Satellite Onboard Computing System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

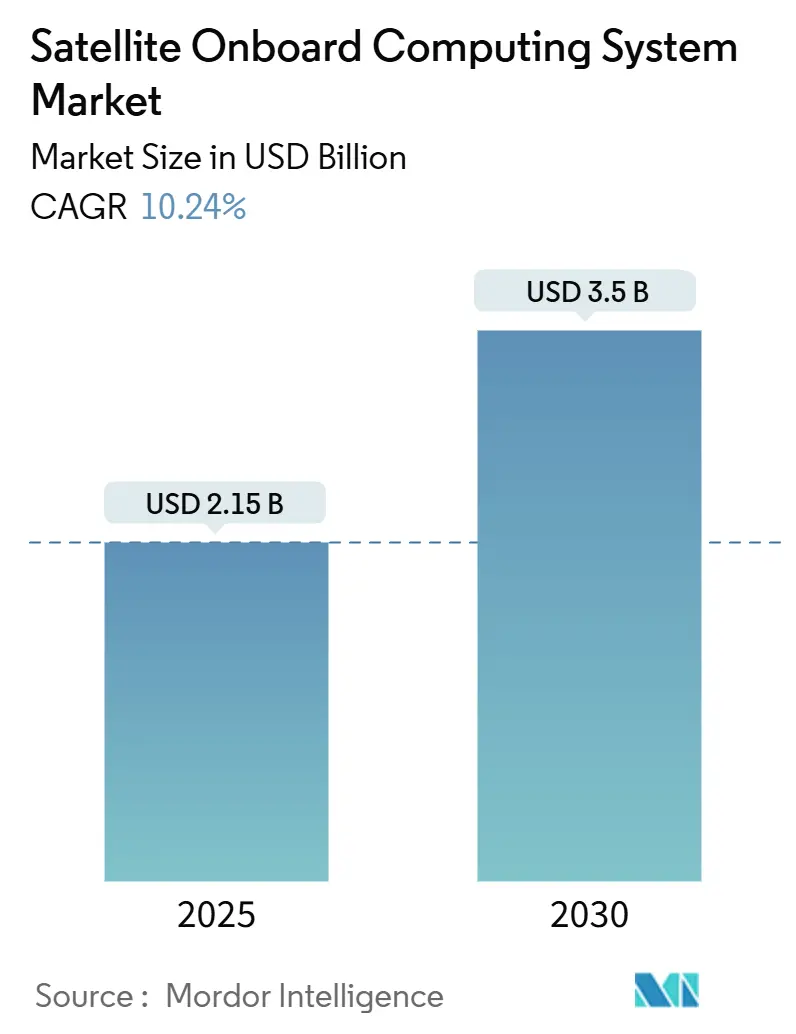

| Market Size (2025) | USD 2.15 Billion |

| Market Size (2030) | USD 3.5 Billion |

| Growth Rate (2025 - 2030) | 10.24% CAGR |

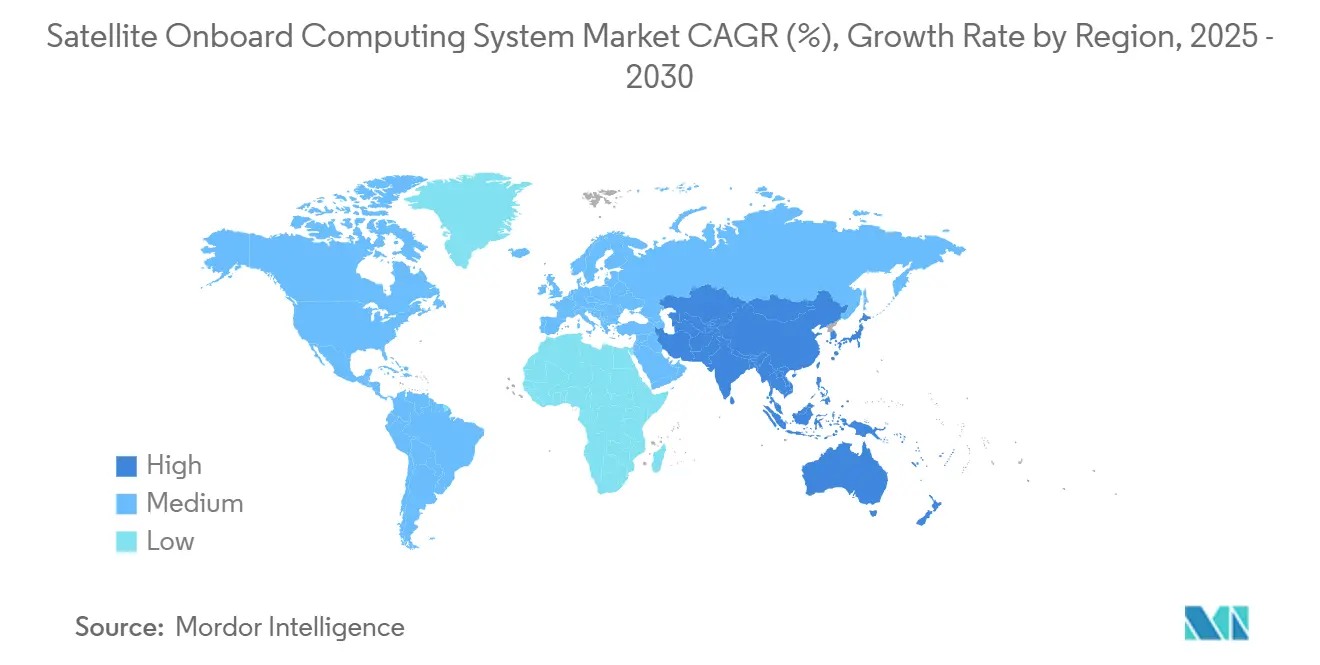

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Satellite Onboard Computing System Market Analysis by Mordor Intelligence

The satellite onboard computing system market size stands at USD 2.15 billion in 2025 and is projected to reach USD 3.50 billion by 2030, advancing at a 10.24% CAGR. The satellite onboard computing system market is moving from rigid hardware to software-defined, edge-AI architectures that demand higher processing density while maintaining radiation tolerance. Lower launch costs, the rise of mega-constellations, and the need for secure, autonomous operations foster strong procurement momentum among commercial operators and defense agencies. Suppliers that combine radiation-hardened processors with modular software stacks are best placed to capture design wins as constellation programs scale. Expanding domestic semiconductor initiatives in North America, Europe, and Asia-Pacific aim to mitigate supply bottlenecks and anchor future growth.

Key Report Takeaways

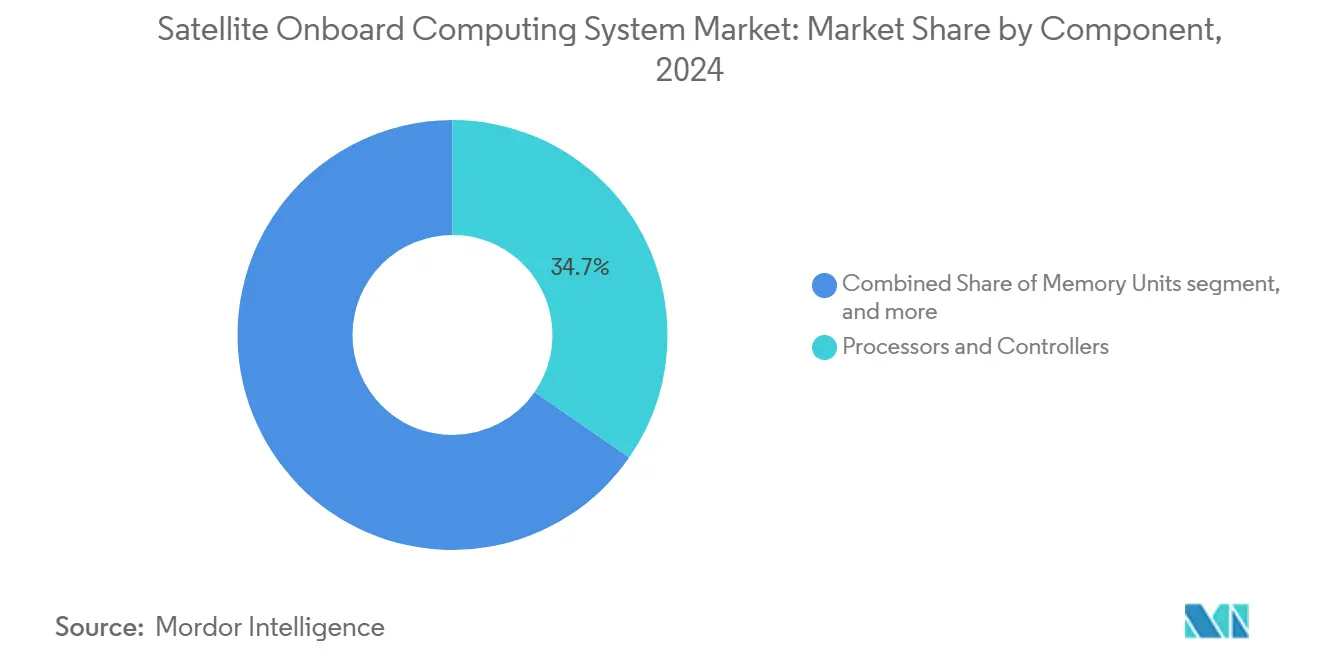

- By component, processors and controllers led 34.65% of the satellite onboard computing system market share in 2024; software and operating systems are forecasted to expand at a 14.60% CAGR through 2030.

- By satellite platform size, small satellites held 41.50% of the satellite onboard computing system market size in 2024, while pico/nano satellites are projected to grow at a 16.70% CAGR to 2030.

- By orbit, LEO captured 67.80% revenue in 2024; HEO missions are set to advance at a 14.42% CAGR through 2030.

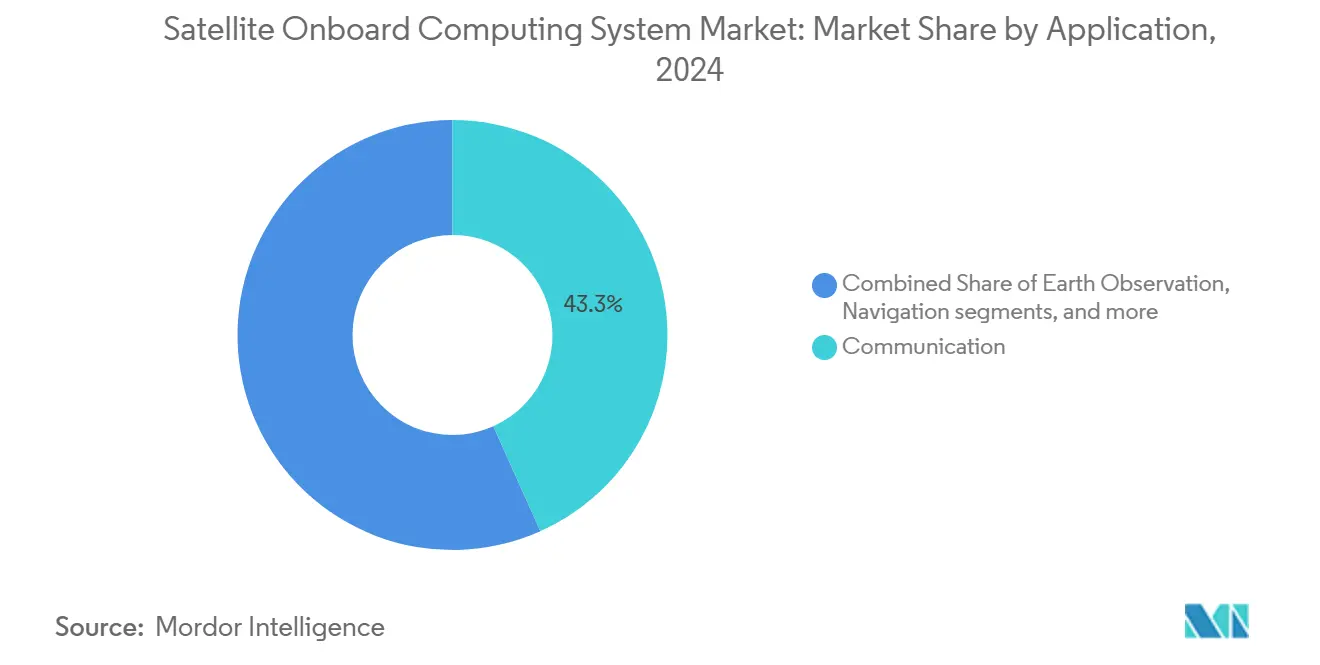

- By application, communication accounted for 43.30% of the revenue share in 2024, whereas earth observation is growing at a 13.65% CAGR.

- By end-user, commercial and civil programs held a 57.10% share in 2024, while defense and government demand expanded at a 12.70% CAGR.

- By geography, North America retained a 37.90% share in 2024, but Asia-Pacific is the fastest-growing geography, with a 13.50% CAGR.

Global Satellite Onboard Computing System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in small-satellite and constellation launches | 2.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Advances in radiation-hardened processors | 2.1% | North America and EU core, spill-over to APAC | Long term (≥ 4 years) |

| Rising defense demand for secure ISR satellites | 1.9% | Global, concentrated in NATO and allied nations | Short term (≤ 2 years) |

| Lower launch costs expanding mission count | 1.7% | Global, with commercial operators leading adoption | Medium term (2-4 years) |

| Onboard edge-AI for real-time analytics | 1.4% | North America, EU, and advanced APAC markets | Long term (≥ 4 years) |

| Software-defined modular satellite designs | 1.2% | Global, with early adoption in commercial sector | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Small-Satellite and Constellation Launches

Mega-constellation economics reshape computing payload requirements by favoring standardized, modular boards that can be produced in high volumes and integrated quickly. Operators like SpaceX already manage thousands of LEO spacecraft that carry onboard computers and are responsible for autonomous collision avoidance, dynamic beam steering, and network optimization without waiting for ground control signals. The processing load rises further once satellites run edge AI models for traffic routing and capacity prediction. Thermal dissipation becomes a design bottleneck because densely packaged electronics must shed heat in a vacuum where conduction and convection are absent, compelling wider use of heat pipes, loop heat pipes, and phase-change materials certified for spaceflight.[1]Source: IEEE, “Thermal Management Technologies for Embedded Cooling Applications,” ieeexplore.ieee.org Compliance with ECSS electromagnetic-compatibility standards underpins market entry for European missions, pushing vendors to document subsystem shielding and grounding architectures from the outset.[2]Source: European Cooperation for Space Standardization, “ECSS Standards,” ecss.nl Together, these forces enlarge demand for high-performance, radiation-tolerant processors and flexible software stacks that can keep pace with constellation-scale update cycles while fitting within constrained power and mass envelopes.

Advances in Radiation-Hardened Processors

Open-source RISC-V instruction sets allow satellite integrators to add custom acceleration for encryption, signal processing, or machine-learning inference without being locked to proprietary roadmaps. Europe’s Frontgrade Gaisler LEON cores underscore regional ambitions for processor sovereignty, supporting fault-tolerant pipelines, triple-modular redundancy, and memory-scrubbing logic that mitigates single-event upsets. Moving below the 28 nm node raises transistor density and clock speed yet introduces new radiation vulnerabilities, so designers embed layered error-correction schemes at cache, interconnect, and system-controller levels. ISO 21980 harmonizes qualification tests for commercial off-the-shelf parts in LEO, shortening component vetting and lowering cost barriers for emerging suppliers.[3]Source: International Organization for Standardization, “ISO 21980:2020,” iso.org The intersection of smaller geometries, flexible intellectual-property cores, and standardized test protocols delivers higher MIPS-per-watt while preserving mission reliability, propelling the satellite onboard computing system market into a performance class previously reserved for terrestrial servers.

Rising Defense Demand for Secure ISR Satellites

Geopolitical flashpoints have intensified investment in satellites that can process classified imagery and signals intelligence onboard, remain resilient to jamming, and continue operating if command links are contested. Programs such as the UK’s TYCHE concept illustrate how militaries are shifting toward fully autonomous spacecraft capable of real-time target recognition and threat assessment. Lockheed Martin’s acquisition of Terran Orbital strengthens vertical control over hardened computing stacks by marrying high-throughput small-sat manufacturing with proprietary encryption, anti-tamper hardware, and radiation shielding techniques. Defense agencies often invoke ECSS-E-ST-80C security requirements, mandating secure-boot chains, physical intrusion detection, and lifecycle cyber-hardening from component sourcing through in-orbit operations. Meeting these standards elevates unit costs but creates a premium segment where vendors can differentiate on assurance levels, driving a steady revenue stream even when commercial demand is cyclical.

Lower Launch Costs Expanding Mission Count

Reusable launch vehicles have dropped average LEO insertion prices toward USD 2,700 per kg, enabling universities, start-ups, and emerging-economy governments to sponsor missions once considered uneconomic. Lower barriers translate into a broader customer base seeking turnkey computing modules that slot into CubeSat frames or standardized microsatellite buses without lengthy integration. Rideshare manifests further favor plug-and-play electronics because launch providers bundle diverse payloads bound for different orbital planes. The same cost dynamics encourage constellation operators to fly on-orbit spares, relaxing individual satellite reliability targets and raising aggregate hardware demand. Looking ahead, commercial space stations and orbital manufacturing facilities will require autonomous control computers capable of managing life-support loops, robotic manipulators, and in-situ resource utilization processes, reinforcing long-term growth prospects for radiation-tolerant, software-defined computing platforms.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of rad-hard electronics | -1.8% | Global, with emerging markets most affected | Long term (≥ 4 years) |

| Space-grade semiconductor supply bottlenecks | -1.5% | Global, with Asia-Pacific manufacturing concentration | Short term (≤ 2 years) |

| EMI from mega-constellation cross-links | -1.2% | Global, concentrated in heavily congested orbital regions | Medium term (2-4 years) |

| AI accelerator thermal/radiation limits | -1.0% | Global, affecting advanced computing applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Radiation-Hardened Electronics

Radiation-hardened components can cost more than 100 times their commercial counterparts because custom substrates, shielding, and lengthy qualification soak tests restrict economies of scale. Traditional techniques such as silicon-on-insulator wafers and triple-modular redundancy add further complexity, pushing unit prices beyond reach for price-sensitive constellation operators. Some firms now pursue hybrid designs that pair commercial dies with system-level redundancy, soft-error scrubbing, and selective shielding to balance risk and cost. Everspin’s spin-transfer-torque MRAM exemplifies targeted innovation; the technology achieves non-volatility, high endurance, and radiation tolerance without resorting to exotic fabrication, trimming material premiums while satisfying mission resilience thresholds. Even so, capital budgets remain strained when fleet sizes exceed thousands of spacecraft, and operators lobby regulators to relax qualification thresholds in favor of “good-enough” reliability models shaped by statistical redundancy across the constellation.

Space-Grade Semiconductor Supply Bottlenecks

Radiation-tolerant processors and memories depend on a handful of specialty foundries, many concentrated in East Asia, which exposes satellite programs to earthquakes, power outages, or geopolitical tensions. Long lead times often exceeding 18 months reflect wafer-fab queue constraints and mandatory lot-acceptance testing, so any production hiccup can cascade into launch delays. Recent mergers, notably BAE Systems’ USD 4.8 billion purchase of Ball Aerospace, illustrate strategic vertical integration intended to lock down secure component flows and in-house packaging capabilities. Yet such consolidation can limit second-source options, reducing buyer leverage and amplifying systemic risk. US and European Union governments have responded with funding incentives for domestic rad-hard fabs. Still, meaningful capacity diversification will take years, keeping supply tight and prices elevated in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Processors Drive Integration

Processors and controllers generated 34.65% revenue in 2024, confirming their role as the coordination core of every subsystem. This share equates to the most significant slice of the satellite onboard computing system market, and demand continues to rise as software-defined operations proliferate. Memory Units follow, buoyed by MRAM adoption that combines non-volatility with high endurance. Data-handling interfaces gain relevance due to swelling sensor payloads that must pre-process data before download.

Software and operating systems is the fastest-growing component at a 14.60% CAGR, reflecting the shift toward mission re-configurability through over-the-air updates. ECSS-E-ST-40C governs software life-cycle practices across Europe, ensuring cross-platform compatibility and predictable response times. Power management and thermal housings round out the stack, addressing heat dissipation and energy constraints intrinsic to high-density processors. Suppliers that package these layers into modular “compute tiles” strengthen their bargaining power with prime contractors. The satellite onboard computing system market size linked to software and operating systems is projected to expand more quickly than any hardware category by 2030.

By Satellite Platform Size: Small Satellites Dominate

Small satellites between 101 kg and 500 kg control 41.50% of 2024 revenue, reflecting an optimal mix of payload volume and ride-share economics. This class can host multi-core rad-hard CPUs and sizeable memory banks without breaching mass budgets. Medium and large satellites serve deep-space science, radar imaging, or broadcast duties demanding heavy power budgets.

Pico/nano satellites under 10 kg show a 16.70% CAGR, propelled by CubeSat standards and academic R&D. Miniaturized processors and hybrid MRAM/SRAM memory let even these tiny buses run edge-AI workloads. Swarm architectures distribute tasks such as image mosaicking across dozens of nodes. As a result, the satellite onboard computing system market enjoys a widening customer base that now includes universities, research labs, and emerging-economy operators.

By Orbit: LEO Dominance with HEO Upside

LEO maintained a 67.80% share in 2024, underpinned by broadband constellations and daily imaging services. Short signal paths mean less onboard transmit power, lower latency, and tighter feedback loops between spacecraft and users. This efficiency reduces system mass, benefiting the overall satellite onboard computing system market size.

HEO missions grow at 14.42% CAGR as governments demand persistent Arctic coverage for communications and surveillance. HEO crossings through the Van Allen belts expose electronics to severe radiation, boosting demand for hardened chipsets and advanced scrubbing. Designers increasingly deploy phase-change thermal materials to keep CPU junction temperatures within safe limits, protecting system reliability across wide orbital temperature swings.

By Application: Communication Leads, Earth Observation Accelerates

Communication payloads claimed 43.30% revenue share in 2024 because modern digital processors must manage thousands of steerable beams and dynamic spectrum allocation. Software-defined radios (SDRs) let operators push firmware that retunes frequencies on demand. Navigation satellite refreshes, such as GPS III, keep demand steady for precision timing processors.

Earth observation exhibits the fastest rise, with a 13.65% CAGR. Onboard GPUs now perform real-time analytics on hyperspectral or SAR images, cutting raw-data downlink volumes and latency to insight. Radiation-tolerant AI accelerators from suppliers such as Cosmic Shielding enable these tasks without prohibitive power draw. The satellite onboard computing system market thus expands into value-added services, not just data delivery.

By End-User: Commercial Growth Outpaces Defense

Commercial and civil entities accounted for 57.10% of revenue in 2024, benefiting from venture capital inflows and the recurring revenue lure of connectivity services. They prize time-to-orbit and unit economics over absolute radiation immunity, favoring hybrid COTS-plus-rad-hard boards that hit price-performance sweet spots.

Defense and government demand, rising at a 12.70% CAGR, is rooted in the need for secure, autonomous ISR platforms. TEMPEST-grade shielding, quantum-safe encryption, and trusted supply chains increase program costs but keep volumes significant. Vertical integration among primes consolidates procurement, influencing future vendor selection. Balanced growth rates keep the satellite onboard computing system market resilient to single-sector downturns.

Geography Analysis

North America led with 37.90% revenue in 2024 on vertically integrated aerospace primes, deep venture funding, and government procurement that mandates domestic content. Mega-constellation rollouts from SpaceX and Amazon drive volume orders for compute modules, while the US Space Force channels classified demand toward rad-hard subcontractors. ITAR rules shield local vendors yet complicate export ambitions.

Europe leverages ESA funding and ECSS standards to sustain a robust supply ecosystem. Airbus and Thales champion software-defined satellites that align with sovereign industrial policy. The EU Chips Act directs investment toward resilient semiconductor fabs, a move expected to lower exposure to Asian foundries by the late-decade horizon.

Asia-Pacific records the fastest CAGR at 13.50%, anchored by China’s state-backed constellation programs, India’s cost-efficient launch assets, and Japan’s semiconductor prowess. Indigenous processor projects in China and India aim to curb reliance on US or EU suppliers, adding new capacity to the satellite onboard computing system market. South Korea and Australia expand their space ecosystems through public-private partnerships, while Southeast Asian operators explore small-sat platforms for maritime surveillance. Middle East and African nations pursue Earth-observation satellites suited to arid climate monitoring, spurring niche demand for rugged compute boards.

Competitive Landscape

The satellite onboard computing system market is moderately fragmented, featuring incumbent primes like Lockheed Martin, BAE Systems, Northrop Grumman, Airbus, and Thales alongside specialized chipmakers like Microchip Technology and Frontgrade Gaisler. Legacy vendors benefit from certified supply chains, long-flight heritage, and bundled platform offerings.

Consolidation is accelerating. BAE Systems absorbed Ball Aerospace for USD 4.8 billion to secure payload and computing depth, while Lockheed Martin spent USD 450 million on Terran Orbital to gain automated small-sat assembly lines [flightglobal.com]. These deals reduce supplier count and concentrate bargaining power.

Disruptive entrants target RISC-V processors, MRAM memory, and radiation-aware AI accelerators that bridge the cost-performance gap between commercial silicon and space-grade hardware. Firms that can certify software stacks to ECSS-E-ST-80C security standards while retaining commercial-grade economics stand to draw design wins in next-generation constellations. Innovation and consolidation coexist, sustaining competitive tension and propelling the satellite onboard computing system market forward.

Satellite Onboard Computing System Industry Leaders

Airbus SE

BAE Systems plc

Honeywell International Inc.

Microchip Technology Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Redwire Corporation strategically delivered the onboard computer for ESA’s Comet Interceptor mission. Developed under a contract with OHB Italia S.p.A., this achievement positions Redwire as a key player in advancing space exploration, enabling the study of a pristine comet carrying untouched material from the Solar System’s formation.

- August 2024: Dhruva Space partnered with Singapore-based Zero-Error Systems (ZES) to enhance its On-Board Computer (OBC) subsystem. By integrating ZES' LDAP-IC-ZES100, this collaboration aims to protect COTS electronics from radiation-induced micro-SEL/SEL while improving performance, reliability, and processing power for Dhruva Space's upcoming satellite missions.

Global Satellite Onboard Computing System Market Report Scope

| Processors and Controllers |

| Memory Units |

| Data handling and Interfaces |

| Power Management Units |

| Thermal Management and Housing |

| Software and Operating System |

| Pico/Nano Satellites (Less than 10 kg) |

| Micro Satellites (10 to 100 kg) |

| Small Satellites (101 to 500 kg) |

| Medium Satellites (501 to 1,000 kg) |

| Large Satellites (Greater than 1,000 kg) |

| Low Earth Orbit (LEO) |

| Medium Earth Orbit (MEO) |

| Geostationary Earth Orbit (GEO) |

| Highly Elliptical Orbit (HEO) |

| Communication |

| Earth Observation |

| Navigation |

| Meteorology |

| Others |

| Commercial and Civil |

| Defense and Government |

| Research and Educational Institutes |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Component | Processors and Controllers | ||

| Memory Units | |||

| Data handling and Interfaces | |||

| Power Management Units | |||

| Thermal Management and Housing | |||

| Software and Operating System | |||

| By Satellite Platform Size | Pico/Nano Satellites (Less than 10 kg) | ||

| Micro Satellites (10 to 100 kg) | |||

| Small Satellites (101 to 500 kg) | |||

| Medium Satellites (501 to 1,000 kg) | |||

| Large Satellites (Greater than 1,000 kg) | |||

| By Orbit | Low Earth Orbit (LEO) | ||

| Medium Earth Orbit (MEO) | |||

| Geostationary Earth Orbit (GEO) | |||

| Highly Elliptical Orbit (HEO) | |||

| By Application | Communication | ||

| Earth Observation | |||

| Navigation | |||

| Meteorology | |||

| Others | |||

| By End-User | Commercial and Civil | ||

| Defense and Government | |||

| Research and Educational Institutes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Satellite on-board computing system market in 2025?

It is valued at USD 2.15 billion, with a projected rise to USD 3.50 billion by 2030, advancing at a 10.24% CAGR.

Which component segment is growing fastest?

Software and operating systems posts the highest growth at a 14.60% CAGR to 2030.

What orbit segment drives most revenue today?

LEO accounts for 67.80% of 2024 revenue, thanks to broadband constellations.

Why is Asia-Pacific the fastest-growing region?

National programs in China, India, and Japan pursue indigenous processors and constellation rollouts, lifting regional CAGR to 13.50%.

How are defense needs shaping product design?

Secure, jam-resistant computing that processes classified data on board is pushing vendors to integrate encryption, radiation-hardening, and AI accelerators.

What challenges could slow market growth?

High costs for rad-hard parts and limited foundry capacity create supply risks that can delay satellite programs.

Page last updated on: