Optical Satellite Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

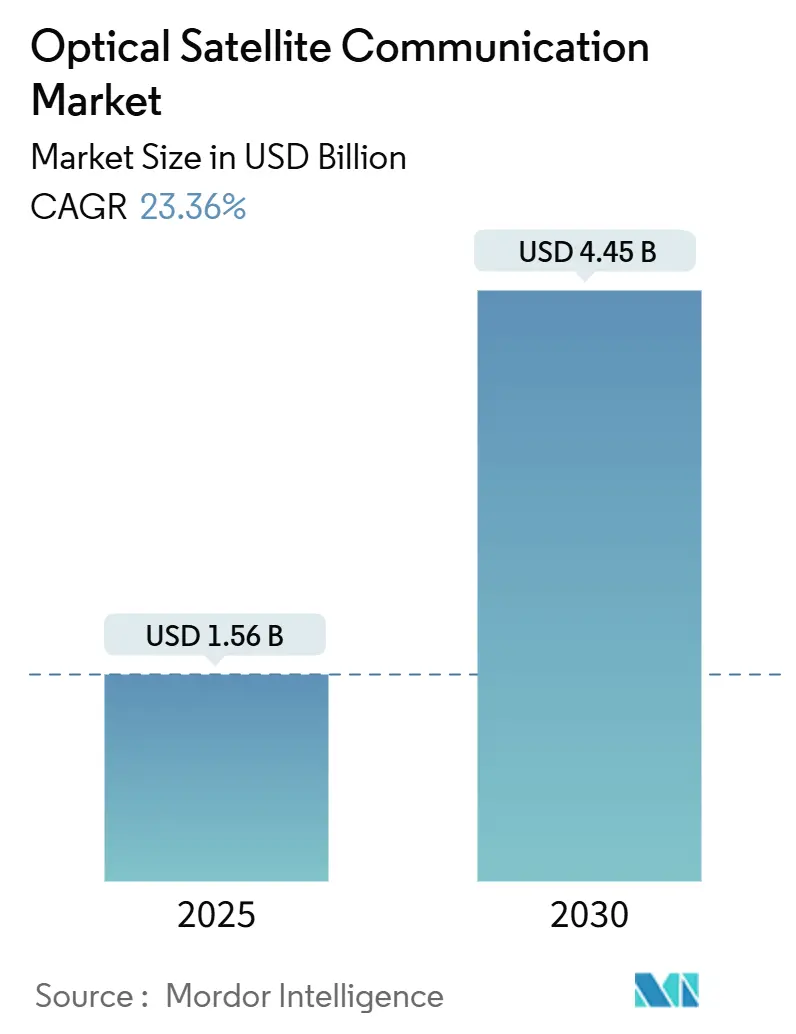

| Market Size (2025) | USD 1.56 Billion |

| Market Size (2030) | USD 4.45 Billion |

| Growth Rate (2025 - 2030) | 23.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Optical Satellite Communication Market Analysis by Mordor Intelligence

The optical satellite communication market size is USD 1.56 billion in 2025 and is projected to reach USD 4.45 billion by 2030, advancing at a 23.36% CAGR. Funding for laser-based inter-satellite links, Low-Earth-Orbit (LEO) constellations, and chronic radio-frequency spectrum congestion pushes operators toward space-qualified optical solutions. US and allied defense agencies are scaling procurements of quantum-ready laser terminals to harden networks against electronic warfare threats. China’s 100 Gbps space-to-ground demonstration showcases the competitive pace of Asian programs and underscores the technology’s throughput advantage over legacy RF links. At the same time, supply-chain strain in photonics-grade gallium and germanium is elevating component costs and motivating vertical integration among satellite prime contractors. Overall, the optical satellite communication market is crossing a threshold where performance, regulatory, and security benefits outweigh the capital premium of laser hardware.

Key Report Takeaways

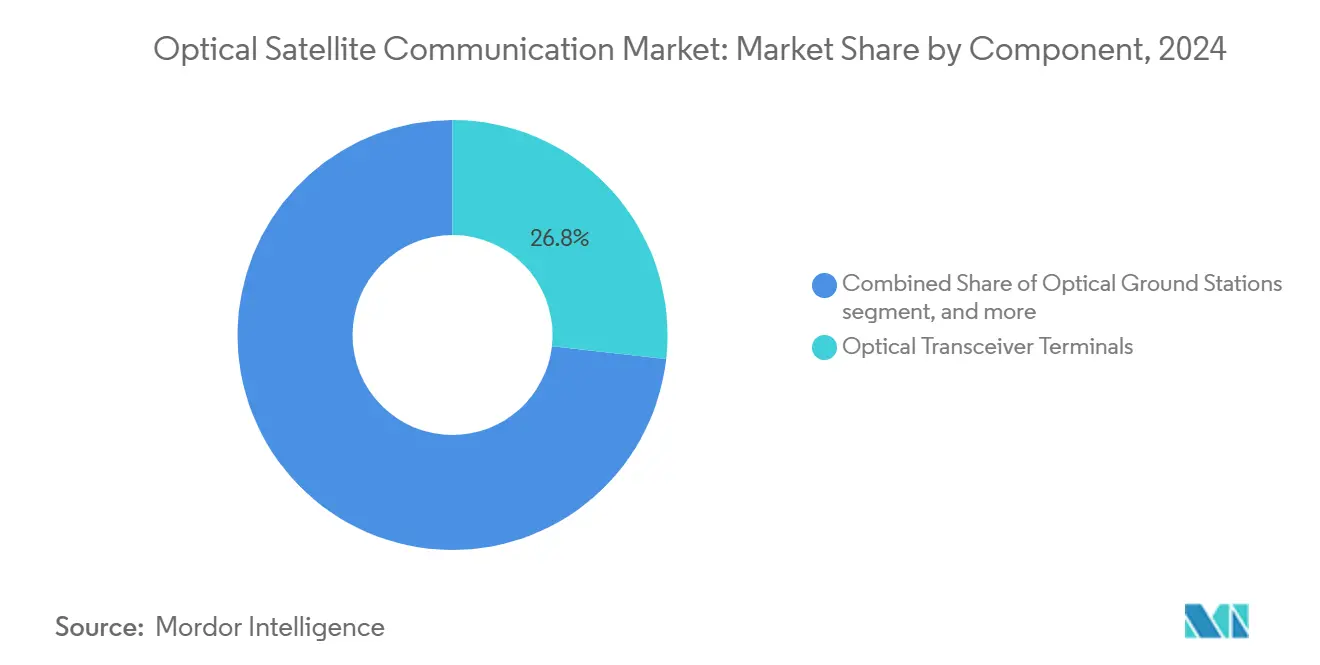

- By component, optical transceiver terminals led with 26.78% revenue share in 2024, while beam-steering assemblies are poised for a 26.76% CAGR through 2030.

- By orbit, LEO platforms held 58.84% of the optical satellite communication market share in 2024; high-elliptical and cislunar orbits are expanding at a 24.43% CAGR to 2030.

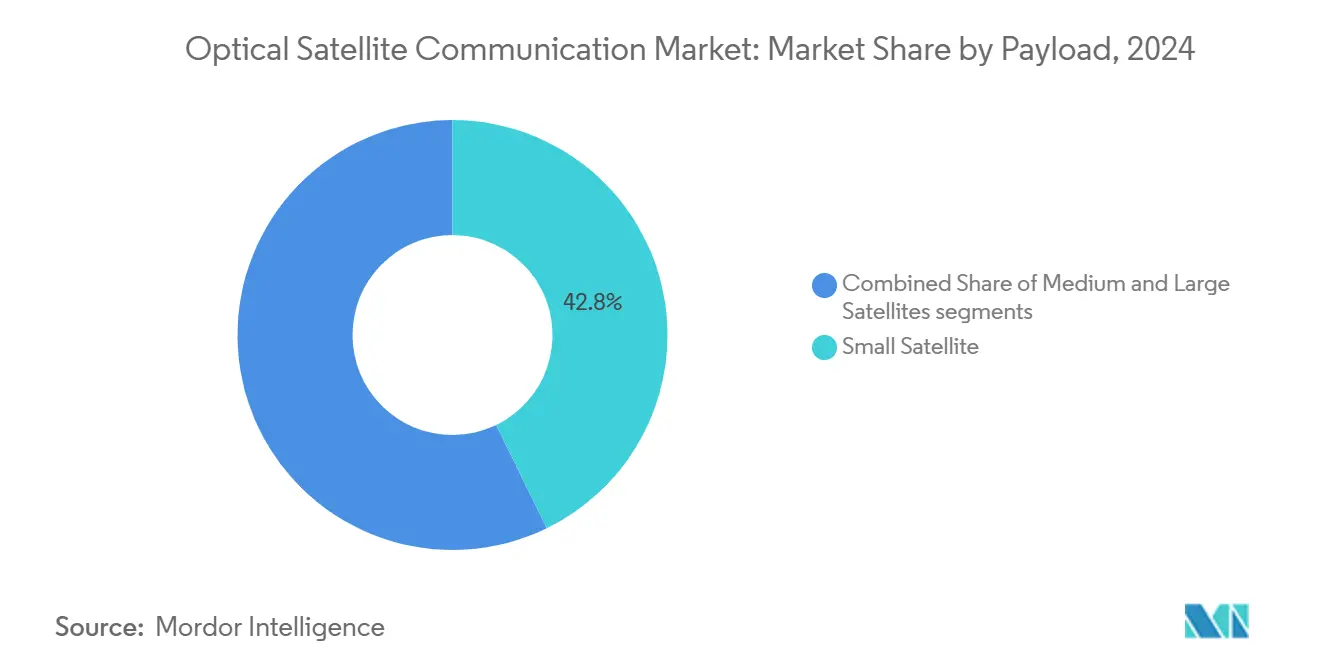

- By payload, small satellites accounted for a 42.78% share of the optical satellite communication market in 2024; medium satellites are projected to grow at a 25.78% CAGR between 2025 and 2030.

- By end-user, government and defense programs controlled a 48.81% share in 2024, whereas academic and scientific agencies represent the fastest segment at a 24.89% CAGR.

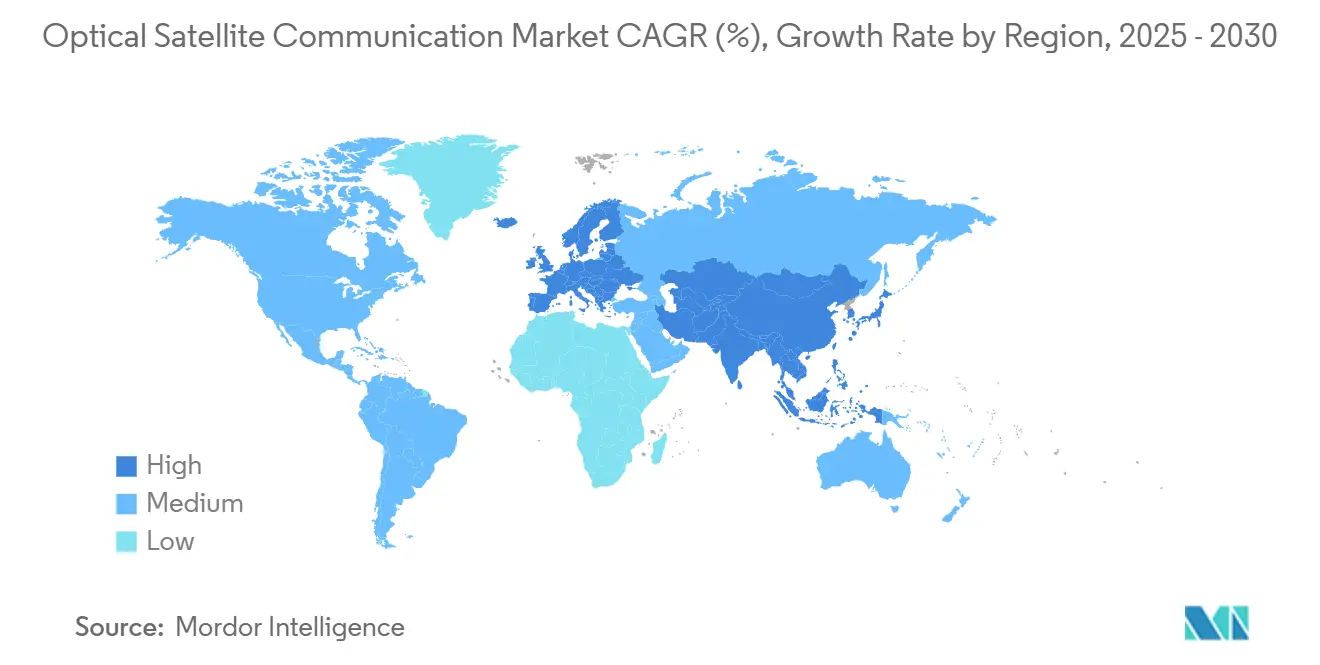

- By geography, North America captured a 26.65% share in 2024, but Asia-Pacific is forecasted to register a 25.33% CAGR to 2030.

Global Optical Satellite Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of LEO broadband constellations | +6.20% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Demand for high-throughput secure links | +4.80% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Spectrum congestion in RF bands | +3.90% | Global, particularly dense orbital regions | Long term (≥ 4 years) |

| Government space-budget acceleration | +5.10% | North America, Europe, and Asia-Pacific defense sectors | Medium term (2-4 years) |

| Standardization of optical inter-sat terminals | +2.70% | Global, with leadership from North America and Europe | Medium term (2-4 years) |

| Quantum-ready satellite links (QKD demand) | +1.80% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of LEO Broadband Constellations

Operators are embedding optical inter-satellite links as the canonical backbone of LEO networks to eliminate dependence on terrestrial relay chains. SpaceX validated cross-vendor laser interoperability by linking York Space Systems spacecraft with Starlink units under the US Space Development Agency’s Proliferated Warfighter Space Architecture program. Airbus received an extension order for 100 OneWeb satellites that will ship with baseline optical terminals, signaling that laser links have moved from experiment to requirement. MDA Space’s USD 1.3 billion EchoStar contract—a 100-plus satellite direct-to-device constellation—centers on optical links for data routing resiliency. These commitments demonstrate a clear preference for laser mesh networking to meet latency, capacity, and autonomy targets in orbit.

Demand for High-Throughput Secure Links

Military and intelligence agencies view optical technology as the most promising path toward jam-resistant, low-probability-of-intercept communications. L3Harris won USD 89.4 million under the Defense Experimentation Using Commercial Space Internet initiative to field laser-capable terminals for airborne platforms. NATO evaluation of Lithuania’s POLARIS system, coupled with Thales Alenia Space’s quantum-key distribution mission, illustrates how defense buyers are coupling high data rates with quantum-safe encryption. Narrow beamwidth, absence of RF emissions, and in-line quantum key exchange deliver a differentiated security envelope that conventional Ka-band links cannot match, making optical the architecture of record for contested theaters.

Spectrum Congestion in RF Bands

With thousands of small satellites filing for Ka- and Ku-band allocations, International Telecommunication Union coordination windows have become long and litigation-prone. The European Space Agency’s HydRON initiative proposes an all-optical relay network to bypass spectrum licensing and deliver fiber-like capacity from orbit. The Consultative Committee for Space Data Systems (CCSDS) is finalizing cross-compatible optical link layer standards that allow satellites to operate without national spectrum filings while maintaining interoperability. Such regulatory simplicity and high carrier frequency position laser communications as the pragmatic solution to escalating RF congestion.

Government Space-Budget Acceleration

Lessons from Ukraine and South China Sea contingencies have pushed defense ministries to ring-fence funding for resilient space communications. The US Space Force allocated USD 100 million in Phase 2 Enterprise Space Terminal contracts split between CACI, General Atomics, and Viasat to prototype beyond-LEO laser crosslinks.[1]U.S. Space Force, “Space Laser Communication Terminal Phase 2,” ssc.spaceforce.mil ESA’s Moonlight program is underwriting cislunar optical infrastructure for permanent lunar presence, signaling cross-agency alignment on laser adoption.[2]European Space Agency, “HydRON: Satellites using lasers,” esa.int Government solicitations increasingly stipulate optical terminals as non-negotiable, raising the baseline specifications for every spacecraft tendered after 2025.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Atmospheric attenuation and cloud cover | -2.80% | Global, with higher impact in tropical and monsoon regions | Long term (≥ 4 years) |

| High CAPEX of space-qualified laser terminals | -3.40% | Global, particularly affecting smaller operators | Medium term (2-4 years) |

| Orbital-debris line-of-sight disruption risk | -1.90% | Global, concentrated in high-traffic orbital zones | Long term (≥ 4 years) |

| Photonics-grade supply-chain bottlenecks | -2.10% | Global, with acute impact in regions dependent on Chinese materials | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Atmospheric Attenuation and Cloud Cover

Persistent cloud layers in equatorial and monsoon regions depress optical ground-station link availability below 30% on some days, compromising service level agreements. Safran’s IRIS adaptive-optics ground terminal tackles turbulence and cloud-edge diffraction, but at a premium hardware cost.[3]Safran Group, “Safran revolutionizing space communications,” safran-group.com Portable stations such as TeraNet-3 achieve rapid redeployment within 48 hours, but scaling a global weather-diverse network requires capital outlays that dwarf comparable RF gateways. Operators therefore pursue hybrid architectures: optical for backbone and RF for fallback, tempering near-term adoption rates.

High CAPEX of Space-Qualified Laser Terminals

Radiation-hardened laser diodes, precision gimbals, and redundant control electronics elevate terminal pricing beyond USD 2 million per unit, deterring resource-constrained CubeSat programs. Honeywell’s modular OISL aims to trim costs by leveraging commercial off-the-shelf photonics, yet pricing parity with Ka-band transponders remains unlikely before 2028. Component certification cycles stretch to 24 months, extending time to market. The capital burden reinforces a two-tier market: premium defense and megaconstellation buyers who can absorb costs and smaller operators who delay optical adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Transceivers Drive Current Revenue

Optical transceiver terminals held 26.78% of 2024 revenue as they combine laser sources, detectors, and control logic into ruggedized, radiation-tolerant packages. The optical satellite communication market size for transceivers is forecasted to reach USD 1.37 billion by 2030, tracking broad constellation rollouts. Momentum is shifting toward agile beam-steering assemblies, which are expected to post a 26.76% CAGR through 2030 thanks to multi-aperture arrays that can simultaneously address several links. Integrating photonic-integrated circuits cuts terminal volume by 40%, facilitating the adoption of microsats. Suppliers such as MACOM are sampling 10-50 W space-hardened optical amplifiers to support long-haul geostationary links.

Second-tier components—optical ground stations, modems, and controllers—converge into turnkey “optical teleport” offerings that package telescopes, adaptive optics, and cloud-mitigation software under service contracts. Interoperability with CCSDS blue-book waveforms allows operators to mix vendor hardware while maintaining cross-link compatibility. The component landscape will likely consolidate around vertically integrated primes that can guarantee end-to-end performance and security compliance.

By Orbit: LEO Dominance with Cislunar Growth

LEO's optical satellite communication market share stood at 58.84% in 2024, driven by the density of broadband satellites requiring tens of thousands of intra-constellation links. Shorter path losses and lower pointing requirements lower both capex and operating costs. High-elliptical, medium-Earth, and cislunar orbits represent just 8% of current deployed links but are projected to expand at 24.43% CAGR, supported by NASA's Orion O2O system and ESA's Moonlight data relays.[4]NASA, “Orion Artemis II Optical Communications System,” nasa.gov As exemplified by ESA's EDRS Global, optical interoperability between LEO and GEO relays is widening the addressable market to include deep-space scientific missions.

Use cases in Geostationary Orbit revolve around data-backhaul relays that offload imagery and IoT traffic from LEO nets. Hybrid LEO-GEO laser chains remove latency bottlenecks by avoiding terrestrial fiber back-haul and contested RF gateways, thereby addressing sovereign data-residency requirements.

By Payload: Small Satellites Lead, Medium Satellites Accelerate

CubeSats and microsats collectively commanded 42.78% of optical terminals shipped in 2024 because their low mass budgets align with compact, less than 3 kg laser packages. However, medium satellites between 250-1,000 kg are projected to experience the fastest 25.78% CAGR as operators migrate to higher-throughput buses that can mount dual-aperture optical payloads. Two-way laser communications demonstrated by Spire over 5,000 km validate optical performance on 6U platforms. Large geostationary spacecraft, while fewer in count, will continue to install kilowatt-class lasers for gateway-free video trunk links, securing a long-tail demand curve through 2030.

Standardization across payload classes through CCSDS waveforms enables heterogeneous constellations where CubeSats act as data collectors and relay through medium satellites equipped with high-gain optical amplifiers. This architecture lowers latency and minimizes dependence on dense RF ground networks.

By End-User: Defense Leads, Academia Accelerates

Defense ministries retained 48.81% spending share in 2024, locking in multi-year contracts for enterprise-grade laser terminals under tight information-assurance mandates. The optical satellite communication market size for defense applications is forecast to expand with the US Space Force's requirement for >1 Tbps resilient space backbone. Academic and scientific agencies, growing at 24.89% CAGR, leverage optical links for real-time data return on lunar regolith studies and quantum entanglement experiments. Spain's quantum-key GEO mission is emblematic of science-driven optical adoption.

Commercial broadband providers are now embedding optical mesh links to decouple coverage from terrestrial gateways, thereby accelerating time-to-revenue in underserved regions. Earth-observation firms benefit from gigabit-class downlink, enabling rapid delivery of perishable intelligence to agricultural and disaster-response users.

Geography Analysis

By Geography: North America Leads, Asia-Pacific Accelerates

North America controlled 26.65% of 2024 revenue thanks to SpaceX, Amazon’s Kuiper, and entrenched defense contractors that collectively absorb the majority of US photonics output. Federal R&D, including DARPA’s Space-BACI optical program, underwrites a domestic supply chain that is resilient to export restrictions. Asia-Pacific, however, is sprinting at a 25.33% CAGR on the back of China’s 100 Gbps transmission milestone and India’s commercialization reforms under IN-SPACe. Japan’s i-QKD constellation proposal and Australia’s push for sovereign optical gateways widen regional demand.

Europe leverages ESA programs to evolve a standards-first ecosystem, focusing on exportable terminals that comply with ITAR-free requirements. The Middle East and Africa are nascent but could leapfrog RF deployments by adopting turnkey optical teleports bundled with commercial constellation capacity. South America shows modest adoption, mainly via Earth-observation operators seeking low-latency imagery delivery for agribusiness clients.

Competitive Landscape

The market has a moderate concentration level, with the top five vendors controlling nearly 60% of revenue, leaving room for agile entrants to capture niche workloads. Tesat-Spacecom and Mynaric form the incumbent core, shipping flight-proven laser terminals to defense and commercial primes. Airbus and Thales internalize terminal production to protect program schedules and margins, while Boeing and Lockheed integrate optics across links into next-generation small-sat buses. Kepler Communications, Odysseus Space, and LinQuest are exploiting white spaces in transportable gateways and quantum-ready hardware.

Standardization under CCSDS S-band and LE crosslink blue books reduces vendor lock-in, fostering price competition. Hardware roadmaps increasingly emphasize software-defined control loops, enabling on-orbit waveform upgrades that extend spacecraft utility beyond 10 years. Supply constraints in gallium-based laser diodes are steering primes to develop domestic epitaxial foundries, potentially reshaping geographic manufacturing patterns.[5]Center for Strategic and International Studies, “Beyond Rare Earths,” csis.org

M&A watchpoints center on vertically aligned deals: photonics fabricators merging with bus integrators, and ground-segment operators acquiring terminal makers to offer turnkey “laser-as-a-service” packages. Firms that couple end-to-end integration with export-compliant supply chains stand to achieve pricing power as constellations scale from dozens to thousands of satellites.

Optical Satellite Communication Industry Leaders

Thales Group

Airbus SE

Mynaric AG

Tesat-Spacecom GmbH & Co. KG

Space Exploration Technologies Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: MDA Space secured a USD 1.3 billion EchoStar contract for 100+ Open RAN D2D satellites with optical inter-satellite links.

- May 2025: The US Space Force issued USD 100 million Enterprise Space Terminal Phase 2 awards to CACI, General Atomics, and ViaSat for standardized laser terminals.

- May 2025: General Atomics partnered with L3Harris Technologies, Inc., and Advanced Space to develop beyond-LEO optical subsystems under Phase 2 Enterprise Space Terminal.

- March 2025: MACOM released Opto-Amp 10-50 W radiation-tolerant optical amplifiers tailored for LEO-to-GEO networks.

- February 2025: Airbus SE won the UK Ministry of Defense (MOD) contract for Oberon SAR satellites with integrated optical downlinks, which will boost sovereign ISR capacity.

Global Optical Satellite Communication Market Report Scope

| Optical Transceiver Terminals |

| Optical Ground Stations |

| Modems and Controllers |

| Beam Steering and Pointing Assemblies |

| Others |

| Low-Earth Orbit (LEO) |

| Medium-Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

| Others (HEO and Cislunar Orbits) |

| Small Satellites |

| Medium Satellites |

| Large Satellites |

| Government and Defense |

| Commercial Broadband Operators |

| Earth-Observation Service Providers |

| Academic and Scientific Agencies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Optical Transceiver Terminals | ||

| Optical Ground Stations | |||

| Modems and Controllers | |||

| Beam Steering and Pointing Assemblies | |||

| Others | |||

| By Orbit | Low-Earth Orbit (LEO) | ||

| Medium-Earth Orbit (MEO) | |||

| Geostationary Orbit (GEO) | |||

| Others (HEO and Cislunar Orbits) | |||

| By Payload | Small Satellites | ||

| Medium Satellites | |||

| Large Satellites | |||

| By End-User | Government and Defense | ||

| Commercial Broadband Operators | |||

| Earth-Observation Service Providers | |||

| Academic and Scientific Agencies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the optical satellite communication market?

The market is valued at USD 1.56 billion in 2025 and is forecasted to hit USD 4.45 billion by 2030, advancing at a 23.36% CAGR.

Which orbit segment leads in revenue?

LEO systems account for 58.84% of 2024 revenue due to broadband constellation deployments.

Why are defense agencies prioritizing laser links?

Narrow beams, high data rates, and quantum-ready encryption make optical links resilient against jamming and interception.

What limits widespread optical ground-station rollout?

Persistent cloud cover and high capex for adaptive-optics telescopes restrict viable sites, especially in tropical regions.

Which region is growing fastest?

Asia-Pacific is projected to expand at a 25.33% CAGR, propelled by Chinese and Indian satellite programs.

How consolidated is the vendor landscape?

The top five suppliers hold about 60% of revenue, reflecting moderate concentration with space for new entrants.

Page last updated on: