Satellite Communications Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 34.28 Billion |

| Market Size (2031) | USD 52.49 Billion |

| Growth Rate (2026 - 2031) | 8.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Communications Market Analysis by Mordor Intelligence

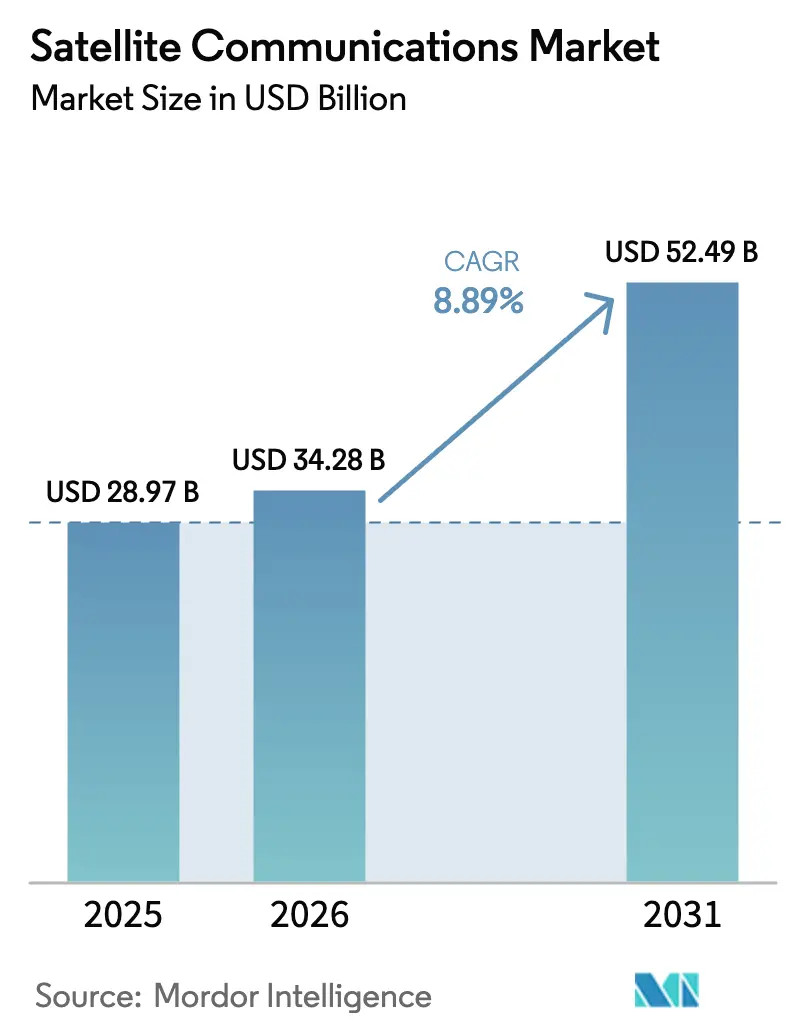

The satellite communications market size is expected to grow from USD 29.87 billion in 2025 to USD 34.28 billion in 2026 and is forecasted to reach USD 52.49 billion by 2031 at 8.89% CAGR over 2026-2031. The shift from geostationary fleets to low Earth orbit (LEO) constellations underpins this expansion, as reusable launch vehicles slash deployment costs and direct-to-device standards broaden addressable demand. Spectrum scarcity drives operators toward digital payloads and higher frequency bands, while government procurement programs mitigate the risk of commercial investment. Vertically integrated entrants now own launch, manufacturing, and ground segments, compressing time-to-orbit and reshaping cost curves across the satellite communications market.

Key Report Takeaways

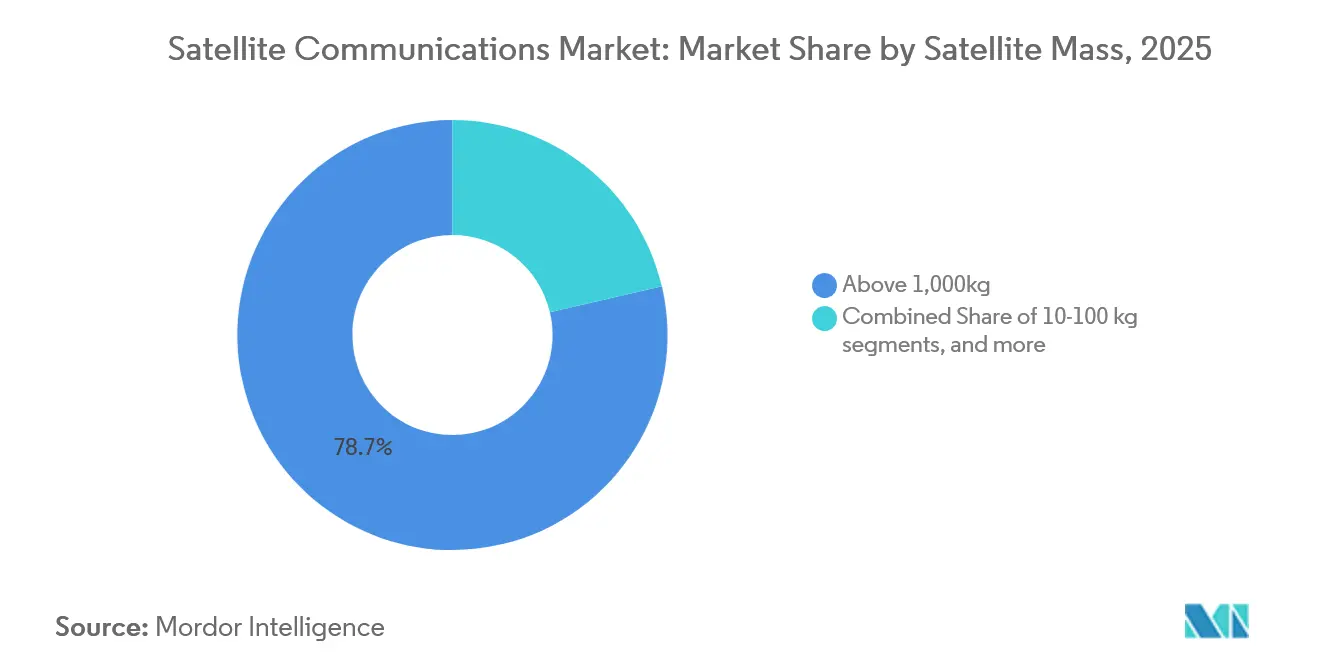

- By satellite mass, above 1,000 kg platforms held 78.65% of the satellite communications market share in 2025, whereas the 10-100 kg class is projected to advance at 8.95% CAGR through 2031.

- By orbit class, LEO systems captured a 52.85% share of the satellite communications market size in 2025, and medium Earth orbit (MEO) is expected to grow at a 9.68% CAGR through 2031.

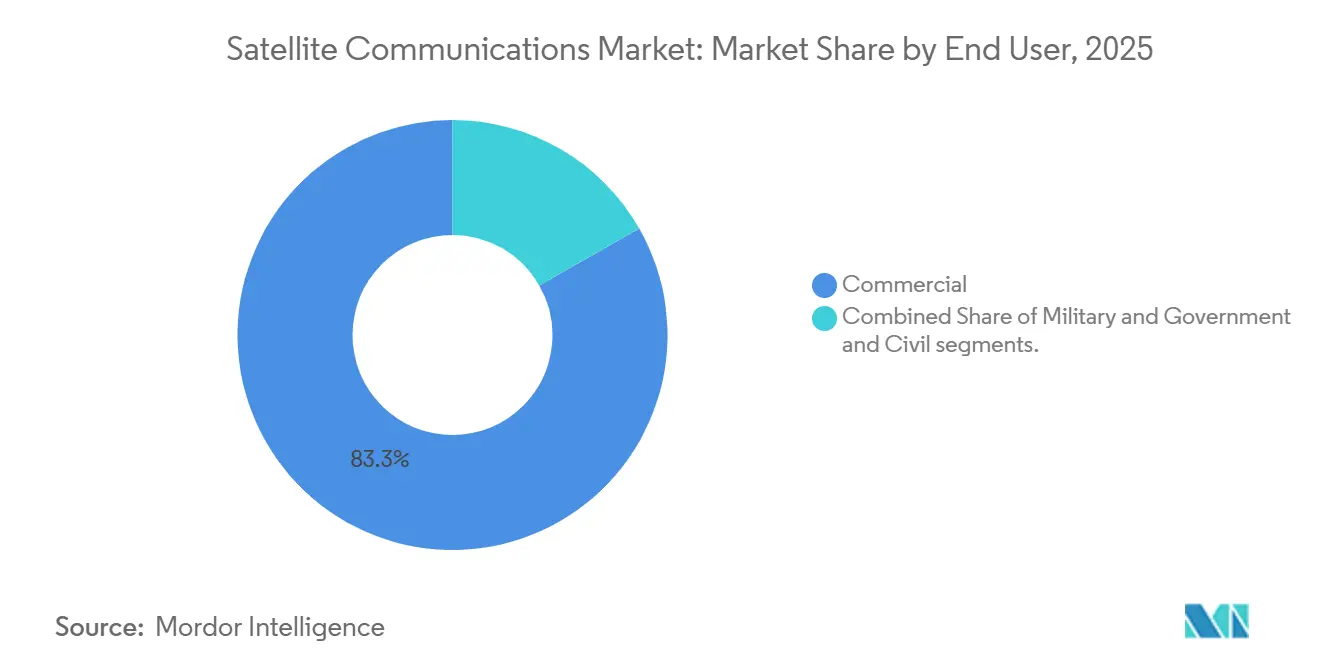

- By end user, the commercial segment commanded 83.25% share of the satellite communications market in 2025, while military and government demand is expanding at a 10.95% CAGR.

- By frequency band, L- and S-band services retained a 67.55% share in 2025, with Q/V and optical links forecasted to climb at a 9.65% CAGR.

- By geography, North America led with 51.21% satellite communications market share in 2025, although Asia-Pacific is on track for a 9.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Satellite Communications Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining launch costs and reusable rockets | +1.80% | Global, concentrated in US and China | Medium term (2-4 years) |

| Surge in LEO mega-constellations enabling global broadband | +2.20% | Global, early deployment in developed markets | Long term (≥ 4 years) |

| HTS and digital payloads driving bandwidth economics | +1.10% | Global, strongest in high-traffic corridors | Short term (≤ 2 years) |

| Direct-to-device satellite 5G standards (3GPP NTN) | +1.50% | Global, led by North America and Europe | Medium term (2-4 years) |

| Government rural-connectivity subsidies (BEAD, RDOF, EU Digital Decade) | +1.30% | North America and Europe, expanding to APAC | Short term (≤ 2 years) |

| Multi-orbit, multi-band terminals unlocking mobility markets | +0.90% | Global, concentrated in maritime and aviation sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining launch costs and reusable rockets

SpaceX reused Falcon 9 boosters 20 times each by late 2024, dropping launch economics from USD 10,000 per kilogram to USD 1,400, which opens constellations to smaller operators.[1]SpaceX, “Starlink Constellation Updates and Launch Statistics,” spacex.com Cheaper access to orbit lets manufacturers redesign buses around standardized dispensers and faster refresh cycles. Ariane 6 and reusable Long March variants intensify price competition, accelerating the rollout of satellite communications in emerging economies.[2]European Space Agency, “Ariane 6 Program Status,” esa.int Regulatory agencies now confront congested launch manifests, forcing spectrum and orbital-slot coordination to catch up.

Surge in LEO mega-constellations enabling global broadband

Starlink surpassed 5,000 active spacecraft in 2024, offering 100 Mbps service to rural households and maritime users. Amazon’s Kuiper and OneWeb add thousands more units, shifting the satellite communications market toward software-defined networks with on-board routing that mitigates interference. China’s sovereign plan for 13,000 satellites by 2030 may fragment connectivity standards and prompt new bilateral agreements for cross-border spectrum access. Debris-mitigation mandates favor larger, longer-lived buses with autonomous propulsion.

HTS and digital payloads driving bandwidth economics

High-throughput satellites achieved 20 bits per hertz spectral efficiency in 2024, and Intelsat’s software-defined payloads delivered 40% incremental capacity through real-time beam shaping.[3]Intelsat, “Software-Defined Payload Performance,” intelsat.com SES O3b mPOWER offers terabit-scale links with sub-150 ms latency, enabling cloud backhaul for oil rigs and cruise ships. Digital payload reconfiguration cuts response time to traffic spikes from days to minutes, supporting disaster-relief connectivity. Elevated component costs limit widespread adoption; however, government contracts and premium enterprise use cases help offset the initial investment. Improved bandwidth economics narrow the gap between satellite and fiber in low-density markets, strengthening the satellite communications market.

Direct-to-device satellite 5G standards (3GPP NTN)

3GPP Release 17 enables unmodified phones to exchange text and SOS messages with satellites; Apple’s iPhone 14 service was expected to launch commercially in 2024. T-Mobile and SpaceX field-tested two-way texting using existing 1.9 GHz spectrum. Doppler shift, power control, and seamless terrestrial-space handover require extensive software upgrades, but once standardized, they unlock a multi-billion-device addressable base. Regulatory alignment across ITU regions remains incomplete, which delays the rollout of full voice and data services. Direct-to-device revenue potential boosts investor confidence throughout the satellite communications market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Orbital-debris regulations raising compliance costs | -0.80% | Global, strictest in US and Europe | Long term (≥ 4 years) |

| Spectrum-allocation bottlenecks and cross-service interference | -0.70% | Global, acute in congested orbital slots | Medium term (2-4 years) |

| Space-to-ground cybersecurity and jamming threats | -0.60% | Global, highest impact in conflict regions | Short term (≤ 2 years) |

| Price-compression from terrestrial 5G/Fiber substitutes in dense areas | -0.90% | Developed markets, urban and suburban areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Orbital-debris regulations raising compliance costs

The FCC now requires disposal within 5 years post-mission, adding USD 50,000–200,000 per satellite for propulsion systems.[4]Federal Communications Commission, “Orbital Debris Mitigation Report,” fcc.gov ESA guidelines enforce collision-avoidance maneuvers that shorten operational life by up to 12 months. ClearSpace-1’s delay and EUR 100 million (USD 108.21 million) cost overruns highlight the complexity of active debris removal. Insurers raised premiums by 15-25% in 2024, prompting operators to consider self-insurance pools. A regulatory patchwork complicates multinational fleets, increasing program management overhead across the satellite communications market.

Spectrum-allocation bottlenecks and cross-service interference

C-band clearing for US 5G costs satellite operators USD 3 billion and forces equipment retuning at 12% of earth stations.[5]CTIA, “C-Band Transition Impact Report,” ctia.org ITU’s WRC-23 failed to finalize Ka-band frameworks for LEO filings, extending coordination cycles to two years. Military-reserved bands restrict commercial capacity in conflict zones, causing congestion to spill over into civilian channels. Advanced dynamic-sharing algorithms mitigate some interference but require capital-intensive upgrades to gateways. Frequency coordination delays raise financing costs, slowing constellation rollouts in the satellite communications market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Satellite Mass: Small sats disrupt heavyweight dominance

The 10-100 kg category expanded at an 8.95% CAGR through 2031, while spacecraft above 1,000 kg retained 78.65% of the satellite communications market share in 2025. CubeSat fleets like Planet’s 200-unit constellation demonstrate resilience by sacrificing individual redundancy for swarm benefits. Modular avionics and automotive-grade electronics reduce build cycles to 18 months, enabling rapid sensor upgrades for Earth-observation and IoT use cases.

Standardized separation rings cut integration costs by 60%, and rideshare manifests on reusable rockets minimize per-satellite launch fees. However, tighter debris-mitigation rules impose disproportionate costs on sub-10 kg craft, steering commercial focus toward the 10-100 kg sweet spot. Mid-class 500-1,000 kg buses serve higher-power payloads such as next-gen HTS and optical links, bridging performance gaps while maintaining two-satellite ride options. The satellite communications market size for lightweight platforms is expected to continue expanding as national space programs seek sovereign imaging capacity without incurring billion-dollar budgets.

By Orbit Class: Hybrid architecture gains traction

LEO networks captured 52.85% of the satellite communications market share in 2025, thanks to their sub-50 ms latency, which is critical for cloud gaming and edge compute workloads. MEO solutions achieve a 9.68% CAGR, offering near-global coverage with fewer than 20 satellites and a latency of 150-300 ms, suitable for enterprise VPN and cruise Wi-Fi. GEO remains indispensable for wide-beam broadcasting and transoceanic mobility, despite its static share.

Operators integrate cross-orbit routing that shifts delay-sensitive traffic to LEO and bulk video to GEO Tbps spot beams. Electric propulsion enables mid-life altitude changes, hedging against demand uncertainty. Government bandwidth contracts increasingly mandate multi-orbit redundancy, driving capital allocation toward flexible fleets. The satellite communications market size will shift toward balanced constellations that leverage latency, capacity, and coverage advantages across various orbital regimes.

By End User: Defense spending catalyzes commercial scale

Commercial services held 83.25% of 2025 revenue, but military and government contracts grew at 10.95% CAGR as the Pentagon committed USD 13 billion to commercial capacity leasing. Direct-to-device emergency capability attracts public-safety agencies that need nationwide fallback communications. Commercial maritime and aviation customers upgrade to LEO backhaul for real-time telemetry and passenger streaming.

Dual-use satellites blur the boundaries between civilian and defense applications, allowing operators to amortize secure payloads over a broader customer base. Cyber-hardened beams command premium pricing among classified users, boosting margins. Humanitarian NGOs leverage subsidized bandwidth during natural disasters, thereby widening social-impact metrics that help firms win government tenders and expand the satellite communications market.

By Frequency Band: L and S band systems to climb up the spectrum ladder

L and S-band systems commanded a 67.55% share in 2025 due to all-weather performance and low-cost mobile terminals. Q/V and optical links expand at a 9.65% CAGR, delivering 20 Gbps per beam to maritime defense users and data center backbones. Ka-band adoption accelerates for consumer broadband as phased-array costs fall below USD 400. At the same time, Ku-band remains a viable option for broadcast and enterprise applications due to the familiarity with antennas.

C-band monetization from terrestrial 5G funds satellite gateway upgrades, but secondary sharing increases the complexity of interference management. Optical inter-satellite links bypass congested gateways, providing terabit trunks among LEO rings, yet cloud cover limits direct-to-ground optical use. Spectrum scarcity prompts operators to shift toward higher bands, despite stricter pointing requirements, thereby reinforcing product differentiation in the satellite communications market.

Geography Analysis

North America held a 51% market share in satellite communications in 2025, supported by Starlink’s prolific launch cadence and USD 13 billion in DoD service contracts. The FCC’s one-stop licensing portal slashes application turnarounds to eight months, while Telesat focuses on enterprise and government verticals. Canadian rural broadband subsidies and Mexican spectrum reforms open incremental markets.

Asia-Pacific advances at 9.45% CAGR to 2031, propelled by China’s 13,000-satellite Guowang plan and India’s private-sector liberalization. Japan emphasizes disaster resiliency and maritime autonomy through SKY Perfect JSAT, while South Korea exports smallsat buses to Southeast Asia. Australia’s vast interior drives LEO and GEO backhaul demand for remote mining and agriculture. Strong domestic manufacturing policies fuel regional supply chains, which lower capital expenditure barriers, thereby deepening the satellite communications market.

Europe pursues strategic autonomy via the EU IRIS² secure-connectivity project, prioritizing environmental sustainability and debris mitigation. Germany and France anchor manufacturing through Airbus and Thales, whereas the United Kingdom is expected to expand independent licensing post-Brexit. The Middle East and Africa rely on satellite coverage to bridge connectivity gaps, although lower purchasing power restricts the adoption of premium services. Sovereign wealth-fund-backed capacity orders in Saudi Arabia and United Arab Emirates underwrite gateway builds, accelerating connectivity along maritime trade routes.

Competitive Landscape

Industry concentration remains moderate. Intelsat US LLC, Viasat, Inc., and SpaceX hold significant GEO inventory, yet vertical integrators such as SpaceX and Amazon commoditize capacity through mass production and internal launch supply. Merger talks between Intelsat and SES aim to scale up negotiations to include payload pricing and spread R&D costs across larger fleets.

Equipment makers L3Harris and Viasat embed cybersecurity features into terminal hardware, differentiating themselves from low-cost Asian suppliers. Patent filings for phased-array antennas and optical cross-links increased by 18% in 2024, signaling a surge in efforts to secure intellectual property in software-defined networking. Niche operators target maritime, aero, and sovereign government segments, leveraging specialized gateways and 24-hour customer support. Direct-to-device alliances between mobile network operators and satellite providers reshape roaming economics, anchoring future growth in the satellite communications market.

Satellite Communications Industry Leaders

SES S.A.

Starlink (Space Exploration Technologies Corp.)

Intelsat US LLC

Hughes Network Systems, LLC

Viasat, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: The Indian Space Research Organisation (ISRO) launched the country’s heaviest communication satellite, CMS-03.

- October 2025: SpainSat NG-II, the second new-generation secure communications satellite built by Airbus for Spain, was successfully launched from the Kennedy Space Center in the United States.

- June 2025: SpaceX Launches 23 Starlink Satellites from Florida and Successfully Lands Booster at Sea.

- June 2025: Alén Space deployed its new satellite into orbit, achieving a significant milestone in its mission to advance maritime communications by validating the new VDES (VHF Data Exchange System) standard.

Global Satellite Communications Market Report Scope

This report analyzes the global satellite communication market, focusing on satellite-based voice, data, and broadband services utilized in commercial, military, and civil applications. It evaluates market dynamics, technological advancements, and key adoption factors, including the growing demand for global connectivity, low-latency communication, and robust networks for defense, emergency response, and enterprise operations.

The market is categorized by satellite mass (below 10 kg, 10–100 kg, 100–500 kg, 500–1,000 kg, above 1,000 kg), orbit class (LEO, MEO, GEO), end user (commercial, military and government, civil/emergency/NGO/academic), and frequency band (L & S, C, Ku, Ka, Q/V, and optical links). The report offers insights into market size and forecasts in USD, a competitive landscape analysis, regulatory frameworks, and technological developments driving the growth of the satellite communication industry.

| Below 10 kg |

| 10-100 kg |

| 100-500 kg |

| 500-1,000 kg |

| Above 1,000 kg |

| Low-Earth Orbit (LEO) |

| Medium-Earth Orbit (MEO) |

| Geostationary-Earth Orbit (GEO) |

| Commercial |

| Military and Government |

| Civil (Emergency/NGO/Academic) |

| L and S Band |

| C Band |

| Ku Band |

| Ka Band |

| Q/V and Optical Links |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Satellite Mass | Below 10 kg | ||

| 10-100 kg | |||

| 100-500 kg | |||

| 500-1,000 kg | |||

| Above 1,000 kg | |||

| By Orbit Class | Low-Earth Orbit (LEO) | ||

| Medium-Earth Orbit (MEO) | |||

| Geostationary-Earth Orbit (GEO) | |||

| By End User | Commercial | ||

| Military and Government | |||

| Civil (Emergency/NGO/Academic) | |||

| By Frequency Band | L and S Band | ||

| C Band | |||

| Ku Band | |||

| Ka Band | |||

| Q/V and Optical Links | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.