Satellite IoT Communication Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

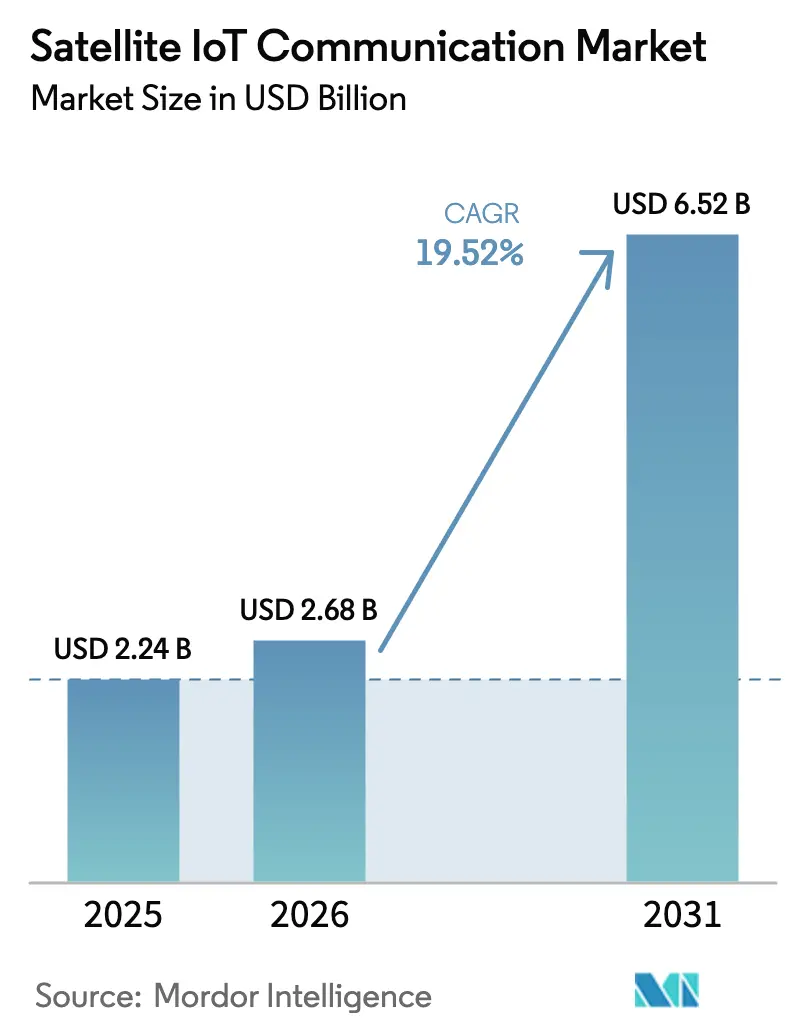

| Market Size (2026) | USD 2.68 Billion |

| Market Size (2031) | USD 6.52 Billion |

| Growth Rate (2026 - 2031) | 19.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Satellite IoT Communication Market Analysis by Mordor Intelligence

The Satellite IoT Communication Market size was valued at USD 2.24 billion in 2025 and estimated to grow from USD 2.68 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 19.52% during the forecast period (2026-2031). This vigorous pace links directly to the harmonization of 5G-Advanced Non-Terrestrial Network (NTN) standards, falling small-satellite launch prices, and public funding that underwrites rural rollouts. Standardized Release 17 and 18 specifications now let devices roam between space- and land-based networks without protocol changes [1]3rd Generation Partnership Project, “Release 17 & 18 Specifications for 5G-Advanced Non-Terrestrial Networks,” 3gpp.org. At the same time, rideshare launch fees have dropped below USD 5,000 per kg, removing cost barriers for new constellations [2]Space Exploration Technologies Corp., “Rideshare Program and Small Satellite Launch Services,” spacex.com. Government capital grants under the USD 65 billion ReConnect and EUR 2.4 billion CEF-Digital programs shrink deployment risk in thinly populated regions [3]United States Department of Agriculture, “ReConnect Program Rural Broadband Funding,” usda.gov. Extra-narrowband spectrum cleared at WRC-23, coupled with stricter maritime ESG mandates, further expands addressable demand in shipping, agriculture, and environmental monitoring [4]International Telecommunication Union, “World Radiocommunication Conference 2023 Spectrum Allocations,” itu.int.

Key Report Takeaways

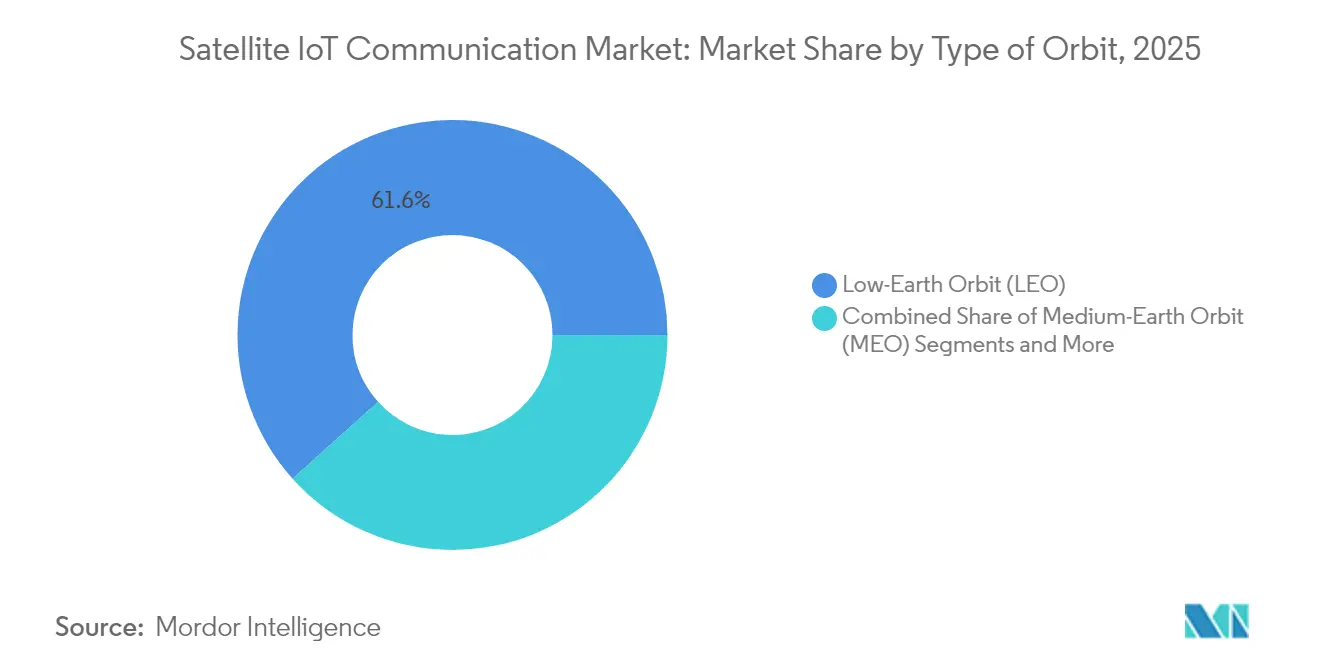

- By type of orbit, LEO satellites led with 61.65% of the satellite IoT communication market share in 2025; MEO systems are projected to grow at a 20.05% CAGR through 2031.

- By frequency band, L-Band held 28.25% revenue share in 2025, while Ka-Band shows the highest expansion at a 20.12% CAGR to 2031.

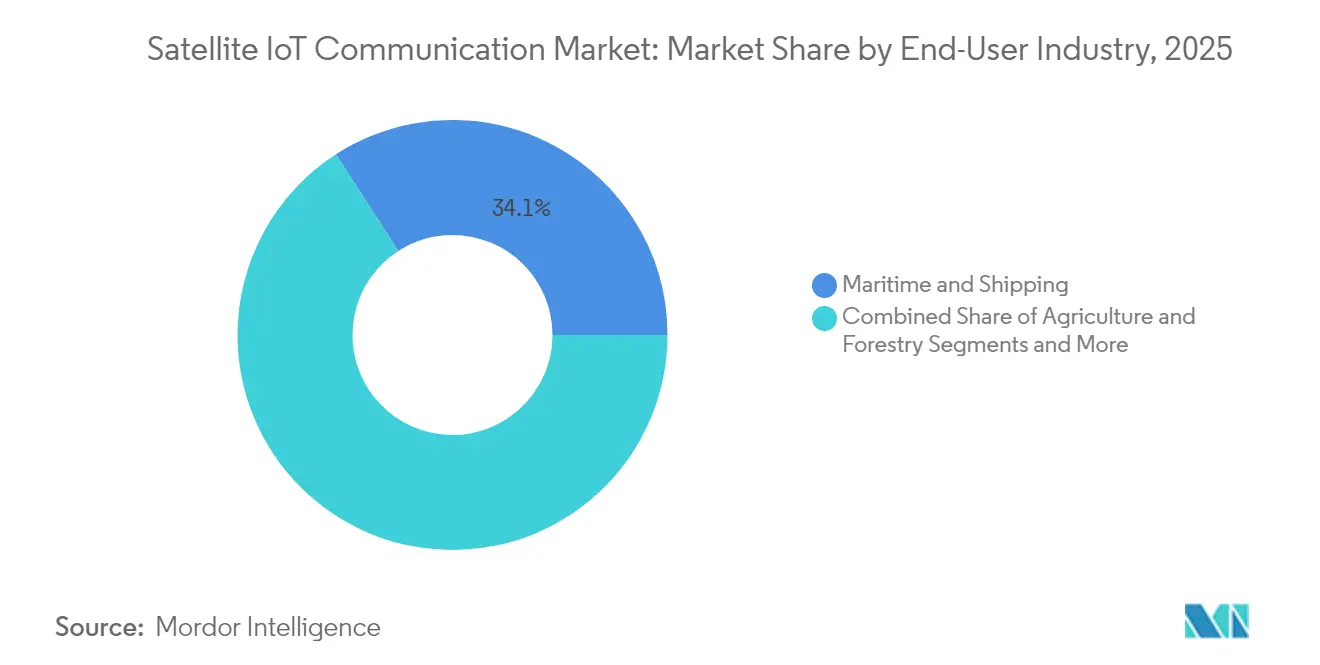

- By end-user industry, maritime and shipping accounted for a 34.12% share of the satellite IoT communication market size in 2025, whereas environmental monitoring is advancing at a 20.78% CAGR through 2031.

- By service type, satellite asset tracking commanded a 40.55% share of the satellite IoT communication market size in 2025; direct-to-device connectivity records the fastest 20.64% CAGR through 2031.

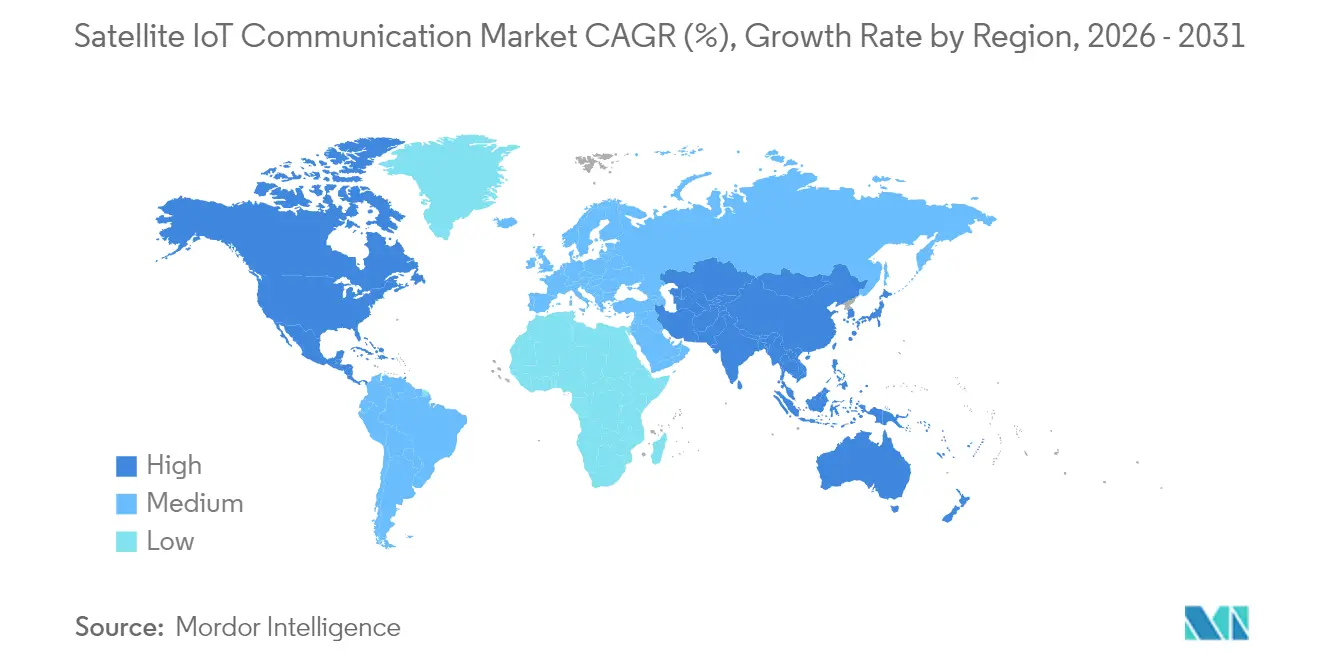

- By geography, North America occupied a 35.05% share in 2025, while the Asia Pacific is set to climb at a 20.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Satellite IoT Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Development and growth of 5G-Advanced NTN specifications | +3.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rapid drop in manufacturing and launch costs of <200 kg satellites | +4.1% | Global, concentrated in regions with launch capabilities | Short term (≤ 2 years) |

| Government rural-connectivity subsidies (e.g., US ReConnect, EU CEF-Digital) | +2.8% | North America and Europe primarily, expanding to APAC | Medium term (2-4 years) |

| New ITU spectrum allocations (WRC-23) for narrowband IoT links | +2.3% | Global | Long term (≥ 4 years) |

| Maritime ESG compliance demand for continuous asset telemetry | +3.4% | Global, with concentration in major shipping routes | Short term (≤ 2 years) |

| Carbon-credit traceability for remote agriculture and forestry | +1.7% | APAC core, spill-over to South America and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Development and Growth of 5G-Advanced NTN Specifications

Release 17 and 18 specifications unify terrestrial and satellite connectivity, removing the need for dual-mode chipsets and cutting device bill-of-materials by up to 30%. Doppler shift compensation and timing-advance algorithms built into the standard stabilize links from rapidly moving LEO spacecraft, supporting delay-sensitive applications such as remote robotics. Regulators, including the FCC and ETSI, now embed these rules in device certification, trimming launch-to-market cycles. Seamless roaming means industrial IoT installations remain connected during terrestrial outages, an advantage heightened during extreme-weather emergencies. The framework also opens native smartphone connectivity, driving consumer familiarity that will spill over into enterprise demand.

Rapid Drop in Manufacturing and Launch Costs of Sub-200 kg Satellites

Standardized satellite buses, additive manufacturing, and bulk component orders have cut per-unit build costs from USD 500,000 in 2020 to under USD 150,000 in 2024. With launch fees now below USD 5,000 per kg on rideshare missions, a 24-satellite IoT constellation can orbit for under USD 80 million, hitting financing thresholds that venture capital is willing to underwrite. New entrants exploit this cost curve to tailor power budgets and antenna patterns for low-rate telemetry instead of retrofitting broadband birds. Agriculture-focused networks, for example, fly narrow-beam L-Band payloads optimized for soil-sensor packets. Cost trajectories are expected to fall further as in-orbit servicing extends spacecraft life, reducing replenishment needs.

Government Rural-Connectivity Subsidies Drive Infrastructure Investment

Public subsidies reduce capital intensity by up to 60% for operators that extend coverage to zones beyond profitable terrestrial reach. ReConnect awards bundle grants and low-interest loans, encouraging hybrid networks that link surface LoRa gateways through LEO backhaul. CEF-Digital earmarks EUR 2.4 billion for similar projects, tagging precision agriculture and environmental monitoring as priority use cases. Subsidies also fund integration pilots with farm-management software and SCADA platforms, creating reference customers that validate performance. China’s rural revitalization plan assigns satellite links to village cooperatives, though exact IoT carve-outs remain undisclosed. Collectively, these programs create baseline demand that smooths revenue volatility in the satellite IoT communication market.

New ITU Spectrum Allocations Enable Expanded Capacity

WRC-23 freed 1.6-1.7 GHz and 2.4-2.5 GHz blocks for narrowband satellite IoT, boosting usable bandwidth by about 40% and easing congestion in crowded L- and S-bands. Binding interference-protection rules shield these links from terrestrial mobile spillover, preventing packet loss on mission-critical telemetry. Satellite operators must file detailed power-flux-density plans, favoring incumbents with existing coordination teams. The package also opens experimental allocations that permit direct-to-device handheld links, accelerating consumer adoption. As global filings are clear, constellations can scale node counts per satellite without triggering service degradations, underpinning volume growth in the satellite IoT communication market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Congestion and interference in crowded L- and S-bands | -2.1% | Global, particularly dense shipping routes and urban areas | Short term (≤ 2 years) |

| Limited battery life of ground sensors in remote cold regions | -1.4% | Northern regions (Canada, Russia, Scandinavia, Alaska) | Medium term (2-4 years) |

| Lack of global standard for Sat-to-Device antenna modules | -1.8% | Global | Medium term (2-4 years) |

| Rising space-debris mitigation insurance premiums | -1.2% | Global, concentrated among LEO operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Congestion and Interference in Crowded L- and S-Bands

L- and S-band links face growing packet collisions as maritime and logistics users add endpoints, with interference incidents up 45% between 2023 and 2024. Peak traffic on shipping lanes can cut throughput by 30%, forcing resends that drain sensor batteries. Legacy coordination schemes designed for voice circuits cannot handle millions of bursty IoT transmissions. Operators shift some traffic into Ka-Band, but rain fade and higher terminal costs limit mass adoption. Until adaptive beamforming and dynamic channel allocation mature, service-quality uncertainty may dampen near-term uptake, shaving growth off the satellite IoT communication market.

Limited Battery Life of Ground Sensors in Remote Cold Regions

Battery degradation of up to 70% in Arctic climates forces maintenance cycles inside 24 months, compared with five-year lifetimes in temperate zones. Lithium-ion capacity drops 20% for each 10 °C below zero, while transmit-power requirements rise due to component inefficiency. Limited daylight restricts solar recharging, raising the total cost of ownership for oil-pipeline monitors and wildlife tags. Advanced chemistries such as lithium-thionyl chloride improve endurance yet remain too costly for volume deployment. Unless low-temperature energy harvesting or ultralow-power modems reach scale, this constraint will cap addressable device counts in high-latitude portions of the satellite IoT communication market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Orbit: Latency-Smart LEO Retains Lead While Cost-Efficient MEO Accelerates

Low-Earth Orbit platforms captured 61.65% of the satellite IoT communication market share in 2025, leveraging sub-100 millisecond round-trip latency that supports autonomous vehicle telemetry and closed-loop industrial control. This dominance translates into large production runs, sometimes over 1,000 spacecraft, that unlock supplier volume discounts and rapid iteration cycles. However, MEO networks are expanding at a 20.05% CAGR because eight to twenty satellites can blanket the globe, cutting constellation capex by as much as 50% relative to LEO fleets.

The operational calculus differs across customer groups. Battery-powered sensors in remote mining sites often favor LEO because lower link budgets extend battery life. Maritime operators eye MEO for uninterrupted coverage on polar routes where LEO passes create brief outages. Regulatory bodies now weigh orbital-slot filings against debris-mitigation plans, a factor that could tilt future launches toward higher altitudes with longer orbital lifetimes. Both architectures, therefore, coexist, supporting varied service-level agreements inside the satellite IoT communication market.

By Frequency Band: Workhorse L-Band Meets High-Capacity Ka

L-Band maintained a 28.25% share of 2025 revenue, trusted for foliage-penetrating, all-weather links needed in maritime and crop-monitoring applications. Devices can operate on milliwatts, stretching battery life and bringing subscription fees within reach of price-sensitive agribusinesses. Ka-Band, despite its weather vulnerability, posts a leading 20.12% CAGR as spectrum abundance allows higher throughputs that support imagery and video-centric edge analytics.

Migration paths vary by vertical. Environmental monitoring agencies adopt Ka for streaming multispectral data, while asset-tracking fleets stick with L-Band until terminal costs fall. Spectrum coordination hurdles persist: newcomers must negotiate with incumbents that hold global filings, which could slow competitive entry but also safeguard service quality. The balance suggests a multiband future where operators mix payloads to hedge against frequency-specific constraints, enriching solution depth in the satellite IoT communication market.

By End-User Industry: Maritime Compliance Dominates; Environmental Monitoring Surges

Maritime and shipping applications accounted for 34.12% of 2025 revenue, driven by International Maritime Organization rules mandating continuous emissions and route reporting. Vessel telemetry combines GPS, fuel-rate, and cargo-condition data, feeding carbon-accounting dashboards for charterers. Environmental monitoring, though smaller today, is rising at a 20.78% CAGR as governments tie carbon-credit issuance to sensor-verified datasets.

Diversification improves resilience. Agriculture uses soil-moisture sensing to trim water and fertilizer inputs, while defense agencies deploy border surveillance masts that push encrypted alerts via satellite backhaul. Utilities monitor wildfire-prone transmission lines, and extractive industries watch tailings dams to prevent catastrophic spills. The breadth of demand protects the satellite IoT communication market from over-reliance on any single vertical, supporting steady long-run growth.

By Service Type: Asset Tracking Sustains Scale; Direct-to-Device Unlocks New Volumes

Satellite asset tracking held 40.55% of the satellite IoT communication market size in 2025, the historical cornerstone that underpins logistics and theft-prevention value propositions. Mature APIs integrate with warehouse management software, creating switching costs that favor incumbent operators. Direct-to-device connectivity, however, is expanding fastest at a 20.64% CAGR thanks to 3GPP-standard roaming into NTN layers that smartphone makers embed at the chipset level.

Remote monitoring and control sits between these extremes, serving oil wells, water-treatment plants, and renewable-energy farms where crews visit only for scheduled maintenance. Backhaul connectivity forms the underlying transport on which all other services rely, bundling multiple device streams into a single satellite link. Collectively, the service stack widens the total addressable space, cementing multi-application demand in the satellite IoT communication market.

Geography Analysis

North America commanded 35.05% of 2025 revenue, buoyed by defense surveillance budgets and the ReConnect subsidy that underwrites rural deployments. Arctic sovereignty patrols drive Canada’s purchase of cold-weather-tolerant sensors, while US coastal shipping lanes adopt emissions tracking to comply with ESG scorecards. Mexico’s near-shore manufacturing exports rely on satellite telemetry to maintain just-in-time inventory flows between inland plants and border crossings.

Asia Pacific registers the fastest 20.85% CAGR to 2031 as China, India, and Southeast Asian states scale digital agriculture. China’s rural revitalization agenda channels public lending into cooperative-owned sensor networks, and India’s domestic launch capacity lowers access costs for local integrators. Japan and South Korea showcase factory-floor automation that depends on uninterrupted IoT data feeds, while Australia’s mining belts outfit haul-roads and conveyor lines with satellite gateways to monitor equipment health.

Europe delivers steady expansion underpinned by ESG regulation and the CEF-Digital fund. Germany’s precision-farming subsidies reimburse satellite subscription fees, and French aquaculture firms meet traceability mandates via continuous telemetry. The U.K. advances smart-port initiatives that use satellite analytics to optimize berth allocation. Beyond these mature regions, the Middle East and Africa emerge as opportunity pools where oil operators and agritech programs tap satellite IoT to overcome terrestrial gaps, broadening geographic revenue diversity in the satellite IoT communication market.

Competitive Landscape

Market structure remains moderately fragmented. Iridium Communications and ORBCOMM preserve scale through legacy constellations, regulatory clearances, and vertically integrated device portfolios. Yet launch-cost deflation lets entrants such as Fleet Space Technologies field narrowband fleets at capital requirements under USD 100 million. Strategic moves center on locking down spectrum filings, buying modem makers, and offering cloud dashboards that minimize customer integration work.

Direct-to-device propositions intensify rivalry as Apple and Android chipset vendors embed NTN messaging. Incumbents respond by partnering with carriers; Iridium aligned with Deutsche Telekom in September 2025 to meld satellite fallback into terrestrial footprints. Environmental-monitoring specialism forms another battleground; Swarm positions nanosatellites at ultra-low power tiers while legacy providers upscale payload sensitivity. Meanwhile, the FCC’s orbital-debris rules push insurance premiums higher, a hurdle newcomers counter with on-orbit drag sails.

Overall, suppliers compete on latency, power efficiency, and API simplicity rather than raw bandwidth. This spectrum of differentiation encourages multipolar rivalry, sustaining innovation cadence inside the satellite IoT communication market.

Satellite IoT Communication Industry Leaders

-

Iridium Communications Inc.

-

ORBCOMM Inc.

-

Inmarsat (Viasat, Inc.)

-

Globalstar, Inc.

-

Fleet Space Technologies Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Iridium Communications partnered with Deutsche Telekom to deliver global connectivity through the upcoming NTN Direct service, integrating satellite links into the carrier’s terrestrial IoT backbone.

- May 2025: Iridium Communications teamed with Syniverse to streamline NTN Direct roaming for mobile network operators, enabling continuous handset coverage worldwide.

- June 2024: ORBCOMM unveiled OGx, a next-generation satellite IoT service that lowers device power draw through patented waveform technology and offers flexible subscription pricing.

Global Satellite IoT Communication Market Report Scope

Satellite IoT refers to using satellite communication services and networks to connect terrestrial IoT sensors and end nodes to a server (e.g., in a private or public cloud), either in alternative with or in conjunction with terrestrial communication networks.

The Satellite IoT Communication Market is segmented by Type of Orbit (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Geostationary Orbit (GEO)), by Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Low-Earth Orbit (LEO) |

| Medium-Earth Orbit (MEO) |

| Geostationary Orbit (GEO) |

| L-Band |

| S-Band |

| C-Band |

| Ku-Band |

| Ka-Band |

| Maritime and Shipping |

| Agriculture and Forestry |

| Logistics and Intermodal Freight |

| Defense and Security |

| Environmental Monitoring |

| Other End-user Industries |

| Satellite Asset Tracking |

| Remote Monitoring and Control |

| Direct-to-Device Connectivity |

| Backhaul Connectivity |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Type of Orbit | Low-Earth Orbit (LEO) | |

| Medium-Earth Orbit (MEO) | ||

| Geostationary Orbit (GEO) | ||

| By Frequency Band | L-Band | |

| S-Band | ||

| C-Band | ||

| Ku-Band | ||

| Ka-Band | ||

| By End-user Industry | Maritime and Shipping | |

| Agriculture and Forestry | ||

| Logistics and Intermodal Freight | ||

| Defense and Security | ||

| Environmental Monitoring | ||

| Other End-user Industries | ||

| By Service Type | Satellite Asset Tracking | |

| Remote Monitoring and Control | ||

| Direct-to-Device Connectivity | ||

| Backhaul Connectivity | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the satellite IoT communication market in 2026?

It is valued at USD 2.68 billion in 2026 and is on track to post a 19.52% CAGR to 2031.

Which orbit class holds the largest share today?

Low-Earth Orbit networks account for 61.65% of 2025 revenue due to their latency and power advantages.

What is the fastest-growing application segment?

Direct-to-device connectivity leads with a projected 20.64% CAGR through 2031 as smartphones adopt satellite fallback.

Which region will expand quickest by 2031?

Asia Pacific is set for a 20.85% CAGR, driven by digital agriculture programs and domestic launch capacity.

What regulatory change most benefits future growth?

New ITU spectrum allocations at 1.6–1.7 GHz and 2.4–2.5 GHz add 40% capacity for narrowband satellite IoT links.

How do falling launch costs affect competition?

Sub-USD 5,000 per kg rideshare pricing allows startups to field constellations for under USD 100 million, intensifying rivalry.

Page last updated on: