Europe Satellite Attitude and Orbit Control System Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

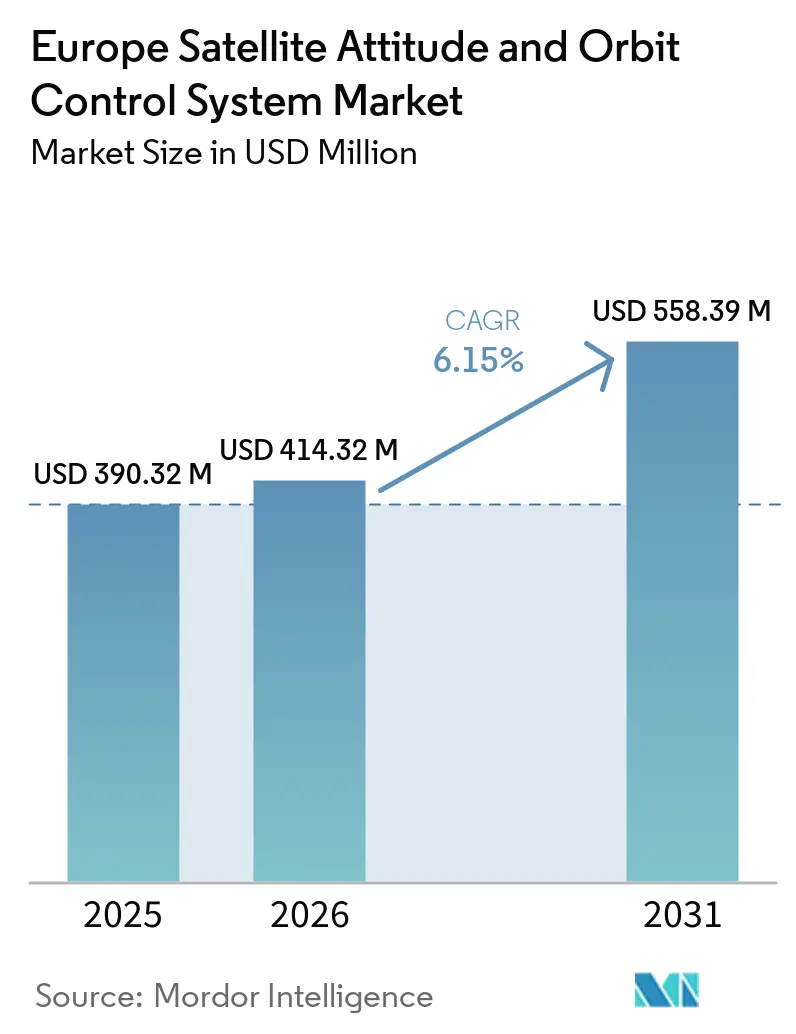

| Base Year Market Size (2025) | USD 390.32 Million |

| Market Size (2026) | USD 414.32 Million |

| Market Size (2031) | USD 558.39 Million |

| Growth Rate (2026 - 2031) | 6.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Satellite Attitude and Orbit Control System Market Analysis by Mordor Intelligence

The Europe satellite attitude and orbit control system market size is expected to grow from USD 390.32 million in 2025 to USD 414.32 million in 2026 and is forecast to reach USD 558.39 million by 2031 at a 6.15% CAGR over 2026-2031. Momentum builds around sovereign space programs, multi-orbit constellations, and precision payloads that demand higher pointing accuracy and agile maneuvering. The upgrade wave from geostationary replacements to LEO fleets is reinforcing serial production of attitude-and-orbit-control (AOCS) subsystems and software, shortening integration cycles for commercial and defense users. ESA’s 2025 ministerial decisions channel new funding into transport, Earth observation (EO), and navigation payloads that require tight control performance, increasing demand for reliable sensors, actuators, and autonomy software. Heightened space weather risk, export controls, and acute engineering talent shortages remain structural headwinds. Yet, the market continues to expand as governments prioritize dual-use connectivity, debris removal, and in-orbit servicing.

Key Report Takeaways

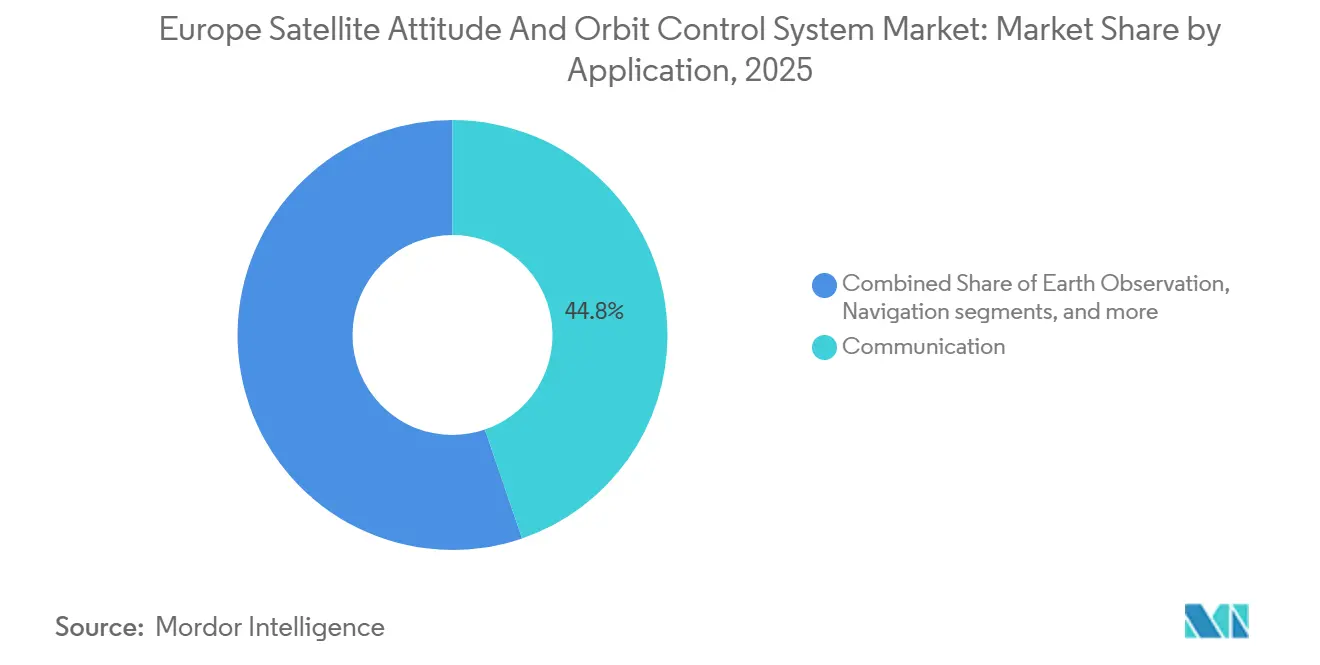

- By application, communication satellites led the Europe satellite attitude and orbit control system market with 44.75% share in 2025, while Earth observation (EO) is forecast to grow at a 7.71% CAGR through 2031.

- By mass, small satellites accounted for around 46.75% of the Europe satellite attitude and orbit control system market in 2025, while the medium satellite class is projected to grow fastest at a 7.83% CAGR.

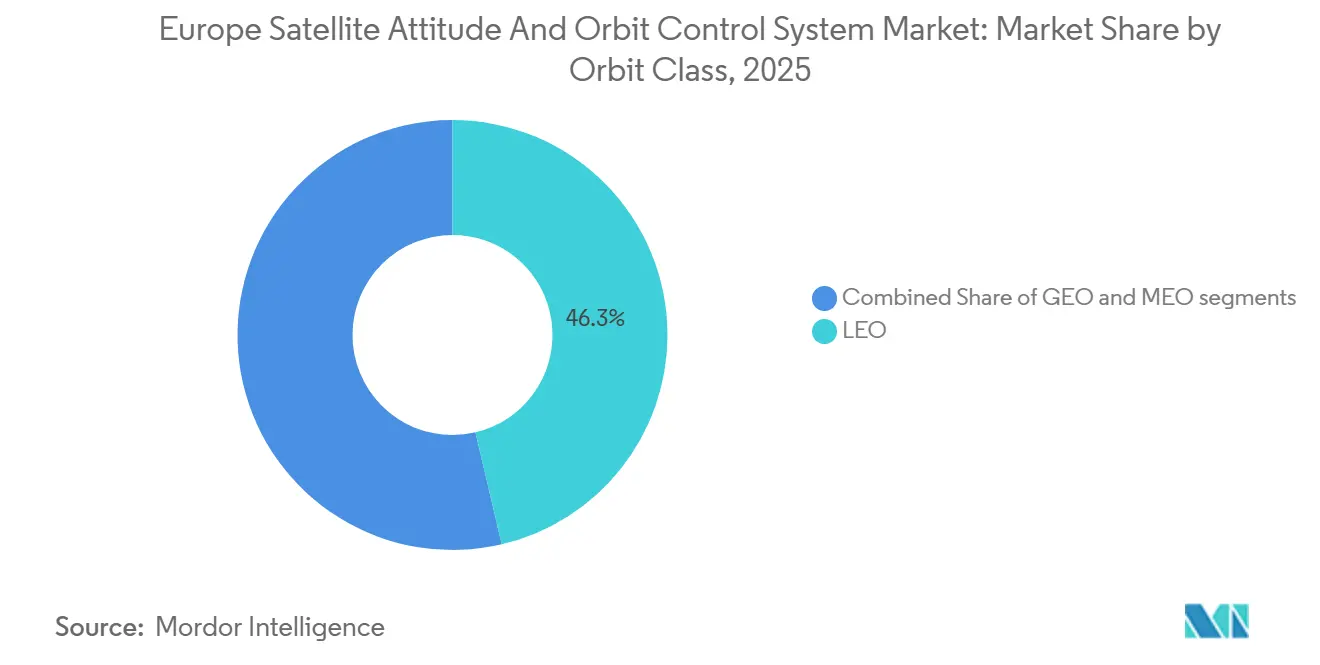

- By orbit class, LEO captured 46.32% revenue share in 2025, and MEO missions are forecast to record the strongest 7.91% CAGR to 2031.

- By end user, commercial operators accounted for 47.69% of 2025 spending, but military and government demand are forecast to grow at a 7.52% CAGR, driven by dual-use architectures and servicing contracts.

- By geography, the United Kingdom contributed 35.22% of 2025 revenue, while France is forecast to grow at an 8.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Satellite Attitude and Orbit Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in small-satellite constellations for EO and Internet of Things (IoT) | +3.2% | Europe-wide, concentrated in UK, Germany, France | Medium term (2-4 years) |

| ESA and national funding expansion | +2.8% | Europe member states, Norway, Switzerland | Long term (≥ 4 years) |

| Declining COTS component costs | +2.1% | Europe manufacturing hubs | Short term (≤ 2 years) |

| Demand for in-orbit servicing and debris mitigation | +1.9% | Europe-wide, focus on France and Germany | Long term (≥ 4 years) |

| AI-based autonomous AOCS algorithms | +1.6% | Technology hubs in UK, Germany, Netherlands | Medium term (2-4 years) |

| European microlaunchers enabling custom orbits | +1.4% | Launch sites in Germany, Spain, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Small-Satellite Constellations for EO and IoT

The EU-backed IRIS² program will place 290 satellites in orbit by 2030, compelling AOCS suppliers to deliver autonomous formation-flying and collision-avoidance capabilities that operate seamlessly across hundreds of spacecraft.[1]European Space Agency, “IRIS² Secure Connectivity Programme,” ESA.INT It is building common software frameworks that let different manufacturers plug standardized AOCS modules into multi-vendor constellations, shortening integration cycles and lowering costs.[2]European Commission, “Copernicus Programme Overview,” DEFENCE-INDUSTRY-SPACE.EC.EUROPA.EU Constellation economics demand sub-meter pointing accuracy at price points 60-80% below legacy GEO hardware, pushing European vendors to adopt modular star trackers and scalable reaction-wheel clusters. Real-time fleet management also raises the bar for onboard autonomy, since human operators cannot micromanage every satellite in flocks of more than 100 nodes. As a result, platforms that combine precision, affordability, and AI-driven self-coordination are emerging as clear winners in the European satellite attitude and orbit control system market.

ESA and National Funding Expansion

ESA’s 2024-2025 budget rose 17% to USD 8.97 billion, with new allocations for quantum sensors and AI navigation research directly supporting next-generation AOCS programs.[3]UK Space Agency, “Innovate UK Space Funding,” GOV.UK Germany’s USD 1.4 billion space plan and France’s USD 10.49 billion infrastructure push reinforce that momentum, underwriting prototype flights and component-qualification campaigns through 2030. Funding packages emphasize dual-use technology, ensuring that civil and defense satellites can share common AOCS architectures for economies of scale. Cooperative schemes like ESA’s ARTES accelerate laboratory concepts, such as neuromorphic processors, into orbit, narrowing Europe’s innovation gap with regions with narrower public budgets. For suppliers, generous grants offset high, non-recurring engineering costs, accelerating time-to-market for advanced attitude-control solutions.

Declining COTS Component Costs

Leveraging automotive and consumer-electronics lines, European manufacturers have cut the prices of star trackers and inertial measurement units by up to 50% compared with traditional space-qualified builds. Radiation tolerance is achieved through software error-correction and redundant architectures rather than costly custom chips, keeping prices low without sacrificing reliability. Falling hardware costs let CubeSat operators incorporate high-precision pointing capability once reserved for multi-ton platforms, broadening the customer base of the Europe satellite attitude and orbit control system market. Procurement priorities are shifting, too; buyers now weigh software-update cadence and cybersecurity hardening alongside mechanical pedigree, rewarding vendors that bring agile firmware practices into the space domain.

Demand for In-Orbit Servicing and Debris Mitigation

European attitude and orbit control system solutions are facing heightened performance expectations amid the rise of active debris removal and on-orbit servicing missions. These missions are pushing the requirements beyond traditional station-keeping, emphasizing the need for high-precision rendezvous and vision-based navigation capabilities. ESA’s ClearSpace-1 mission, awarded at around EUR 86 million (USD 101.54 million), marks a pivotal moment, showcasing autonomous debris-capture technologies poised to shape future commercial servicing frameworks. Concurrently, Airbus’s Bartolomeo external platform is actively validating advanced sensors and payload technologies in orbit, paving the way for their integration into future operational servicing missions. On a broader scale, insurers are increasingly prioritizing conjunction risk and spacecraft manoeuvrability, amplifying the demand for platforms with efficient electric propulsion systems. These systems are adept at performing frequent low-thrust collision avoidance manoeuvres.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Export restrictions on space-grade parts | –0.9% | UK, Germany, France | Long term (≥ 4 years) |

| High radiation-qualification costs | –0.7% | Nordic and Eastern European SMEs | Medium term (2–4 years) |

| Vulnerability to space weather | –0.5% | High-latitude operators across Europe | Short term (≤ 2 years) |

| AOCS engineering talent shortage in SMEs | –0.6% | Germany, France, UK | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Export Restrictions on Space-Grade Parts

Export control regimes, such as US ITAR requirements and Europe's dual-use framework, are imposing significant compliance burdens on satellite supply chains. These regulations often lengthen procurement timelines and complicate rapid-deployment models favored by small-satellite operators. In response, many European spacecraft manufacturers are increasingly adopting ITAR-free architectures to maintain export flexibility. Additionally, post-Brexit regulatory differences have created challenges for UK-based suppliers involved in Europe-linked programs. Some of these firms are expanding their presence in the region to ensure continued market access. At the program level, Europe's heightened focus on strategic autonomy, especially in initiatives like IRIS², underscores the push to localize critical subsystems within Europe's industrial base. Consequently, manufacturers are now prioritizing export freedom and supply-chain resilience, alongside technical performance, when choosing next-generation components.

High Radiation-Qualification Costs

In the European attitude and orbit control system supply chain, radiation assurance consistently exerts significant pressure on both costs and schedules. Testing campaigns for total ionizing dose and single-event effects can cumulatively exceed several hundred thousand euros for a specific component family. This financial hurdle poses challenges, especially for programs with smaller production scales. Securing beam time at specialized heavy-ion facilities, like CERN or prominent Helmholtz centers, further elongates qualification timelines. This is especially true for SME suppliers, who often grapple with limited scheduling flexibility. While certain NewSpace operators are venturing into more risk-tolerant deployment models, European regulators and mission owners remain steadfast. They emphasize debris mitigation and long-term reliability, upholding a conservative approach to radiation assurance mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Imaging Agility Drives Earth Observation Growth

Communication satellites accounted for 44.75% of 2025 revenue in the European satellite attitude and orbit control system market, supported by broadband rollouts and sovereign connectivity initiatives. EO platforms, however, post the fastest 2026-2031 advance at 7.71% CAGR, propelled by Copernicus expansion and climate-monitoring missions that demand tighter pointing accuracy for hyperspectral instruments.

Ongoing EO missions are pushing European AOCS performance thresholds. Next-generation Copernicus payloads demand greater pointing precision and stability. Consequently, the EO segment is poised for above-average growth in AOCS value. A consistent demand for high-accuracy reaction wheels, compact sun sensors, and rapid-response control architectures bolsters this growth. In contrast, while communications platforms still dominate AOCS spending, they are shifting towards standardised LEO bus designs. These designs prioritise cost efficiency and platform commonality, thereby reducing subsystem value intensity. Navigation programmes, on the other hand, maintain stability. The Galileo Second Generation satellites, with their focus on extended operational lifetimes, ensure steady procurement cycles. Additionally, space observation and technology demonstration missions are pioneering autonomous control capabilities that are anticipated to be integrated into larger constellation architectures in the future.

By Satellite Mass: Small Platforms Capture Innovation Investment

Small satellites accounted for 46.75% of 2025 revenue in the European satellite attitude and orbit control system market, favored for its balance of payload capacity and rideshare economics. This growth will be further propelled by the consistent reduction in component costs and an increase in the number of rideshare missions. With the development of miniaturized reaction wheels, star trackers, and control electronics, it has now become possible for spacecraft weighing less than 100kg to use highly capable three-axis stabilization systems.

Yet medium satellites are projected to capture an incremental 7.83% CAGR, reshaping supplier roadmaps toward advanced autonomy, hybrid propulsion, and low-power avionics. Small satellites are expected to be the largest in terms of revenue generation, owing to their strategic importance in EO and institutional missions; large satellites are expected to see a drop in demand. This drop in demand has not affected the intricacy of the gyros and reaction wheel assemblies in this mass range.

By Orbit Class: MEO Refresh Cycles Accelerate

LEO satellites represented 46.32% of 2025 deployments in the European satellite attitude and orbit control system market, attracting commercial data and connectivity services that benefit from low-latency links. LEO is poised to reclaim its dominance in the AOCS manufacturing and deployment sector, marking the initial surge in the transition of large broadband satellite constellations toward deployment readiness.

MEO systems, led by Galileo augmentation and regional constellations, are forecasted to expand at a 7.91% CAGR, reflecting operators' desire for fewer spacecraft while retaining near-global coverage. Medium Earth orbit missions are set to play a pivotal role in shaping the Europe satellite attitude and orbit control system landscape. This momentum is primarily driven by the ongoing refresh of the Galileo system and by growing interest in hybrid positioning concepts.

By End User: Dual-use Architectures Blur Boundaries

Commercial operators captured 47.69% of 2025 demand, reflecting Europe's thriving new-space sector and venture-capital inflows into data-as-a-service business models. While commercial operators still dominate spending, they're increasingly gravitating towards standardized LEO platforms, exerting downward pressure on hardware margins. Consequently, the focus of value capture is shifting towards software-centric capabilities, notably advanced control algorithms and in-orbit performance optimization services. Additionally, academic and technology-demonstration missions play a pivotal role in innovation, often acting as preliminary validation platforms for autonomous functions before they're integrated into commercial fleets.

However, military and government customers are driving growth with a 7.52% CAGR to 2031, fueled by strategic autonomy policies and recognition that space assets underpin defense and economic security. The European AOCS demand is set to grow steadily, outpacing the global market, driven by military and government programs. These programs are responding to heightened performance demands tied to missions like active debris removal, space situational awareness, and secure sovereign communications. Initiatives such as ESA's ClearSpace-1 are elevating standards for autonomous rendezvous and proximity operations, underscoring the demand for advanced control architectures.

Geography Analysis

The United Kingdom accounted for 35.22% of 2025 revenue, while France is projected to record the fastest growth at an 8.23% CAGR through 2031, underscoring a regional balance between mature commercial leadership and accelerating defense-led spending. The UK’s role in program management, operations, and service delivery for global LEO broadband supports a stable base for ongoing AOCS integration and fleet sustainment. A new tranche of LEO satellites awarded to European manufacturers reinforces confidence in the serial production of AOCS and learning-curve gains across partner facilities. France’s trajectory reflects a rising focus on sovereign capabilities and precision EO, including laser-linked constellations that require tight pointing and robust attitude determination. Germany’s leadership in ESA funding for 2026-2028 amplifies demand for AOCS across transport, EO, and navigation lines, anchoring multi-year work packages and de-risking subsystem roadmaps in the region.

Across Northern and Western Europe, NewSpace companies are expanding serial production and winning multi-satellite awards that favor standardized AOCS blocks. This trend supports cluster effects in avionics, software-defined subsystems, and flight software verification, where consistent interfaces and test regimes compress time-to-orbit. The Europe satellite attitude and orbit control system market is also shaped by research and science missions that set ambitious control targets, as in drag-free control for gravitational wave detection, which confirms the competence base in France, Germany, and pan-European consortia. Policy emphasis on EU program performance and funding transparency supports supplier predictability when planning investments in rad-hard computing and high-precision sensors.

Competitive Landscape

Prime contractors anchor the largest institutional and commercial programs, while specialized manufacturers scale serial production for small- and mid-size buses, together shaping a balanced competitive field in Europe. Tier-1 players convert flagship awards in broadband, EO, and science into steady AOCS demand that carries significant content value in sensors, actuation, and software. Subsystem specialists focus on reaction wheels, magnetorquers, GPS receivers, and avionics that integrate with multiple buses, which allows them to generate revenue across competitive integrators.

The Europe satellite attitude and orbit control system market also includes operator-driven manufacturing investments that add in-house integration capacity, tightening feedback loops between operations and platform engineering. Corporate combination plans among leading European primes indicate a consolidation wave that could rebalance workshare across countries and streamline supply chains for institutional missions. Strategic moves in product portfolios matter as much as contract wins. Ultra-precision programs such as drag-free flight for gravitational wave detection signal a technological edge in Europe that can cascade into commercial offerings with higher stability and robustness. Bus platforms that incorporate higher-torque actuators and optional control-moment gyroscopes improve agility for EO, disaster response, and intelligence use cases while maintaining standardized avionics to keep integration predictable. Onboard computing roadmaps are shifting toward radiation-tolerant processors with secure architectures, enabling autonomous collision avoidance, formation flight, and dynamic retargeting that reduce operational overhead for larger fleets.

The supplier base is adding throughput and deepening collaboration with ESA programs, national agencies, and commercial operators. Serial production contracts for multi-satellite batches improve learning curves and spread qualification costs across planned deliveries, while ensuring consistent test and validation regimes. Primes that coordinate multi-country footprints are prepared to meet surge demand for institutional missions, and increasingly open interface standards are lowering switching costs for components and avionics.

ESA’s performance oversight and standardized engineering practices continue to anchor quality and reliability as competitive differentiators, which sustains user trust in European AOCS solutions. In this environment, the Europe satellite attitude and orbit control system market balances innovation with heritage, which helps participants protect margins while meeting rising performance demands across orbits and missions.

Europe Satellite Attitude and Orbit Control System Industry Leaders

Airbus SE

Thales Group

AAC Clyde Space AB

OHB System AG (OHB SE)

GomSpace A/S (GomSpace Group AB)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Planet Labs Germany, a top provider of daily Earth change data and insights, inked a significant 7-figure, 2-year deal with the Greek government. This partnership aims to bolster Greece's National Satellite Space Project. The contract, facilitated by the European Space Agency (ESA), represents the interests of both the Hellenic Ministry of Digital Governance and the Hellenic Space Center. It encompasses a range of data services, including near-daily medium-resolution imagery and high-resolution tasking, all designed to support various broad-area monitoring initiatives.

- October 2025: Airbus, Thales, and Leonardo signed a framework merger to combine their satellite manufacturing operations into a new European champion to better compete in AOCS-enabled satellite constellations.

- March 2025: ESA continued development of the EUR 86 million (USD 101.63 million) ClearSpace-1 active debris removal mission, advancing autonomous rendezvous and capture technologies that will elevate precision AOCS requirements for future European spacecraft.

- December 2024: ESA awarded a EUR 290 million (USD 336.35 million) contract to the SpaceRISE consortium, led by SES, Eutelsat, and Hispasat, for IRIS²’s first 290 satellites, mandating autonomous formation-flying AOCS.

Europe Satellite Attitude and Orbit Control System Market Report Scope

This study examines every element that helps a satellite maintain its orientation and remain in the correct orbit while operating for, by, or within Europe. This report does not cover several key areas: launch-vehicle guidance, navigation, and control systems; ground-station tracking and telemetry infrastructure; satellite bus structures; and power and thermal subsystems, unless they're directly tied to AOCS. Additionally, we only touch on payload instruments if their requirements significantly affect attitude performance.

The Europe satellite attitude and orbit control system (AOCS) market is segmented by application, satellite mass, orbit class, end user, and geography. By application, the market is segmented into communication, Earth observation (EO), navigation, space observation, and others. By satellite mass, the market is segmented into small satellite, medium satellite, and large satellite. By orbit class, the market is segmented into geostationary Earth orbit (GEO), medium Earth Orbit (MEO), and low Earth orbit (LEO). By end user, the market is segmented into commercial, military and government, and others. The report also covers the market sizes and forecasts for the Europe satellite attitude and orbit control system in major countries across the region. For each segment, the market size and forecast are provided in terms of value (USD).

| Communication |

| Earth Observation (EO) |

| Navigation |

| Space Observation |

| Others |

| Small Satellite | Femtosatellite |

| Picosatellite | |

| Nanosatellite | |

| Microsatellite | |

| Minisatellite | |

| Medium Satellite | |

| Large Satellite |

| Geostationary Earth Orbit (GEO) |

| Medium Earth Orbit (MEO) |

| Low Earth Orbit (LEO) |

| Commercial |

| Military and Government |

| Others |

| United Kingdom |

| France |

| Germany |

| Russia |

| Rest of Europe |

| By Application | Communication | |

| Earth Observation (EO) | ||

| Navigation | ||

| Space Observation | ||

| Others | ||

| By Satellite Mass | Small Satellite | Femtosatellite |

| Picosatellite | ||

| Nanosatellite | ||

| Microsatellite | ||

| Minisatellite | ||

| Medium Satellite | ||

| Large Satellite | ||

| By Orbit Class | Geostationary Earth Orbit (GEO) | |

| Medium Earth Orbit (MEO) | ||

| Low Earth Orbit (LEO) | ||

| By End User | Commercial | |

| Military and Government | ||

| Others | ||

| By Geography | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.