Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

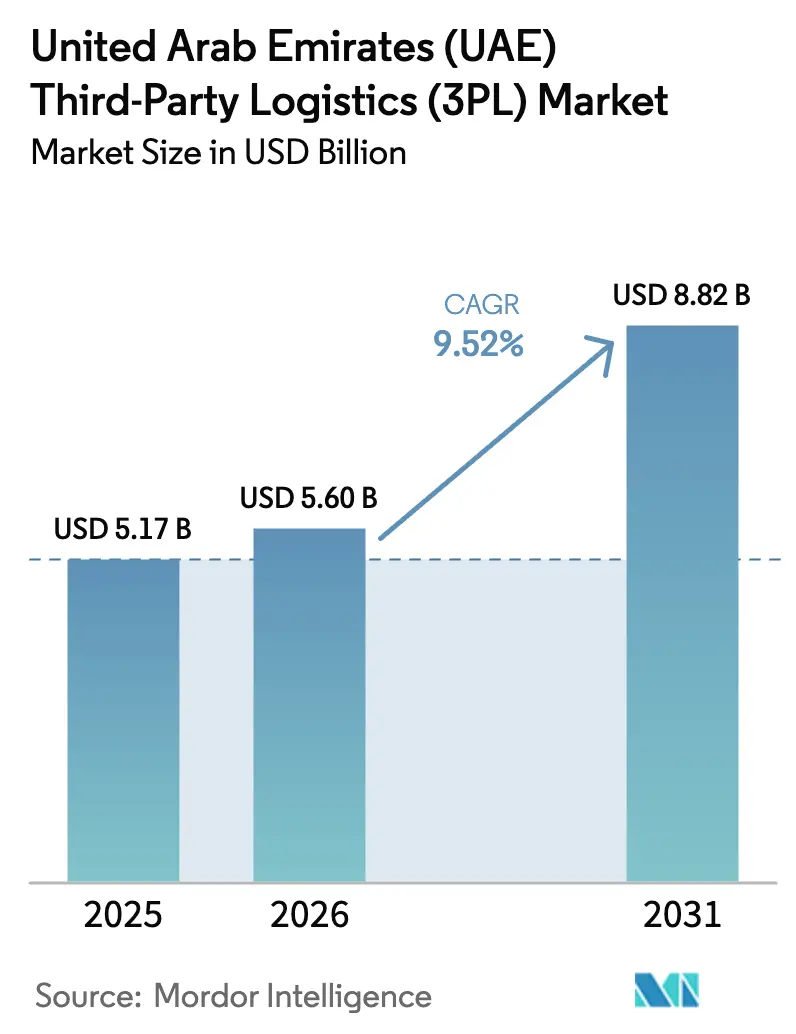

| Base Year Market Size (2025) | USD 5.17 Billion |

| Market Size (2026) | USD 5.60 Billion |

| Market Size (2031) | USD 8.82 Billion |

| Growth Rate (2026 - 2031) | 9.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates (UAE) Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The United Arab Emirates Third-Party Logistics Market size is estimated at USD 5.60 billion in 2026, and is expected to reach USD 8.82 billion by 2031, at a CAGR of 9.52% during the forecast period (2026-2031).

The sharp expansion reflects a logistics ecosystem where artificial intelligence, automation, and carbon-neutral initiatives converge with the country’s role as a multimodal bridge between Asia, Europe, and Africa. Robust e-commerce demand, free-zone clustering, and government-backed infrastructure programs are pushing providers to invest in advanced fulfillment centers, IoT-enabled fleets, and temperature-controlled facilities. Hybrid operating strategies that combine selected asset ownership with network orchestration capabilities are emerging as the dominant model, allowing providers to hedge against driver shortages and warehouse rent inflation. Meanwhile, the completed 900 km Etihad Rail and the USD 35 billion Al Maktoum International Airport expansion promise to further integrate sea, air, road, and rail corridors, cementing the UAE 3PL market as a preferred Gulf gateway for time-sensitive cargo. Sustainability is another accelerating theme as warehouse operators pilot solar micro-grids and green building materials to align with the UAE’s Net-Zero 2050 vision.

Key Report Takeaways

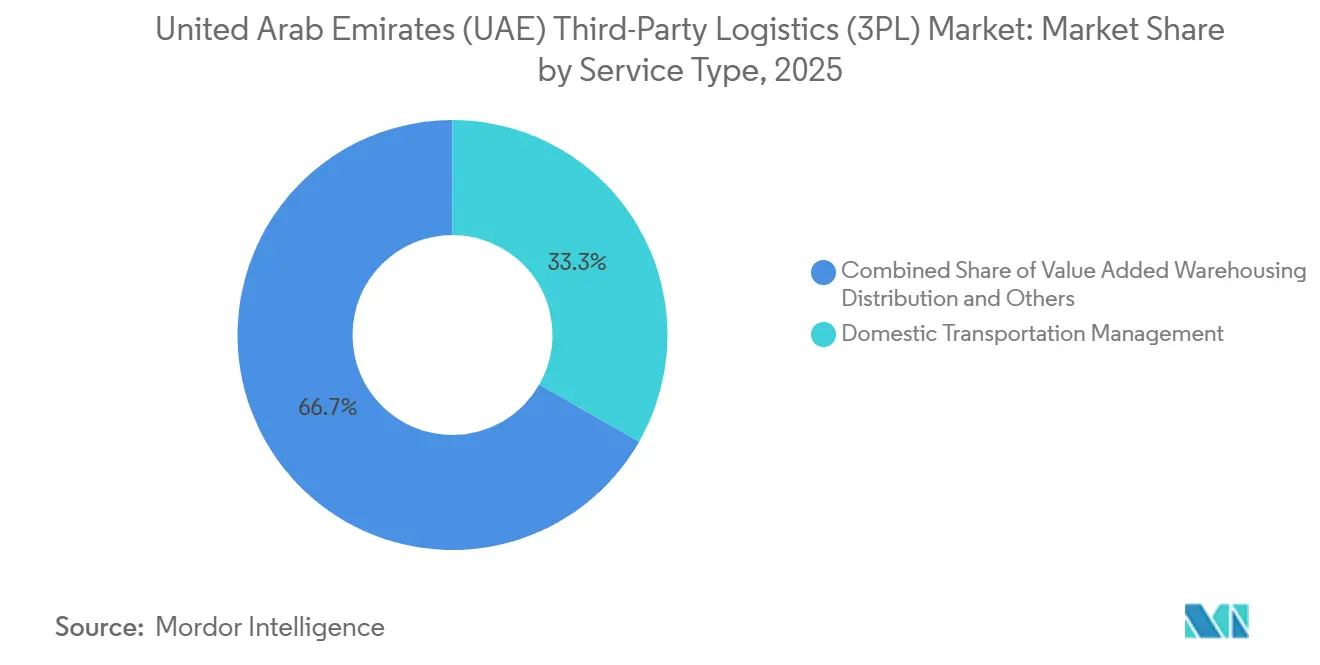

- By service type, domestic transportation management held 33.26% of the UAE 3PL market share in 2025, while Value-Added Warehousing and Distribution is forecast to grow at a 10.03% CAGR through 2031.

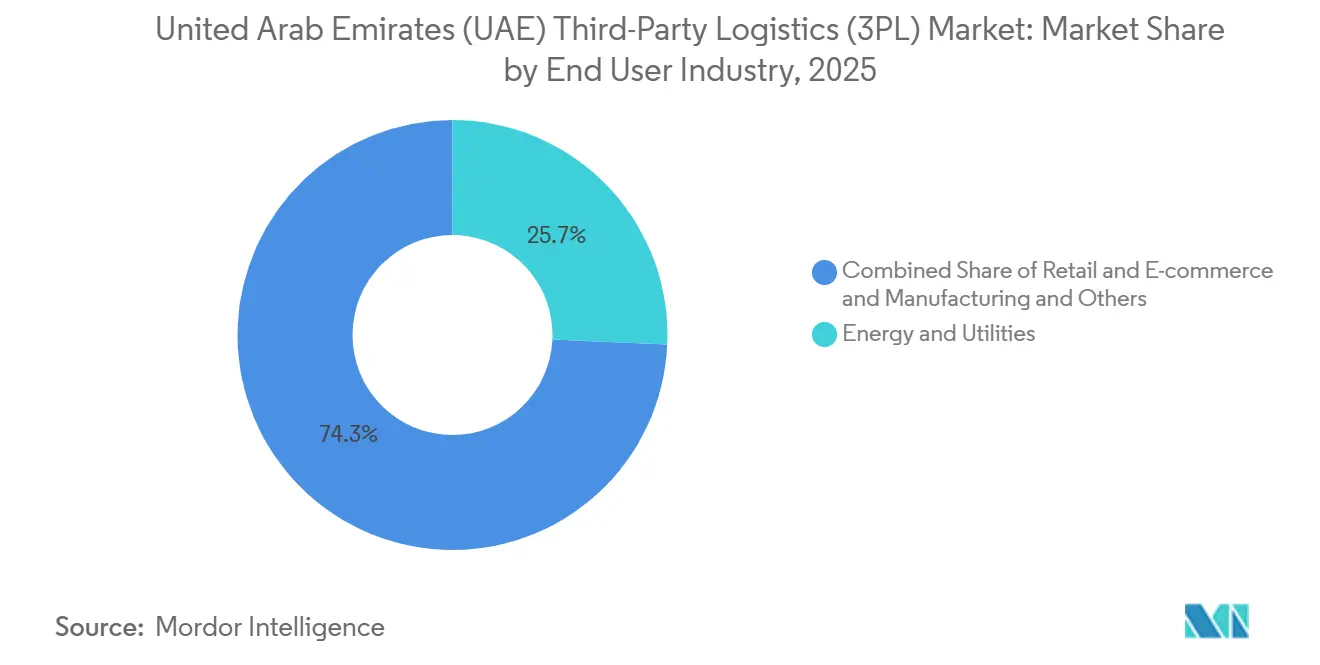

- By end-user industry, energy & utilities commanded 25.71% of the UAE 3PL market size in 2025, whereas Life Sciences & Healthcare is projected to expand at a 12.84% CAGR between 2026 and 2031.

- By logistics model, the asset-light approach accounted for 41.53% share of the UAE 3PL market size in 2025, yet hybrid models are advancing at a 9.91% CAGR through 2031.

- By geography, Dubai captured 66.12% of the UAE 3PL market share in 2025, and the Rest of the UAE is expected to accelerate at an 11.07% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Arab Emirates (UAE) Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid E-commerce Penetration | +2.3 | Dubai, Abu Dhabi, with expansion to all emirates | Short term (≤2 yrs) |

| Ambitious national logistics strategy (UAE Logistics Strategy 2030) | +2.1 | National, with infrastructure concentration in Dubai, Abu Dhabi | Long term (≥5 yrs) |

| Expansion of free-zone based fulfillment hubs | +1.4 | Dubai (NIP, JAFZA), Abu Dhabi (ICAD, Khalifa Port) | Medium term (≈3-4 yrs) |

| Growing cold-chain demand in pharma & F&B | +1.6 | Dubai, Abu Dhabi, with a regional distribution reach | Medium term (≈3-4 yrs) |

| AI-driven route-optimization adoption by SMEs | +1.2 | National, with higher adoption in urban centers | Short term (≤2 yrs) |

| Carbon-neutral warehousing pilots | +0.7 | Dubai, Abu Dhabi (pilot phase, limited scale) | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Rapid e-commerce penetration

Digital retail’s share of total UAE transactions is set to rise from 8.2% in 2021 to 26.5% in 2026, pushing annual last-mile volumes from 185 million to 665 million parcels. Third-party logistics providers are responding with micro-fulfillment centers, automated sortation lines, and crowd-sourced delivery platforms that slash order-to-door times. Kuehne + Nagel and Expeditors International each committed to 23,000 m² facilities in Dubai South, confirming that scale logistics infrastructure remains a competitive prerequisite.[1]Asia Cargo News, “Kuehne + Nagel E-commerce Fulfillment Center in Dubai,” asiacargonews.com The driver’s influence is strongest in Dubai and Abu Dhabi, where cash-on-delivery fell below 27% of online transactions after the widespread adoption of digital wallets, thereby removing a historic friction point. Mobile shopping and social commerce add further complexity, requiring 3PL operators to synchronize inventory, order processing, and returns across multiple sales channels. The result is a sustained rise in warehouse automation investments and API-based integrations that let retailers outsource fulfillment while maintaining real-time inventory visibility.

Ambitious national logistics strategy (UAE Logistics Strategy 2030)

The national roadmap aims to elevate the logistics sector’s GDP contribution to 5% and place the country among the world’s top ten logistics hubs. Central to the plan is a USD 35 billion expansion of Al Maktoum International Airport that will handle 12 million tons of cargo annually when fully open in 2031. Parallel upgrades, including the operational Etihad Rail network, forge seamless rail-to-port connectivity across all seven emirates. Regulatory harmonization, single-window customs, unified cargo clearance, and 100% foreign ownership in selected sub-sectors reduce dwell times and attract multinational shippers. The long-term, high-impact driver positions the UAE 3PL market to capture transshipment flows that currently bypass the Gulf, while offering domestic industries faster access to global supply chains.

Expansion of free-zone based fulfillment hubs

Tax-free zones such as Jebel Ali Free Zone (JAFZA) and National Industries Park provide manufacturers and retailers with bonded corridors that link sea and air gateways within minutes. Free-zone tenants benefit from 100% foreign ownership, zero import duties, and on-site customs centers that cut clearance times. These advantages spur demand for integrated 3PL services ranging from kitting to reverse logistics, especially for re-export shipments bound for Africa and South Asia. The medium-term driver also disperses logistics activity beyond Dubai toward fast-developing clusters in Abu Dhabi’s ICAD and Khalifa Port.

Growing cold-chain demand in pharma & F&B

Government spending of AED 4.95 billion (USD 1.35 billion) on healthcare facilities and the rise of telehealth are stimulating demand for GDP-compliant pharmaceutical logistics. RSA Global and Americold’s joint venture to build an 8-chamber, 40,000-pallet cold store in Jebel Ali Free Zone underlines the scale of specialized infrastructure coming online. Fresh food initiatives, including Dubai’s plan to host the world’s largest fruit and vegetable hub, amplify the need for sub-zero warehousing, data-loggers, and validated packaging. Competitive advantage now hinges on real-time temperature monitoring, pharma-grade certifications, and the ability to consolidate multi-sector volumes to maximize asset utilization.

Restraint Impact Table*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Driver Shortages | -1.5 | National, particularly acute in Dubai, Abu Dhabi | Medium term (3-4 yrs) |

| Rising warehouse rents in Dubai & Abu Dhabi | -1.8 | Dubai (JAFZA, Dubai South), Abu Dhabi (ICAD) | Medium term (3-4 yrs) |

| Fragmented customs processes across emirates | -1.1 | Cross-emirate operations, particularly Northern Emirates | Medium term (3-4 yrs) |

| Limited rail freight connectivity | -0.6 | National infrastructure development is ongoing | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Persistent Driver Shortages

Federal labor reforms and burgeoning gig-economy alternatives have shrunk the pool of licensed commercial drivers, raising 3PL wage bills by up to 12%. The shortage is most acute for drivers with hazmat, refrigerated, or urban last-mile credentials. Providers are launching retention bonuses, accelerated training pipelines, and controlled trials of autonomous trucks inside industrial zones, yet large-scale automation remains five years out due to pending regulations. Over the medium term, sustained labor tightness is expected to compress margins in domestic haulage unless technology offsets headcount needs.

Rising warehouse rents in Dubai & Abu Dhabi

Prime logistics rents in JAFZA and Dubai South advanced 18% year-over-year in Q3 2025, outpacing general inflation and pressuring operating costs. Warehousing already represents up to 30% of 3PL expense structures, so rent spikes threaten profitability, especially for small providers. Strategies to mitigate the squeeze include high-bay racking, autonomous mobile robots, and migration to lower-cost emirates. New supply pipelines in Abu Dhabi’s ICAD and Sharjah’s free zones may temper rental escalation by 2028, yet location-critical sectors such as e-commerce fulfillment will continue to pay premiums for proximity to airports and express parcel hubs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Warehousing Complexity Drives Value Migration

Value-Added Warehousing and Distribution segment of the UAE 3PL market is projected to advance at the fastest 10.03% CAGR over 2026-2031. Providers are layering kitting, light assembly, and quality inspection services on top of storage to capture higher margins and reduce client handling steps. DP World’s integrated warehousing platform now combines temperature-controlled space, IoT sensors, and blockchain-verified chain-of-custody, illustrating the move toward turnkey solutions[2]DP World, “Logistics Services in UAE,” dpworld.com. International Transportation Management remains steady at roughly 34% share due to the country’s strategic re-export role and expanding air-sea corridors.

Domestic Transportation Management holds the largest 33.26% slice of the UAE 3PL market share but faces cost pressure from driver shortages and diesel volatility. Network optimization software and route-planning AI help offset these challenges, yet capital outlays may squeeze smaller carriers. Multimodal offerings leveraging Etihad Rail create fresh cross-selling potential by linking inland depots directly to ports, thus reducing drayage times and emissions.

By End-User Industry: Healthcare Logistics Outpaces Traditional Sectors

Energy & Utilities led with 25.71% UAE 3PL market share in 2025, supported by ADNOC Logistics & Services’ offshore fleet additions and ongoing hydrocarbon export volumes. Nevertheless, Life Sciences & Healthcare is set to register the highest 12.84% CAGR as specialized storage and time-critical delivery capabilities become mandatory for vaccines and precision-medicine therapies. Abu Dhabi’s Critical Care Transport System standard illustrates how regulation is elevating service-level requirements.

Retail & e-commerce is another bright spot, buoyed by social-commerce adoption and same-day delivery expectations. Manufacturing benefits from the “Operation 300 Billion” policy that incentivizes domestic production, increasing inbound raw-material flows and outbound finished-goods shipments. Finally, Food & beverage logistics is being reshaped by consumer demand for fresh imports, prompting investment in reefers and HACCP-certified cross-docks.

By Logistics Model: Hybrid Strategies Balance Flexibility and Control

Asset-light operators captured 41.53% of the UAE 3PL market size in 2025 by orchestrating carrier networks without heavy balance-sheet commitments. Yet hybrid strategies are climbing at a 9.91% CAGR as market leaders selectively acquire critical assets. DHL Global Forwarding’s takeover of Danzas AEI Emirates, including 20 owned facilities, demonstrates the pivot toward infrastructure control in geographies where service quality and capacity access determine customer stickiness.

Pure asset-heavy models persist in niche areas, such as pharma cold chain, where regulatory compliance and temperature integrity demand direct facility ownership. RSA Cold Chain’s decision to fund its own sub-zero warehouses highlights the barriers to entry for new challengers in specialized verticals. The evolving balance suggests that UAE 3PL market participants will continue to toggle between owning and leasing based on service criticality, risk appetite, and capital availability.

Geography Analysis

Dubai’s unparalleled infrastructure density secured 66.12% of the UAE 3PL market share in 2025. Five-parallel-runway expansion at Al Maktoum International Airport will lift annual freight capacity to 12 million t and reinforce the emirate’s role as the Gulf’s premier air-cargo hub. Bonded corridors within EZDubai enable seamless sea-to-air transfers that bypass traditional customs checks, slashing lead times for high-value electronics and fashion.

Abu Dhabi is closing the gap by aligning logistics assets with its industrial diversification agenda. ICAD and Khalifa Port serve fast-growing clusters in advanced manufacturing, renewable energy components, and healthcare supplies. The emirate’s Department of Health mandates GDP-compliant transport for sensitive medical cargo, creating a specialized service pool that only certified 3PLs can penetrate. Backed by sovereign wealth funds, local players are scaling multi-temperature facilities and investing in route-optimization AI to serve both domestic and regional markets.

Sharjah, Ras Al-Khaimah, and Fujairah, grouped as the Rest of the UAE, are forecast to record an 11.07% CAGR through 2031. Cheaper land, rents up to 30% below Dubai, and new highway links such as the USD 3.5 billion Al Mafraq-Al Ghuwaifat road improve connectivity to Jebel Ali Port and Saudi borders. The completed 900 km Etihad Rail further integrates northern emirates into national trade lanes, allowing 3PLs to stage inventory closer to end customers without sacrificing transit speed[3]Etihad Rail, “Network Overview,” etihadrail.ae . Cost-sensitive clients in FMCG and heavy manufacturing increasingly view these emirates as viable alternatives for large-footprint distribution centers.

Competitive Landscape

The UAE 3PL market features moderate fragmentation punctuated by rapid consolidation moves. DHL Global Forwarding’s integration of 1,100 employees and 20 facilities through its Danzas acquisition bolstered its end-to-end capabilities and solidified its hybrid model positioning. ADQ’s interest in Aramex signals possible sovereign-backed consolidation playbooks that could reshape competitive hierarchies.

Scale alone is no longer sufficient; technology and specialized certifications now drive customer preference. Aramex posted AED 1.6 billion (USD 435 million) in Q3 2025 revenue, with domestic express and logistics units offsetting weaker long-haul volumes, underscoring the pivot toward localized, high-service segments[4]Aramex, “Q3 2025 Results,” aramex.com . Kuehne + Nagel’s 45,000-pallet e-commerce hub inside EZDubai exemplifies investments that blend automation with bonded status to shorten order cycles for digital merchants.

Niche specialists remain competitive in areas such as pharmaceutical cold chain, bulk liquids, and reverse logistics. RSA Global’s facility pipeline, Tristar’s hazardous-materials expertise, and GAC’s marine logistics offerings illustrate how focused capabilities can coexist alongside multinational giants. The convergence of scale, technology, and specialization will likely drive further mergers, joint ventures, and free-zone partnerships over the planning horizon.

United Arab Emirates (UAE) Third-Party Logistics (3PL) Industry Leaders

Aramex

DHL Global Forwarding

GAC

CEVA Logistics (CMA CGM)

FedEx Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emirates SkyCargo outlined its 2026 logistics strategy after significantly expanding its fleet in 2025, deploying up to ten new Boeing 777F freighters by year-end.

- November 2025: AKI Logistics launched a new 3PL business unit in the UAE from central hubs in Dubai Industrial City and Dubai Investment Park.

- May 2025: DP World announced a USD 2.5 billion investment in 2025 to expand its logistics infrastructure globally, including enhancements at Jebel Ali and other key trade hubs.

- February 2025: Kuehne + Nagel began operations at a 23,000 m² bonded e-commerce fulfillment center in EZDubai, adding 45,000 pallet positions.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the United Arab Emirates third-party logistics market as every fee-based domestic or international movement, warehousing, and related value-added activity that a shipper outsources to an independent 3PL, whether asset-heavy, asset-light, or hybrid in model. Transaction values are recorded at the point the service is billed to the shipper, expressed in constant 2024 USD.

(Scope exclusion: turnkey facility management, last-mile services performed by in-house captive fleets, and pure digital freight marketplaces remain outside this boundary.)

Segmentation Overview

- By Service

- Domestic Transportation Management

- Road

- Air

- More

- International Transportation Management

- Road

- Air

- Sea

- Multimodal / Intermodal

- Value-Added Warehousing and Distribution (VAWD)

- Domestic Transportation Management

- By End-User Industry

- Automotive

- Energy and Utilities

- Manufacturing

- Life Sciences and Healthcare

- Technology and Electronics

- Retail and E-commerce

- Consumer Goods and FMCG

- Food and Beverages

- More

- By Logistics Model

- Asset-Light (Management-Based)

- Asset-Heavy (Own Fleet and Warehouses)

- Hybrid

- By Emirate

- Dubai

- Abu Dhabi

- Sharjah

- Rest of UAE

Detailed Research Methodology and Data Validation

Primary Research

Semi-structured interviews with managers at freight forwarders, free-zone warehouse operators, e-commerce merchants, and procurement heads across Dubai, Abu Dhabi, and Sharjah refined service mix ratios, contract pricing progression, and asset utilization. Follow-up surveys with pharma and FMCG shippers gauged cold-chain uptake and last-mile outsourcing intent, adding firsthand consensus to desk findings.

Desk Research

Mordor analysts compiled macro and trade indicators from tier-one public sources such as UAE Federal Competitiveness & Statistics Centre, Dubai Customs TEU tables, Central Bank monthly exchange series, IATA freight-ton-kilometer dashboards, and Emirates NBD PMI prints, which clarify demand pulses across manufacturing and retail. Company filings, port operator presentations, and association notes (FIATA, TIACA) helped benchmark 3PL contract wins and warehouse stock. Shipment splits and operator financials were cross-checked on D&B Hoovers and Volza. The sources quoted here illustrate the spectrum; many others informed data capture, validation, and gap checks.

Market-Sizing & Forecasting

A top-down construct starts with Dubai Customs and Abu Dhabi Ports cargo volumes, e-commerce parcel counts, and free-zone warehouse permits, which are then apportioned by average logistics spend coefficients from shipper interviews. Select bottom-up checks, sampled 3PL revenue roll-ups and lane-level rate cards, validate and adjust totals. Key variables steering the model include container throughput growth, cross-border e-commerce GMV, fuel-adjusted road freight tariffs, warehouse rent indices, regulatory incentives under the UAE Logistics Strategy 2030, and project timetables for the GCC rail link. Forecasts are generated through multivariate regression blended with scenario analysis, with elasticities derived from five-year historical relationships and expert sentiment guiding the base case. Where operator data are partial, gaps are bridged using peer-derived service mix averages.

Data Validation & Update Cycle

Outputs pass variance and anomaly screens, after which a senior analyst reviews assumptions against external benchmarks. We refresh every twelve months, with interim updates triggered by currency swings above 5%, material policy shifts, or significant M&A, ensuring clients receive the latest calibrated view before release.

Why Mordor's UAE Third Party Logistics Baseline Commands Reliability

Published estimates often vary because publishers pick different service baskets, base years, or price assumptions.

Key gap drivers we observe include inclusion of courier express parcel and 4PL revenues, omission of value-added warehousing, differing currency conversion dates, and uneven refresh cadences.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.10 B (2025) | Mordor Intelligence | |

| USD 6.56 B (2024) | Regional Consultancy A | Adds 4PL and CEP turnover, earlier fiscal close |

| USD 5.78 B (2024) | Trade Journal B | Excludes warehousing income, relies on press releases |

| USD 7.50 B (2024) | Global Consultancy C | Converts at spot FX, counts freight forwarding contracts |

The comparison shows how scope breadth, pricing treatments, and update timing inflate or deflate totals. By anchoring estimates to clearly defined services, audited trade volumes, and an annual refresh discipline, Mordor Intelligence offers decision-makers a balanced, transparent baseline they can trace back to measurable UAE-specific drivers.

Key Questions Answered in the Report

What is the forecast value of the UAE 3PL market in 2031?

The market is projected to reach USD 8.82 billion by 2031 based on a 9.52% CAGR.

Which service segment is growing fastest in UAE third-party logistics?

Value-Added Warehousing and Distribution is expected to expand at a 10.03% CAGR through 2031.

How big is Dubai’s share of national 3PL activity?

Dubai accounted for 66.12% of shipments and contract revenue in 2025.

Why is healthcare logistics a priority for providers?

Regulatory standards and cold-chain demand push Life Sciences & Healthcare to a 12.84% CAGR, the fastest among end-user sectors.

What model is replacing pure asset-light strategies?

Hybrid approaches that blend selective facility ownership with network management are scaling at 9.91% CAGR.

Page last updated on: