Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.12 Billion |

| Market Size (2031) | USD 24.61 Billion |

| Growth Rate (2026 - 2031) | 10.23% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

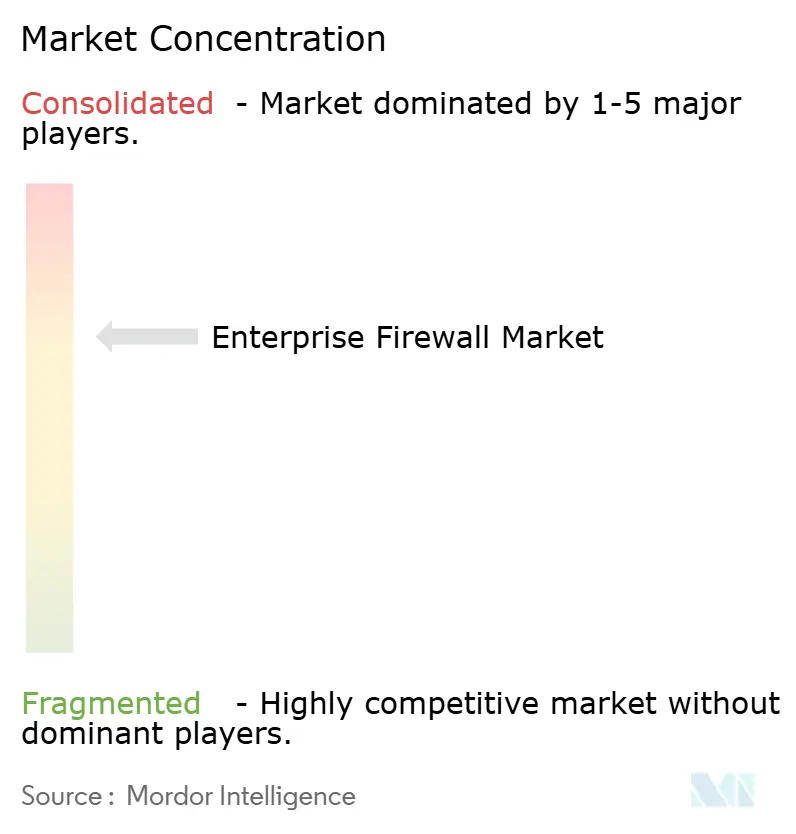

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Enterprise Firewall Market Analysis by Mordor Intelligence

The Enterprise Firewall Market size in 2026 is estimated at USD 15.12 billion, growing from 2025 value of USD 13.72 billion with 2031 projections showing USD 24.61 billion, growing at 10.23% CAGR over 2026-2031. Hybrid work models add urgency, pushing buyers toward Firewall-as-a-Service to protect remote users while reducing hardware overhead. [1]Microsoft, “What Is Azure Firewall?” Microsoft.com Vendors respond with unified platforms that blend network and security functions, while compliance frameworks such as PCI DSS and DORA increase demand for continuous policy enforcement and audit reporting. Semiconductor cost inflation and skills shortages constrain short-term hardware rollouts, yet subscription revenues keep margins resilient as platformization gains pace.

Key Report Takeaways

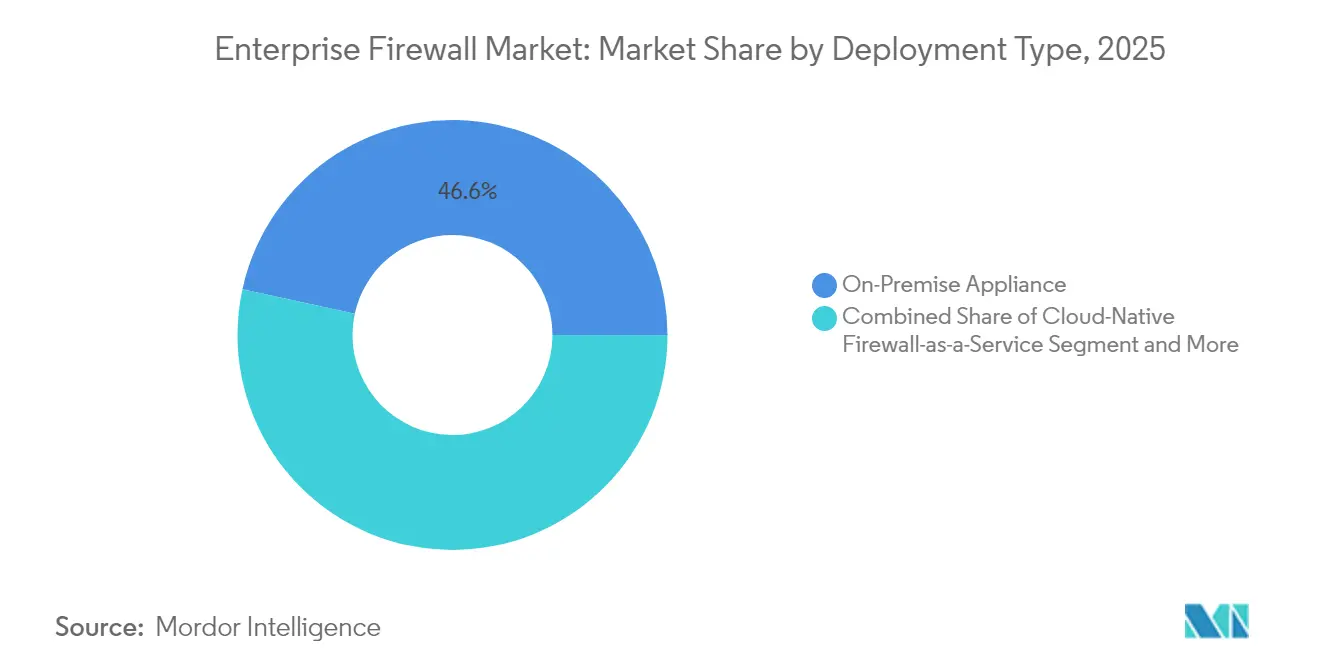

- By deployment type, on-premise appliances held 46.58% of the enterprise firewall market share in 2025, while cloud-native Firewall-as-a-Service is forecast to grow at a 13.68% CAGR through 2031.

- By component, hardware appliances contributed 47.65% revenue share in 2025; managed and professional services are projected to expand at a 13.52% CAGR to 2031.

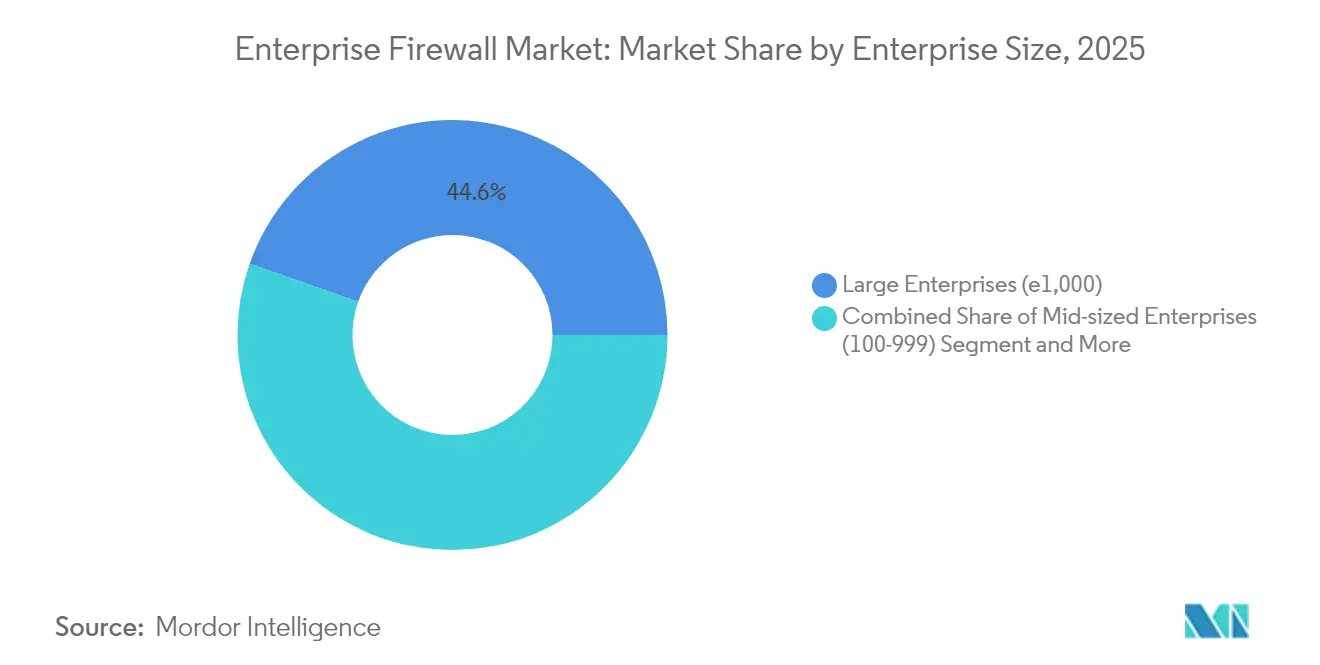

- By enterprise size, large organizations accounted for 44.62% of 2025 revenues, whereas small and micro enterprises are set to grow at 13.84% CAGR, aided by cloud-delivered entry-level offerings.

- By industry, BFSI led with a 27.12% share in 2025, while retail and e-commerce are expected to register the fastest 12.76% CAGR, owing to rising digital payments and compliance needs.

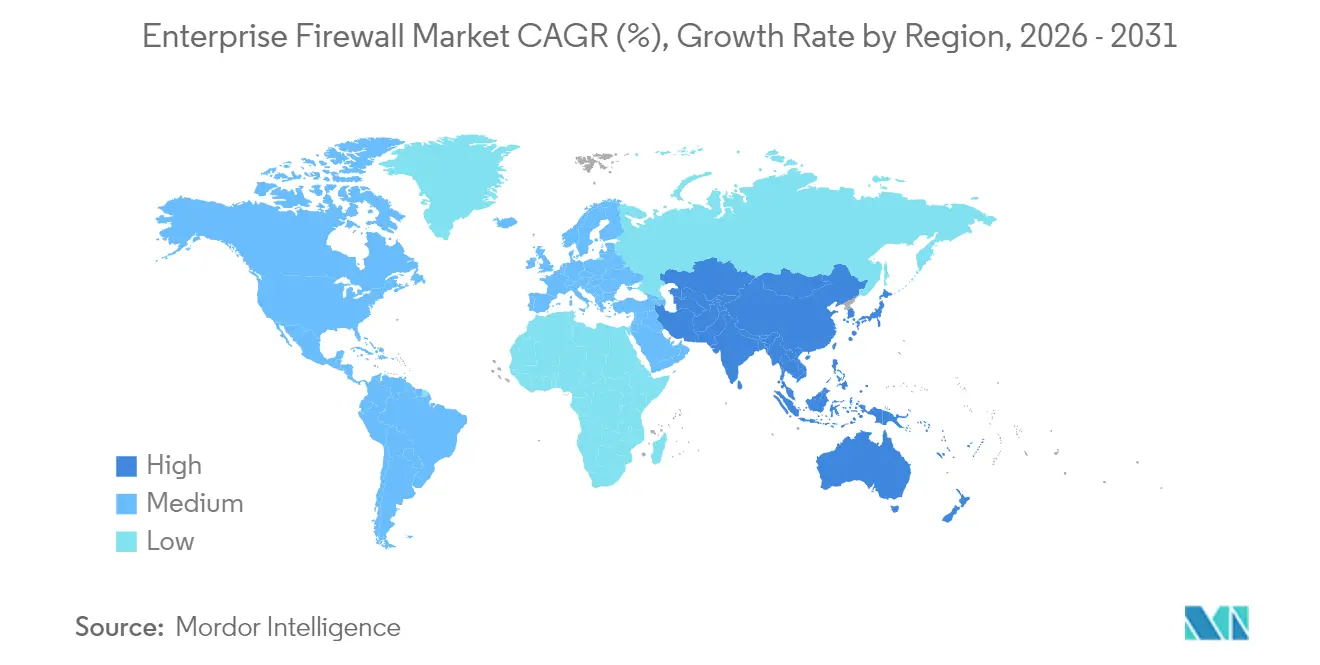

- By geography, North America commanded 35.02% of 2025 revenues; Asia-Pacific is positioned for a 12.38% CAGR on the back of digital sovereignty programs and cloud investment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Enterprise Firewall Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating sophistication of multi-vector attacks | +2.8% | North America, Europe | Short term (≤ 2 years) |

| Rapid adoption of hybrid and remote work | +2.1% | North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Regulatory mandates for zero-trust segmentation | +1.9% | North America, Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Cloud workload proliferation | +1.7% | Global, highest in Asia-Pacific | Medium term (2-4 years) |

| AI-driven polymorphic malware | +1.4% | Technology hubs worldwide | Short term (≤ 2 years) |

| Sovereign traffic-inspection clauses | +1.2% | Asia-Pacific, Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Sophistication of Multi-Vector Attacks

Attackers now weaponize legitimate software and AI to breach endpoints, cloud workloads, and lateral pathways in one campaign, leaving static rule sets ineffective. Palo Alto Networks observed that 86% of incidents in 2024 caused direct business disruption, prompting enterprises to deploy next-generation firewalls that correlate real-time intelligence across distributed sensors. A global telecom uncovered more than 200 privileged sessions sitting outside domain controllers, underscoring east-west blind spots. [2]Reveald, “Global Industrial Company Case Study,” Reveald.com Vendors embed machine-learning inspection to flag behavioral anomalies, enabling enterprises to quarantine suspicious traffic within milliseconds and cut dwell time.

Rapid Adoption of Hybrid and Remote Work Architectures

Decentralized workforces rely on home networks and unmanaged devices, expanding the threat surface far beyond data-center perimeters. Organizations shift toward secure access service edge models that fuse identity, device health, and firewall controls inside a single cloud point of enforcement. Microsoft notes that encrypted VPN tunnels often evade traditional inspection, so many firms migrate to Firewall-as-a-Service for uniform policy wherever users connect. Partnerships such as Bell Canada with Palo Alto Networks highlight how carriers wrap AI-powered firewalls around managed connectivity for remote teams.

Regulatory Mandates for Zero-Trust and Segmentation

Updated frameworks such as the U.S. Department of Defense Zero Trust Overlays require continuous verification and micro-segmentation, pushing enterprises to deploy firewalls that adjust policies dynamically on risk signals. Compliance programs, including DORA and HIPAA, now expect granular audit trails and automated policy evidence, making manual rule maintenance unsustainable. An American manufacturer adopted Fortinet Security Fabric to meet new certification targets and cut ongoing configuration workload by 30%.

Cloud Workload Proliferation Requiring East-West Security

Containerized and serverless apps spin up thousands of ephemeral flows that bypass perimeter choke points. Google Cloud’s hierarchical firewall policies illustrate how micro-segmentation must scale programmatically rather than appliance by appliance. Industrial adopters such as SCG Chemicals use distributed firewalls to protect operational technology traffic while aligning with IEC-62443 standards. Vendors answer with API-driven policy engines and context-aware deep-packet inspection that follow every workload regardless of location.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget constraints among SMBs | -1.8% | Emerging markets worldwide | Medium term (2-4 years) |

| Skills shortage for complex policy management | -1.4% | North America, Europe | Long term (≥ 4 years) |

| IPv6 transition delaying hardware refresh | -0.9% | Global | Medium term (2-4 years) |

| Data-residency shift to regional SOCs | -0.7% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget Constraints Among SMBs

Many small firms lack full-time security personnel and face pressure to allocate limited capital to core operations, slowing the adoption of advanced firewalls. Cyber-insurance carriers now offer premium reductions to policyholders that deploy managed security services, but up-front subscription costs still deter buyers in price-sensitive regions. Vendors respond with entry-level cloud firewalls that include automated policy templates and usage-based billing, lowering procurement hurdles.

Skills Shortage to Manage Complex Policies

AI-augmented firewalls promise automation, yet they require teams versed in threat-intelligence feeds, segmentation design, and machine-learning tuning. Rockwell Automation highlights that industrial operators need staff who understand both IT and OT protocols, a rare combination commanding premium wages. [3]Rockwell Automation, “Best Practices for OT Firewall Management,” Rockwellautomation.com Organizations increasingly outsource 24/7 monitoring to managed detection and response partners, fueling the services CAGR while limiting do-it-yourself deployments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud-Native Gains Momentum

On-premise appliances retained 46.58% of the 2025 enterprise firewall market share on the back of predictable throughput and regulatory comfort with air-gapped designs. In revenue terms, the segment accounted for the largest slice of the enterprise firewall market size, even as refresh cycles extend because of protocol migration uncertainty. Enterprises running latency-sensitive workloads in data centers continue to favor purpose-built hardware that embeds accelerators for high-speed TLS inspection.

Cloud-native Firewall-as-a-Service, advancing at a 13.68% CAGR through 2031, brings centralized policy, elastic scale, and pay-as-you-grow economics that resonate with firms embracing multicloud and remote work strategies. The model also simplifies compliance evidence because providers surface continuous audit logs via portals. Virtual appliances sit between both worlds, letting enterprises replicate rule sets across private clouds and edge locations without shipping hardware, which eases branch rollouts during zero-trust transitions. The blended approach underlines how buyers now map firewall form factor to workload locality rather than defaulting to a single architecture.

By Component: Services Surge as Complexity Increases

Hardware appliances captured 47.65% of 2025 revenues, reflecting persistent demand for deterministic performance, hardware encryption offload, and tamper-resistant designs that satisfy audit teams. This slice of the enterprise firewall market size is expected to grow steadily, yet its proportion declines as buyers shift budget toward lifecycle services that unlock the appliance’s full potential.

Managed and professional services are forecast to expand at 13.52% CAGR because continuous tuning, threat-feed integration, and compliance reporting outstrip many in-house teams’ bandwidth. Service providers bundle playbooks for DORA, HIPAA, and sector-specific standards, helping clients cut mean-time-to-respond and satisfy regulators. Vendors increasingly embed AI-driven copilots into management consoles, yet human specialists remain essential for contextualising anomalies and aligning policies with evolving business objectives.

By Enterprise Size: SMBs Embrace Accessible Solutions

Large organizations held 44.62% of 2025 spending, sustaining the biggest single slice of the enterprise firewall market size thanks to sizeable threat-hunting teams and capital budgets for global rollouts. They drive early adoption of AI inspection engines and sandbox detonation features, often piloting capabilities that cascade downstream once proven.

Small and micro enterprises are projected to post a 13.84% CAGR through 2031 as Firewall-as-a-Service reduces up-front costs and automates day-to-day administration. Microsoft’s Azure Firewall Basic and Fortinet’s SMB-focused bundles pre-load recommended rules, freeing owners from complex configuration. Midmarket firms act as the bridge, often co-sourcing policy management with MSSPs while retaining visibility through shared portals.

By End-user Industry: BFSI Leads, Retail Accelerates

Banking, financial services, and insurance generated 27.12% of 2025 revenues, making it the largest vertical slice of the enterprise firewall market. Strict data-protection mandates, real-time fraud risks, and 24/7 uptime expectations push banks toward clustered active-active firewalls that embed behavioral analytics. A major North American institution projects USD 100 million savings over five years after replacing legacy rule sets with Fortinet’s automated fabric that slashes change-window labor.

Retail and E-commerce are forecast to expand at a 12.76% CAGR to 2031, supported by surging online transaction volumes and point-of-sale digitization that expose merchants to credential-stuffing and card-skimming attacks. Omnichannel strategies demand consistent policy across stores, mobile apps, and fulfillment centers, driving adoption of cloud firewalls that integrate web-application protection and bot mitigation. Manufacturing, healthcare, and public sector segments follow close behind as Industry 4.0 and electronic health record initiatives widen attack surfaces.

Geography Analysis

North America led with 35.02% of 2025 revenues, anchored by strict federal rules and high breach remediation costs that spur proactive purchasing. Enterprises there standardize on zero-trust architectures and increasingly choose consolidated platforms to cut operational fragments. Bell Canada’s alliance with Palo Alto Networks shows how telcos bundle AI-driven firewalls with connectivity to serve a dispersed workforce.

Asia-Pacific is set for a 12.38% CAGR through 2031, the fastest across regions. Governments in India, Indonesia, and Japan press for local inspection of citizen data, encouraging procurement of firewalls deployable in country-specific clouds. Domestic vendors in China gain share by aligning with encryption rules and supplying inline machine-learning modules that process Mandarin threat intel. Multinational cloud providers partner with regional SOC operators to satisfy sovereignty clauses while maintaining global telemetry reach.

Europe maintains steady momentum on GDPR and the upcoming DORA framework, which requires demonstrable segmentation and incident reporting. SonicWall’s new European SOC exemplifies vendor investment to provide local data handling and rapid response aligned with residency laws. Germany and the United Kingdom focus on industrial espionage defenses, whereas France and Spain invest in cloud firewalls capable of per-tenant policy isolation for multicloud expansion.

Regulatory Landscape

Enterprise firewall deployments are increasingly shaped by prescriptive cyber risk requirements that move beyond policy statements into operational controls. In the EU, DORA (Regulation (EU) 2022/2554) raises the bar for financial entities by requiring periodic review of firewall rules and connection filters for ICT systems supporting critical or important functions (at least every six months), reinforcing demand for continuous policy governance and audit-ready reporting.

Across critical-infrastructure and digital-service scope, the EU is also tightening network-security obligations through instruments linked to NIS 2, supported by ENISA guidance (June 2025) on cybersecurity risk-management measures that include network security and access control practices. In the UK, the Department for Science published a draft Revised Telecommunications Security Code of Practice (June 2026) that offers technical guidance for public telecoms providers and explicitly references firewall security functions at security-zone boundaries, creating sector-specific compliance pressure on telecom and managed-service firewall architectures.

Value Chain Analysis

The enterprise firewall value chain begins with silicon and platform inputs (general-purpose CPUs, ASIC/NPUs, memory, NICs, and cryptographic components), then progresses through OS and security software stacks (policy engines, threat intelligence, TLS inspection, IPS/IDS signatures, and centralized management). OEMs and leading vendors combine hardware acceleration with software controls into appliances, virtual instances, and cloud-native Firewall-as-a-Service offerings, while procurement teams increasingly add supply-chain assurance steps such as SBOM requests and checks for device authenticity to limit risks from third-party dependencies and counterfeit equipment.

Go-to-market typically mixes direct enterprise sales with channel partners, service providers, and telecom operators that bundle firewall capabilities into managed security and connectivity packages. Downstream, implementation and lifecycle services (design, migration, policy tuning, compliance reporting, and 24/7 monitoring) have become a key value-capture layer as skills shortages make day-to-day policy operations harder to staff internally. Recent product direction also reflects closer coupling between networking throughput needs and security outcomes, as vendors highlight specialized silicon for encrypted-traffic inspection and AI-era workloads, alongside tighter integration with broader security platforms and observability.

Competitive Landscape

The enterprise firewall market shows moderate concentration. Fortinet, Palo Alto Networks, and Check Point anchor the field with extensive portfolios, yet the top five providers collectively control less than 70% of revenue, leaving room for innovators. Fortinet leverages over 500 AI patents to embed generative models inside its Security Fabric, while Palo Alto Networks’ Precision AI blends machine learning, deep learning, and LLMs for context-aware detection. Both firms prioritize ARR growth: Palo Alto Networks reported USD 5.1 billion in next-generation security ARR for fiscal Q1 2025, up 34% year over year.

Acquisition strategy accelerates convergence. Fortinet bought Lacework to bolster cloud workload protection and Next DLP for data loss prevention, while Cisco moved for Splunk to broaden telemetry and response orchestration. Check Point refocused on Infinity Global Services to lift subscription mix to 83% of revenue, signalling a switch from box-based billing to OPEX models.

Challengers differentiate via probabilistic firewalls and AI-native architectures that score traffic risk rather than match it to static rules. White-space also appears in operational-technology security, where vendors such as Rockwell Automation partner with firewall providers to fuse deterministic latency controls with deep packet inspection. Supply-chain chip constraints squeeze appliance margins yet push incumbents to invest in FPGA-based acceleration that reduces silicon dependence, thereby buffering future shortages.

Enterprise Firewall Industry Leaders

Fortinet, Inc.

Palo Alto Networks, Inc.

Check Point Software Technologies Ltd.

Cisco Systems, Inc.

Juniper Networks, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Operational automation and policy governance represent a clear whitespace, since compliance frameworks (including DORA and NIS 2-aligned guidance) require repeatable controls, evidence, and frequent ruleset review across hybrid environments. That, in turn, lifts demand for network security policy management and orchestration capabilities that reduce manual change windows, standardize segmentation intent, and generate audit artifacts across on-premises and cloud enforcement points, which aligns with the market shift toward managed and professional services.

AI-era enterprise networking is also driving a performance and control-plane upgrade cycle across data centers, campuses, and distributed edges, as organizations handle higher volumes of encrypted traffic and face new exposure from unsanctioned AI application usage. Vendor moves in 2026 show where budgets are going: Fortinet expanded FortiGate G-series platforms with AI-focused positioning (including shadow AI detection on new appliances and agentic capabilities in FortiOS 8.0), and Check Point introduced an agentic network security orchestration platform designed to compress policy work into verified automation. Together, these launches highlight opportunity for vendors and service providers that can combine high-throughput inspection with automated policy workflows across SASE, cloud, and traditional perimeter deployments.

Recent Industry Developments

- June 2026: WatchGuard launched new high-performance Firebox rackmount appliances (including models built for 100G networking via OCP 3.0 expansion). The release targets throughput-heavy enterprise networks and refresh cycles where encrypted inspection and east-west traffic volumes stress legacy firewall capacity.

- May 2025: Check Point introduced an agentic network security orchestration platform to compress policy work into verified automation. The platform integrates with SASE, cloud, and on-prem deployments to streamline policy creation and enforcement. This move expands automation capabilities across enterprise security architectures.

- August 2024: Fortinet acquired Next DLP to strengthen data loss prevention capabilities within its broader security portfolio. The deal supports tighter integration of firewall enforcement with data-centric controls as enterprises standardize policy across cloud, endpoint, and network layers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the enterprise firewall market covers revenue earned from firewall products and closely tied subscriptions used by organizations to control, inspect, and secure network traffic across enterprise locations, data centers, and cloud workloads.

Scope exclusions: We exclude stand-alone web application firewalls, pure SD-WAN gateways, and single-purpose intrusion detection sensors when they are sold as independent categories.

Segmentation Overview

- By Deployment Type

- On-Premise Appliance

- Cloud-Native Firewall-as-a-Service (FWaaS)

- Hybrid/Virtual Appliance

- By Component

- Hardware Appliance

- Virtual Appliance/Software

- Managed and Professional Services

- By Enterprise Size

- Small and Micro Enterprises ( <100 employees )

- Mid-sized Enterprises (100-999)

- Large Enterprises (≥1,000)

- By End-user Industry

- BFSI

- Healthcare and Life Sciences

- Manufacturing and Industrial

- Government and Defense

- Retail and E-commerce

- Telecom and Media

- Education and Research

- Energy and Utilities

- Other End-user Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Singapore

- Malaysia

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base structure of the model and to set realistic bounds on demand and spending. We reviewed public cybersecurity guidance and incident patterns, along with IT spending signals, to understand where enterprise firewall refresh cycles tend to cluster.

Common inputs came from public and official sources such as NIST publications, CISA advisories, US SEC filings, OECD digital economy statistics, and ITU indicators, followed by reputable press coverage and industry association materials where definitions are clarified. We also used paid subscriptions for company financials and intelligence, news and financials screening, and patent databases to map product focus and commercialization timing. The sources mentioned above are illustrative, since many other public materials were also used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to pressure test adoption assumptions and to fill gaps that public data does not explain well, including pricing packaging and how policy enforcement differs between on-premises deployments and cloud-delivered offerings. We spoke with a spread of channel partners, enterprise security leaders, network teams, and managed service providers across APAC, EMEA, and the Americas. Their input helped align the model to real buying cycles and renewal patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 12% | APAC: 42% |

| Mid tier: 49% | Functional/Unit leaders: 40% | EMEA: 33% |

| Smaller Players: 16% | Managers: 48% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using both top-down and bottom-up checks, so totals remain consistent with real enterprise security spend signals. In the top-down build, enterprise IT and security spending indicators are translated into firewall demand pools using penetration and refresh assumptions tied to network perimeter changes and cloud workload growth, and then the totals are corroborated with selective supplier and channel approximations.

Several inputs materially shaped the model, including enterprise headcount and site footprint trends, refresh and renewal timing for perimeter and internal segmentation controls, shifts in cloud workload share, average contract duration, and observed pricing progression by form factor (appliance, virtual, and cloud-delivered). Where bottom-up coverage was incomplete, gaps were handled through conservative coverage ratios and sanity checks against adjacent network security categories, before assumptions were finalized.

For forecasting, scenario analysis was applied, since buying behavior can change quickly after major breach cycles, compliance pushes, or sudden changes in remote access and cloud migration. The forward view was adjusted based on expert expectations for subscription mix, replacement timing, and how policy enforcement is consolidated across hybrid environments.

Data Validation & Update Cycle

Model outputs were checked against multiple independent signals, including vendor-reported security revenue direction, enterprise security budget commentary, and regional adoption cues gathered during interviews. When variances appeared, the assumptions behind penetration, refresh timing, and subscription attachment were revisited, and follow-up calls were triggered if the shift looked structural rather than temporary.

A multi-step internal review was completed before sign-off, so calculation logic, unit consistency, and currency conversion timing were verified. Reports are refreshed annually, and interim updates are made when material events occur that can move demand or pricing. Before delivery, a final analyst pass is run to ensure the latest public announcements and market signals are reflected.

Mordor Intelligence's Global Enterprise Firewall Market Market Size Compared Against Other Published Estimates

Published market sizes for enterprise firewalls can look different because each study sets its own boundary for what counts as a firewall revenue stream, and because base years and currency timing are not always aligned. The split between product revenue and attached subscriptions also changes the total, especially when cloud-delivered offerings are bundled in different ways.

Key gaps usually come from scope choices, including whether managed firewall services and threat-intelligence subscriptions are counted only when tied to core firewall deployments, or counted as part of a broader managed security bucket. By tracking contract structures and refreshing product versus subscription attachment assumptions, Mordor Intelligence keeps the total anchored to enterprise firewall use cases rather than adjacent security categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.12 B (2026) | |

| Global Consultancy A | USD 14.18 B (2024) | Uses a different base year and can treat the market as a wider enterprise network security spend pool, which may pull in adjacent services and pricing assumptions that do not map cleanly to firewall-only revenue. |

| Industry Publisher B | USD 11.30 B (2023) | Often applies a narrower definition focused on firewall product sales, with limited visibility on bundled subscriptions and renewal-driven revenue, which can reduce the reported total versus models that account for attachment. |

Overall, the spread is best explained by differences in year anchors and how attached subscriptions and services are treated, not by a single math issue. When the scope is consistently tied to enterprise firewall deployments and the pricing and renewal logic is checked with practitioners, the resulting number is easier to trace and repeat over time.

Key Questions Answered in the Report

What is the current value of the enterprise firewall market?

The market stands at USD 15.12 billion in 2026.

How fast is the enterprise firewall market expected to grow?

It is projected to expand at a 10.23% CAGR to reach USD 24.61 billion by 2031.

Which deployment model is growing the quickest?

Cloud-native Firewall-as-a-Service is set to grow at a 13.68% CAGR through 2031.

Why are services outpacing hardware in growth?

Skills shortages and complex compliance demands push enterprises to rely on managed and professional services, which are forecast to rise at a 13.52% CAGR.

Which region offers the highest growth potential?

Asia-Pacific, propelled by digital sovereignty mandates, is forecast to record a 12.38% CAGR through 2031.

What drives firewall adoption in the BFSI sector?

Strict regulatory requirements, high-value data assets, and real-time fraud risks make BFSI the largest vertical, holding 27.12% of 2025 revenues.

Page last updated on: