Europe Automotive Steel Stamping Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

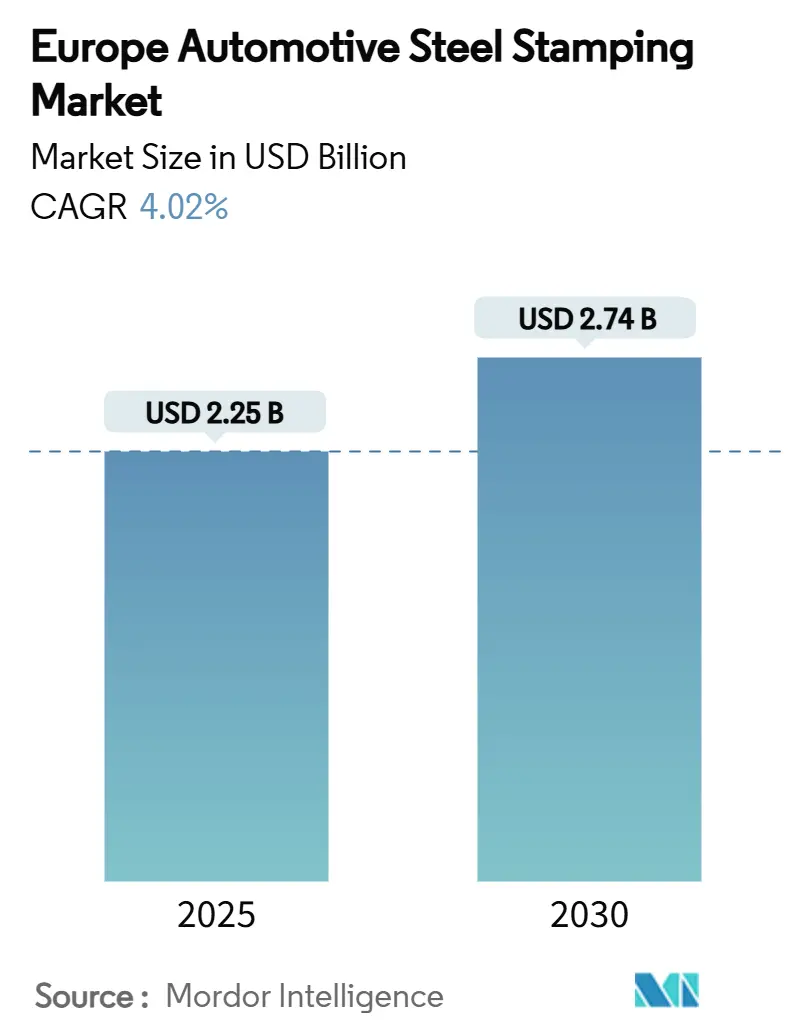

| Market Size (2025) | USD 2.25 Billion |

| Market Size (2030) | USD 2.74 Billion |

| Growth Rate (2025 - 2030) | 4.02% CAGR |

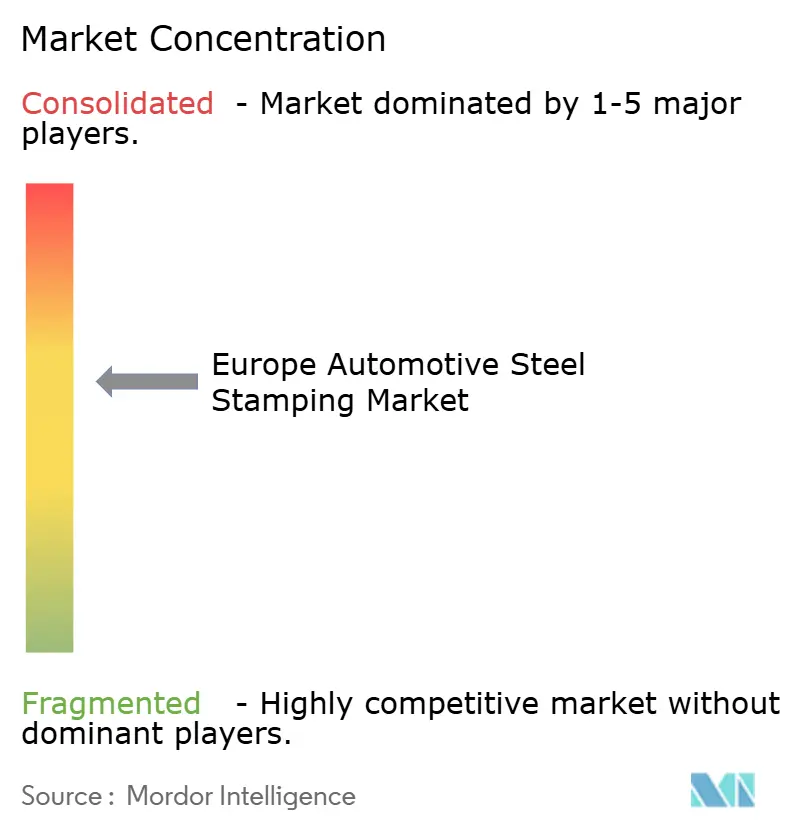

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Steel Stamping Market Analysis by Mordor Intelligence

The Europe automotive steel stamping market size is estimated at USD 2.25 billion in 2025 and is forecast to reach USD 2.74 billion by 2030, advancing at a 4.02% CAGR. The incremental value comes from steady passenger-car demand, accelerating electric-vehicle adoption, and the ongoing recovery of European manufacturing capacity. Cost-effective steel continues to hold share against aluminum because stamping suppliers adopt servo presses, laser blanking, and energy-saving production cells. OEM investments in in-house press shops, such as BMW’s USD 200 million outlay, signal a long-term commitment to local supply resilience [1]“BMW Invests in New Press Shop to Secure Body-in-White Supply,” BMW Group, bmwgroup.com. Tight EU carbon rules, wider use of ultra-high-strength grades, and collaboration between steelmakers and Tier-1s sustain component innovation even while energy prices and flat-steel volatility weigh on margins. These cross-currents explain the measured yet durable expansion path of the Europe automotive steel stamping market.

Key Report Takeaways

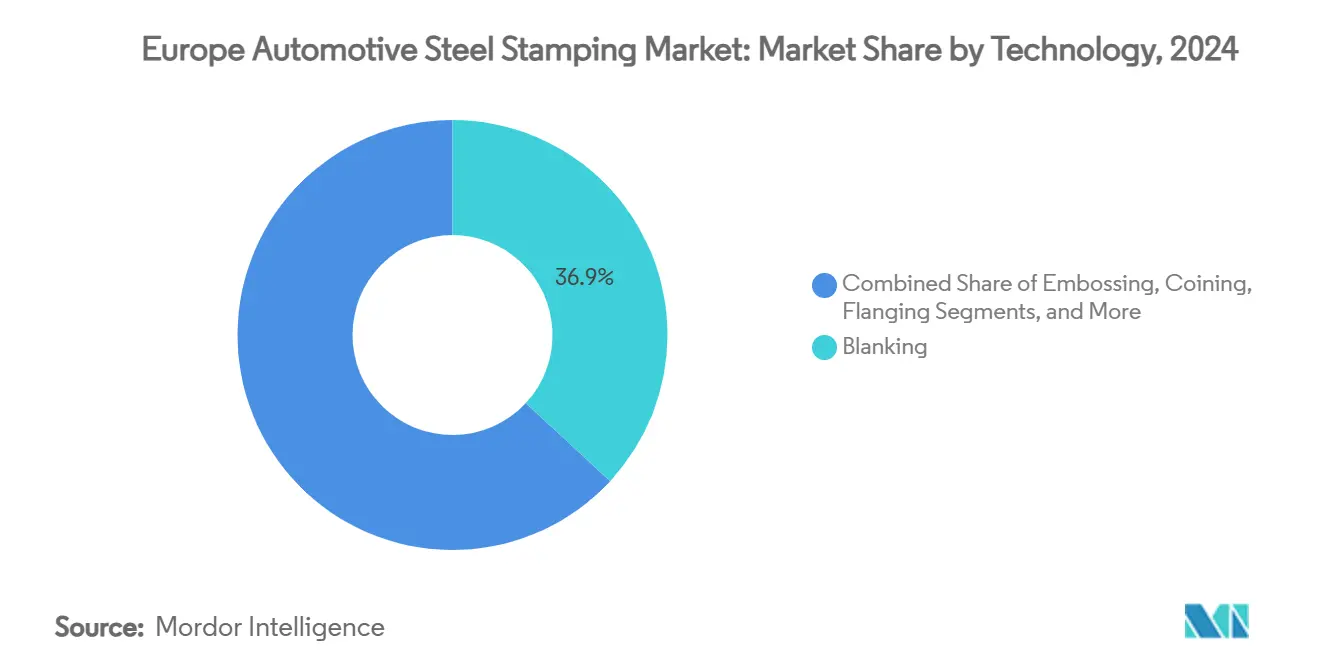

- By technology, blanking led with 36.85% of Europe automotive steel stamping market share in 2024, while its 4.45% CAGR keeps it the fastest-growing technology through 2030.

- By process, roll forming held 33.26% share of the Europe automotive steel stamping market size in 2024, and hot stamping is projected to expand at a 5.34% CAGR to 2030.

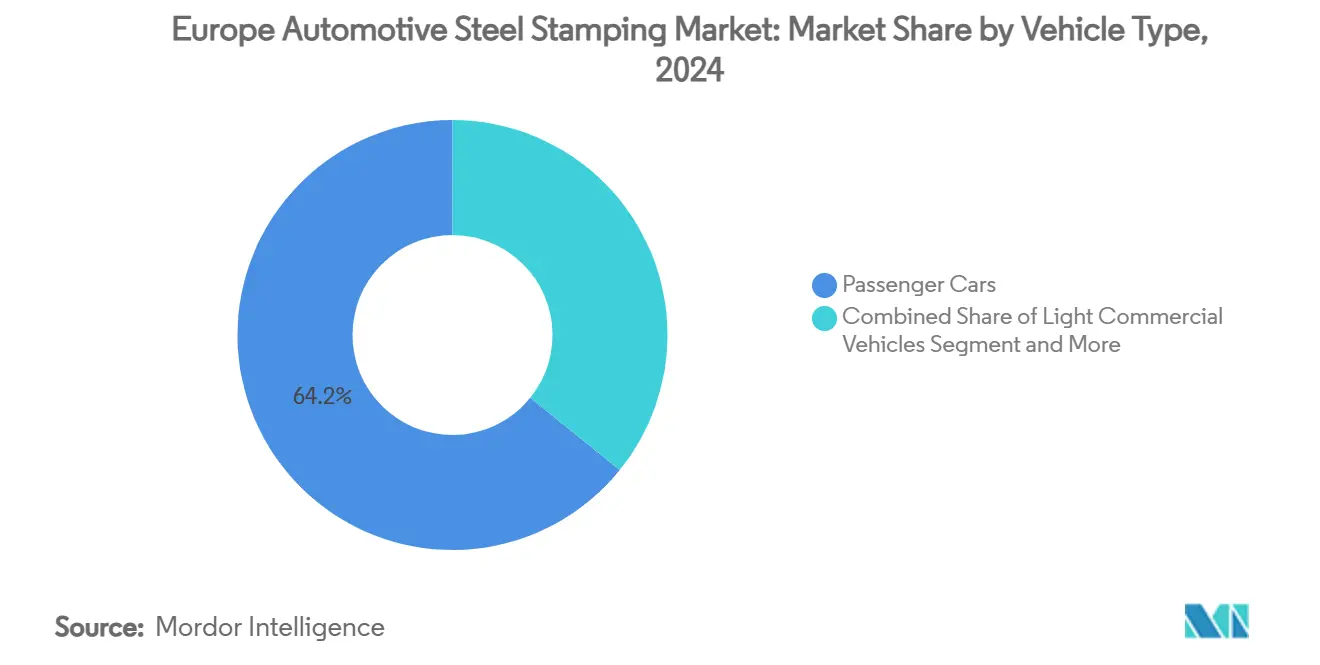

- By vehicle type, passenger cars captured 64.15% of Europe automotive steel stamping market size in 2024, and will also post the highest 4.77% CAGR through 2030.

- By propulsion, internal-combustion models retained 74.82% share in 2024, yet electric propulsion registers the sharpest growth at 6.04% through 2030.

- By country, Germany accounted for 29.44% of Europe automotive steel stamping market share in 2024, whereas Poland recorded the quickest 5.68% CAGR over the forecast period.

Europe Automotive Steel Stamping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Structural Part Demand Surge | +1.2% | Germany, Poland, Sweden | Long term (≥ 4 years) |

| EU CO₂ Norms Driving Lightweighting | +0.8% | Germany, France | Medium term (2-4 years) |

| UHSS Use Enabling Thinner Gauges | +0.7% | Premium OEM hubs | Long term (≥ 4 years) |

| EU Passenger-Car Output Recovery | +0.6% | Italy, Spain, the Czech Republic | Short term (≤ 2 years) |

| Servo-Press & Laser-Blanking Adoption | +0.5% | Western and Eastern Europe | Medium term (2-4 years) |

| OEM–Tier-1 In-House Stamping JVs | +0.4% | Germany, UK, France | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging EV-Specific Structural Part Demand

Pure-battery platforms feature long floor pans, giga-press panel concepts, and multimetal hybrids that demand precision hot stamping. Gestamp already attributes 20% of its European revenue to EV programs, validating a shift in order books toward battery protection systems and under-body cross-members [2]“Annual Report 2024,” Gestamp, gestamp.com. Grades exceeding 2,000 MPa tensile strength are now routine in critical bodies-in-white. High complexity raises qualification barriers, so larger suppliers consolidate share, and the Europe automotive steel stamping market benefits from technology-driven pricing power.

EU CO₂-Emission Norms Pressuring OEM Lightweighting

Stricter fleet-average carbon caps oblige automakers to shave weight without sacrificing crash integrity. Advanced high-strength grades let press shops cut sheet gauges by up to 20% while preserving stiffness, so the Europe automotive steel stamping market becomes an enabler of regulatory compliance. Electric cars paradoxically lift steel tonnage per unit because battery modules need robust impact cages. Steelmakers such as ArcelorMittal partner with specialized stampers to co-engineer battery enclosures that beat aluminum on cost and reparability [3]“Steel Battery Enclosures for Electric Vehicles,” ArcelorMittal, arcelormittal.com. Hydrogen-enabled direct-reduction investments by ThyssenKrupp and peers ensure future supplies of low-carbon feedstock, which supports OEM sustainability pledges.

Uptake of Ultra-High-Strength Steels Enabling Thinner Gauges

Fortiform and similar UHSS series generate 40% weight savings against legacy mild grades. Processing them demands tighter temperature windows and higher forming speeds, investments that favor established Tier-1s. Kirchhoff’s trials with Fortiform show crack-free cold stamping of 1,200 MPa panels, opening cost-efficient options beyond hot forming. Such successes reinforce the premium positioning of the Europe automotive steel stamping market in advanced materials.

Recovery of EU Passenger-Car Production Post-COVID

Vehicle assemblies rebounded through 2024 as semiconductor allocation improved and order backlogs cleared. EUROFER reported an 11.2% jump in new registrations, which translated into fuller press-shop utilization. Volume normalization lifts margins because overhead absorption improves, yet the rebound remains uneven across regions. Eastern sites in Slovakia and Poland run near capacity owing to near-shoring, whereas some German plants still sit below pre-pandemic peaks. This patchwork recovery urges suppliers to rebalance footprints while maintaining European automotive steel stamping market coverage.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex and Energy Costs in EU Plants | -0.9% | Germany, Western Europe | Short term (≤ 2 years) |

| Volatility in Flat-Steel Prices | -0.6% | EU suppliers | Short term (≤ 2 years) |

| Skilled-Labor Shortages in Western Europe | -0.5% | Germany, France, UK | Medium term (2-4 years) |

| Competition from Aluminum and Composites | -0.4% | Premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capex and Energy Costs in EU Plants

Electricity can absorb 40% of the operating expenditure at a press shop. Under the EU Emissions Trading Scheme, each megawatt-hour faces an extra carbon levy, inflating cash costs versus Asian or American peers. ThyssenKrupp’s restructuring targets EUR 150 million in annual savings, reflecting how producers safeguard competitiveness within the Europe automotive steel stamping market.

Volatility in Flat-Steel Prices

Geopolitical turmoil and freight disruptions widened coil price swings, yet many Tier-1s sign fixed-price agreements with carmakers. Without hedging, margin erosion ensues when hot-rolled indexes spike. Liquidity strains hinder smaller press shops from investing in new servo lines, delaying modernization within the Europe automotive steel stamping market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Versatile Blanking Sustains Leadership

Blanking generated the highest 36.85% share of Europe automotive steel stamping market size in 2024, thanks to its foundational role across models and materials. Demand remains buoyant because both compact urban EVs and commercial vans rely on precision blanks for door outers, structural rails, and battery enclosures. Recently introduced fiber-laser cells shorten changeovers from hours to minutes, letting suppliers address growing design variability with minimal downtime. The process also yields cleaner cut edges, which reduce downstream cracking on ultra-high-strength grades, and this advantage underpins the 4.45% CAGR projected through 2030. Over the period, capacity additions cluster in Poland, Hungary, and Spain, where lower utility tariffs and investment incentives enhance cost competitiveness for the Europe automotive steel stamping market.

Laser blanking’s tooling-free paradigm encourages prototype iterations, suiting premium OEMs that continually refresh trims. Concurrently, high-speed mechanical blankers serve volume ICE models, so technology choice varies by program size. Embossing and coining remain niche, aimed at aesthetic trims and accurate clearance parts. Flanging continues to support door arch reinforcements and hatch openings but faces slower growth because giga-castings shrink part counts per car. Bending stations evolve toward all-electric actuation that aligns with plant-wide carbon reduction targets. Collectively, the breadth of blanking applications cements its prime position in the Europe automotive steel stamping market.

By Process: Hot Stamping Surges on Safety Needs

Roll forming controlled 33.26% of Europe automotive steel stamping market share in 2024 due to its proven economics for long roof bows, rails, and rocker beams. Yet the safety agenda pushes OEMs to specify 1,500 MPa martensitic parts for side-impact zones. Hot stamping is uniquely capable of forming complex shapes with such strength, explaining its fastest 5.34% CAGR to 2030. Installations of PHS lines equipped with quench dies concentrate in Germany and Sweden, where premium SUVs require stringent crash modules. Process integrators report that tailored-tempered panels now appear in mass-market hatchbacks, indicating trickle-down adoption.

Sheet-metal forming still handles multi-stage draws for large body panels, but servo presses raise stroke rates by 20% and cut energy per hit. Metal fabrication tasks—spot welding, clinching, riveting—move closer to presses, promoting cell-based manufacturing with reduced logistical overhead. Other specialized techniques emerge for EV battery trays, such as press-hardening of roll-cladded steel-aluminum sandwiches, expanding the capability set of the Europe automotive steel stamping market. Suppliers that execute cross-process flexibility gain scheduling leverage and higher plant utilization.

By Vehicle Type: Passenger Cars Retain Scale Advantage

Passenger models delivered 64.15% of Europe automotive steel stamping market size in 2024 and will rise at a moderate 4.77% CAGR as order recovery stabilizes across the region. Hatchbacks and compact SUVs dominate die schedules because affordability matters amid consumer inflation. Plant refurbishments target cycle-time gains to meet OEM take-rate spikes for panoramic roofs and ADAS sensor brackets, both of which require extra stamped reinforcements. Despite the volume stability, OEMs still demand piece-price reductions, compelling stampers to extract cost through scrap minimization and flexible die standards.

Electric vans and last-mile delivery chassis drive the commercial segment, prompting new die sets for heavy-gauge floor members. Unibody LCVs share press lines with passenger vehicles, allowing balanced shift loading. Heavy-duty truck frames, while lower in unit count, attract dedicated high-tonnage presses capable of 20 mm thickness. As freight electrification broadens, heavy vehicle builders incorporate structural battery housings that mimic passenger-car safety cages, expanding addressable tonnage for the Europe automotive steel stamping market. Suppliers with multi-press portfolios can switch between these categories with limited retooling.

By Propulsion: ICE Dominates, EVs Accelerate

Internal-combustion engine (ICE) vehicles retained the highest 74.82% share of Europe automotive steel stamping market size in 2024, furnishing the core volume that keeps press-shop utilization high across the region. Stamping houses continue to supply engine cradles, exhaust shields, and fuel-system brackets in large lots, enabling efficient amortization of legacy tooling while incremental servo-press upgrades squeeze scrap rates. Battery-electric and plug-in hybrid (BEV + PHEV) programs, though smaller in absolute tonnage, introduce new content such as multi-layer battery trays and reinforced under-body cross-members that demand ultra-high-strength grades. Stampers therefore allocate hot-forming lines to EV programs during off-peak ICE cycles, balancing takt times across mixed-propulsion order books and protecting margins in a price-sensitive environment.

EV platforms deliver the segment’s fastest 6.04% CAGR through 2030, reflecting EU zero-emission targets and OEM model launches that collectively lift advanced-steel demand even as total part counts per vehicle fall. Each electric SUV contains 40–50% more high-strength steel than its ICE equivalent once pack protection and crash-energy paths are included, offsetting weight lost to aluminum closures. Europe's automotive steel stamping market share for EV applications consequently rises year over year, pulling servo-press, laser-blanking, and hot-stamping investments toward Poland, Hungary, and Sweden, where OEM gigafactories cluster. Continuous collaboration with steelmakers on fire-resistant coatings and thermally conductive sandwich grades further deepens value addition, positioning established Tier-1s to capture the propulsion shift without sacrificing ICE cash flows.

Geography Analysis

Germany held 29.44% of Europe automotive steel stamping market size in 2024 because of its dense cluster of press-shop integrators, technology institutes, and high-end vehicle plants. The region benefits from co-location with steel giants capable of supplying AHSS coils within hours. Yet rising electricity prices create urgency to adopt regenerative drive systems on presses. Firms partner with municipal utilities on cogeneration schemes to lower energy bills and shrink Scope 2 emissions. The workforce challenge remains acute, prompting dual-education programs that combine die-design coursework with on-the-job apprenticeships, thereby safeguarding knowledge transfer in the Europe automotive steel stamping market.

Poland enjoys the highest 5.68% CAGR as Western OEMs place engine-housing, side-rail, and closure-panel production in new greenfield facilities. Investors cite lower wages, available industrial land, and EU structural funds as compelling. Domestic suppliers upgrade press sizes to 2,000 tons to service SUV floor assemblies previously shipped from Germany. Universities expand metallurgy and robotics courses, ensuring a steady technician pipeline. Logistics links via Baltic ports streamline coil inflows and panel exports, reinforcing Poland’s role inside the Europe automotive steel stamping market.

France, Spain, and Italy maintain strong stamping demand tied to Stellantis and Renault footprints. Local subsidy schemes accelerate EV adoption, leading to in-house battery-tray stamping lines inside vehicle plants. Spain’s Valencia hub converts older presses to servo drives using retrofit kits that cut energy 30%. Italy leverages specialist toolmakers around Turin to supply dies for complex hot-formed pillars. The UK focuses on premium brands; Jaguar Land Rover’s shift to aluminum closures moderates steel tonnage yet new Range Rover platforms still specify high-strength side beams. Sweden and Czech Republic pursue sustainability branding and near-shore reliability, supporting export volumes to neighboring markets. Collectively, these sub-regions contribute stability and localized innovation to the Europe automotive steel stamping market.

Competitive Landscape

The competitive field shows moderate concentration: Gestamp, Benteler, Magna, Kirchhoff, and voestalpine dominate safety-critical stampings and advanced hot-forming modules. Market leadership stems from in-house die design, dedicated material labs, and long-term alliances with ArcelorMittal, SSAB, and ThyssenKrupp for exclusive steel grades. Gestamp booked EUR 12.27 billion in 2024 revenue, with 20% tied to EV content, underscoring scale advantages in the Europe automotive steel stamping market. Benteler adds value through tube-integrated floor systems that combine roll forming and stamping, lowering vehicle pack height.

Strategic moves revolve around sustainability. Gestamp pilots low-emission coil supply chains using ArcelorMittal’s scrap-to-steel XCarb route. Gedia links with Salzgitter on hydrogen-reduced slabs for side-impact beams. Such collaborations let Tier-1s offer OEMs carbon-footprint certificates for each part, a rising tender criterion. Technology investments include servo-press islands that halve takt time and predictive-maintenance suites that feed real-time sensor data to AI dashboards. Suppliers also court startups like Fisker and Nio to secure early-stage EV contracts, diversifying customer portfolios within the Europe automotive steel stamping market.

Barriers to entry remain high. A modern hot-stamping line costs USD 30 million and requires complex quench die know-how. Quality traceability standards such as IATF 16949 and strict OEM audit protocols deter smaller fabricators. Yet niche specialists prosper in prototyping and short-run luxury work where agility trumps scale. Robotics integrators and software firms create ecosystem competition by offering automated press-room modules, but established Tier-1s often absorb these players to internalize intellectual property. Consequently, the Europe automotive steel stamping market sustains a balanced rivalry that encourages continual capability upgrades without collapsing into price wars.

Europe Automotive Steel Stamping Industry Leaders

Gestamp Automoción S.A.

Benteler International AG

Magna International Inc. (Cosma)

Kirchhoff Automotive GmbH

CIE Automotive S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SEYI-Europe announced it will display a new servo press suited for high-strength steel and aluminum at LAMIERA 2025 in Milan, featuring an in-house drive motor for energy-efficient automotive component production.

- July 2023: ArcelorMittal Europe – Flat Products signed an agreement with Gestamp to recycle stamping scrap as raw material for XCarb recycled-content coils, strengthening circular-economy supply within automotive stamping.

Europe Automotive Steel Stamping Market Report Scope

| Blanking |

| Embossing |

| Coining |

| Flanging |

| Bending |

| Other Technologies |

| Roll Forming |

| Hot Stamping |

| Sheet-Metal Forming |

| Metal Fabrication |

| Other Processes |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Internal-Combustion Engine (ICE) |

| Electric Vehicles (BEV + PHEV) |

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Poland |

| Sweden |

| Czech Republic |

| Rest of Europe |

| By Technology | Blanking |

| Embossing | |

| Coining | |

| Flanging | |

| Bending | |

| Other Technologies | |

| By Process | Roll Forming |

| Hot Stamping | |

| Sheet-Metal Forming | |

| Metal Fabrication | |

| Other Processes | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| By Propulsion | Internal-Combustion Engine (ICE) |

| Electric Vehicles (BEV + PHEV) | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Poland | |

| Sweden | |

| Czech Republic | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the Europe automotive steel stamping market?

The market stood at USD 2.16 billion in 2024 and is projected to reach USD 2.74 billion by 2030.

How fast is the market expected to grow over the next five years?

It is set to expand at a 4.02% CAGR between 2025 and 2030, supported by rising EV content and regulatory pressures.

Which country is the fastest-growing stamping hub in Europe?

Poland posts the quickest 5.68% CAGR through 2030, driven by near-shoring and greenfield investments.

Why does steel remain competitive against aluminum for EVs?

Battery packs need strong, cost-efficient protection, and ultra-high-strength steel offers the required crash resistance at a lower cost than aluminum.

Page last updated on: