adoption of tailored tempering techniques, where differential cooling creates varying strength zones within single components to optimize crash performance and weight reduction. AP&T's installation at Simwon's Texas facility demonstrates hot stamping's efficiency gains, achieving 15-20% output improvements compared to conventional forming methods.

Roll forming processes serve specialized applications in structural rails and reinforcement components, while metal fabrication encompasses secondary operations including welding, assembly, and finishing. The process landscape shifts toward integrated manufacturing cells that combine multiple operations, reducing material handling and improving quality control throughout the production sequence. Hot stamping's growth trajectory aligns with safety regulation requirements and lightweighting mandates, as press-hardened components enable 20-40% weight reduction in vehicle body structures while enhancing collision protection.

By Vehicle Type: Commercial Segments Drive Growth

Light commercial vehicles accelerate at 5.03% CAGR from 2025-2030, outpacing passenger cars' steady performance as e-commerce logistics and last-mile delivery demand surge across North America. Passenger cars maintain a 63.17% market share in 2024, reflecting their continued dominance in overall vehicle production volumes and stamping content per unit. The commercial vehicle segment benefits from Ford's USD 3 billion Super Duty expansion and growing demand for electric delivery vehicles that require specialized battery mounting structures and reinforced chassis components. Heavy commercial vehicles represent the smallest segment but show resilience through infrastructure spending and freight transportation growth, with Volvo's USD 700 million investment in Mexico highlighting international confidence in North American commercial vehicle markets.

The vehicle type segmentation reflects changing consumer preferences and regulatory influences, with CAFE standards driving lightweighting initiatives across all categories while safety regulations mandate stronger structural components. Commercial vehicle stamping requirements differ significantly from passenger cars, requiring thicker materials, larger press capacities, and specialized forming techniques for heavy-duty applications. The segment dynamics suggest sustained growth in commercial applications as supply chain regionalization and e-commerce expansion create long-term demand for specialized commercial vehicle platforms.

By Propulsion: EV Transition Accelerates Component Innovation

Electric vehicles surge at 14.18% CAGR from 2025-2030, driven by battery pack enclosure requirements and structural modifications needed for EV architecture integration. Internal combustion engines maintain 72.36% market share in 2024, reflecting the extended transition period and hybrid powertrain adoption that combines ICE and electric components within single vehicle platforms. The propulsion segmentation reveals fundamental shifts in stamping requirements, where EVs demand specialized battery protection structures, reinforced floor pans, and modified crash management systems that differ substantially from conventional ICE vehicles. Magna's OPTiForm™ Battery Enclosure demonstrates steel's advantages in EV applications, utilizing deep draw stamping to create single-component designs that enhance structural efficiency while reducing assembly complexity.

The propulsion mix evolution creates dual challenges for stampers, who must invest in EV-specific tooling while maintaining ICE production capabilities during the transition period. Battery electric vehicles require approximately 50% higher press-hardened steel content compared to conventional vehicles, creating opportunities for advanced forming processes and high-strength materials. Hybrid powertrains represent an intermediate segment requiring components for both propulsion systems, adding complexity to stamping operations while providing volume stability during the EV transition.

Geography Analysis

In 2024, the United States accounted for 68.42% of the North American automotive steel stamping market, supported by entrenched clusters in Michigan, Ohio, Tennessee, Alabama, and South Carolina. Cleveland-Cliffs’ vertically integrated model feeds these hubs with automotive-grade coil, reducing logistics and inventory buffers. OEM investments such as Ford’s USD 3 billion Super Duty expansion and BMW’s USD 200 million press shop buttress domestic demand. Inflation Reduction Act content credits additionally reward local battery-pack enclosure work, locking in supplier proximity advantages.

Mexico is forecast to post the fastest 4.53% CAGR to 2030. Hyundai Steel’s USD 5.8 billion electric-arc furnace complex, Stellantis’ USD 1.6 billion EV line, and Volvo’s USD 700 million assembly plant broaden material self-sufficiency and lift press-capacity utilization along the Bajío and Nuevo León corridors. Lower labor costs and USMCA tariff certainty reinforce Mexico’s attractiveness for export-oriented and domestic-market programs. Local steelmakers such as DeAcero and ArcelorMittal expand coil width and coating lines to match automotive spec requirements, shortening order cycles for nearby stampers.

Canada maintains a stable yet modest share, sustained by Honda’s CAD 15 billion (USD 11.1 billion) EV hub in Ontario and supplier co-location initiatives. Abundant hydroelectric power and low-carbon steel aspirations underpin green-steel pilot projects, while integrated stamping-and-assembly lines at Ford’s Oakville complex illustrate flexibility between ICE and EV volume mixes. Cross-border trade keeps roughly 55% of Canadian-built stampings in US final assemblies, reinforcing trilateral ecosystem interdependence.

Competitive Landscape

Competitive intensity is moderate. The top five suppliers—Cleveland-Cliffs, Magna, Gestamp, Martinrea, and American Axle—collectively held about 38% of 2024 revenue, leaving meaningful room for regional specialists. Vertical integration and scale underpin Cleveland-Cliffs’ margin resilience, while Magna leverages multi-process capability in battery enclosures and body-in-white modules. Gestamp and Martinrea emphasize servo-press automation and hot-stamp expertise to meet OEM lightweighting roadmaps. American Axle’s proposed Dowlais merger will deliver a USD 12 billion entity spanning driveline and advanced metal forming, aiming for procurement synergies and cross-selling.

Consolidation will likely continue as tier-1 suppliers absorb smaller shops to secure capacity and dilute overhead in an environment of OEM cost-down mandates. Simultaneously, composite producers such as the newly rebranded ANDRITZ Schuler highlight alternative pathways but still sell high-tonnage presses to steel stampers, indicating complementary rather than purely disruptive intent. Success factors increasingly revolve around digital quality analytics, regional footprint alignment with EV launch calendars, and the flexibility to shift tonnage between ICE and EV architectures without re-rigging entire production halls.

North America Automotive Steel Stamping Industry Leaders

-

Magna International Inc.

-

Gestamp Automoción S.A.

-

Martinrea International Inc.

-

Flex-N-Gate Corporation

-

Autokiniton US Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Cleveland-Cliffs reported record steel shipments of 4.3 million net tons with 26% of sales directly to automotive markets, demonstrating the integrated steel producer's dominant position in automotive stamping supply chains while achieving USD 4.9 billion in quarterly revenues.

- March 2025: Hyundai Steel announced USD 5.8 billion investment in Louisiana for an Electric Arc Furnace-based integrated steel mill producing 2.7 million metric tons of automotive steel plates annually by 2029, supporting regional stamping operations with enhanced material supply.

- June 2024: BMW Manufacturing opened its first press shop in North America at Spartanburg, South Carolina, investing over USD 200 million to stamp sheet metal parts for BMW X3 with capacity for 10,000 parts daily using advanced servo technology .

North America Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet-Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Car |

| Light Commercial Vehicle |

| Heavy Commercial Vehicle |

| Internal Combustion Engine (ICE) |

| Electric Vehicle (EV) |

| United States |

| Canada |

| Mexico |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet-Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Car |

| Light Commercial Vehicle | |

| Heavy Commercial Vehicle | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Electric Vehicle (EV) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America automotive steel stamping market in 2025?

It is valued at USD 19.43 billion and is set to reach USD 23.22 billion by 2030 at a 3.62% CAGR.

Which stamping process is growing fastest in North America?

Hot stamping is projected to expand at an 8.04% CAGR through 2030 because press-hardened steels meet rising crash and lightweighting standards.

Why do USMCA rules matter for regional stamping suppliers?

Content thresholds of 85% in 2025, moving to 90% in 2026, incentivize automakers to source 70% of steel locally, securing contracts for North American press shops.

What impact does EV production have on steel stampings?

Each battery electric vehicle requires specialized enclosures and reinforced floor structures, driving a 14.18% CAGR for EV-related stamping demand.

Which country is the fastest-growing stamping base in North America?

Mexico is forecast to record a 4.53% CAGR to 2030, supported by USD 5.8 billion in new steel capacity and multiple OEM EV programs.

How concentrated is supplier power in this market?

The market shows moderate concentration, with major OEMs and Tier-1 suppliers holding significant share alongside a fragmented base of independent stampers.

Page last updated on: