Emerging Architectures Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.11 Billion |

| Market Size (2031) | USD 10.39 Billion |

| Growth Rate (2026 - 2031) | 27.28% CAGR |

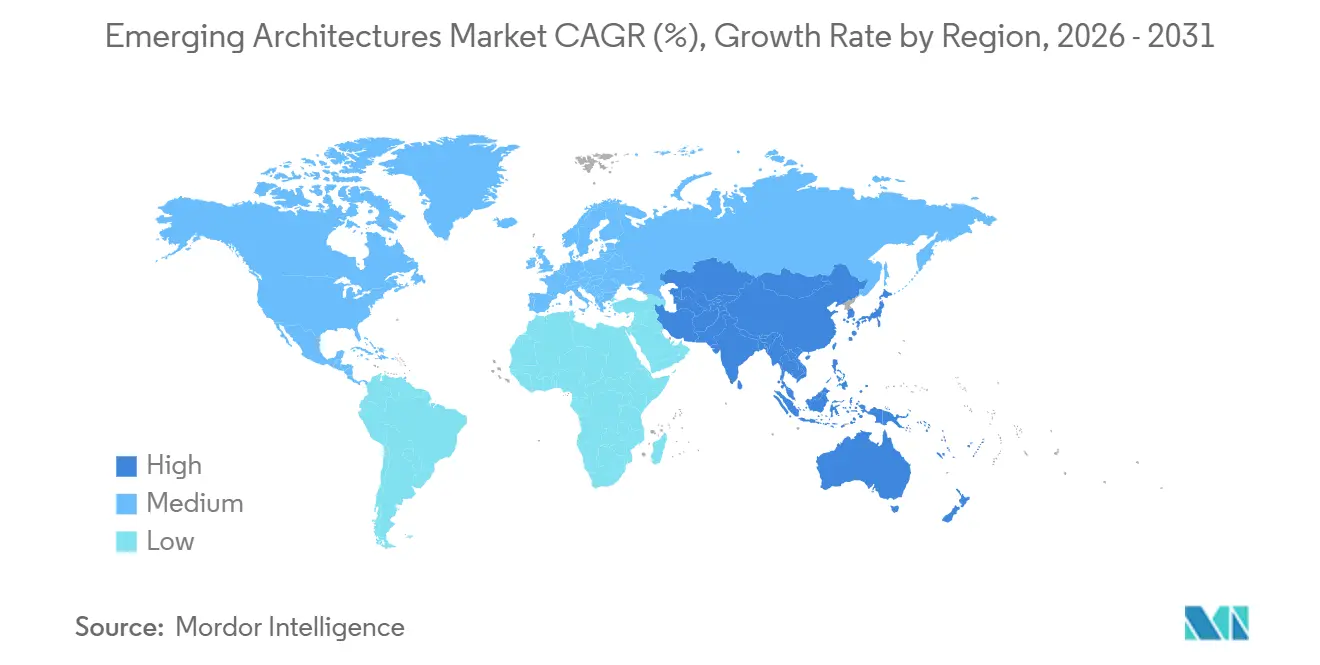

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

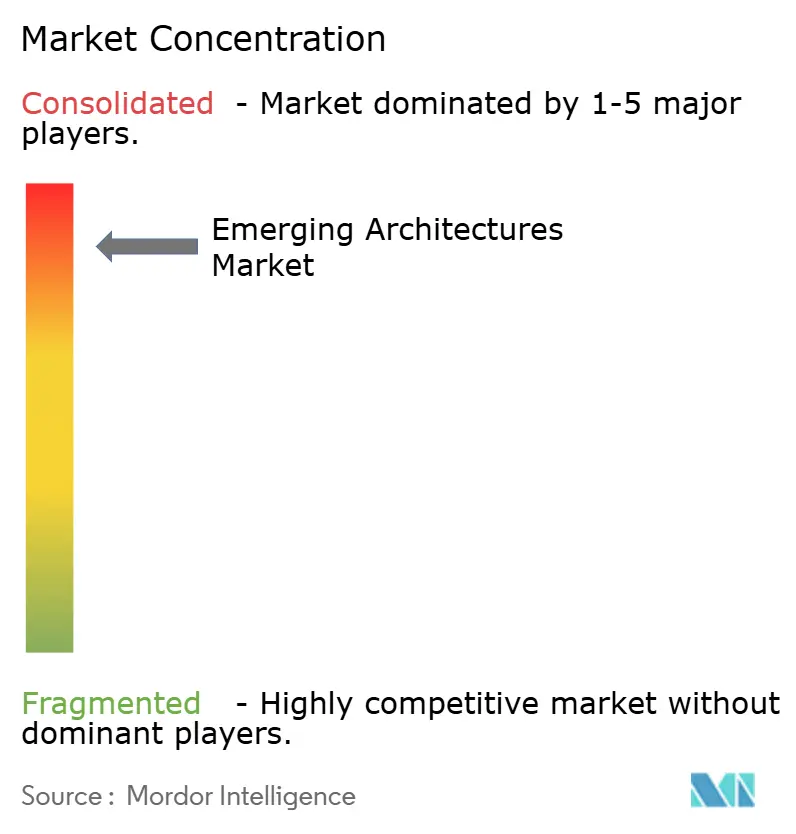

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Emerging Architectures Market Analysis by Mordor Intelligence

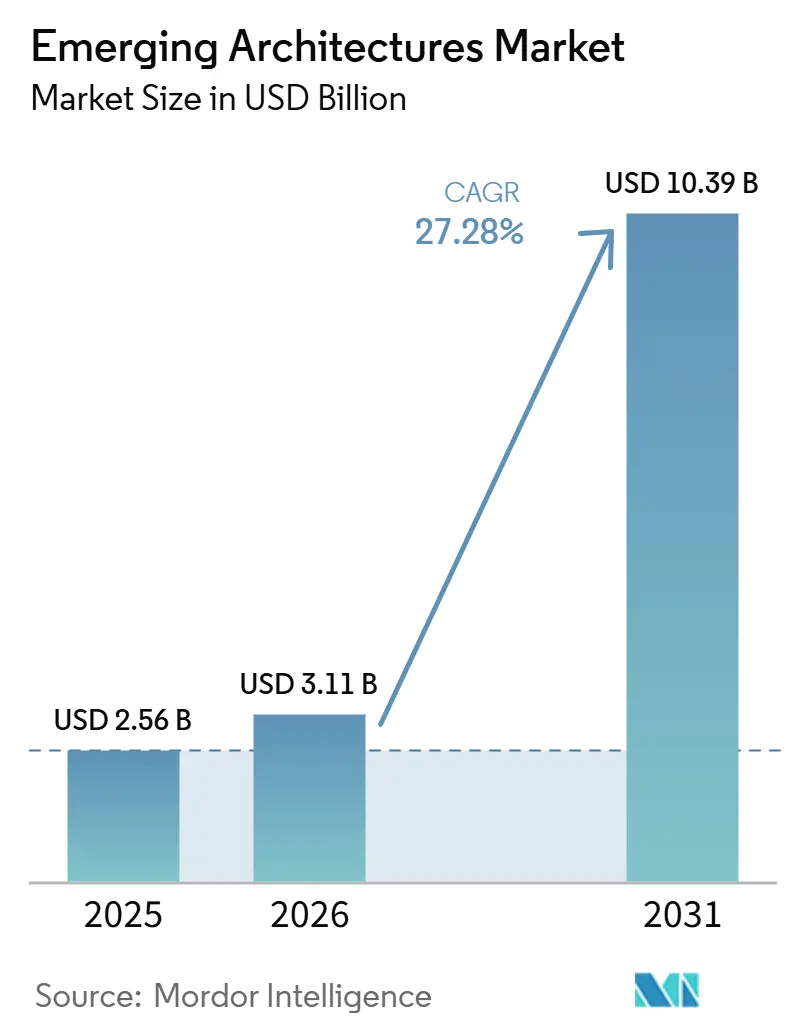

The Emerging architectures market size is projected to be USD 2.56 billion in 2025, USD 3.11 billion in 2026, and reach USD 10.39 billion by 2031, growing at a CAGR of 27.28% from 2026 to 2031. The Emerging architectures market is being shaped by a deeper shift in how memory and compute are linked inside AI systems, with silicon interposers, through-silicon vias, and heterogeneous die stacking moving into the core design path for both data center and edge compute platforms. The pace of product migration from older HBM generations to HBM3E and then HBM4 has shortened platform cycles and kept qualification pressure high across suppliers, packaging partners, and large customers. The emerging architectures market also remains concentrated around a narrow production base, which gives advanced packaging availability and supplier execution a direct influence on delivery schedules and system costs. Export controls and regional supply chain policies are widening the difference between where top-tier HBM can be produced, where it can be packaged, and where it can be shipped. That leaves the emerging architectures market with strong expansion potential in AI training, AI inference, and custom silicon deployments, while still carrying meaningful constraints around capacity, thermal management, and trade policy.

Key Report Takeaways

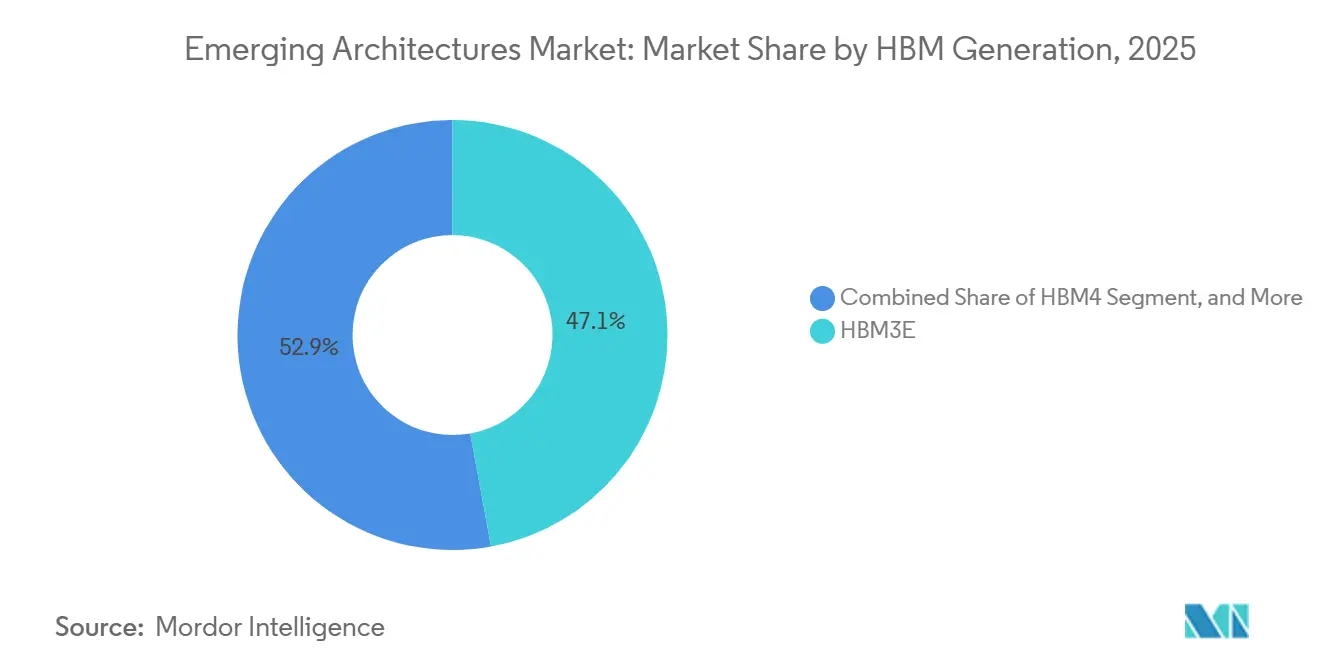

- By HBM generation, HBM3E held 47.14% of revenue of the emerging architectures market in 2025, while HBM4 is projected to expand at a 27.79% CAGR through 2031.

- By memory capacity per stack, the above 24 GB to 36 GB tier held 58.67% revenue share in 2025, while the above 36 GB to 48 GB tier is projected to grow at a 28.11% CAGR through 2031.

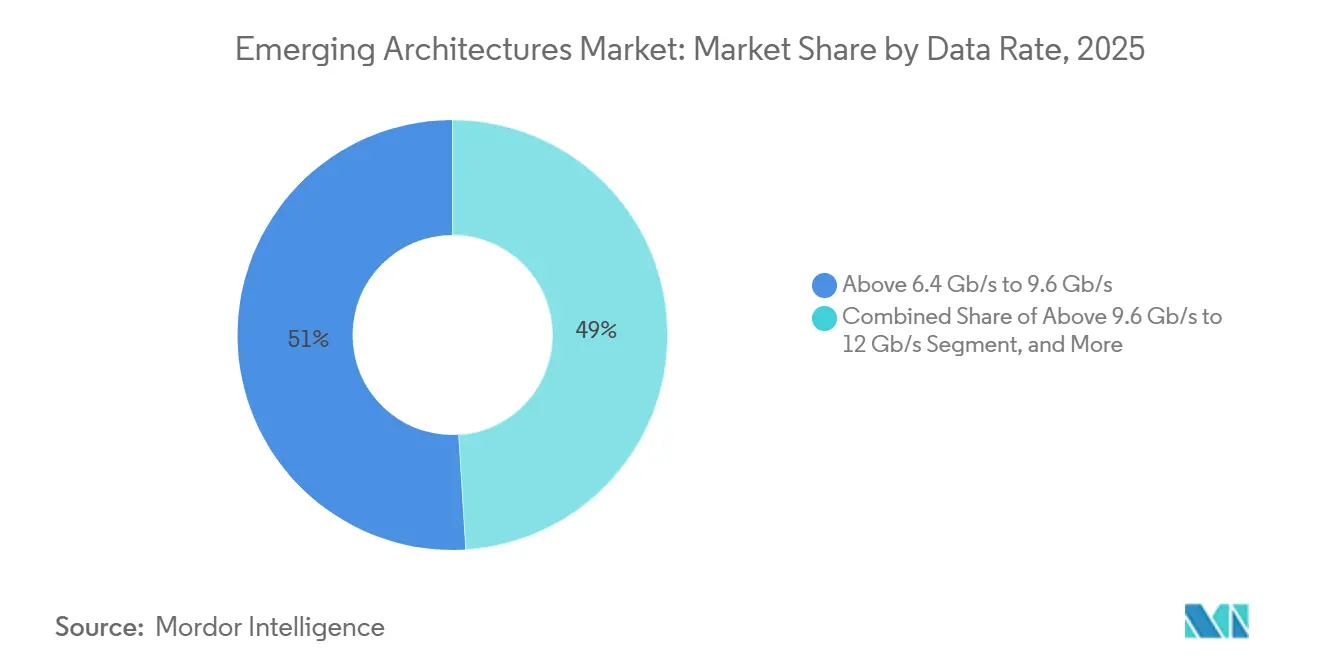

- By data rate, the above 6.4 Gb/s to 9.6 Gb/s tier held 50.99% revenue share in 2025, while the above 9.6 Gb/s to 12 Gb/s tier is projected to grow at a 27.99% CAGR through 2031.

- By host processor type, GPUs held 78.67% of the emerging architectures market share in 2025, while AI accelerator and custom ASIC demand is projected to expand at a 28.23% CAGR through 2031.

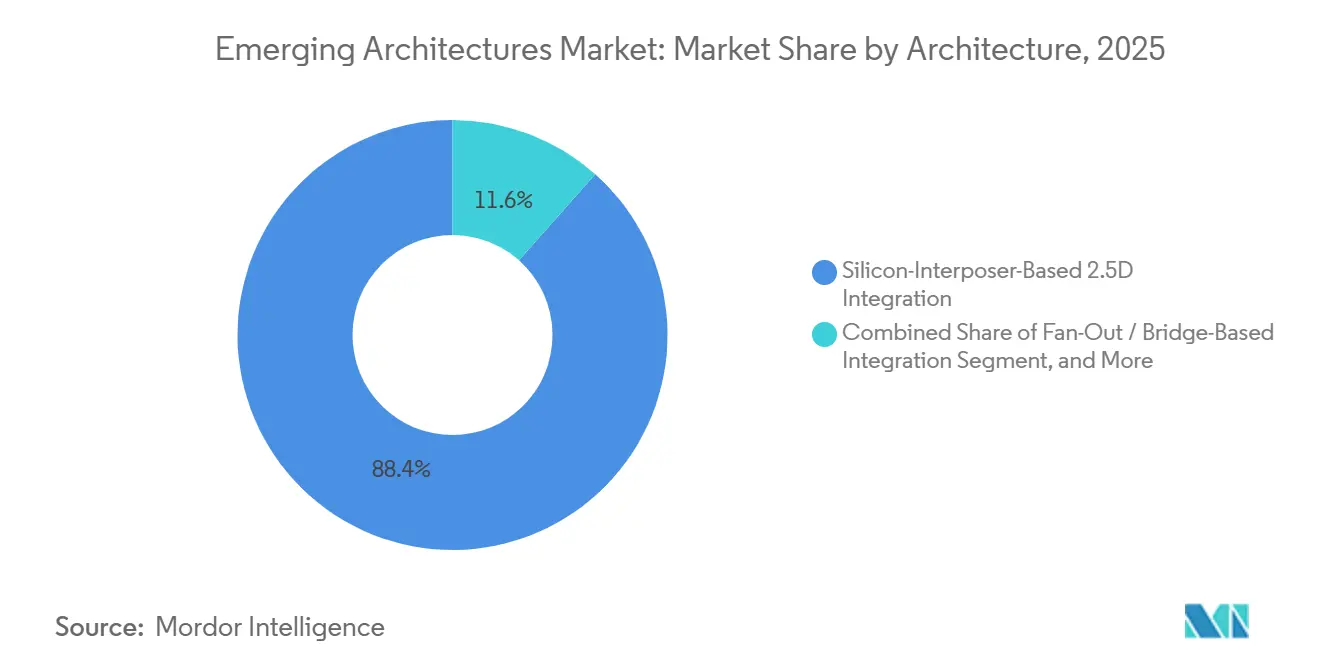

- By architecture, silicon-interposer-based 2.5D integration held 88.44% revenue share in 2025, while direct 3D heterogeneous integration is projected to grow at a 28.22% CAGR through 2031.

- By application, AI training held 51.34% revenue share in 2025, while AI inference is projected to grow at a 28.34% CAGR through 2031.

- By geography, Asia-Pacific held 61.66% revenue share of the emerging architectures market in 2025 and is also projected to record the fastest regional growth at a 28.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Emerging Architectures Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Server Proliferation and GPU Attach Rates | +5.0% | Global | Short term (≤ 2 years) |

| Hyperscaler Shift to On-Package Memory Architectures | +4.5% | North America and Asia-Pacific | Medium term (2-4 years) |

| HBM4 Qualification Cycles for Next-Generation AI Platforms | +4.0% | Global | Short term (≤ 2 years) |

| Localized Semiconductor Subsidies for Advanced Packaging and HBM Fabs | +3.5% | United States, South Korea, Japan | Medium term (2-4 years) |

| Edge AI Inference Demand in Automotive ADAS and Autonomous Platforms | +2.5% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Photonics-Ready Memory Roadmaps and Co-Packaged Optics Convergence | +2.0% | Global hyperscaler core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Server Proliferation And GPU Attach Rates

AI server deployment continues to raise the memory requirement for each new system entering service. The Emerging architectures market benefits because more accelerator-heavy server designs rely on HBM-enabled packaging rather than conventional off-package memory layouts. Higher attach rates also mean that memory demand can rise faster than server shipments when buyers move toward denser accelerator configurations. Custom silicon programs add another layer of pull because they require dedicated memory and packaging combinations instead of fully standardized designs. IEEE Electronics Packaging Society estimated that chiplet-based solutions enabled by HBM integration architectures will generate USD 100 billion to USD 110 billion in annual revenue in 2026, which shows how much value is now tied to these designs.[1]IEEE Electronics Packaging Society, “Heterogeneous Integration Roadmap (HIR): Supply Chain Chapter 18,” IEEE Electronics Packaging Society, eps.ieee.org

Hyperscaler Shift To On-Package Memory Architectures

Large cloud buyers have moved beyond normal server procurement and are now treating packaging access as a strategic supply issue. That shift strengthens the Emerging architectures market because HBM integration is becoming a core part of accelerator planning rather than a downstream component choice. TSMC’s CoWoS capacity expanded 106% in 2025, yet the backlog persisted, which shows that demand growth is running ahead of even aggressive supply additions. As packaging and memory take a larger share of accelerator cost, procurement decisions increasingly depend on assembly access, thermal performance, and yield, not only on the logic die itself. This change gives HBM suppliers, interposer providers, and outsourced assembly partners a more durable role in the bill of materials for AI hardware.

HBM4 Qualification Cycles For Next-Generation AI Platforms

HBM4 is moving the Emerging architectures market into a tighter performance and qualification race. Samsung shipped the first commercial HBM4 to Nvidia in February 2026, using a 4nm logic base die and a 2048-bit I/O interface with 11.7 Gb/s transfer speed, which marked a clear step up from earlier generations.[2]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com The move to logic base dies increases the technical link between foundry capabilities, memory stack design, and packaging compatibility. Qualification now depends on stable yield, thermal control, and cost per gigabyte at production scale, which raises the bar for every supplier in the chain. Faster product cycling between HBM3E, HBM4, and follow-on versions should keep the Emerging architectures market on a steep technology path through the forecast period.

Localized Semiconductor Subsidies For Advanced Packaging And HBM Fabs

Public funding is changing where future HBM capacity can be built and where it can be packaged. The Emerging architectures market stands to benefit because subsidy programs reduce the capital burden of adding high-cost back-end and memory infrastructure. IEEE Electronics Packaging Society noted that CHIPS Act direct funding included USD 458 million for SK Hynix’s USD 3.87 billion HBM packaging plant in Indiana and USD 407 million for Amkor Technology’s USD 7 billion advanced packaging campus in Arizona. Those commitments support geographic diversification in a supply chain that has stayed heavily concentrated in a few Asian locations. Over time, subsidy-backed expansion can reduce single-region exposure, even if new sites still take several years to reach meaningful output.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited CoWoS and Advanced Packaging Capacity | -3.5% | Global, concentrated in Taiwan | Short term (≤ 2 years) |

| Geo-Political Export Controls on AI Accelerators and HBM-Enabled Systems | -2.5% | US-China bilateral, global spill-over | Medium term (2-4 years) |

| TSV Yield Losses and Stack Complexity Above 12-Layer Architectures | -2.0% | Global | Short term (≤ 2 years) |

| Thermal Throttling and Power Delivery Limits in Ultra-High Bandwidth Devices | -1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited CoWoS And Advanced Packaging Capacity

Packaging capacity remains one of the clearest constraints on the Emerging architectures market. Even when memory output rises, final system supply can stay limited if interposer assembly, bonding, and testing lines do not expand at the same pace. Larger package sizes and more complex HBM integration also raise the cost of each new accelerator generation, which keeps pressure on both suppliers and buyers. IEEE Electronics Packaging Society expects the thermo-compression bonding step used in HBM integration to grow at a 13.4% CAGR and reach USD 1.1 billion by 2030, which underlines how persistent this bottleneck remains across the value chain. As long as advanced packaging growth trails demand, the Emerging architectures market will continue to face delayed deliveries and elevated assembly costs.

Geo-Political Export Controls On AI Accelerators And HBM-Enabled Systems

Export controls are creating a split demand map for advanced AI hardware and the memory systems attached to it. The Emerging architectures market is exposed because the highest-performance HBM stacks sit close to the same policy boundary as leading AI accelerators. Suppliers can still serve some demand in restricted markets, but top-tier configurations face tighter scrutiny, longer review cycles, and more detailed compliance obligations. That slows procurement and makes planning more difficult for both vendors and customers in affected regions. The result is a market where technical readiness alone does not determine sales timing, customer mix, or regional volume allocation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Generation: HBM3E Anchors Revenue As HBM4 Redefines The Competitive Threshold

HBM3E held 47.14% of the Emerging architectures market size in 2025, which reflects how widely it was deployed across current AI accelerator programs. The segment benefited from mass rollout on Nvidia’s Blackwell platform and from wider use in large inference and training systems. Earlier generations still retained a residual role in parts of enterprise inference and non-AI compute where the performance requirement was lower and cost sensitivity was higher. That left HBM3E as the commercial center of the Emerging architectures market in 2025 because it combined scale, maturity, and immediate platform fit.

HBM4 is projected to grow at a 27.79% CAGR through 2031, making it the fastest-growing generation in the Emerging architectures market. The transition is tied to next-cycle platform requirements that need a wider interface and stronger bandwidth performance than HBM3E can deliver at similar packaging density. Samsung’s February 2026 commercial shipment of HBM4 with a 4nm logic base die shows that suppliers are already moving the technology from qualification into supply. As HBM4 spreads, competition will depend less on being first to sample and more on who can keep output stable, costs controlled, and thermals manageable. That shift should make the generation mix one of the strongest indicators of supplier position over the next few years.

By Memory Capacity Per Stack: High-Capacity Configurations Shift Market Structure

The above 24 GB to 36 GB tier held a 58.67% revenue share in 2025, which made it the leading capacity band in the Emerging architectures market. That position came from 12-layer HBM3E stacks becoming the practical design reference for new AI accelerators. Lower-capacity tiers remained relevant for legacy inference deployments and non-AI workloads where memory bandwidth did not justify the cost of deeper stacking. The 2025 mix showed that buyers were already favoring denser stacks when they needed to improve compute utilization and system throughput.

The above 36 GB to 48 GB tier is projected to grow at a 28.11% CAGR through 2031, which signals a clear move toward higher-capacity stacks in the Emerging architectures market. This band is supported by the rollout of 16-layer HBM4 and HBM4E products that raise memory capacity per package without requiring a wider system footprint. The change matters because larger stacks can support more demanding AI inference and training loads inside a fixed accelerator envelope. It also increases the importance of yield control, bonding quality, and thermal stability at each additional layer. Capacity expansion per stack is therefore becoming both a performance lever and a manufacturing challenge in the Emerging architectures market.

By Data Rate: Higher-Speed Tiers Drive AI Infrastructure Density

The above 6.4 Gb/s to 9.6 Gb/s tier held 50.99% revenue share in 2025, which made it the main operating band in the Emerging architectures market. This range largely covered the performance profile of HBM3E used in current AI accelerators. Lower-speed tiers remained tied to legacy memory configurations with little forward momentum in advanced AI systems. The 2025 mix showed that buyers had already accepted higher per-pin data rates as a necessary condition for serving larger models and denser accelerator racks.

The above 9.6 Gb/s to 12 Gb/s tier is projected to grow at a 27.99% CAGR through 2031, making it the main next-step speed band in the Emerging architectures market. Samsung confirmed 11.7 Gb/s performance for its commercial HBM4, with peak speed reaching 13 Gb/s, which places the new generation directly in this transition zone. Data rate gains also matter alongside interface width, because HBM4’s 2048-bit structure lifts total memory bandwidth beyond what a per-pin metric alone suggests. That allows suppliers to improve delivered bandwidth without relying only on raw clock increases. As a result, the speed ladder in the Emerging architectures market is evolving through both interface design and per-pin advancement.

By Host Processor Type: GPUs Lead But Custom ASICs Reshape Supplier Economics

AI accelerator and custom ASIC demand is projected to grow at a 28.23% CAGR through 2031, which makes it the fastest-growing processor segment in the Emerging architectures market. Hyperscalers are expanding proprietary silicon programs and are increasingly pairing those processors with HBM through the same advanced packaging route used by GPUs. That creates a wider customer base for memory suppliers and raises the number of custom qualification paths that must be supported. It also deepens co-design ties between the processor owner, the memory supplier, and the packaging partner.

GPUs held 78.67% of the Emerging architectures market share in 2025, so they remained the clear anchor of host processor demand. Nvidia Blackwell deployments and AMD MI-series ramps kept GPU-led systems at the center of commercial volume. CPU and APU combinations with HBM remained concentrated in high-performance computing niches, while FPGA and adaptive SoC use cases stayed limited to lower-volume edge inference and network processing. Networking ASICs, DPUs, and switch ASICs are emerging as another possible lane for HBM as AI traffic places more pressure on memory bandwidth inside the network itself. The processor mix is therefore broadening, even though the Emerging architectures market still depends heavily on GPUs for current revenue.

By Architecture: 2.5D Silicon Interposer Leads But 3D Integration Establishes A Technical Beachhead

Silicon-interposer-based 2.5D integration held 88.44% revenue share in 2025, which shows how strongly the Emerging architectures market remained tied to a single production approach. TSMC’s CoWoS platform has been the only large-scale route for bringing HBM stacks together with leading-edge logic dies in commercial volume. IEEE EDTM 2025 research demonstrated a 1.8 TB/s HBM design using 2.5D packaging and a 5-metal-layer silicon interposer connection, which confirms that the current model still has meaningful technical headroom.[3]IEEE EDTM, “A 1.8TB/s HBM Heterogeneously Integrated GPU Design Exploring 2.5D Packaging Technology,” IEEE EDTM, doi.org RDL-based and fan-out or bridge-based approaches remain more relevant in lower-complexity inference and networking environments where full silicon interposer cost is harder to justify.

Direct 3D heterogeneous integration is projected to grow at a 28.22% CAGR through 2031, making it the fastest-growing architecture segment in the Emerging architectures market. The appeal lies in its ability to raise memory-per-GPU bandwidth and package density beyond what larger 2.5D interposers can deliver efficiently. The main barrier is still thermal behavior, because vertical stacking raises local power density and makes heat removal harder as packages become denser. That means the shift to direct 3D will depend on more than design ambition alone. It will require suppliers to solve heat, yield, and power delivery in a way that can survive volume production.

By Application: AI Training Holds The Revenue Lead As AI Inference Alters The Demand Profile

AI inference is projected to grow at a 28.34% CAGR through 2031, which makes it the fastest-growing application in the Emerging architectures market. Deployed AI systems are pushing memory needs higher because longer context windows, agentic workflows, and multimodal services all increase the memory footprint tied to each inference task. This changes the demand profile from a concentrated training cluster model to a wider production infrastructure model. It also means memory bandwidth becomes important in steady-state service delivery, not only in periodic model training.

AI training held 51.34% revenue share in 2025, so it remained the largest application segment in the Emerging architectures market. Large model training clusters still required sustained high-bandwidth throughput across hyperscaler infrastructure, which supported this lead position. High-performance computing and supercomputing formed a stable secondary layer with long procurement cycles and multi-year platform commitments. Networking, telecom, professional visualization, automotive compute, and aerospace and defense together formed an emerging demand tier where edge AI inference is bringing HBM-equipped systems into more specialized settings. The application spread is widening, even though training still accounted for the largest revenue pool in 2025.

Geography Analysis

Asia-Pacific held 61.66% revenue share in 2025 and is projected to grow at a 28.41% CAGR through 2031, which means it led both current scale and future growth in the Emerging architectures market. The region’s position comes from South Korea’s central role in HBM manufacturing and Taiwan’s dominant role in advanced packaging. This concentration gives Asia-Pacific a structural edge because the core memory and interposer capabilities already sit inside the same regional production ecosystem. Asia-Pacific therefore remains the operational center of the Emerging architectures market, even as other regions try to build a larger domestic footprint.

North America is the main demand anchor for the Emerging architectures market because it concentrates a large share of AI accelerator purchases and hyperscale system deployment. The United States also stands out as the most active destination for new subsidy-backed advanced packaging capacity. IEEE Electronics Packaging Society identified CHIPS Act funding for SK Hynix’s Indiana HBM packaging plant and for Amkor’s Arizona packaging campus, which marks an early shift from minimal local capacity toward a functioning domestic base. Amkor also stated that its Arizona project expanded to USD 7 billion, with high-volume manufacturing targeted from 2028, which reinforces the long-build nature of regional diversification. Canada and Mexico are not expected to hold significant HBM fabrication or advanced packaging positions during the forecast period.

Europe’s role in the Emerging architectures market is still more demand-led than supply-led. Regional activity is concentrated in HPC installations and in automotive AI inference requirements that place strict safety and reliability demands on memory subsystems. The Emerging architectures market has only limited direct manufacturing exposure in South America and the Middle East and Africa, where revenue mainly comes from AI server deployment rather than memory production. Buyers in these regions also face added lead-time and compliance risk when high-end HBM systems are exposed to export control reviews.

Competitive Landscape

The Emerging architectures market is highly consolidated at the HBM manufacturing layer, with SK Hynix, Samsung, and Micron as the only commercial volume suppliers. That narrow supplier base gives each qualification cycle, yield improvement, and packaging commitment a direct effect on revenue distribution. SK Hynix strengthened its position in June 2026 when it announced a multi-year technology partnership with Nvidia to co-develop next-generation AI memory for Nvidia’s AI factory buildout. Samsung is competing through a vertically integrated model that combines advanced foundry logic for HBM4 base dies, DRAM production, and packaging under one structure, which supports tighter control over product development and manufacturing execution.

At the packaging layer, the Emerging architectures market is less concentrated than memory manufacturing, but it still revolves around a small set of critical capabilities. TSMC’s CoWoS platform remains the main large-volume route for HBM integration with leading-edge logic, which keeps packaging access central to competitive position. Amkor’s Arizona buildout shows how OSAT participation is moving from peripheral support to strategic relevance as customers seek more geographic diversity in back-end assembly. This shift means that success in the Emerging architectures market depends on more than memory design alone. It also depends on who can secure advanced packaging slots, manage stack complexity, and keep thermals under control.

White space remains open in testing infrastructure for known-good-die stacking, in-package optical input and output, and hybrid bonding equipment. Companies such as Hanmi Semiconductor, Hanwha Semitek, Rambus, and Cadence Design Systems are building relevance where process complexity rises with HBM4E and direct 3D integration. These positions may not dominate revenue today, but they gain importance as the Emerging architectures market pushes into denser stacks and more difficult assembly flows. Competition is therefore likely to widen around tools, packaging, and interface design, even while memory supply remains concentrated among a few leaders.

Emerging Architectures Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Taiwan Semiconductor Manufacturing Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK Hynix and Nvidia announced a multi-year technology partnership to co-develop next-generation AI memory for Nvidia's global AI factory buildout, covering HBM4 and the Vera Rubin platform and including provisions for extended development cycles, advanced fabrication investment, and sustained supply.

- June 2026: Intel disclosed its Cross-Batch Memory (XBM) architecture through a patent publication. XBM replaces conventional HBM's silicon interposer with serial UCIe connectivity and BEOL DRAM technology, targeting lower packaging costs and scalable AI memory architectures

- February 2026: Samsung Electronics shipped the world's first commercial HBM4 to Nvidia, using a 4nm logic base die, achieving 11.7 Gb/s data transfer speed with peak performance up to 13 Gb/s. Samsung subsequently projected cumulative HBM4 sales of USD 10 billion for 2026 and began sampling HBM4E only 3 months later, signaling a compressed product introduction cycle.

- January 2026: Arteris completed the acquisition of Cycuity to integrate hardware cybersecurity assurance with its Network-on-Chip (NoC) and chiplet interconnect IP portfolio, enhancing secure next-generation SoC architectures.

Global Emerging Architectures Market Report Scope

The Emerging Architectures Market refers to the market for new and evolving computing architectures designed to improve performance, efficiency, scalability, and flexibility. It includes technologies such as chiplets, 2.5D/3D integration, advanced packaging, domain-specific accelerators, and heterogeneous computing systems.

The Emerging Architectures Market Report is Segmented by HBM Generation (HBM2 and Earlier, HBM2E, HBM3, HBM3E, HBM4, and HBM4E / Enhanced HBM4 and Next-Generation HBM), Memory Capacity per Stack(Up to 8 GB, Above 8 GB to 16 GB, Above 16 GB to 24 GB, Above 24 GB to 36 GB, Above 36 GB to 48 GB, and Above 48 GB), Data Rate (Up to 4.0 Gb/s, Above 4.0 Gb/s to 6.4 Gb/s, Above 6.4 Gb/s to 9.6 Gb/s, Above 9.6 Gb/s to 12 Gb/s, and Above 12 Gb/s), Host Processor Type (GPU, AI Accelerator and Custom ASIC, CPU and APU, FPGA and Adaptive SoC, and Networking ASIC, DPU, and Switch ASIC), Architecture (Silicon-Interposer-Based 2.5D Integration, RDL / Organic-Interposer-Based 2.5D Integration, Fan-Out / Bridge-Based Integration, and Direct 3D Heterogeneous Integration), Application (AI Training, Inference, HPC, Cloud, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2 and Earlier |

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E / Enhanced HBM4 and Next-Generation HBM |

| Up to 8 GB |

| Above 8 GB to 16 GB |

| Above 16 GB to 24 GB |

| Above 24 GB to 36 GB |

| Above 36 GB to 48 GB |

| Above 48 GB |

| Up to 4.0 Gb/s |

| Above 4.0 Gb/s to 6.4 Gb/s |

| Above 6.4 Gb/s to 9.6 Gb/s |

| Above 9.6 Gb/s to 12 Gb/s |

| Above 12 Gb/s |

| GPU |

| AI Accelerator and Custom ASIC |

| CPU and APU |

| FPGA and Adaptive SoC |

| Networking ASIC, DPU, and Switch ASIC |

| Other Host Processor Type |

| Silicon-Interposer-Based 2.5D Integration |

| RDL / Organic-Interposer-Based 2.5D Integration |

| Fan-Out / Bridge-Based Integration |

| Direct 3D Heterogeneous Integration |

| Other Architectures |

| AI Training |

| AI Inference |

| High-Performance Computing and Supercomputing |

| Cloud and Hyperscale Computing |

| Enterprise Servers, Databases, and Analytics |

| Networking and Telecom Infrastructure |

| Professional Visualization and Graphics |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By HBM Generation | HBM2 and Earlier | |

| HBM2E | ||

| HBM3 | ||

| HBM3E | ||

| HBM4 | ||

| HBM4E / Enhanced HBM4 and Next-Generation HBM | ||

| By Memory Capacity per Stack | Up to 8 GB | |

| Above 8 GB to 16 GB | ||

| Above 16 GB to 24 GB | ||

| Above 24 GB to 36 GB | ||

| Above 36 GB to 48 GB | ||

| Above 48 GB | ||

| By Data Rate | Up to 4.0 Gb/s | |

| Above 4.0 Gb/s to 6.4 Gb/s | ||

| Above 6.4 Gb/s to 9.6 Gb/s | ||

| Above 9.6 Gb/s to 12 Gb/s | ||

| Above 12 Gb/s | ||

| By Host Processor Type | GPU | |

| AI Accelerator and Custom ASIC | ||

| CPU and APU | ||

| FPGA and Adaptive SoC | ||

| Networking ASIC, DPU, and Switch ASIC | ||

| Other Host Processor Type | ||

| By Architecture | Silicon-Interposer-Based 2.5D Integration | |

| RDL / Organic-Interposer-Based 2.5D Integration | ||

| Fan-Out / Bridge-Based Integration | ||

| Direct 3D Heterogeneous Integration | ||

| Other Architectures | ||

| By Application | AI Training | |

| AI Inference | ||

| High-Performance Computing and Supercomputing | ||

| Cloud and Hyperscale Computing | ||

| Enterprise Servers, Databases, and Analytics | ||

| Networking and Telecom Infrastructure | ||

| Professional Visualization and Graphics | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the Emerging architectures market?

The Emerging architectures market size is projected at USD 2.56 billion in 2025, USD 3.11 billion in 2026, and USD 10.39 billion by 2031, at a 27.28% CAGR.

Which region leads revenue and growth in this space?

Asia-Pacific led with 61.66% revenue share in 2025 and is also projected to post the fastest regional growth at 28.41% through 2031.

Which HBM generation is expanding the fastest?

HBM4 is the fastest-growing generation, with a projected 27.79% CAGR, while HBM3E held the largest share in 2025 at 47.14%.

Why are GPUs still dominant if custom ASICs are growing quickly?

GPUs held 78.67% of host processor demand in 2025 because they remain the main commercial platform, while custom ASICs are growing faster as hyperscalers scale proprietary silicon.

What is the biggest bottleneck for supply expansion?

CoWoS and related advanced packaging capacity remain the main bottleneck because memory output alone does not translate into shipped systems without interposer assembly, bonding, and testing capacity.

Which application is changing the demand pattern the most?

AI inference is changing the mix most quickly, with a projected 28.34% CAGR, because deployed AI services need high memory bandwidth across a wider installed base.

Page last updated on: