Middle East Third-Party Logistics (3PL) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

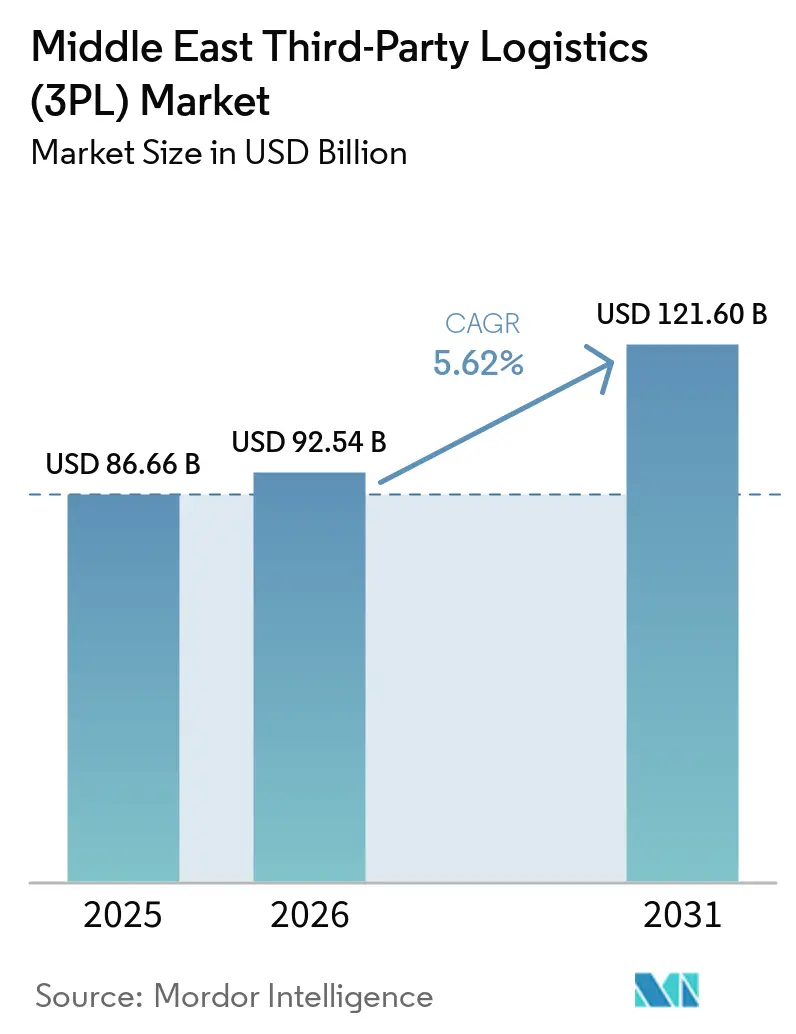

| Base Year Market Size (2025) | USD 86.66 Billion |

| Market Size (2026) | USD 92.54 Billion |

| Market Size (2031) | USD 121.60 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

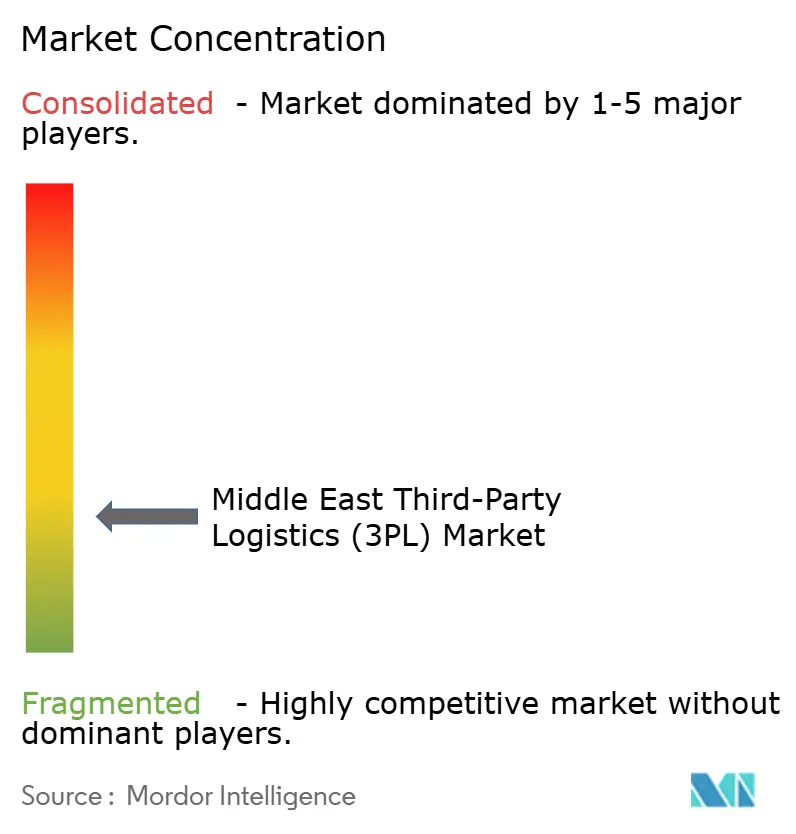

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Third-Party Logistics (3PL) Market Analysis by Mordor Intelligence

The Middle East Third-Party Logistics Market size is expected to increase from USD 86.66 billion in 2025 to USD 92.54 billion in 2026 and reach USD 121.60 billion by 2031, growing at a CAGR of 5.62% over 2026-2031.

Softer oil demand, diversified manufacturing growth, and steady e-commerce adoption underpin the trajectory, while clients now rank regulatory compliance, ESG reporting, and real-time visibility ahead of pure freight-rate considerations. Green Sukuk placements worth USD 2.5 billion during 2024 financed solar-powered warehouses and electric truck rollouts, signaling capital-market preference for sustainable logistics assets. Small-parcel volumes on Turkey-GCC lanes expanded after trade accords cut customs times to 12-18 hours, driving demand for bonded sortation hubs. Hydrogen mega-projects at NEOM and Duqm add project-cargo pipelines for cryogenic equipment, reinforcing the shift from commoditized trucking toward specialized, technology-enabled service lines.

Key Report Takeaways

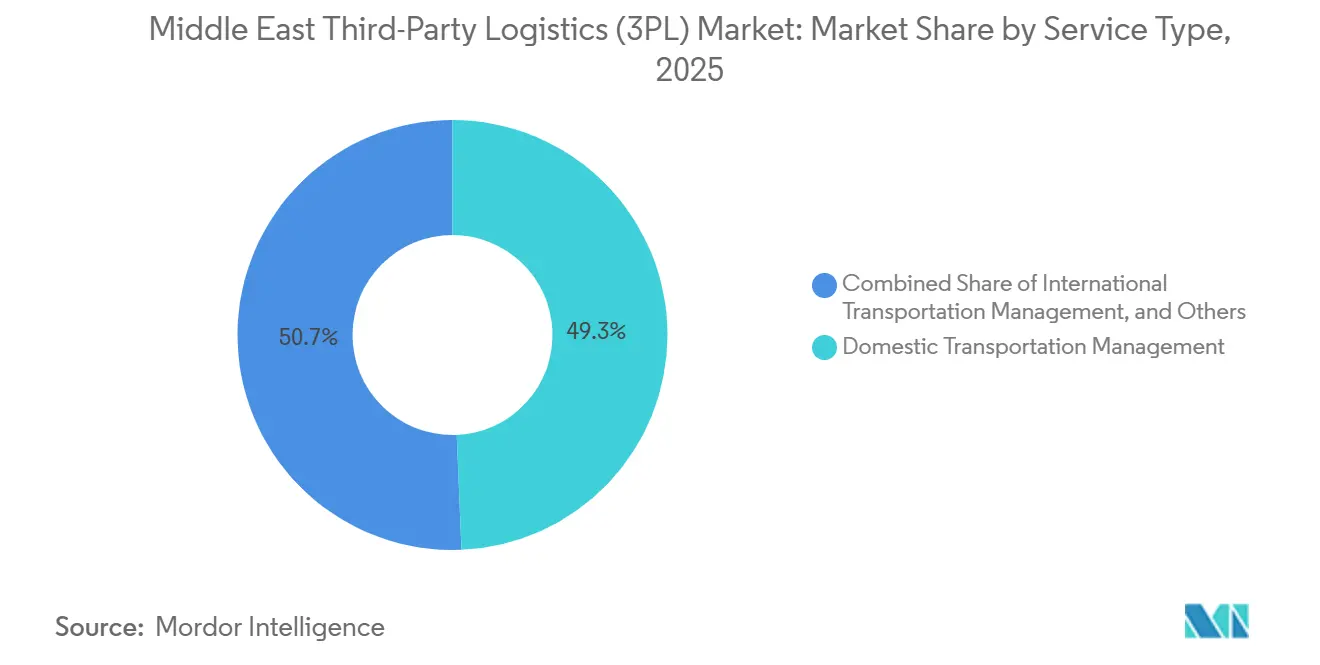

- By service, domestic transportation management led with 49.34% of the Middle East third-party logistics market share in 2025, while value-added warehousing and distribution is forecast to post the fastest 6.98% CAGR through 2031.

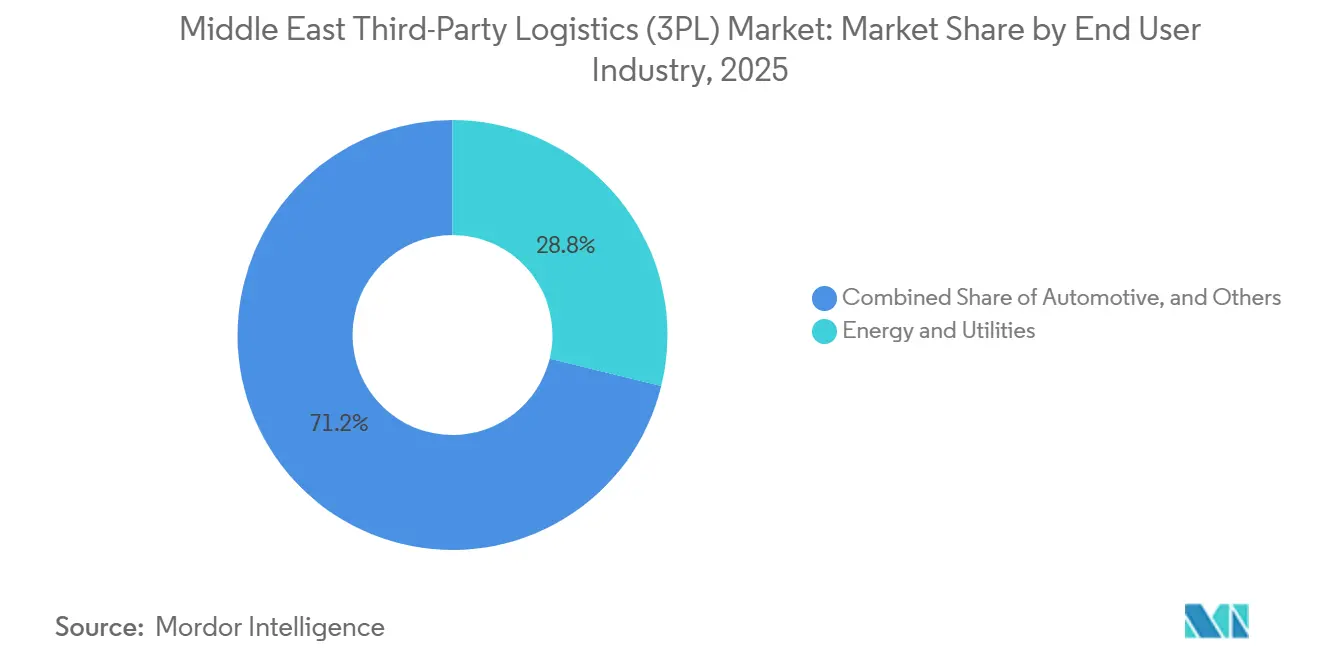

- By end-user industry, energy and utilities held 28.82% market share in 2025; e-commerce is projected to accelerate at a 7.91% CAGR to 2031.

- By logistics model, hybrid setups commanded 45.53% market share in 2025, although asset-light management-based models are expanding at 6.23% CAGR during the forecast period.

- By geography, Saudi Arabia accounted for 25.41% of the Middle East third-party logistics market size in 2025, whereas the UAE is advancing at a 7.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Third-Party Logistics (3PL) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Turkey-GCC cross-border e-commerce accords accelerating small-parcel flows | +1.2% | Turkey-UAE-Saudi Arabia corridors with spillover to Qatar, Kuwait | Short term (≤ 2 years) |

| Green Sukuk financing spurring roll-out of solar-powered, ESG-certified warehouses | +0.9% | Saudi Arabia, UAE with regional demonstration effects | Medium term (2-4 years) |

| Hydrogen export mega-projects (NEOM, Oman) generating demand for cryogenic bulk-gas logistics | +0.7% | Saudi Arabia, Oman with port infrastructure linkages | Long term (≥ 4 years) |

| Mandatory GS1 serialization in Saudi pharma supply chain expanding compliance-ready 3PL contracts | +0.8% | Saudi Arabia with GCC regulatory harmonization potential | Short term (≤ 2 years) |

| Dark-store instant-grocery start-ups outsourcing hyper-local fulfilment to 3PL micro-hubs | +1.0% | UAE, Saudi Arabia metropolitan areas with regional expansion | Short term (≤ 2 years) |

| UAE aerospace and satellite-assembly clusters driving growth in project-cargo 3PL services | +0.6% | UAE with regional aerospace supply chain linkages | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Turkey-GCC Cross-Border E-commerce Accords Accelerating Small-Parcel Flows

Bilateral facilitation agreements slashed customs clearance from as high as 72 hours to 12-18 hours in 2024, which triggered a surge in Turkish e-commerce exports valued at USD 4.2 billion. Faster clearance reshaped the cost curve for air freight and automated sortation, letting 3PLs invest in bonded facilities near Turkish free-zone airports. Consolidated pre-cleared shipments now trim logistics costs by up to 30%, redirecting Gulf online retailers toward Turkey as a China-plus-one sourcing base. Dubai and Abu Dhabi serve as transshipment nodes, amplifying parcel densities that feed regional last-mile networks. Providers owning multi-country brokerage APIs are therefore winning contracts ahead of asset-heavy rivals limited to domestic fleets[1]“United Arab Emirates - Renewable Energy and Clean Energy.” U.S. International Trade Administration, trade.gov/country-commercial-guides/united-arab-emirates-renewable-energy-and-clean-energy-0.

Green Sukuk Financing Spurring Roll-out of Solar-Powered, ESG-Certified Warehouses

Islamic green instruments mobilized USD 2.5 billion for logistics assets in 2024, cutting financing costs for developers that commit to measurable carbon metrics. The Public Investment Fund’s USD 3 billion tranche earmarked a portion for LEED-rated distribution centers that underpin Vision 2030. Each facility must report energy intensity and renewable-power share, which embeds third-party audits into everyday operations. Larger 3PLs with in-house sustainability teams gain an edge, while smaller operators struggle with verification fees. In the UAE, a planned 500,000 sqm solar-powered park showcases how public-private initiatives reset the minimum ESG standard clients now expect.

Hydrogen Export Mega-Projects Generating Demand for Cryogenic Bulk-Gas Logistics

NEOM’s USD 8.4 billion plant targets 600 t/day of green hydrogen by 2026, requiring heavy-lift routes for electrolyzers and minus-253 °C tanks that only a handful of certified 3PLs can handle. Oman’s Duqm zone adds similar demand across 150 km² of new infrastructure. The complexity of cryogenic transfers limits eligible carriers, forcing EPC contractors to lock in multi-year logistics contracts early. Providers able to marry project-cargo engineering with regulatory conformity are securing double-digit margin deals unreachable in commoditized freight markets. Knowledge gained positions them for future hydrogen corridors in Europe and Asia[2]“NEOM Hydrogen Project Logistics Infrastructure,” WALL STREET JOURNAL, wsj.com.

Mandatory GS1 Serialization in Saudi Pharma Supply Chains

The Saudi Food and Drug Authority imposed January 2025 deadlines for unit-level traceability, converting warehouses into regulated data centers alongside physical storage. Contract renewals hinge on audit readiness, so manufacturers now pay premiums for 3PLs with scanner infrastructure, secure databases, and exception-handling protocols. End-to-end serialization boosts visibility, reduces counterfeits, and strengthens expiry management, but also raises capital barriers that squeeze smaller providers out of pharma lanes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent container-equipment imbalance inflating repositioning costs on GCC lanes | -0.9% | GCC ports with global shipping network effects | Short term (≤ 2 years) |

| Slow GCC VAT-framework harmonisation complicating bonded cross-border movements | -0.7% | GCC cross-border corridors, particularly Saudi-UAE-Qatar | Medium term (2-4 years) |

| Shortfall of pharmaceutical-grade reefer assets amid rising vaccine and biologics trade | -0.6% | Saudi Arabia, UAE with regional pharmaceutical distribution impacts | Medium term (2-4 years) |

| Escalating ransomware and cyber-intrusion risks increasing 3PL insurance premiums and downtime | -0.5% | Regional 3PL providers with global cybersecurity threat landscape | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Container-Equipment Imbalance Inflating Repositioning Costs on GCC Lanes

Empty-equipment transfers now cost importers USD 400-600 per TEU as Red Sea detours reduce inbound container pools. Carriers pass part of the burden to 3PLs locked in fixed-price contracts, eroding margins. Gulf import dominance versus lower export flows sustains the deficit, while alternative break-bulk solutions are unviable for FMCG shippers. Providers with repositioning alliances or container-sharing platforms can contain costs, but most mid-tier players face profitability headwinds until fleet geography normalizes[3]“2024 Investment Climate Statements: Qatar.” U.S. Department of State, www.state.gov/reports/2024-investment-climate-statements/qatar .

Slow GCC VAT-Framework Harmonization Complicating Bonded Cross-Border Movements

Cross-border logistics operations face compliance challenges due to varying VAT timelines and rates among Gulf Cooperation Council states. Goods moving between Saudi Arabia (15% VAT), UAE (5% VAT), and Bahrain (10% VAT) necessitate specific documentation, bonded warehouse procedures, and tax reconciliation. This not only heightens administrative overhead but also extends transit times. Furthermore, the absence of a unified VAT treatment for in-transit bonded goods compels 3PL providers to adopt distinct compliance procedures for each GCC market. This fragmentation diminishes operational efficiency and elevates error rates in tax documentation, potentially leading to customs delays and penalties[4]“2024 | United States Trade Representative.” U.S. Trade Representative, ustr.gov/about/policy-offices .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Compliance Complexity Elevates VAWD Premium

Value-added warehousing and distribution is set to grow at a 6.98% CAGR through 2031 as clients prioritize regulatory compliance, serialization tracking, and ESG certification. This shift has moved competition from cost-per-pallet metrics to audit-readiness and technology integration. International transportation management faces challenges like container equipment imbalances and geopolitical uncertainties, but providers with multimodal coordination capabilities can differentiate by optimizing real-time capacity and costs. Domestic transportation management, projected to hold a 49.34% of the Middle East third-party logistics market share in 2025, benefits from e-commerce growth and quick commerce demands, though driver shortages and fuel cost volatility are squeezing margins on fixed-price contracts.

In pharmaceutical logistics, GS1 serialization integration within VAWD operations ensures compliance while improving inventory visibility and stock rotation. GCC ports, positioned as transshipment hubs, support sea freight coordination, but container shortages limit capacity and increase spot-rate volatility. Air freight services, crucial for time-sensitive pharmaceutical and aerospace cargo, face bottlenecks due to regional airport capacity constraints. Road transportation in GCC markets benefits from better highway infrastructure and cross-border facilitation but struggles with rising costs from driver nationalization mandates and licensing restrictions.

By End-User Industry: E-Commerce Disrupts Energy Dominance

E-commerce is set to grow at a 7.91% CAGR through 2031, driven by quick commerce platforms requiring micro-fulfillment networks and creating opportunities for 3PL providers investing in urban warehouses and last-mile delivery. The energy and utilities sectors are expected to hold a 28.82% of the Middle East third-party logistics market size in 2025, supported by specialized handling of oilfield supplies and petrochemical intermediates, ensuring contract stability. Retail and e-commerce convergence allows 3PL providers to optimize operations by combining store replenishment and direct-to-consumer fulfillment, reducing costs and improving asset utilization.

Life sciences and healthcare logistics are thriving due to pharmaceutical serialization mandates and vaccine distribution, favoring 3PL providers with GDP-compliant cold-chain capabilities. The automotive sector is shifting to electric vehicle components, requiring new handling protocols for lithium-ion batteries. Manufacturing logistics are expanding in Gulf states, driven by growth in food processing and pharmaceutical production. Technology and electronics sectors are benefiting from data center expansions, while food and beverage logistics increasingly demand halal certification and temperature-controlled capabilities, creating specialization opportunities for 3PL providers.

By Logistics Model: Asset-Light Acceleration Challenges Hybrid Dominance

As geopolitical uncertainties and fluctuating demand reshape corporate strategies, asset-light management models are gaining traction, projected to grow at a 6.23% CAGR through 2031. These models prioritize operational flexibility over capital-intensive commitments, offering businesses the agility to adapt. Hybrid logistics models, expected to hold 45.53% market share by 2025, strike a balance by owning critical assets for core operations while leveraging third-party capacities for peak demands and specialized needs. In contrast, asset-heavy models face challenges from rising real estate costs and regulatory pressures but remain essential in sectors requiring dedicated cold-chain facilities and bonded warehouses, where long-term contracts justify their investments.

The rise of asset-light models creates opportunities for technology-driven 3PL providers that use digital platforms to optimize routes, aggregate capacity, and manage client interfaces without significant infrastructure investments. These platforms enable rapid expansion and service diversification, which traditional asset-heavy models cannot match. Regional 3PLs are increasingly adopting hybrid strategies, owning strategic assets like bonded warehouses while outsourcing transportation and seasonal capacity. The success of asset-light models depends on advanced technologies, including real-time visibility systems, predictive analytics, and digital customer portals, which foster client loyalty through seamless integration rather than asset ownership.

Geography Analysis

Saudi Arabia held 25.41% of the Middle East third-party logistics market size in 2025, supported by Vision 2030 investments, pharma serialization, and hydrogen project cargo. Riyadh’s focus on compliance raises barriers for new entrants lacking audit pedigrees.

The UAE is pacing at a 7.50% CAGR through 2031, fueled by Jebel Ali’s 14.1 million TEU throughput in 2024 and aerospace cluster expansion. Dubai’s free-zone incentives facilitate regional distribution, while Abu Dhabi’s satellite assembly spurs niche logistics demand.

Turkey’s customs-time cuts reinforce its role as a manufacturing springboard into the Gulf, while Oman’s Duqm SEZ positions the sultanate as an emerging hydrogen logistics hub. Egypt, Qatar, Bahrain, and Kuwait each offer targeted opportunities tied to infrastructure legacies, financial services, or petrochemical chains. Ongoing GCC fast-track transit initiatives should gradually level cross-border friction, benefiting providers with multi-country operations.

Competitive Landscape

Market rivalry is migrating from fleet size to compliance, technology, and ESG credentials. International heavyweights combine cloud platforms with local partnerships, evidenced by the USD 5 billion GLIDE vehicle from Blackstone and Lunate announced in 2025. Regional champions leverage government ties and cultural fluency to keep multinationals at bay in regulated niches.

White-space arenas include cryogenic hydrogen moves, aerospace project-cargo, pharma serialization, and micro-fulfillment management. DHL’s EUR 130 million (USD 152.92 million) automated warehouse at King Abdullah Port exemplifies scale players’ response: robotics, AI inventory control, and rooftop solar raise operational baselines.

Cybersecurity now factors into RFP scoring as ransomware premiums climb. Providers investing in ISO 27001 data centers and emergency response teams secure multi-year deals, whereas smaller firms often struggle to fund comparable coverage.

Middle East Third-Party Logistics (3PL) Industry Leaders

Aramex

Gulf Agency Company (GAC)

Almajdouie Logistics

Al-Futtaim Logistics

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Aramex inaugurated its inaugural regional hub at the Dubai South Free Zone, specifically tailored for healthcare and pharmaceuticals, enhancing its specialized 3PL offerings for the life sciences domain.

- January 2026: Aramex selected Softeon to implement a Warehouse Management System (WMS) across 70+ facilities globally. The system improved efficiency in Middle East operations and expedited client onboarding for e-commerce, healthcare, and retail clients.

- November 2025: DHL committed EUR 130 million (USD 152.92 million) to a 67,000 sqm automated, solar-powered warehouse at King Abdullah Port.

- October 2025: Blackstone and Lunate formed GLIDE, a USD 5 billion logistics platform targeting MENA acquisitions.

Middle East Third-Party Logistics (3PL) Market Report Scope

| Domestic Transportation Management | Road |

| Air | |

| Others | |

| International Transportation Management | Road |

| Air | |

| Sea | |

| Multimodal / Intermodal | |

| Value-Added Warehousing and Distribution (VAWD) |

| Automotive |

| Energy and Utilities |

| Manufacturing |

| Life Sciences and Healthcare |

| Technology and Electronics |

| E-commerce |

| Consumer Goods and FMCG |

| Food and Beverages |

| Others |

| Asset-Light (Management-Based) |

| Asset-Heavy (Own Fleet and Warehouses) |

| Hybrid |

| United Arab Emirates |

| Saudi Arabia |

| Turkey |

| Egypt |

| Qatar |

| Bahrain |

| Kuwait |

| Oman |

| Rest of Middle East |

| By Service | Domestic Transportation Management | Road |

| Air | ||

| Others | ||

| International Transportation Management | Road | |

| Air | ||

| Sea | ||

| Multimodal / Intermodal | ||

| Value-Added Warehousing and Distribution (VAWD) | ||

| By End-User Industry | Automotive | |

| Energy and Utilities | ||

| Manufacturing | ||

| Life Sciences and Healthcare | ||

| Technology and Electronics | ||

| E-commerce | ||

| Consumer Goods and FMCG | ||

| Food and Beverages | ||

| Others | ||

| By Logistics Model | Asset-Light (Management-Based) | |

| Asset-Heavy (Own Fleet and Warehouses) | ||

| Hybrid | ||

| By Country | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| Qatar | ||

| Bahrain | ||

| Kuwait | ||

| Oman | ||

| Rest of Middle East | ||

Key Questions Answered in the Report

What is the projected value of the Middle East third-party logistics market by 2031?

It is forecast to reach USD 121.60 billion by 2031.

Which service line is growing fastest in the region?

Value-added warehousing and distribution is expanding at 6.98% CAGR to 2031.

Why are asset-light logistics models gaining traction?

Shippers favor flexible, variable-cost structures amid geopolitical and demand uncertainty, driving a 6.23% CAGR for management-based models.

How do green Sukuk influence logistics infrastructure?

They lower financing costs for solar-powered, ESG-certified warehouses, raising sustainability standards across new projects.

Which corridor offers the strongest short-term growth for small-parcel flows?

The Turkey-GCC trade lane, thanks to customs accords cutting clearance times to under 18 hours.

Page last updated on: