Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 78.15 Billion |

| Market Size (2031) | USD 120.96 Billion |

| Growth Rate (2026 - 2031) | 9.12% CAGR |

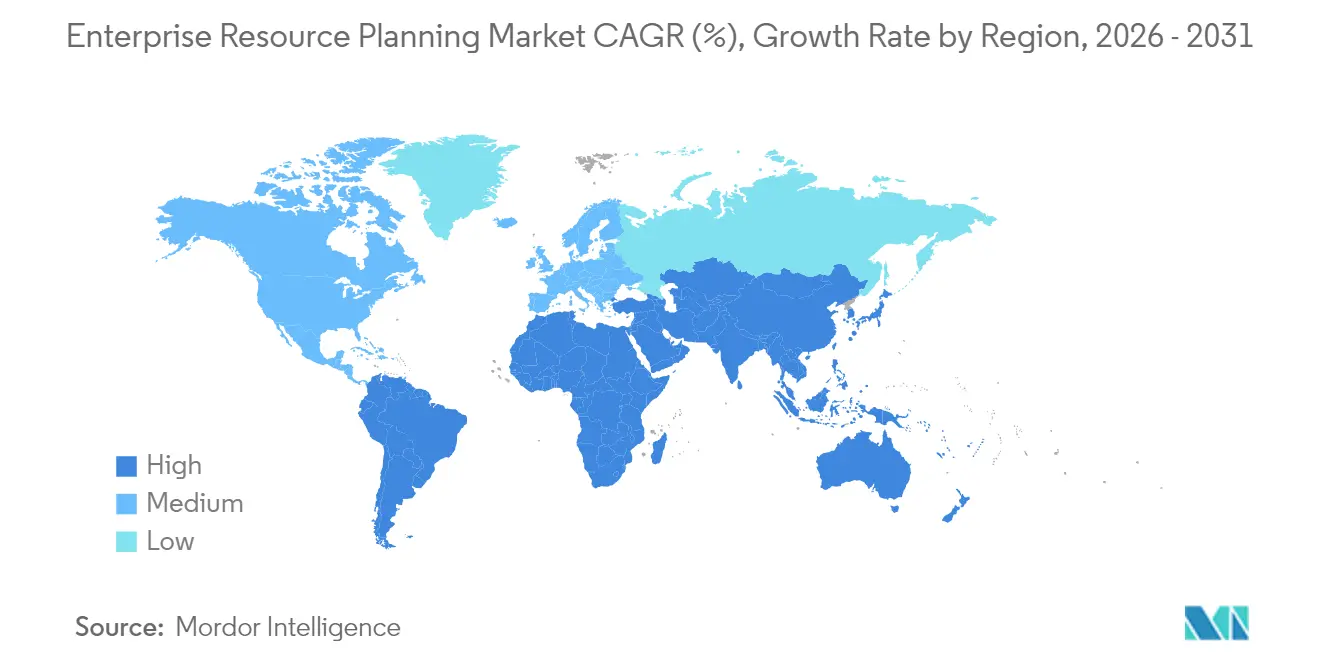

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Resource Planning Market Analysis by Mordor Intelligence

The Enterprise Resource Planning Market size was valued at USD 71.62 billion in 2025 and is estimated to grow from USD 78.15 billion in 2026 to reach USD 120.96 billion by 2031, at a CAGR of 9.12% during the forecast period (2026-2031). Strong demand for integrated process automation, faster cloud migration, and AI-enabled analytics is propelling expansion across manufacturing, services, and public-sector organizations. Vendors have shifted road maps toward cloud-native suites that lower infrastructure costs, while enterprises accelerate modernization to improve real-time visibility and regulatory compliance. Spurred by mandatory e-invoicing laws and ESG accounting requirements, companies are prioritizing embedded compliance capabilities that reduce audit risk and support cross-border operations. Competitive dynamics are shaped by a shortfall of skilled consultants, prompting providers to invest in low-code configuration tools that shorten deployment timelines and lower total cost of ownership.

Key Report Takeaways

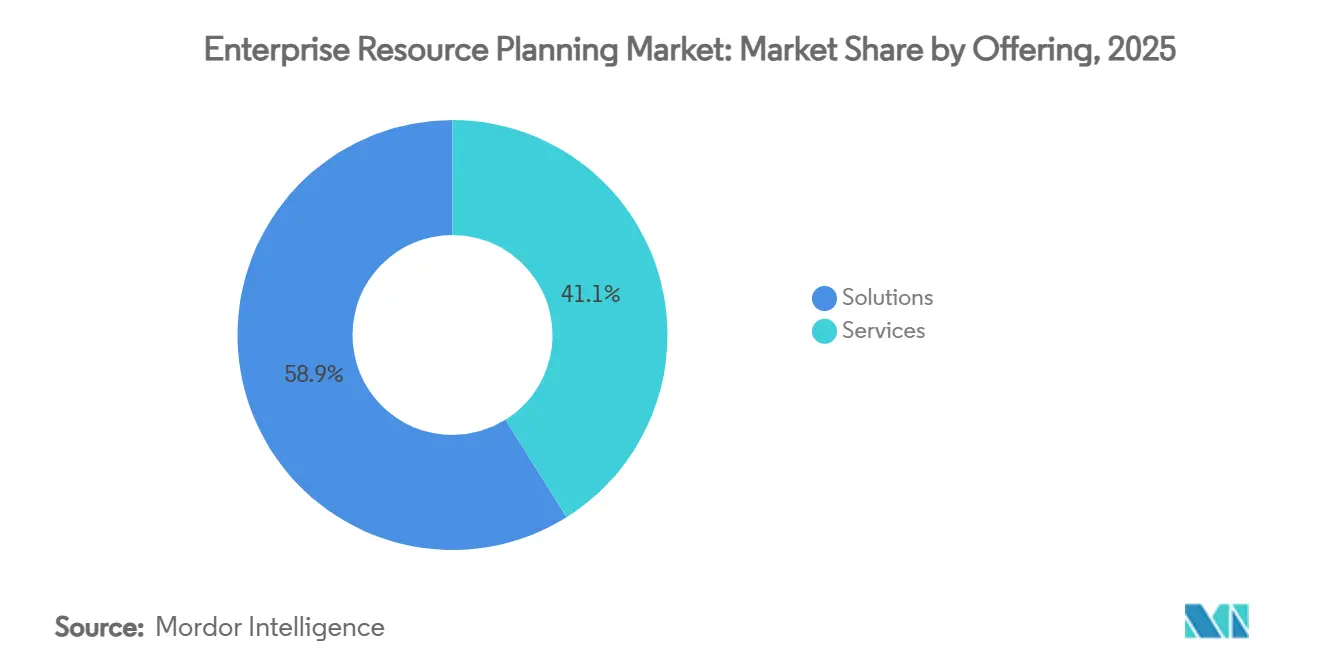

- By offering solutions, it captured 58.35% of the enterprise resource planning market share in 2025, while services are projected to expand at 13.47% CAGR through 2031.

- By deployment, cloud models held a 55.11% share of the ERP market size in 2025, while hybrid models are projected to expand at a 15.48% CAGR through 2031.

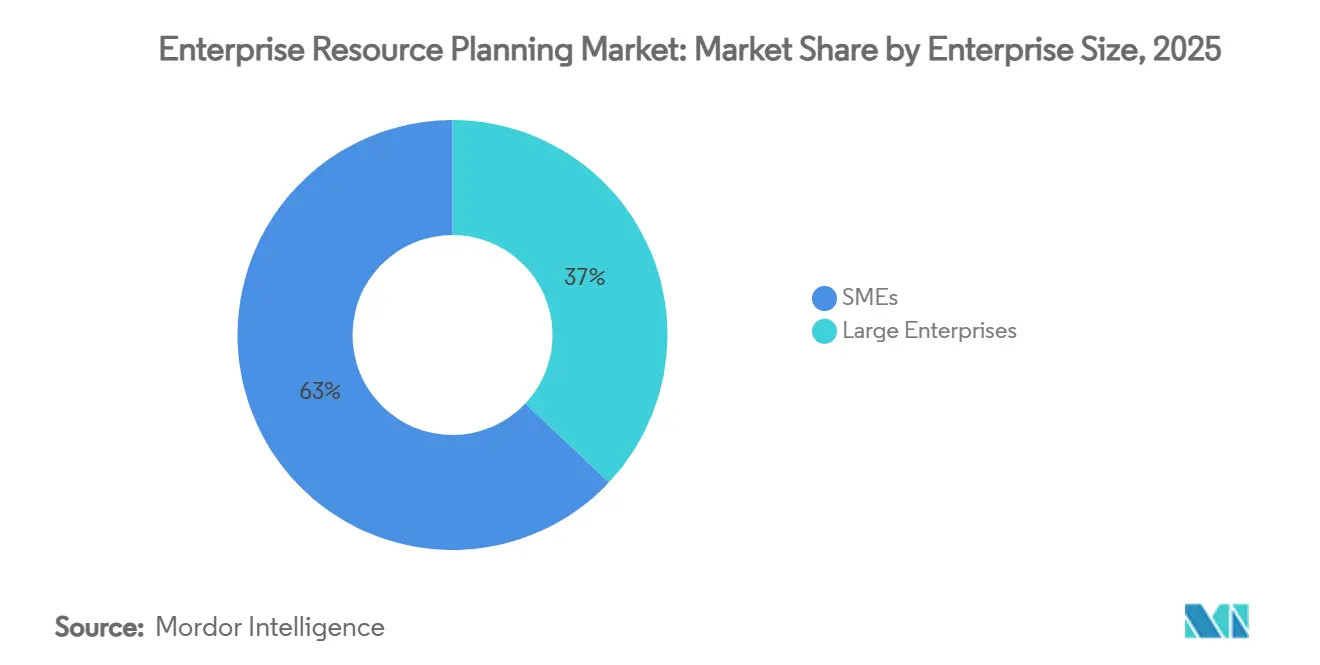

- By enterprise size, large companies commanded a 37.76% share of the market size in 2025, while SMEs are projected to expand at a 14.29% CAGR through 2031.

- By end-user industry, manufacturing accounted for 24.53% of the market share in 2025, while IT and telecom are projected to expand at 15.76% CAGR through 2031.

- By geography, North America led with a 34.02% revenue share in 2025, while the Asia-Pacific region is set to climb at a 11.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Migration Momentum | +2.8% | North America, Europe | Medium term (2-4 years) |

| AI-Driven Analytics Embedded in ERP | +2.1% | Global developed markets | Long term (≥ 4 years) |

| SME SaaS Adoption Surge | +1.9% | Asia-Pacific, Latin America, Middle East and Africa | Short term (≤ 2 years) |

| Mandatory E-Invoicing Mandates | +1.4% | Europe, Latin America, Asia-Pacific | Medium term (2-4 years) |

| ESG Accounting Add-Ons for Scope-3 Tracking | +0.8% | North America, European Union, Asia-Pacific | Long term (≥ 4 years) |

| Generative AI User Experiences | +0.6% | Global tier-one markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Migration Momentum

Enterprises are accelerating the shift from on-premise suites to cloud deployments in the enterprise resource planning market to unlock elastic scalability, subscription pricing, and continuous functional updates. Mid-market firms embrace operating-expense models that free cash for growth, while large companies leverage vendor programs such as RISE with SAP to consolidate fragmented landscapes. In addition, hyperscale hosting options enable customers to localize sensitive ledgers for data sovereignty compliance without sacrificing unified reporting. Continuous release cycles keep tax codes and security patches up to date, reducing audit exposure and disruption during upgrades. As a result, cloud conversions help the market add new subscribers faster than traditional license refreshes.

AI-Driven Analytics Embedded in ERP

Artificial intelligence is recasting the enterprise resource planning market as a real-time decision engine rather than a static record repository. Acumatica’s AI-first strategy, unveiled at its 2025 summit, embeds machine-learning models that predict late payments, optimize production runs, and recommend purchase quantities. Similar natural-language query features in Oracle NetSuite let staff build multi-dimensional reports without SQL expertise. Internal vendor benchmarks show that AI-assisted forecasting can reduce safety-stock buffers by up to 30%, freeing up cash for investment. Low-code AI builders are also democratizing algorithm customization, enabling finance and operations teams to prototype use cases without data science support. These advances expand the market beyond compliance automation, enabling revenue growth.

SME SaaS Adoption Surge

Subscription pricing continues to democratize access to the enterprise resource planning market among small and medium enterprises. Implementation packs now include pre-configured industry templates that shrink project timelines from months to weeks. Asia-Pacific governments offer digitalization credits that offset first-year fees, while mobile-first workforces favor browser-based interfaces that operate on low-cost devices. Providers such as Acumatica ship multilingual user guides and localized tax packs to remove language and compliance barriers. As SMEs gain real-time insights into receivables, inventory, and payroll, satisfaction levels accelerate word-of-mouth referrals that compound adoption rates. The resulting volume growth balances unit pricing pressure and sustains overall revenue expansion for vendors.

Mandatory E-Invoicing Mandates

Tax authorities in Germany, Croatia, Malaysia, and a dozen additional markets began enforcing real-time e-invoice submissions. ERP vendors responded with certified connectors that integrate invoice validation and timestamping directly into payables workflows. Built-in mappings eliminate manual re-keying, reduce exception-handling labor, and lower the risk of fines. Organizations unable to comply face cash-flow interruptions, prompting accelerated investments in modern suites. Mandatory regulations, therefore, act as a structural tailwind for the enterprise resource planning market, especially among export-oriented firms operating across multiple jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implementation and Switching Costs | -1.8% | Global emerging markets | Short term (≤ 2 years) |

| Data Integration and Legacy Complexity | -1.2% | North America, Europe | Medium term (2-4 years) |

| Rising Data-Sovereignty Laws | -0.9% | Global | Long term (≥ 4 years) |

| Shortage of Micro-Vertical ERP Talent | -0.7% | Global developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation and Switching Costs

Upfront license fees, process redesign workshops, and staff training can push ERP projects for a mid-size organization above USD 1 million. Panorama Consulting surveys reveal that total outlays often double when data migration and change-management services are factored in, extending payback periods beyond 3 years. Budget constraints in emerging regions amplify sensitivity to large capital commitments. Although SaaS contracts distribute expense over time, hidden integration work and temporary parallel-run costs remain significant. Consequently, some firms postpone modernization until regulatory deadlines or customer mandates force action, which caps short-term market growth.

Shortage of Micro-Vertical ERP Talent

Global demand for certified consultants continues to exceed supply, especially in complex regulated industries. Industry analysts estimate a 30,000-40,000-person shortfall for SAP alone, which will inflate daily rates and extend implementation timelines. Scarcity is most acute for aerospace, healthcare, and utility templates that embed domain-specific compliance logic. Vendors offer automated configuration wizards and reference-model libraries that shorten discovery stages, but these tools cannot fully replace industry expertise. The resulting talent gap restrains deployment velocity and slows revenue conversion for providers in the ERP market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Solutions Dominance

Solutions maintained a commanding 58.91% share of the enterprise resource planning market in 2025, reflecting the universal need for integrated financial, supply chain, and human capital modules. Yet service revenue is rising at a 13.89% CAGR as customers seek industry-specific consulting, data cleansing, and user adoption coaching. The market for professional services is on track to nearly double by 2031, surpassing traditional customization budgets. Vendors such as Acumatica introduced professional-services editions bundling project accounting, resource scheduling, and revenue recognition to streamline deployment for law, design, and consulting agencies. Growing demand for continuous improvement and AI tuning offsets narrowing software gross margins and secures annuity streams for providers.

Implementation roadmaps now prioritize business-process redesign over feature parity, elevating the strategic role of consulting partners. Low-code workflow builders enable rapid prototyping of industry-specific variants, reducing coding volume while increasing advisory hours. Customers also purchase subscription-based success plans that include quarterly health checks, regulatory patching, and AI model retraining. These shifts reposition services from ancillary to core revenue, reinforcing the hybrid product-plus-consulting value proposition that defines the contemporary market.

By Deployment: Hybrid Models Challenge Cloud Supremacy

Cloud architectures accounted for 55.73% of the market in 2025, securing the majority of new installations thanks to predictable operating expenses and automatic upgrades. However, hybrid configurations that blend private, public, and on-premises assets are advancing at a 16.12% CAGR. Multinational manufacturers frequently retain financial ledgers in local data centers for sovereignty compliance while hosting analytics and collaboration tools in regional clouds. As a result, the enterprise resource planning market size for hybrid solutions is projected to outpace that of pure cloud segments.

SAP’s RISE program exemplifies this trend by enabling customers to deploy S/4HANA on hyperscalers while keeping manufacturing execution systems on-site. Pharmaceutical firms value the ability to preserve plant-floor latency budgets while sharing centralized quality data for global batch release. Hybrid blueprints also support phased migrations, allowing legacy add-ons to retire gradually without the risk of a big bang. Consequently, the market's deployment landscape is evolving toward coexistence models that balance control, performance, and elasticity.

By Enterprise Size: SMEs Drive Market Democratization

Large enterprises held 37.16% share of the market size in 2025, leveraging comprehensive suites to manage multi-entity consolidation, advanced governance, and global tax. Even so, SMEs represent the most dynamic buyer group with a 14.91% CAGR through 2031. Rapid-start bundles, priced per user per month, enable startups to automate quoting, invoicing, and stock control without capital expenditure. The market share gap between large enterprises and SMEs is therefore narrowing, reflecting democratized access to sophisticated functionality.

Low-code customization utilities empower nontechnical staff to tweak forms, build dashboards, and integrate e-commerce storefronts, thereby reducing reliance on external agencies. Vendors profit from predictable recurring revenue, while customers gain earlier visibility into working-capital cycles. Over time, SMEs scale seat counts and module breadth, elevating customer lifetime value. The self-service ethos also encourages experimentation with AI-powered forecasting, deepening the market's footprint in the mid-market.

By End-User Industry: Manufacturing Leadership Faces IT Sector Challenge

Manufacturing accounted for the largest 24.89% share of the enterprise resource planning market in 2025, as intricate bill-of-materials tracking and production scheduling remain mission-critical. Industry 4.0 programs now feed Internet-of-Things sensor data into maintenance and quality-control workflows, which solidifies ERP’s role as the data backbone. Nevertheless, IT and telecom revenue is expanding at a 16.34% CAGR, fueled by 5G monetization, subscription billing, and stringent data-privacy requirements.

Telecom operators embed usage-based charging engines and cross-border tax compliance directly into unified ERP cores to handle high transaction volumes at sub-second latency. Meanwhile, contract electronics manufacturers prioritize real-time traceability and automated compliance reporting, retaining manufacturing’s dominant but slower-growing position. The cross-sector dynamic heightens competition for specialized templates, nudging vendors to accelerate vertical roadmap releases and widening the feature gap between generic and industry-specific editions in the ERP market.

Geography Analysis

North America accounted for 34.02% of the market revenue in 2025, driven by several key factors, including high cloud adoption rates, robust partner networks, and the presence of a significant number of Fortune 500 organizations. The region benefits from its early adoption of SaaS solutions, supported by a mature venture-capital ecosystem that continues to fuel demand for modern ERP suites. These suites are increasingly integrating advanced technologies like artificial intelligence (AI) and sophisticated analytics to meet evolving business needs. Additionally, digital-first government procurement policies are playing a crucial role in encouraging public-sector agencies to adopt ERP systems, further solidifying the region's leadership in the market.

Europe maintains steady market growth, with widespread adoption across key sectors such as manufacturing and public administration. However, the introduction of mandatory e-invoicing laws is triggering a new replacement cycle for ERP systems. To address these regulatory changes, vendors are offering solutions equipped with localized tax engines, GDPR-compliant data-residency features, and pre-configured charts of accounts tailored to regional requirements. These capabilities are enabling businesses to transition from outdated on-premise platforms to modern subscription-based models. As a result, the region is experiencing stable mid-single-digit growth, driven by the need for compliance and operational efficiency.

Asia-Pacific is emerging as the fastest-growing region in the market, with a CAGR of 11.96%. This growth is fueled by rapid industrial expansion in countries such as China, India, and those in Southeast Asia. Government initiatives, including grants and subsidies, combined with the increasing affordability of mobile broadband and the growing availability of cloud infrastructure, are significantly boosting cloud ERP deployments. These deployments are particularly prominent among mid-tier manufacturers and service-oriented firms. Furthermore, hyperscale cloud providers are investing in the development of regional data centers, which not only comply with data-sovereignty regulations but also enhance user response times. These advancements are ensuring that the enterprise resource planning market in Asia-Pacific continues to experience robust double-digit growth, driven by the region's dynamic economic landscape and technological advancements.

Competitive Landscape

The enterprise resource planning market is experiencing moderate consolidation, with major players such as SAP, Oracle, and Microsoft maintaining dominant global market share. These companies leverage broad functional coverage and extensive partner ecosystems to sustain their leadership. SAP, for instance, surpassed 24,000 RISE cloud customers in 2025, demonstrating its ability to meet evolving enterprise needs. Oracle Fusion Cloud, on the other hand, introduced predictive planning and ESG (Environmental, Social, and Governance) accounting modules, which enhance its vertical specialization and appeal to organizations prioritizing sustainability and advanced analytics.

Challenger vendors, including IFS and Acumatica, are capitalizing on their focused sector expertise to carve out significant market niches. IFS achieved over EUR 1 billion (approximately USD 1.12 billion) in recurring revenue in 2024 by emphasizing industrial asset management solutions integrated with AI capabilities that predict machine failures, thereby reducing downtime and operational costs. Acumatica, meanwhile, targets mid-market manufacturers and distributors with its unique unlimited-user licensing model and open APIs, enabling seamless integration. The company has consistently registered compound annual revenue growth of more than 25% since 2021, reflecting strong market traction.

Specialist providers are addressing specific micro-vertical gaps within the market. For example, Unit4 focuses on professional-services organizations that require complex project accounting solutions, while Plex extends its native manufacturing execution capabilities to cater to food and beverage processors. This level of fragmentation below the top-tier players fosters intense competitive pressure, driving continuous innovation across key areas such as financial management, supply chain optimization, and workforce management. As a result, the ERP market remains dynamic and responsive to the diverse needs of its users.

Enterprise Resource Planning Industry Leaders

Microsoft Corporation

SAP SE

Microsoft Corporation

Workday, Inc.

Infor Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Acumatica unveiled its AI-first product strategy at Summit 2025, integrating machine learning across manufacturing, distribution, and finance modules.

- March 2025: iFabric Corp invested CAD 500,000 (USD 370,000) in BlueCherry ERP to streamline operations and support growth goals.

- February 2025: IFS partnered with Saudi Business Machines to deliver integrated IT solutions in Saudi Arabia, broadening Middle East reach.

- January 2025: IFS reported annual recurring revenue topping EUR 1 billion (USD 1.12 billion) on 32% growth, adding more than 350 new customers.

- January 2025: Proteus Technologies launched Vision AI inside Vision ERP, adding predictive analytics and automated workflows for manufacturing and retail clients.

Global Enterprise Resource Planning Market Report Scope

The Enterprise Resource Planning (ERP) Market refers to the global market for integrated software solutions and related services that enable organizations to manage and automate core business processes across functions such as human resources, supply chain, finance, marketing, and other operational areas within a unified system. These solutions are deployed through on-premise and hybrid models, catering to both small and medium enterprises and large enterprises across diverse industry verticals

The Enterprise Resource Planning (ERP) Market is Segmented by Offering (Solutions and Services), Function (HR, Supply Chain, Finance, Marketing, and Other Functions), Deployment (On-Premise and Hybrid), Organization Size (Small and Medium Enterprises and Large Enterprises), Industry Verticals (BFSI, IT and Telecom, Government, Retail and E-Commerce, Manufacturing, Oil, Gas, and Energy, and Other Industry Verticals), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Offering

| Solutions |

| Services |

By Deployment

| On-premise |

| Cloud |

| Hybrid |

By Function

| Human Resources |

| Supply Chain |

| Finance |

| Marketing |

| Other Functions |

By Enterprise Size

| Large Enterprises |

| Small and Medium-Sized Enterprises |

By End-user Industry

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| IT and Telecom |

| Government and Public Sector |

| Energy and Utilities |

| Healthcare |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Offering | Solutions | ||

| Services | |||

| By Deployment | On-premise | ||

| Cloud | |||

| Hybrid | |||

| By Function | Human Resources | ||

| Supply Chain | |||

| Finance | |||

| Marketing | |||

| Other Functions | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium-Sized Enterprises | |||

| By End-user Industry | Manufacturing | ||

| Retail and E-commerce | |||

| BFSI | |||

| IT and Telecom | |||

| Government and Public Sector | |||

| Energy and Utilities | |||

| Healthcare | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast are cloud deployments expanding inside enterprise suites?

Cloud models within the enterprise resource planning market are growing at a 16.12% CAGR through 2031 as firms migrate to subscription pricing and automated updates.

Which area currently delivers the most revenue?

Core software solutions supplied 58.91% of 2025 revenue, reflecting their role as the foundation for integrated processes.

Why are SMEs accelerating adoption?

Low-cost SaaS subscriptions and ready-made industry templates cut implementation cycles to weeks, eliminating historical capital hurdles.

What role does AI play in modern suites?

Embedded algorithms automate routine tasks, provide predictive insights, and enable natural-language queries, thereby improving accuracy and reducing operating costs.

Which geography shows the fastest growth through 2031?

Asia-Pacific is advancing at a 11.96% CAGR, propelled by industrial expansion, government digitalization grants, and widespread mobile connectivity.

How concentrated is the vendor landscape?

The top five providers control a little more than 60% of revenue, indicating moderate concentration and allowing room for niche and regional competitors.

Page last updated on: