Narrowband IoT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

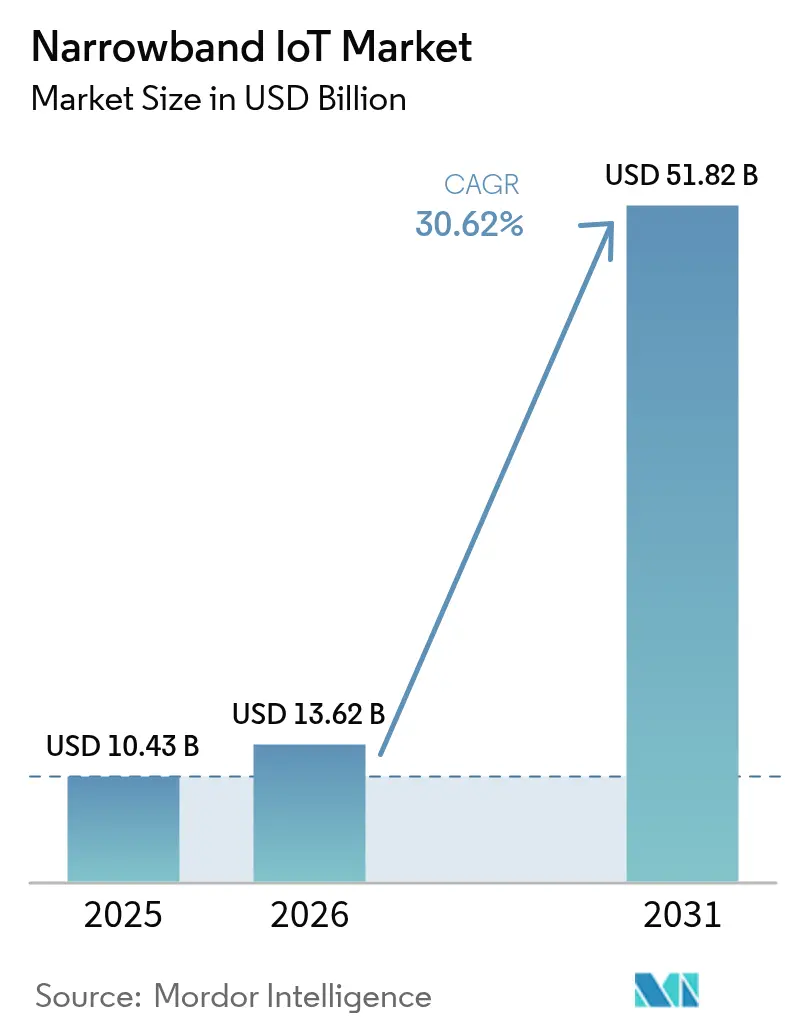

| Market Size (2026) | USD 13.62 Billion |

| Market Size (2031) | USD 51.82 Billion |

| Growth Rate (2026 - 2031) | 30.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Narrowband IoT Market Analysis by Mordor Intelligence

Narrowband IoT market size in 2026 is estimated at USD 13.62 billion, growing from 2025 value of USD 10.43 billion with 2031 projections showing USD 51.82 billion, growing at 30.62% CAGR over 2026-2031.

This growth reflects converging demand for ultra-low-power devices, government-mandated smart infrastructure, and the strategic use of satellite links that extend coverage beyond terrestrial footprints. Operators are prioritizing guard-band spectrum efficiencies and 5G NR-RedCap migration paths that safeguard long-term investments while broadening service portfolios. Technical fragmentation between major infrastructure vendors remains a headwind yet falling module prices and battery lifetimes approaching 10 years continue to unlock high-volume applications in utilities, logistics, and agriculture. The NB-IoT market is therefore progressing from network-centric roll-outs toward device-driven scale as module ASPs slide below USD 3.00.

Key Report Takeaways

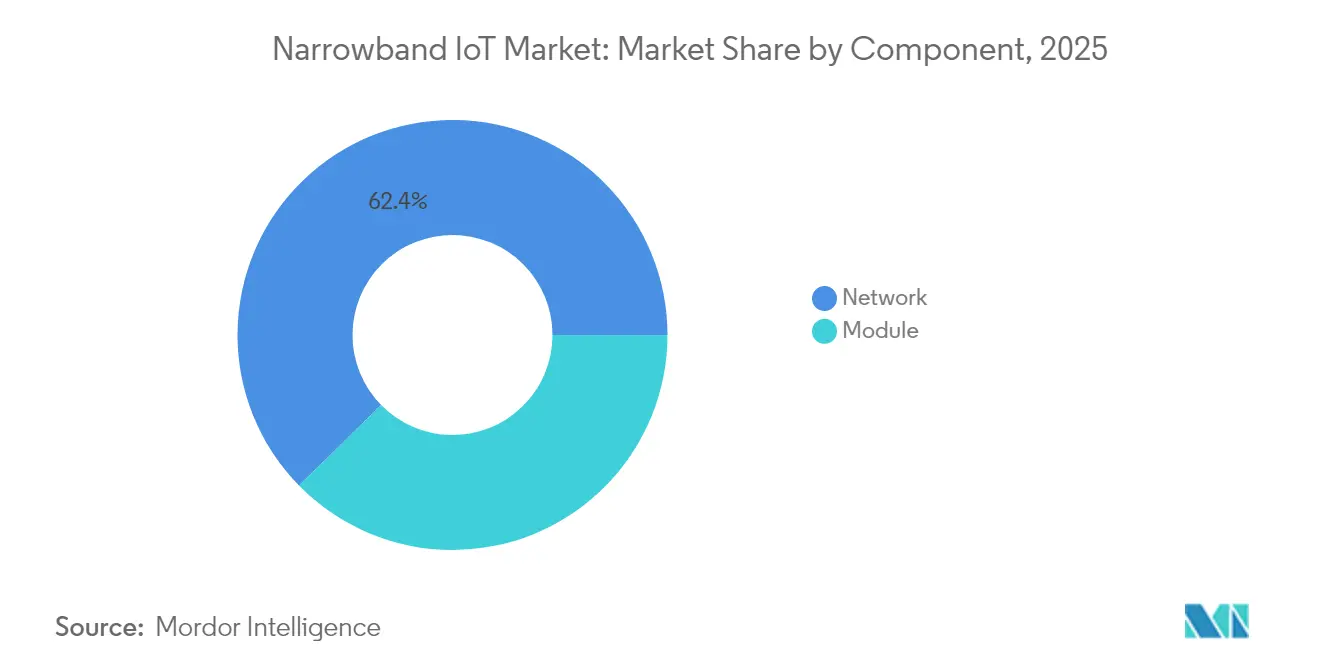

- By component, network infrastructure led with 62.35% revenue share in 2025, while modules are set to rise at 32.55% CAGR through 2031.

- By deployment, stand-alone configurations held 46.65% of NB-IoT market share in 2025; guard-band solutions are on track for a 34.10% CAGR to 2031.

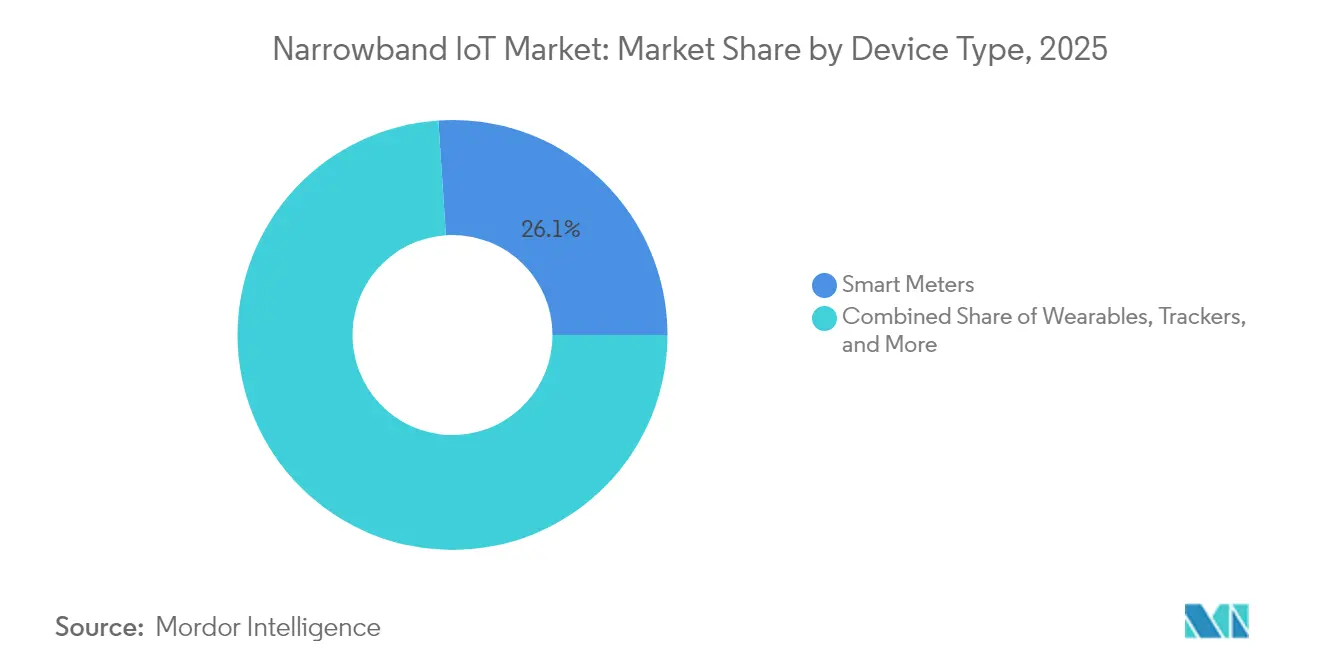

- By device type, smart meters commanded 26.05% of the NB-IoT market size in 2025, and trackers are forecast to expand at 32.12% CAGR to 2031.

- By application, energy and utilities captured 28.25% revenue in 2025, while agriculture and livestock are positioned for a 32.40% CAGR through 2031.

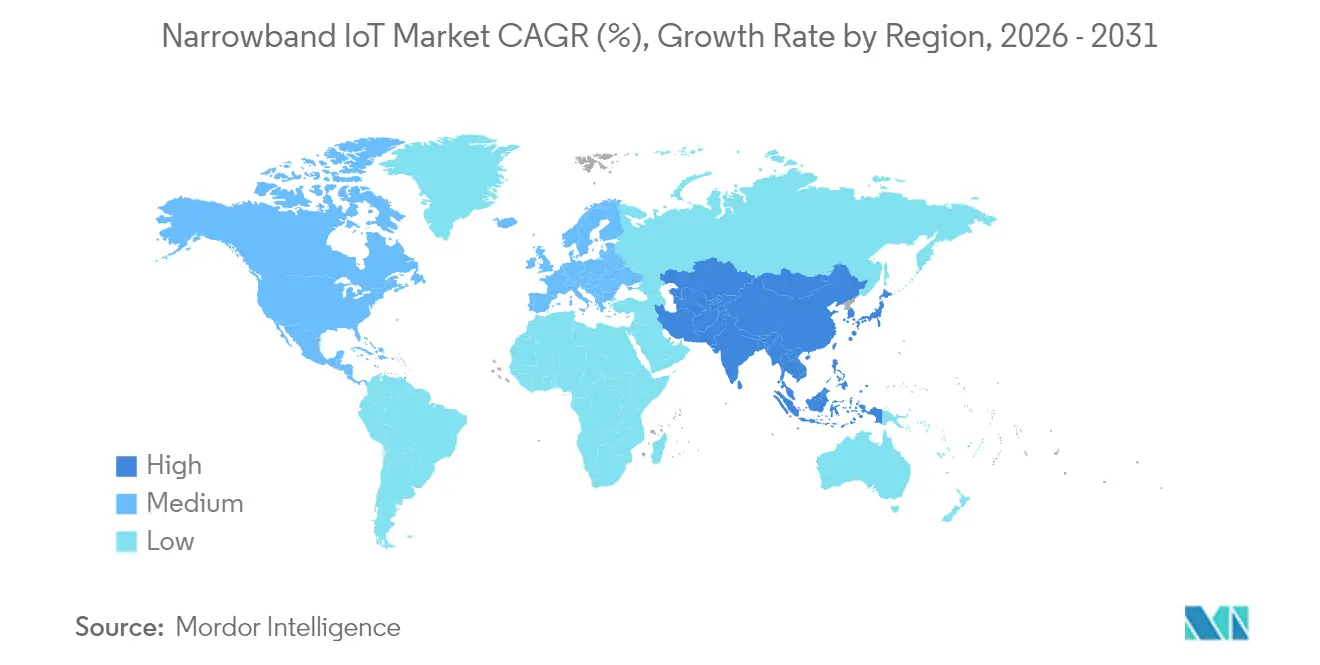

- Regionally, Asia Pacific accounted for 51.75% revenue in 2025 and is projected to grow at 33.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Narrowband IoT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-low power consumption extends battery life | +4.20% | Global, strongest in APAC and Europe | Medium term (2–4 years) |

| Falling NB-IoT module ASPs below USD 3 | +6.80% | Global, notably APAC and Africa | Short term (≤ 2 years) |

| Government-mandated LPWAN roll-outs for smart metering | +5.10% | Europe, North America, Australia | Medium term (2–4 years) |

| Government incentives for smart agriculture and digitisation | +3.90% | APAC core, Australia, select EU markets | Long term (≥ 4 years) |

| Satellite-augmented NB-IoT for remote assets | +2.7% | Global, maritime, mining, and remote farming | Long term (≥ 4 years) |

| 5G NR-RedCap roadmap continuity | +1.8% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ultra-low power consumption extends battery life

Devices can operate for up to 10 years on a single battery by leveraging eDRX, PSM, and Early Data Transmission that collectively cut energy draw and latency[1]Cavli Wireless, “NB-IoT Power-Saving Modes Explained,” cavliwireless.com. Field tests show Pre-Configured Uplink Resources lower energy use 2.5 times and lengthen battery life 1.6 times under dense traffic. This power profile reshapes utility economics because battery replacement often exceeds hardware cost. Support for 50,000 devices per cell adds scale without compromising endurance, validating NB-IoT market adoption across remote metering.

Falling NB-IoT module ASPs below USD 3, enabling mass adoption

Manufacturing scale and integrated chipsets pulled average module prices beneath USD 3.00, unlocking cost-sensitive sectors such as environmental sensing and asset tracking. Subscription fees have also fallen to USD 0.50 per month, giving NB-IoT market propositions parity with unlicensed LPWAN alternatives[2]2Smart, “Low-Cost NB-IoT Connectivity Plans,” 2smart.com. World-mode modems now deliver global band support, letting OEMs certify once and ship worldwide, accelerating device volumes in emerging regions.

Government-mandated LPWAN roll-outs for smart metering

EU energy efficiency rules and Australia’s USD 30 million On-Farm Connectivity Program guarantee steady demand for NB-IoT deployments in water and electricity metering. NB-IoT’s 20 dB coverage gain versus GSM ensures basement meters reliably communicate without repeaters. Mandatory timelines give suppliers volume certainty, sustaining the NB-IoT market over multi-year roll-out horizons.

Government incentives for smart agriculture and rural digitisation

Australia’s USD 48 million Farms of the Future and Victoria’s USD 10 million On-Farm IoT Trial subsidise sensors for soil, water, and livestock monitoring. Europe’s 5GAGRIHUB likewise funds precision-farming pilots. Deep coverage and decade-long batteries suit remote paddocks where power and backhaul are scarce, widening NB-IoT market penetration into rural economies.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from LTE-M and unlicensed LPWAN | -3.40% | North America, Europe, Australia | Short term (≤ 2 years) |

| Limited downlink throughput is hindering OTA updates | -2.10% | Global | Medium term (2–4 years) |

| A fragmented spectrum complicates global roaming | -1.9% | Global | Medium term (2–4 years) |

| Unproven revenue-sharing models | -1.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from LTE-M and unlicensed LPWAN (LoRa, Sigfox)

AT&T’s sunset of NB-IoT and migration to LTE-M highlights operator preference for higher data rates and better mobility when serving moving assets. LoRa’s forecast of 1.3 billion connections by 2030 underscores the private-network attraction for enterprises that need full control. This dual competitive front narrows the NB-IoT market focus to stationary, deep-coverage use cases unless throughput improvements materialise.

Limited downlink throughput is hindering OTA firmware updates

NB-IoT’s 250 kbps cap strains security patch delivery for industrial devices, forcing staggered update windows that prolong risk exposure. Dense networks exacerbate collisions and competing LPWANs now offer broadcast update modes that slash transfer times. Operators trial CoAP/UDP to optimise bandwidth, yet the structural ceiling remains a brake on adoption in smart-city segments needing frequent firmware refreshes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Network Infrastructure Drives Current Revenue

Network infrastructure generated 62.35% of 2025 revenue as operators upgraded cores and radios to support massive device density. This spending reflects the early phase of the NB-IoT market when coverage and capacity build outweigh device volumes. Modules, however, are projected to compound at 32.55% annually through 2031 as falling ASPs shift value downstream to OEMs. Integrated SoCs reduce bill-of-materials and simplify certification, enabling sub-USD 3.00 price points that catalyse high-volume roll-outs. Consumption-based 5G core services from cloud partnerships let carriers defer capex, altering the spending mix toward modules and backend analytics during the forecast window.

A maturing supply chain now offers chipset reference designs and turnkey antenna packages, lowering barriers for new entrants. The NB-IoT industry thus pivots from capacity expansion to application enablement, underscoring a gradual revenue transition from infrastructure to devices and data services.

By Deployment: Stand-alone Leads Despite Guard-band Acceleration

Stand-alone deployments held 46.65% revenue in 2025 because utilities and industrial users favour predictable performance in dedicated spectrum. China’s national smart-meter campaign reinforced this preference, anchoring early NB-IoT market growth on independent carriers. Guard-band strategies are accelerating at 34.10% CAGR as operators reclaim unused LTE buffers, aligning with European policy that prioritises spectral efficiency. In-band options act as midway solutions where guard bands are scarce, balancing coverage with legacy traffic coexistence.

Operators increasingly model spectrum value against expected device density, pushing guard-band adoption in markets with moderate scale. Conversely, mission-critical applications retain stand-alone designs due to isolation benefits. This duality will persist, shaping region-specific deployment blends that maximise both performance and asset utilisation.

By Device Type: Smart Meters Dominate While Trackers Surge

Smart meters captured 26.05% of NB-IoT market share in 2025 as regulatory timelines mandated nationwide roll-outs. Deep indoor penetration and decade-long batteries address basement installations impractical for higher-frequency 5G. Trackers, however, are poised for a 32.12% CAGR because satellite-augmented modules unlock global logistics, wildlife monitoring, and remote asset visibility. Wearables adopt NB-IoT for extended health-monitor lifetimes, while alarms leverage a reliable uplink during emergencies.

Device makers add multi-mode and pin-compatible footprints that let customers toggle between NB-IoT, RedCap, and LTE-M as service availability evolves. This flexibility mitigates technology-lock concerns and widens the NB-IoT market addressable base beyond fixed metering.

By Application: Energy Utilities Lead While Agriculture Accelerates

Energy and utilities generated 28.25% of 2025 revenue, driven by advanced metering infrastructure and grid modernisation goals. Coverage into subterranean vaults plays to NB-IoT strengths, while long lifecycles align with utility planning horizons. Agriculture and livestock sensors are forecast to climb 32.40% annually through 2031 as subsidy programmes defray capital outlays for remote soil and herd monitoring. Smart-city lighting, parking, and environmental networks also expand steadily, supported by municipal climate and safety initiatives.

Transportation operators adopt hybrid terrestrial-satellite NB-IoT for container telemetry outside cellular footprints, reducing cargo loss and streamlining customs. Industrial factories employ vibration and temperature sensors to detect failures early, decreasing downtime. Retail vending units integrate low-cost modules that reconcile inventory automatically, demonstrating the NB-IoT market's versatility across verticals.

Geography Analysis

Asia Pacific accounted for 51.75% revenue in 2025, owing to China Mobile’s 890 million managed connections and a 90% 5G penetration rate achieved by 2023. Industrial policy and massive public-sector tenders create predictable demand pipelines that foster supplier scale. India and Japan now pilot nationwide smart-meter projects, positioning them as secondary growth engines within the region. As stand-alone deployments mature, carriers pivot to guard-band optimisation to accommodate surging device counts without fresh spectrum auctions.

North America faces strategic realignment after AT&T’s NB-IoT exit, yet T-Mobile and Verizon continue to support nationwide footprints, resulting in a mixed competitive landscape. Government infrastructure grants for water and gas meter upgrades partially offset consolidation risk. Emerging RedCap trials provide a future-proofing narrative that could stabilise carrier commitments over the medium term.

Europe maintains steady growth anchored in regulatory mandates for energy efficiency and environmental monitoring. Operators integrate NB-IoT into cross-border roaming arrangements despite fragmented spectrum, while guard-band deployments maximise scarce sub-1 GHz assets. Public-private projects in conservation, such as Vodafone’s endangered species tracking, demonstrate social-impact use cases that sustain adoption.

Competitive Landscape

Vendor incompatibility between Ericsson and Huawei created multiple software variants that complicate multinational roll-outs and elevate integration costs. This technical schism gives LoRa and LTE-M an opening where simplicity and roaming continuity rank high. Chinese infrastructure markets remain largely domestic, allowing Huawei, ZTE, and China Mobile to dictate specifications, whereas Western carriers diversify suppliers to hedge against lock-in.

Strategy now emphasises hybrid connectivity. Quectel-Skylo and OQ Technology-Transatel collaborations provide seamless NTN fallback, ensuring service continuity in deserts, oceans, and polar routes. Module vendors launch pin-compatible RedCap designs that preserve current NB-IoT certifications while offering future upgrade paths. Operators test consumption-based 5G-core services that lower entry costs for smaller utilities and municipalities, democratising the NB-IoT market to second-tier service providers.

Price competition intensifies at the silicon layer. MediaTek’s World-Mode modem undercuts incumbents, while Qualcomm’s industrial-grade IQ series targets extreme-environment use cases. Chipset roadmaps now include AI inference engines that enable on-device anomaly detection, reducing uplink traffic and offsetting throughput constraints. The combined effect is a moderate-concentration market where innovation cycles and multi-mode flexibility outweigh raw scale.

Narrowband IoT Industry Leaders

Huawei Technologies Co., Ltd

Ericsson Corporation

Qualcomm Technologies

AT&T Inc

Verizon Communications Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Qualcomm introduced the X85 5G Modem-RF with an integrated AI processor for efficient IoT connectivity.

- February 2025: MediaTek unveiled the M90 5G-Advanced modem featuring satellite support for IoT devices.

- December 2024: Quectel and Skylo revealed the first NTN module for satellite-augmented NB-IoT.

- November 2024: AT&T confirmed NB-IoT network sunset by Q1 2025 and migration to LTE-M.

Global Narrowband IoT Market Report Scope

NarrowBand-Internet-of-Things (NB-IoT) is a standards-based low power wide area (LPWA) technology that has been created to enable a variety of new IoT devices and applications. NB-IoT dramatically improves user device power consumption, system capacity, and spectrum efficiency, particularly in deep coverage. For a wide range of use scenarios, battery life of more than ten years can be supported.

The Narrowband IoT market is segmented by component (network, module), by deployment (standalone, in-band, guard-band), by device type (wearables, tracker, smart meter, smart lighting, alarm & detector, and others), by application (smart cities, transportation & logistics, energy & utilities, retail, agriculture and others), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, Rest of Europe], Asia Pacific [India, China, Japan, Rest of Asia Pacific], Latin America [Brazil, Argentina, Rest of Latin America], Middle East and Africa [United Arab Emirates, Saudi Arabia, Rest of Middle East and Africa]). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| Network | Core Network |

| Radio Access Network (RAN) | |

| Module | Baseband Chipsets |

| Integrated SoCs |

| Stand-alone |

| In-band |

| Guard-band |

| Wearables | Healthcare Wearables |

| Consumer Wearables | |

| Trackers | Logistics Trackers |

| Smart Meters | Electricity Meters |

| Gas and Water Meters | |

| Smart Lighting | |

| Alarms and Detectors | Smoke Detectors |

| Intrusion Alarms |

| Smart Cities |

| Transportation and Logistics |

| Energy and Utilities |

| Retail and Vending |

| Agriculture and Livestock |

| Industrial Automation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Network | Core Network | |

| Radio Access Network (RAN) | |||

| Module | Baseband Chipsets | ||

| Integrated SoCs | |||

| By Deployment | Stand-alone | ||

| In-band | |||

| Guard-band | |||

| By Device Type | Wearables | Healthcare Wearables | |

| Consumer Wearables | |||

| Trackers | Logistics Trackers | ||

| Smart Meters | Electricity Meters | ||

| Gas and Water Meters | |||

| Smart Lighting | |||

| Alarms and Detectors | Smoke Detectors | ||

| Intrusion Alarms | |||

| By Application | Smart Cities | ||

| Transportation and Logistics | |||

| Energy and Utilities | |||

| Retail and Vending | |||

| Agriculture and Livestock | |||

| Industrial Automation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the NB-IoT market?

The NB-IoT market size reached USD 13.62 billion in 2026 and is projected to hit USD 51.82 billion by 2031.

Which region leads NB-IoT adoption?

Asia Pacific holds 51.75% revenue share thanks to large-scale deployments in China and supportive industrial policies.

Why are module prices falling below USD 3.00 important?

Sub-USD 3.00 modules reduce total device cost, making NB-IoT viable for high-volume applications in agriculture, tracking, and smart cities.

How will 5G NR-RedCap affect NB-IoT investments?

RedCap provides an upgrade path that reuses NB-IoT spectrum and infrastructure, assuring buyers of long-term compatibility.

What deployment mode is growing fastest?

Guard-band deployments are forecast to expand at 34.10% CAGR over 2026-2031 as operators repurpose unused LTE buffer frequencies.

How does satellite augmentation enhance NB-IoT coverage?

Satellite-enabled NB-IoT modules fill connectivity gaps in maritime, mining, and remote farming zones where terrestrial networks are absent.

Page last updated on: