Satellite Telemetry And Control Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.65 Billion |

| Market Size (2030) | USD 6.40 Billion |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

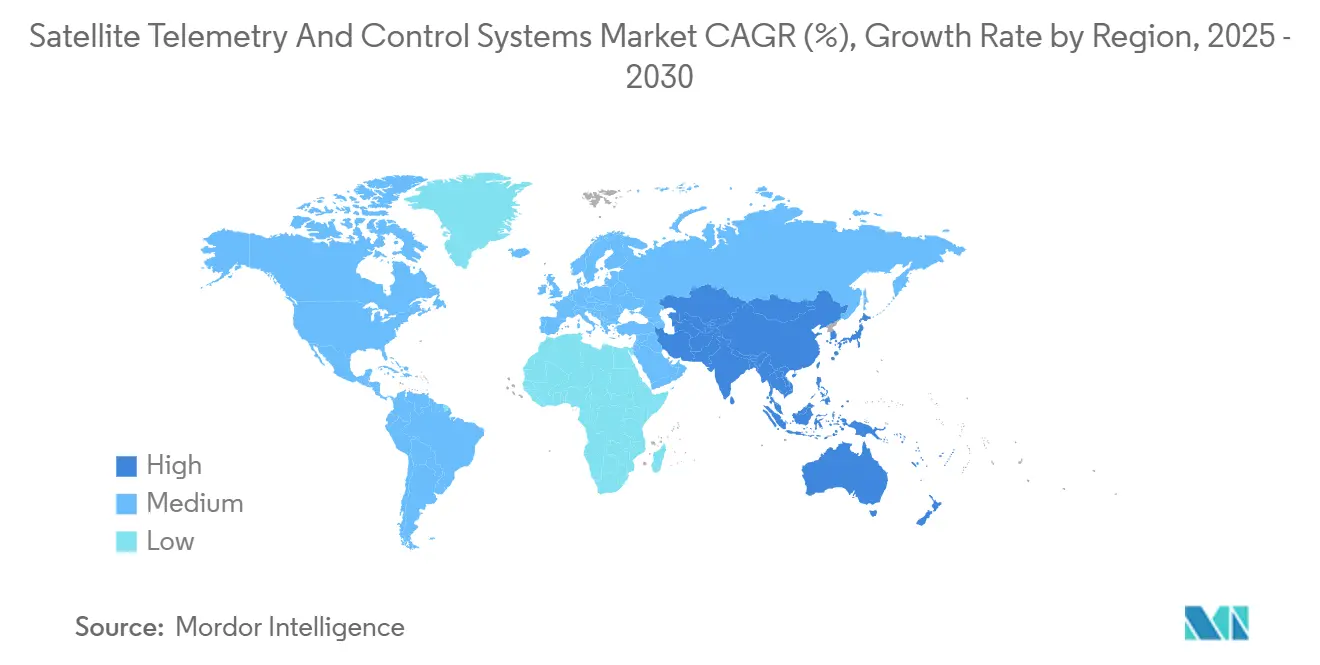

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

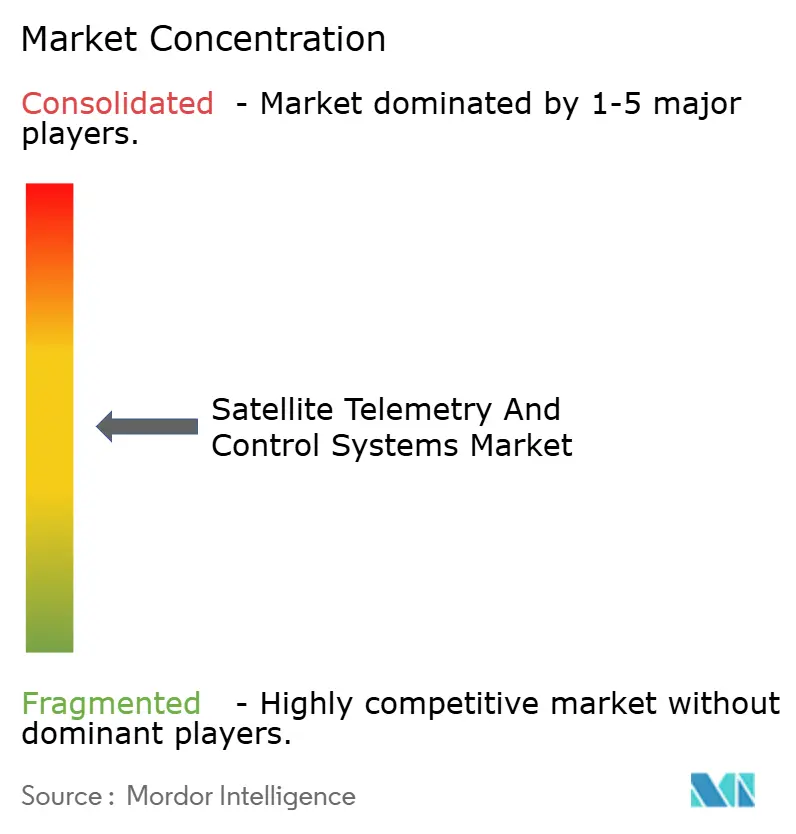

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Telemetry And Control Systems Market Analysis by Mordor Intelligence

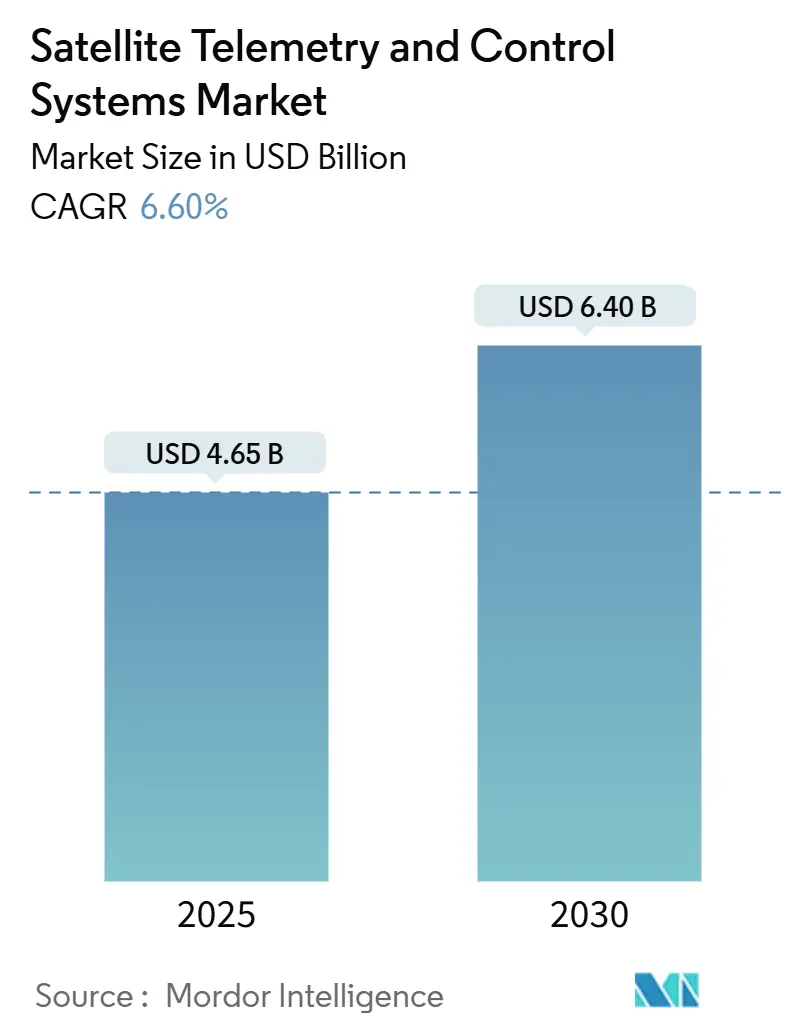

The satellite telemetry and control systems market size was valued at USD 4.65 billion in 2025, and it is forecasted to climb to USD 6.40 billion by 2030, advancing at a 6.60% CAGR. Current growth reflects a decisive swing from hardware-centric ground stations toward cloud-native, software-defined architectures that streamline multi-orbit fleet management, dynamic spectrum use, and autonomous operations. The brisk expansion of small-satellite constellations and defense agencies’ emphasis on secure command link underpins demand across all regions. Commercial operators add further momentum as ground-software-as-a-service (GSaaS) platforms reduce capital outlays and accelerate constellation deployment cycles. In parallel, higher-frequency Ka and V band technologies, AI-driven analytics, and policy incentives for space-debris mitigation sharpen the competitive edge for vendors that can blend hardware reliability with scalable software control.

Key Report Takeaways

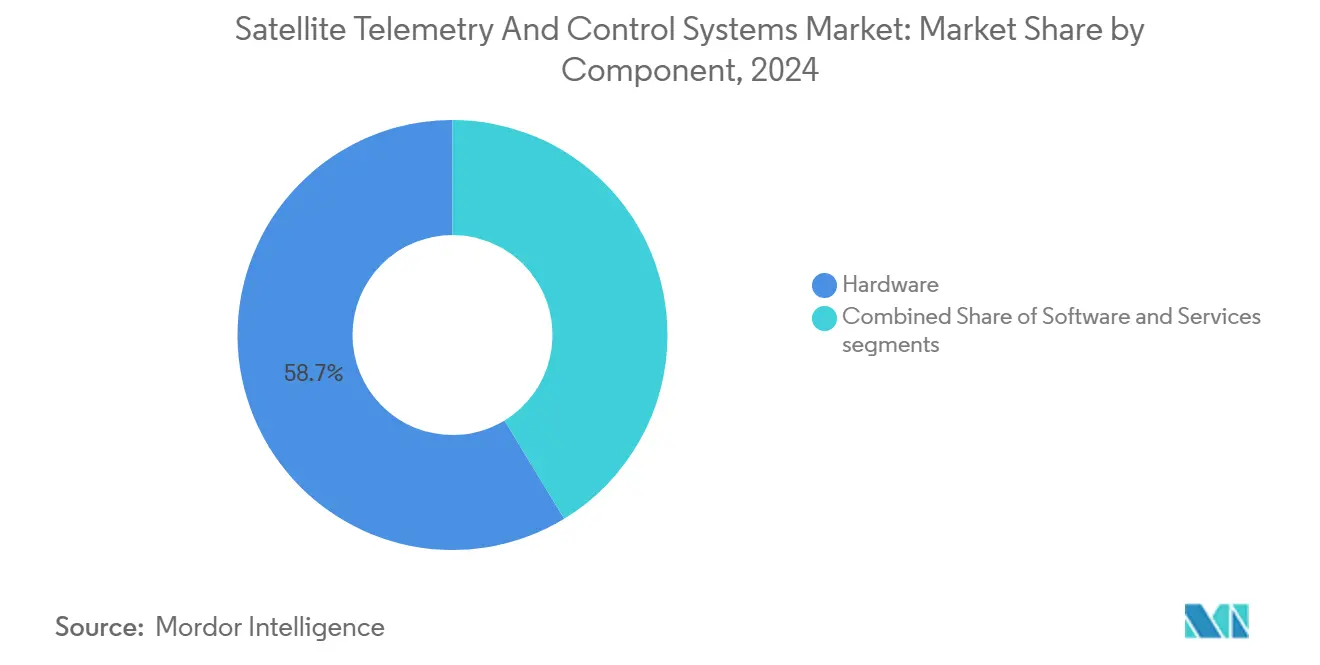

- By component, hardware retained 58.70% of the market share of the satellite telemetry and control systems in 2024; software is projected to deliver a 9.42% CAGR through 2030.

- By solution type, ground-segment products held 46.20% revenue share in 2024, while GSaaS offerings are expected to expand at an 11.40% CAGR to 2030.

- By orbit, low-Earth-orbit (LEO) applications accounted for a 62.40% share of the satellite telemetry and control systems market size in 2024. In contrast, highly elliptical orbit (HEO) solutions are set to grow at 10.80% CAGR through 2030.

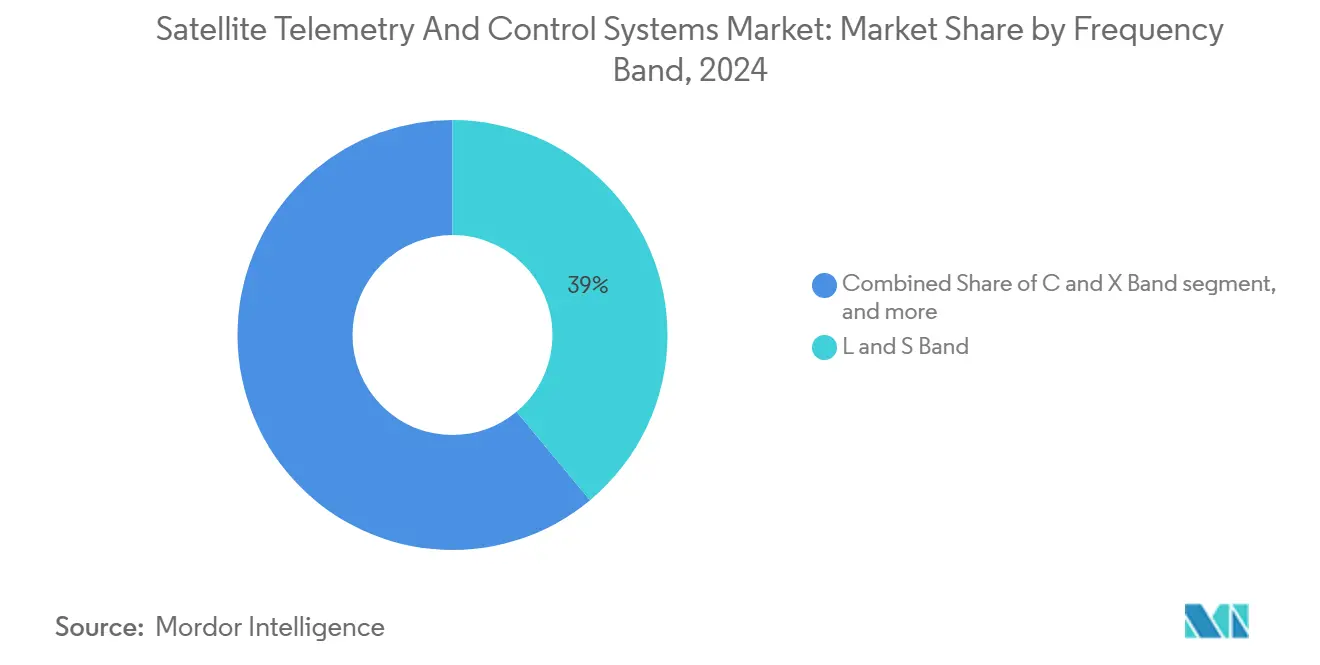

- By frequency band, the L/S-band segment led 38.95% of the satellite telemetry and control systems market size in 2024; Ka/V-band platforms should register a 10.98% CAGR between 2025 and 2030.

- By application, government and defense captured 43.25% of market demand in 2024, yet commercial communications is on track for a 9.55% CAGR to 2030.

- By end-user, satellite operators controlled a 34.55% share in 2024, but commercial enterprises are forecast to post a 9.20% CAGR through 2030.

- By geography, North America led with 39.80% revenue share in 2024; Asia-Pacific is primed for the fastest 8.90% CAGR over 2025-2030.

Global Satellite Telemetry And Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of small-sat constellations | +1.8% | Global with focus in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising defense spend on secure C2 links | +1.2% | North America, Europe, Asia-Pacific defense corridors | Long term (≥ 4 years) |

| Advances in software-defined ground stations | +1.0% | Global, early adoption in North America and Europe | Short term (≤ 2 years) |

| GSaaS business models lowering CAPEX | +0.9% | Global, strong uptake in emerging markets | Medium term (2-4 years) |

| AI-driven autonomous telemetry, tracking, and command (TT&C) operations | +0.7% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Regulatory push for debris-avoidance telemetry | +0.5% | Global, led by FCC, ESA, national space agencies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Small-Sat Constellations

Active satellites are set to soar from roughly 8,000 in 2024 to well above 100,000 by 2030, amplifying requirements for scalable ground networks and automated telemetry processing. Starlink manages more than 7,000 platforms alone, while Project Kuiper has regulatory approval for 3,236 satellites with demonstrated 100 Gbps optical inter-satellite links. Control architectures must now orchestrate thousands of contacts per day, handle complex orbital mechanics, and execute AI-enabled collision-avoidance routines. ESA’s AIKO framework validated autonomous decision-making in 2024, shifting toward machine-scale constellation governance.[1]Source: ESA Communications Department, “AIKO Autonomous Operations Demonstration,” esa.int

Rising Defense Spend on Secure C2 Links

Geopolitical tensions elevated space assets to critical-infrastructure status, prompting record US and European outlays for resilient satellite communications. NASA’s Communications Services Project awarded USD 278.50 million in 2024 to begin replacing government-owned links with commercial solutions, and long-term allocations exceed USD 1.5 billion. Military users now specify anti-jam waveforms, quantum-secure encryption, and multi-orbit redundancy. The US Space Force acquisition strategy and Europe’s IRIS² initiative illustrate stable, multi-year procurement pipelines for hardened telemetry networks.[2]Source: NASA Headquarters, “Commercial Communications Services Project Awards,” nasa.gov

Advances in Software-Defined Ground Stations

Field-programmable radios combined with cloud orchestration cut traditional ground-station costs by allowing a single antenna to support multiple bands and waveforms. Operators can reconfigure spectrum, modulation, and routing through software updates without swapping hardware. Commercial networks integrate dynamically with public-cloud marketplaces, letting satellite teams spin up capacity on demand. This flexibility supports frequency agility during launch campaigns, minimizes interference risk, and enables time-shared antennas for disparate constellations.

GSaaS Business Models Lowering CAPEX

GSaaS converts multimillion-dollar capital budgets into pay-as-you-go operating expenses. Providers aggregate geographically dispersed antennas, deliver secure VPN backhaul, and expose standardized telemetry, tracking, and command APIs. Small constellations and emerging space nations gain prompt access to global coverage without land-acquisition hurdles or export-control complexity. As GSaaS platforms expand presence in Africa, South America, and Southeast Asia, they also unlock supplementary data analytics revenue streams for weather, AIS, and EO downlinks.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ground-station CAPEX | -0.8% | Global, heavier on emerging markets and small operators | Short term (≤ 2 years) |

| Spectrum congestion and regulatory complexity | -0.6% | Global, acute in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| RF-cyber-talent shortage | -0.4% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Solar-weather-driven link unreliability | -0.3% | Global, heightened at high latitudes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Ground-Station CAPEX

A modern multiband tracking site can cost USD 5–15 million before land and licensing, stifling market entry for small developers. Operators seeking global coverage must duplicate facilities across jurisdictions, compounding capital needs and navigating divergent export controls. Although GSaaS offers relief, mission-critical or classified traffic still demands dedicated infrastructure with hardened cybersecurity and cleared personnel, limiting the reach of purely shared models.

Spectrum Congestion and Regulatory Complexity

As mega-constellations burgeon, International Telecommunication Union coordination queues lengthen, and national regulators grapple with cross-border interference. Terrestrial 5G encroaches on legacy satellite bands, while power-flux limits restrain in-orbit transmitters. Technology exists for dynamic spectrum sharing, but the absence of a harmonized policy slows rollout and burdens operators with multi-standard compliance paperwork.[3]Source: Federal Communications Commission, “Spectrum Sharing and Supplemental Coverage from Space,” fcc.gov

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Growth Outpaces Hardware Dominance

Hardware preserved a 58.70% share of the satellite telemetry and control systems market size in 2024 as antennas, RF chains, and tracking mounts remain mission-critical. However, software revenue is slated for a 9.42% CAGR due to cloud orchestration, AI-fault diagnostics, and containerized waveform libraries. Leading ground-station platforms now bundle real-time visualization dashboards, API access, and automated pass scheduling, converting bare-metal installations into service-friendly environments. Hardware roadmaps increasingly emphasize modularity, enabling field upgrades that sustain compatibility with evolving software stacks while curbing lifecycle costs.

Open-standard protocol converters and virtual digital signal processors allow operators to pivot between S-band TT&C and Ka-band payload downlinks without physical swaps. This flexibility enhances spectral efficiency, accommodates future encryption mandates, and future-proofs investments as the satellite telemetry and control systems market shifts further toward software-centric value creation.

By Solution Type: GSaaS Disrupts Traditional Ground-Segment Models

Ground-segment solutions captured 46.20% revenue in 2024, yet GSaaS offerings are forecasted as the segment’s 11.40% CAGR pacesetter. Established teleport operators now license software stacks that expose secure REST endpoints for pass booking, data delivery, and billing, letting microsatellite startups spin up global coverage in weeks instead of years. Satellite-bus subsystems remain indispensable for spacecraft command. However, their firmware increasingly integrates cloud-native hooks that report health data directly into operator dashboards, shrinking the divide between on-orbit assets and terrestrial networks.

As GSaaS networks proliferate, hybrid deployments emerge: strategic sites host sovereign or classified traffic, while non-sensitive downlinks flow through shared assets. Vendors that architect seamless hand-off between dedicated and pay-per-use antennas stand to capture a broader slice of the satellite telemetry and control systems market demand, particularly among enterprises that need strict data-residency compliance in certain regions.

By Orbit: LEO Dominance Challenged by HEO Innovation

LEO fleets held 62.40% of the satellite telemetry and control systems market share in 2024, a dominance powered by broadband mega-constellations. Yet highly elliptical orbits are growing at a faster 10.80% CAGR because operators seek continuous coverage above 65° latitude, where geostationary earth orbit (GEO) visibility diminishes. HEO architectures linger for hours over polar regions, supporting logistics, research bases, and defense commands. Corresponding telemetry systems must accommodate rapid Doppler shifts at perigee and radiation-belt transits, spawning niche demand for robust tracking filters and adaptive coding.

While LEO remains central for global internet roll-outs, convergence is imminent: multi-orbit terminals capable of roaming between GEO, LEO, and HEO links will dominate future procurement cycles, embedding flexibility into fleet control frameworks and broadening the addressable satellite telemetry and control systems market.

By Frequency Band: Ka/V Band Innovation Drives Adoption

Due to favorable rain fade characteristics and widespread terminal bases, L/S-band domains maintained a 38.95% share of the satellite telemetry and control systems market size in 2024. Nevertheless, Ka/V-band traffic is marching at 10.98% CAGR, propelled by high-throughput requirements and advanced phased-array designs that compress antenna footprints. IEEE research has demonstrated Ka-band monolithic microwave integrated circuits surpassing 80% power-added efficiency, mitigating previous cost hurdles.

Successful Ka-band deployments pair adaptive coding with cloud-based fade prediction to reroute high-volume data when atmospheric loss exceeds tolerance. These innovations unlock spectrum efficiency essential for constellations that plan terabit-per-second aggregate capacity. Vendors that deliver dual-band or tri-band transceivers with software-selectable channels will benefit most as the satellite telemetry and control systems tilt toward higher frequencies.

By Application: Commercial Communications Accelerates Beyond Government Base

Government and defense users commanded 43.25% of 2024 revenue, reflecting sovereign priorities for secure command-and-control. Even so, commercial communications are projected to achieve the fastest 9.55% CAGR through 2030 as enterprises integrate satellite links into SD-WAN architectures. Retail, agriculture, and energy firms now consume GSaaS telemetry endpoints as a routine IT expense, mirroring cloud-compute adoption trajectories. Meanwhile, government customers increasingly lease capacity from commercial fleets, blending acquisition channels and spurring hybrid security accreditation frameworks.

The satellite telemetry and control systems industry players that can fuse defense-grade encryption with plug-and-play APIs will straddle both markets, capturing crossover spend and reinforcing ecosystem standardization.

By End-User: Commercial Enterprises Challenge Satellite Operator Dominance

Satellite operators still hold 34.55% market share, yet commercial enterprises are forecasted to have a 9.20% CAGR. The shift stems from IoT expansion, autonomous vehicle telemetry, and direct-to-device services that embed SATCOM chips into consumer handsets. Corporate procurement teams demand SLAs, cloud-native dashboards, and seamless integration with existing cybersecurity policies, in contrast to legacy fleet-management interfaces.

Consequently, platform vendors are tailoring user-experience layers that hide orbital mechanics, present RESTful command calls, and offer pay-per-bit billing. That democratization enlarges the satellite telemetry and control systems market without cannibalizing operator demand, because operators simultaneously rely on such platforms to scale their own fleets economically.

Geography Analysis

North America controlled 39.80% of 2024 revenue as mature aerospace supply chains, robust venture funding, and established defense budgets converged. NASA’s commercial services contracts and FCC debris-mitigation rules shape product requirements and guarantee multi-year spending on telemetry modernization. The region also hosts the highest density of GSaaS antenna farms, enabling sub-second latency hand-offs for broadband constellations across the continental US and polar routes. Still, spectrum sharing debates in the 12–17 GHz bands and high demand for cleared RF-cyber talent temper growth projections.

Asia-Pacific is expected to clock an 8.90% CAGR through 2030, fueled by national space programs in China, India, Japan, and rising commercial ventures across Southeast Asia. India’s regulatory opening via IN-SPACe and China’s USD 20 billion space budget double-count as demand levers for hardware expansion and software control stacks. The region’s extensive archipelagos and underserved rural belts create long-tail connectivity needs that terrestrial fiber cannot meet. Local vendors embracing GSaaS partnerships are already exporting services to Africa and the Middle East, widening addressability for the Satellite Telemetry and Control Systems market.

Europe remains pivotal through ESA projects, Luxembourg-based operators, and rising sovereign constellations such as IRIS². Granular sustainability mandates advance telemetry sophistication by imposing collision-avoidance benchmarks and eco-design criteria for spacecraft propulsion. In turn, providers that certify compliance can secure preferred listings for European institutional missions. Motivated by defense imperatives, Eastern European states are also pooling resources under NATO frameworks, adding incremental opportunities for secure telemetry chains.

Competitive Landscape

The satellite telemetry and control systems market sits at a moderate concentration threshold where neither hardware incumbents nor software insurgents dominate outright. Aerospace primes like Kratos, L3Harris, and Lockheed Martin combine field-proven antennas with defensive cybersecurity suites to protect established defense contracts. However, agile GSaaS firms such as ATLAS Space Operations and Leaf Space leverage pay-per-use economics to court startup constellations and enterprises new to space.

Cross-industry entrants reshape competition. Cloud hyperscalers bundle elastic storage with direct ground-station access, turning satellite downlink into another microservice. Telecom carriers integrate multi-orbit satellite roaming to extend 5G coverage, demanding terminal interoperability and unified policy management. Standards groups under IEEE champion open SDR frameworks, accelerating vendor interchangeability and shortening procurement cycles.

M&A activity rose sharply in 2024. The proposed SES-Intelsat merger aims for multi-orbit breadth, while EchoStar’s tie-up with DISH pools L-band spectrum with extensive retail distribution. Component suppliers also consolidated to secure gallium-nitride amplifier capacity and reduce dependency on constrained semiconductor fabs. Vendors that balance the acquisitive scale with sustained R&D in AI-enabled operations will outpace rivals in capturing long-term market demand for satellite telemetry and control systems.

Satellite Telemetry And Control Systems Industry Leaders

Thales Group

Lockheed Martin Corporation

L3Harris Technologies, Inc.

Kratos Defense & Security Solutions, Inc.

General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Arianespace launched the CSO-3 military observation satellite aboard an Ariane 6 rocket. Developed by Airbus Defence & Space for France’s MUSIS* military program, CSO-3 enhances military operations with advanced coverage and revisit capabilities. Equipped with a high-resolution optical instrument and telemetry systems by Thales Alenia Space, the satellite ensures exceptional imagery, even in low-light conditions, while maintaining data security through encryption modules. It marks the final component of the CSO system.

- January 2025: Leaf Space, a leader in GSaaS solutions, collaborates with ISRO to support the SpaDeX satellites, PSLV launch vehicle tracking, and the POEM-4 platform. Leaf Space’s telemetry system enabled real-time telemetry reception, command operations, and satellite monitoring. SpaDeX, featuring two 220-kilogram spacecraft in a 470 km orbit, showcases docking, undocking, and power transfer capabilities, marking advancements critical for India’s future space initiatives like BAS and lunar missions.

Global Satellite Telemetry And Control Systems Market Report Scope

| Hardware |

| Software |

| Services |

| Ground-Segment |

| Satellite-Bus Subsystems |

| Ground Software-as-a-Service (GSaaS) |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Earth Orbit (GEO) |

| Highly Elliptical Orbit (HEO) |

| L and S Band |

| C and X Band |

| Ku Band |

| Ka and V Band |

| Government and Defense |

| Commercial Communications |

| Earth Observation / Remote Sensing |

| Navigation and Timing |

| Scientific and Deep-Space Missions |

| Satellite Operators |

| Space Agencies |

| Defense Organizations |

| Commercial Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Solution Type | Ground-Segment | ||

| Satellite-Bus Subsystems | |||

| Ground Software-as-a-Service (GSaaS) | |||

| By Orbit | Low Earth Orbit (LEO) | ||

| Medium Earth Orbit (MEO) | |||

| Geostationary Earth Orbit (GEO) | |||

| Highly Elliptical Orbit (HEO) | |||

| By Frequency Band | L and S Band | ||

| C and X Band | |||

| Ku Band | |||

| Ka and V Band | |||

| By Application | Government and Defense | ||

| Commercial Communications | |||

| Earth Observation / Remote Sensing | |||

| Navigation and Timing | |||

| Scientific and Deep-Space Missions | |||

| By End-User | Satellite Operators | ||

| Space Agencies | |||

| Defense Organizations | |||

| Commercial Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What revenue did the Satellite Telemetry and Control Systems market generate in 2025?

The satellite telemetry and control systems market size was valued at USD 4.65 billion in 2025.

How fast is the market expected to grow through 2030?

The satellite telemetry and control systems market is forecasted to climb to USD 6.40 billion by 2030, advancing at a 6.60% CAGR.

Which component segment is expanding the quickest?

Software solutions, advancing at a 9.42% CAGR on the back of AI and cloud adoption.

Why are Ka and V bands gaining momentum?

They enable higher data throughput and spectrum efficiency, supporting mega-constellation traffic while posting a 10.98% CAGR.

Which region will add the most incremental demand by 2030?

Asia-Pacific, driven by national space programs and emerging commercial operators, is projected for an 8.90% CAGR.

How are GSaaS offerings reshaping procurement models?

They turn capital-intensive ground-station builds into operational expenses, letting operators buy pass time on demand and scale globally in weeks.

Page last updated on: