Satellite Attitude And Orbit Control System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 4.69 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Attitude And Orbit Control System Market Analysis by Mordor Intelligence

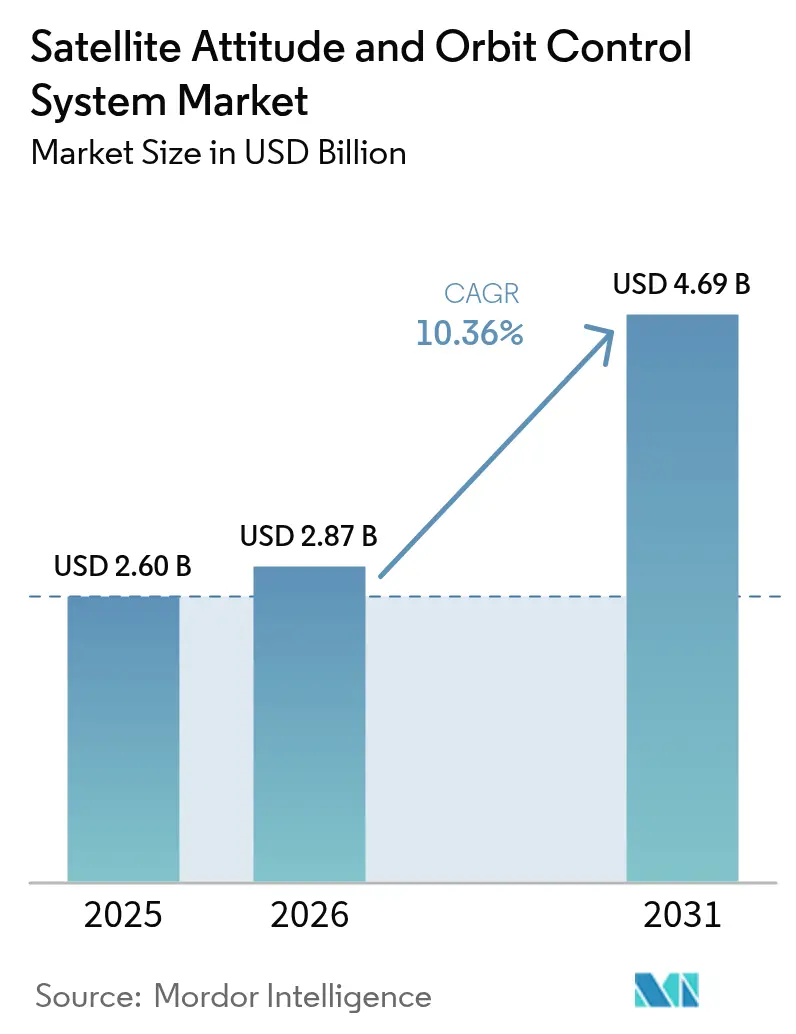

The satellite attitude and orbit control system (AOCS) market size was valued at USD 2.60 billion in 2025 and estimated to grow from USD 2.87 billion in 2026 to reach USD 4.69 billion by 2031, at a CAGR of 10.36% during the forecast period (2026-2031). Extensive deployment of small-sat constellations, rapid progress in artificial-intelligence (AI) based attitude algorithms, and the shift toward autonomous spacecraft operations underpin much of the present momentum in the satellite AOCS market. Suppliers are scaling production through standardized, software-defined architectures that trim cost without eroding pointing performance. Demand is reinforced by defense programs seeking resilient on-orbit assets that can maneuver and re-task without ground support. At the same time, emerging interface standards and miniaturized sensors lower barriers for new entrants, broadening the competitive field in the satellite AOCS market.

Key Report Takeaways

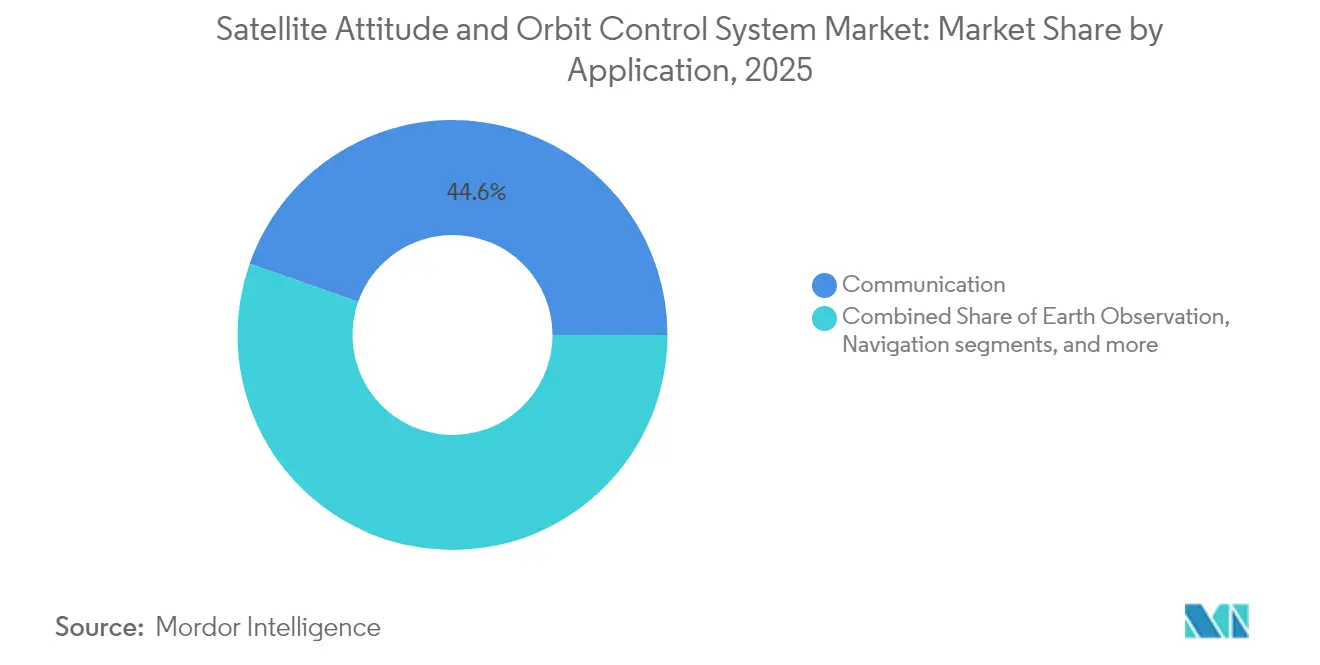

- By application, communication satellites led with 44.62% revenue share in 2025, while Earth observation is projected to advance at a 12.22% CAGR through 2031.

- By satellite mass, the 100 to 500 kg category held 42.11% of the satellite AOCS market share in 2025, whereas the 10 to 100 kg segment is forecasted to expand at an 11.35% CAGR to 2031.

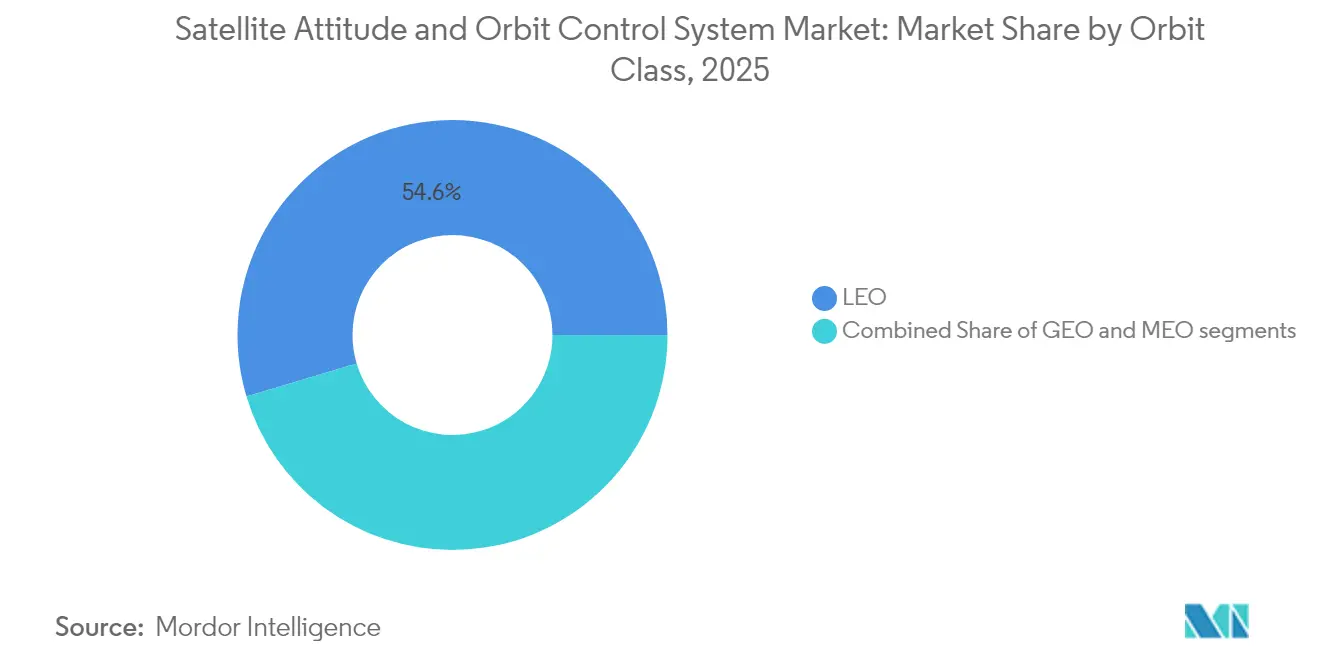

- By orbit class, low Earth orbit (LEO) captured 54.61% share in 2025; medium Earth orbit (MEO) records the fastest projected CAGR at 10.74% through 2031.

- By end user, commercial operators accounted for a 45.02% share in 2025, while military and government demand is increasing at an 11.08% CAGR toward 2031.

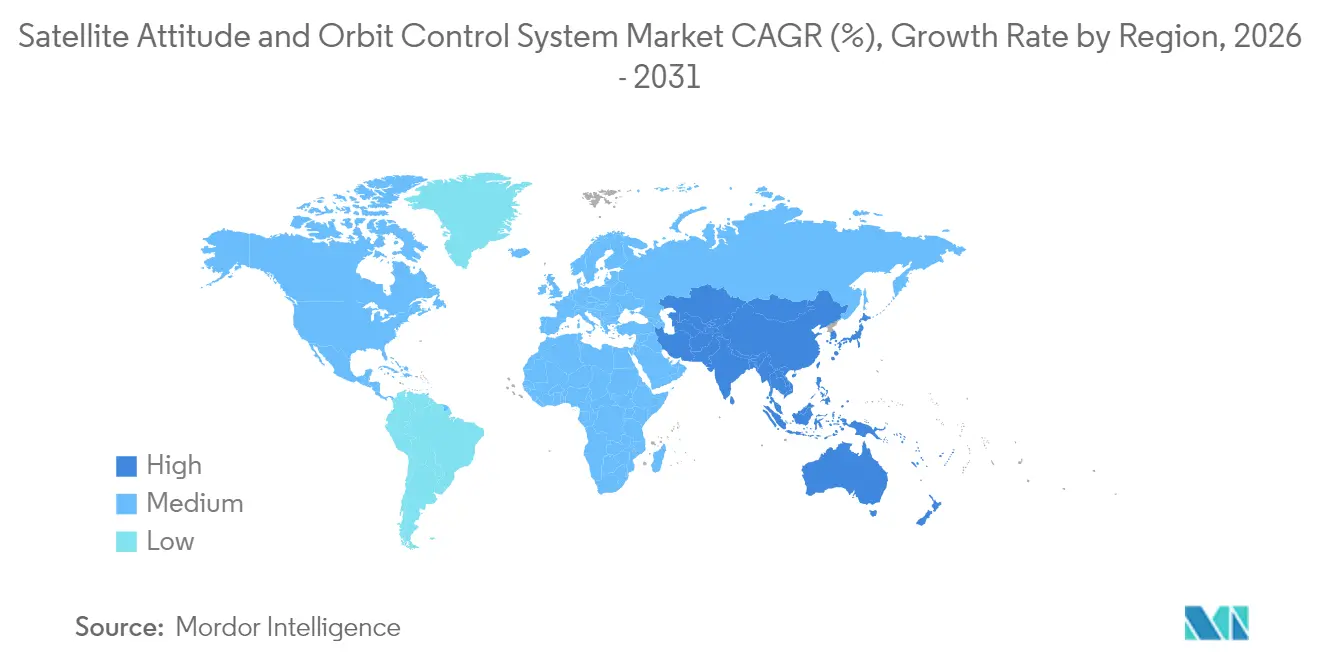

- By geography, North America dominated with a 57.63% share in 2025, whereas Asia-Pacific is set to grow at a 11.86% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Satellite Attitude And Orbit Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of small-sat constellations | +2.8% | Global; concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Advances in MEMS sensors and star-trackers | +1.9% | Global; led by North America and Europe | Short term (≤ 2 years) |

| Rising defense budgets for resilient satellites | +2.1% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-powered autonomous attitude control | +1.7% | North America, Europe; emerging in Asia-Pacific | Medium term (2-4 years) |

| Plug-and-play AOCS interface standards | +1.2% | Global | Short term (≤ 2 years) |

| Integration of micro-ion electric propulsion | +0.9% | Global; focused in advanced space programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Small-Sat Constellations

Constellation operators such as Starlink and Project Kuiper require attitude-control packages that can be manufactured in triple-digit volumes while sustaining sub-arcsecond pointing accuracy.[1]Federal Communications Commission, “Satellite Licensing and Coordination Requirements,” fcc.gov Suppliers respond with modular hardware and software-defined control loops that shorten integration cycles and enable month-level delivery schedules. Volume demand continually drives down unit pricing, boosting accessibility for newer satellite AOCS market players. Standardization further accelerates satellite production, with several integrators now completing more than 100 units per month, and pushes the adoption of robust on-orbit collision-avoidance routines. The collective effect widens the installed base of next-generation platforms, deepening the addressable satellite AOCS market across telecom, Earth-observation, and IoT missions.

Advances in MEMS Sensors and Star-Trackers

MEMS gyroscopes with noise densities below 0.1°/hr/√Hz have moved precision attitude determination from large satellites into 3U-class CubeSats.[2]Nature Electronics, “MEMS Technology Advances in Space Applications,” nature.com Hybrid packages combining MEMS inertial sensors and miniaturized star-tracker optics provide dual-mode redundancy without mass penalties. Drawing less than 100 mW, these compact devices extend mission lifetimes for battery-powered spacecraft and elevate pointing reliability to levels once reserved for multiton observatories. Their adoption raises performance expectations throughout the satellite AOCS market and compresses time-to-orbit for new commercial entrants.

Rising Defense Budgets for Resilient Satellites

The US Space Force allocates USD 29.4 billion in 2025 to build survivable constellations, explicitly funding hardened AOCS that tolerate radiation doses greater than 100 krad and resist electronic warfare. European governments add USD 13.39 billion toward sovereign space-security programs, reinforcing similar capabilities. These investments stimulate demand for secure command links, anti-jamming algorithms, and coordinated formation-flying software. Defense priorities expand the satellite AOCS market into niche domains such as fractionated architectures and autonomous threat response, prompting collaboration between traditional primes and specialized small-sat suppliers.

AI-Powered Autonomous Attitude Control

Machine-learning models now predict perturbations and adjust control laws ahead of disturbances, trimming fuel use up to 15% versus PID-only loops validated prolonged Deep-Space Network-independent navigation, proving AI can close the loop without ground oversight. Real-time fault-detection neural nets reconfigure around actuator failures, elevating reliability and lowering insurance costs. Wider adoption of AI positions the satellite AOCS market to transition from reactive stabilization toward predictive autonomy over the coming decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Space-debris-driven design complexity | −1.4% | Global; notably LEO regions | Medium term (2-4 years) |

| Radiation-hardening cost premium | −0.9% | Global; all orbital regimes | Short term (≤ 2 years) |

| Reaction-wheel rare-earth shortages | −0.7% | Global supply chains | Long term (≥ 4 years) |

| ITAR/export-control supply barriers | −0.8% | International markets outside domestic US | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Space-Debris-Driven Design Complexity

More than 34,000 tracked objects exceed 10 cm, forcing AOCS packages to embed autonomous collision-avoidance logic, add propellant margins, and continuous ephemeris uplink capabilities.[3]European Space Agency, “Space Debris and Mitigation Guidelines,” esa.intThese features raise mass, power, and software-verification workloads, pressing smaller operators who lack global monitoring infrastructure. Compliance with the 25-year deorbit rule further compels the inclusion of drag-enhancement devices or propulsion reserves, elevating costs and eroding the available mass for primary payloads in the satellite AOCS market.

Radiation-Hardening Cost Premium

Geostationary exposure can accumulate beyond 100 krad over 15 years, driving reliance on processors priced 5-10 times higher than COTS parts.[4]IEEE Transactions on Nuclear Science, “Radiation Effects in Space Electronics,” ieeexplore.ieee.org Single-event upsets mandate triple-modular redundancy and error-correction coding, compounding board complexity. Satellites operate in harsh space environments where exposure to intense radiation can damage sensors, microprocessors, and control electronics. The radiation-hardening processes required for AOCS components to ensure reliability and mission longevity increase design complexity, testing requirements, and production costs. Semiconductor shortages lengthen lead times to 18 months for hardened microcontrollers, prompting schedule risks that temper momentum in the satellite AOCS market. These higher costs limit adoption among small satellite manufacturers and emerging space companies with restricted budgets, constraining market growth in the smallsat and LEO constellation segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Communication Satellites Drive Market Leadership

Communication satellites contributed 44.62% of 2025 revenue within the satellite AOCS market. High-throughput geostationary platforms demand sub-0.1° pointing, compelling suppliers to deliver precise, thermally stable sensors and high-torque reaction wheels. Earth observation presents the swiftest climb at a 12.22% CAGR. Climate analytics, agriculture, and disaster-response services hinge on crisp revisit rates and table-top optics that demand robust jitter suppression. Upcoming multi-sensor payloads integrate IMUs directly into payload control loops, tightening performance ties between bus and instrument. As these missions multiply, they magnify the opportunity for agile vendors inside the satellite AOCS market.

By Satellite Mass: Mid-Range Platforms Dominate Deployment

The 100 to 500 kg class accounts for a 42.11% share due to an optimal balance between payload capacity and dedicated-launch affordability. Within this bracket, typical satellites carry four-wheel pyramids offering ≥50 Nms storage and dual-sensor star-tracker suites. In contrast, the 10 to 100 kg category accelerates at 11.35% CAGR, benefiting from standardized deployers and innovation in MEMS sensors. Miniaturized reaction wheels in the 0.5 Nms range make three-axis control feasible within 3U-6U frames. The cost-to-orbit advantage strengthens small-sat adoption, expanding the total addressable satellite AOCS market size for mini-class suppliers.

By Orbit Class: LEO Dominance Reflects Constellation Economics

LEO craft captures 54.61% revenue owing to low-latency communication needs and lower radiation dosage. High magnetic-field intensity allows simple torque-rod desaturation, cutting subsystem mass by up to 15%. MEO platforms, essentially navigation satellites, grow at a 10.74% CAGR. They require stable, long-life wheels and radiation-tolerant electronics. GEO systems prioritize fuel-efficient station-keeping and components that survive protracted exposure, driving premium pricing but smaller volumes. Each regime imposes distinct design rules, prompting tiered product lines across the satellite AOCS market.

By End User: Commercial Growth Outpaces Government Expansion

Commercial operators secured a 45.02% share in 2025 by emphasizing cost-optimized, quick-turn spacecraft. Subscription-based constellations prize high duty cycles and minimal ground-station interaction, steering development of highly reliable, self-calibrating AOCS packages. Military and government users advanced at an 11.08% CAGR. Their missions value encryption, radiation resilience, and threat-adaptive control logic. These requirements raise unit spend and nurture collaborative programs that spill enhancements into commercial variants, enriching the satellite AOCS industry’s technology base.

Geography Analysis

North America generated 57.63% of 2025 revenue, propelled by SpaceX’s mass-production lines, US Space Force procurement, and Canada’s sensor-development pedigree. Robust venture capital ecosystems in California and Colorado nurture start-ups that target bespoke gaps within the satellite AOCS market.

Asia-Pacific leads growth at 11.86% CAGR as China finalizes BeiDou deployments and commences internet mega-constellations. India’s PSLV launch cadence and Japan’s focus on debris-removal missions spur local supply chains, signaling sustained demand for precision attitude modules. Australia and South Korea add momentum through fresh defense allocations targeting sovereign situational awareness.

Europe maintains a strong technical base anchored by ESA programs and national primes in France and Germany, yet grapples with export-control hurdles that can lengthen cross-border integration. ESA’s Clean Space initiative propels innovation in autonomous deorbiting routines, influencing subsystem specs worldwide. South America, the Middle East, and Africa presently contribute limited revenue. However, Brazil and the UAE showcase ambition via indigenous satellite platforms, which are forecasted to tap the satellite AOCS market over the next decade.

Competitive Landscape

The landscape remains moderately fragmented, with heritage primes such as Honeywell International Inc. and Northrop Grumman Corporation defending incumbency through comprehensive catalogs and global support networks. Their multi-orbit flight heritage offers confidence to risk-averse buyers, yet price pressure from constellation operators shifts volume toward nimble specialists. Strategic partnerships rise as primes acquire niche innovators, exemplified by Honeywell’s purchase of Jena-Optronik to capture breakthrough star-tracker designs ahead of rivals. The resulting ecosystem blends legacy quality-assurance processes with start-up agility, accelerating product refresh cycles and expanding service portfolios.

Blue Canyon Technologies LLC (RTX Corporation) and AAC Clyde Space AB seize shares by offering pre-qualified, stackable control units that ship in under six months. Scale-up investments, including AAC’s new 500-unit factory, evidence confidence in expanding addressable volume. Intellectual-property filings cluster around AI fault management, MEMS-optical sensor fusion, and low-power reaction-wheel electronics, highlighting evolving satellite AOCS market battlegrounds. Singapore Technologies Engineering Ltd, a Singapore-based aerospace firm with proven small-satellite and AOCS integration expertise from TeLEOS missions. Strong in system integration and regional manufacturing, though less focused on standalone AOCS components.

Satellite Attitude And Orbit Control System Industry Leaders

Honeywell International Inc.

Northrop Grumman Corporation

Singapore Technologies Engineering Ltd.

Blue Canyon Technologies LLC (RTX Corporation)

AAC Clyde Space AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Blue Canyon Technologies LLC (part of RTX Corporation) announced the launch of its new “Saturn-400” small-sat bus design, which features multiple reaction wheel options (RW4, RW8, RW16) for enhanced attitude control and precision pointing.

- July 2025: Honeywell International Inc. was selected by the US Department of Defense's (DoD's) Innovation Unit under the TQS program to develop quantum-sensing inertial units (CRUISE and QUEST) for navigation and inertial sensing, a capability with relevance to attitude/orbit control subsystems.

- July 2025: AAC Clyde Space invested USD 25 million in a Swedish plant capable of 500 AOCS units annually by 2027.

- February 2025: Moog Inc. announced its participation in the SATELLITE 2025 conference, where it presented new radiation-tolerant high-performance space computing (HPSC) and avionics technologies, relevant as attitude/orbit control increasingly incorporates embedded computing.

Global Satellite Attitude And Orbit Control System Market Report Scope

| Communication |

| Earth Observation |

| Navigation |

| Space Observation |

| Others |

| Below 10 kg |

| 10 to 100 kg |

| 100 to 500 kg |

| 500 to 1000 kg |

| Above 1000 kg |

| Geostationary Earth Orbit (GEO) |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Commercial |

| Military and Government |

| Other |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Application | Communication | ||

| Earth Observation | |||

| Navigation | |||

| Space Observation | |||

| Others | |||

| By Satellite Mass | Below 10 kg | ||

| 10 to 100 kg | |||

| 100 to 500 kg | |||

| 500 to 1000 kg | |||

| Above 1000 kg | |||

| By Orbit Class | Geostationary Earth Orbit (GEO) | ||

| Low Earth Orbit (LEO) | |||

| Medium Earth Orbit (MEO) | |||

| By End User | Commercial | ||

| Military and Government | |||

| Other | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.