Salmonella Testing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.47 Billion |

| Market Size (2030) | USD 4.97 Billion |

| Growth Rate (2025 - 2030) | 7.47% CAGR |

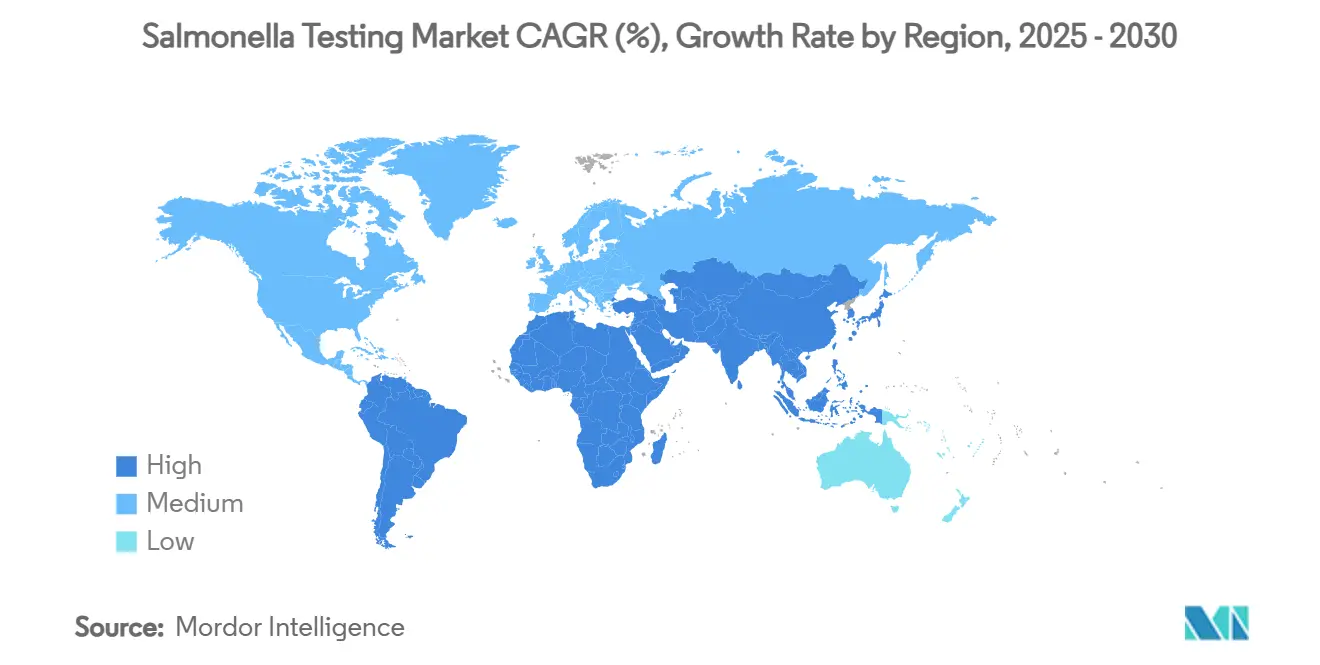

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

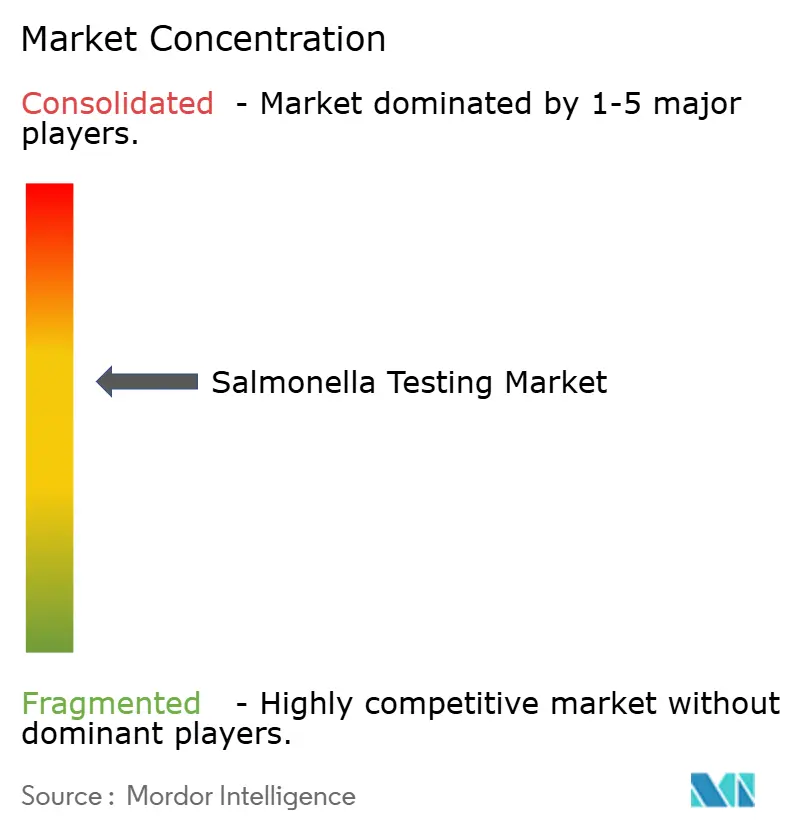

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Salmonella Testing Market Analysis by Mordor Intelligence

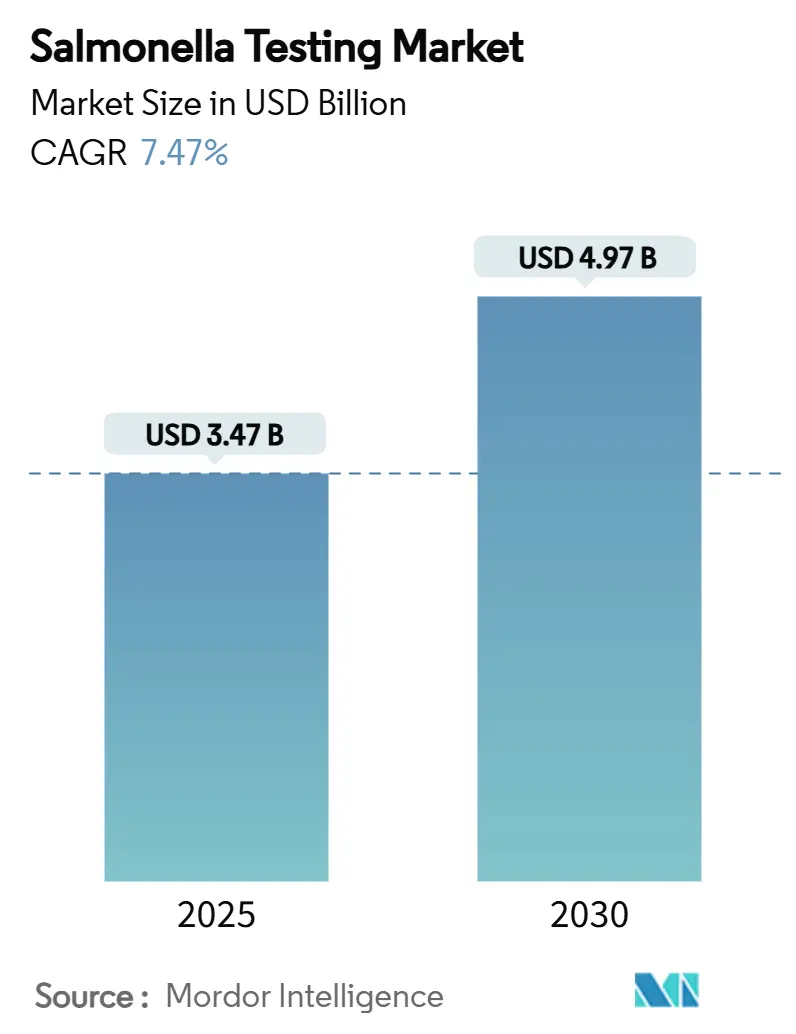

The Salmonella testing market size reached USD 3.47 billion in 2025 and is forecast to climb to USD 4.97 billion by 2030, reflecting a 7.47% CAGR through the period. New product approvals, private-sector investments that fill regulatory gaps, and widening applications in feed, water, and alternative proteins are together pushing the Salmonella testing market toward rapid molecular diagnostics and automated workflows. North America keeps its lead thanks to strict FSMA enforcement, yet Asia-Pacific shows the fastest trajectory as China, Australia, and Southeast Asian nations roll out genomic-surveillance networks that require higher test volumes. Test-kits and reagents continue to dominate purchases, although services see steeper growth as manufacturers without advanced labs outsource whole-genome sequencing and antimicrobial-resistance profiling. Competitive intensity is rising, with large reference labs acquiring regional players to build global footprints and start-ups introducing AI-powered point-of-need systems that compress result times from 48 hours to minutes. Market headwinds—chiefly the high cost of rapid kits for small firms, a lack of trained microbiologists in emerging regions, and false positives in complex matrices—moderate, but do not derail, the overall upward trend.

Key Report Takeaways

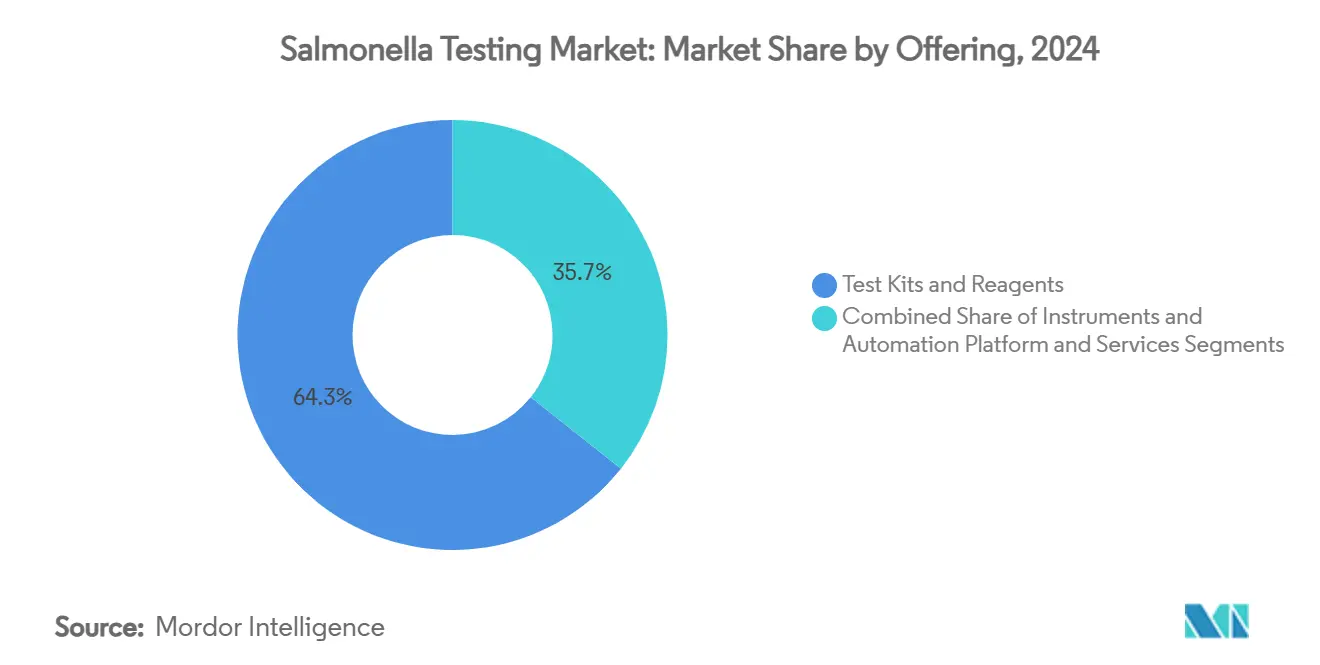

- By offering, test kits and reagents held 64.32% of Salmonella testing market share in 2024, while services are projected to grow at 11.23% CAGR to 2030.

- By test type, PCR commanded 37.48% of the Salmonella testing market size in 2024; isothermal methods are advancing at 10.58% CAGR through 2030.

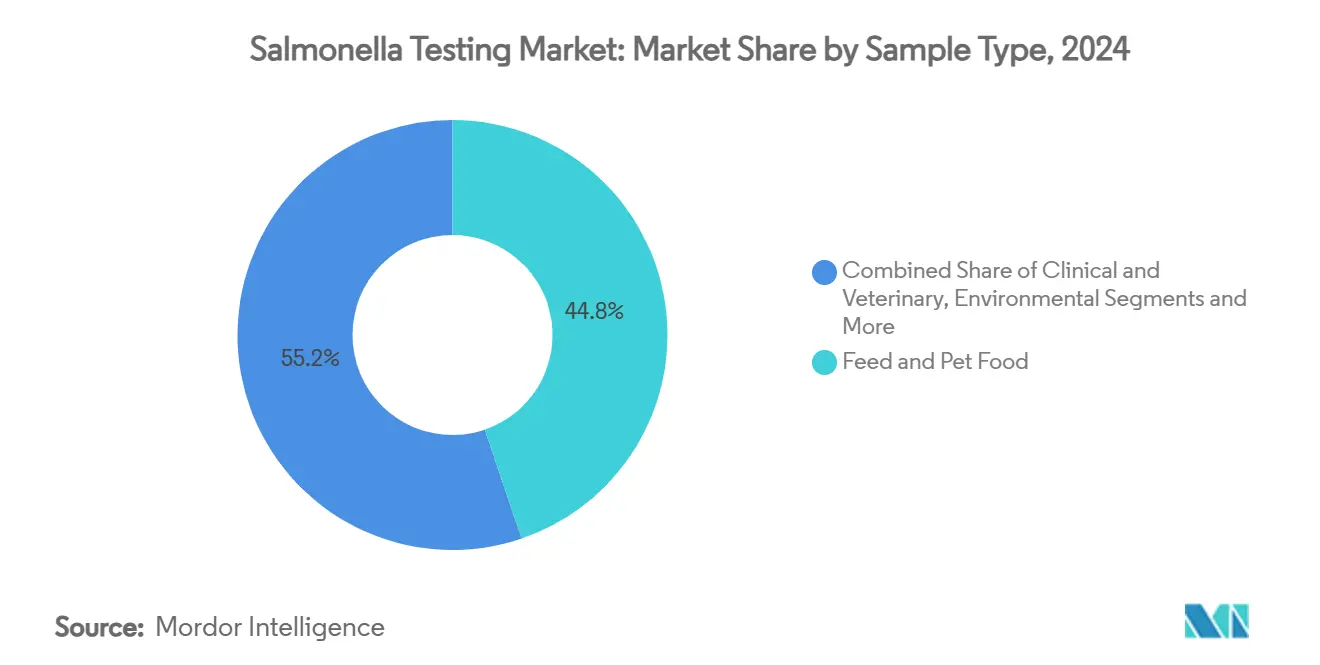

- By sample type, feed and pet food accounted for 44.78% of the Salmonella testing market in 2024 and is the fastest segment, growing at an 11.46% CAGR.

- By end-user, food and beverage manufacturers captured 33.44% of the Salmonella testing market share in 2024, yet contract laboratories exhibited the quickest rise at a 9.47% CAGR.

- North America represented 31.72% of the Salmonella testing market in 2024; Asia-Pacific is expanding at 9.41% CAGR to 2030.

Global Salmonella Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Enforcement Of FSMA & EU Microbiological Criteria | +1.2% | North America & EU | Medium term (2-4 years) |

| Rising Incidence Of Salmonellosis In Poultry & Eggs | +1.8% | Global | Short term (≤ 2 years) |

| Shift From Culture To Rapid PCR/LAMP Assays | +1.5% | Global, with early gains in North America, EU | Medium term (2-4 years) |

| National Genomic-Surveillance Roll-Outs | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Feed-Testing Boom Post Antibiotic-Growth-Promoter Bans | +1.1% | Global | Medium term (2-4 years) |

| Pathogen Testing Demand In Alternative Proteins | +0.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent FSMA & EU Microbiological Criteria

FDA guidance issued in 2024 obliges animal-feed producers to sample routinely, and USDA-FSIS now inspects plants making as little as 1,000 lb a month, vastly expanding the Salmonella testing market.[1]Center for Veterinary Medicine, “CPG Sec 690.800 Compliance Policy Guide Salmonella in Food for Animals,” fda.gov Equivalent updates in Europe mandate environmental monitoring programs that only rapid, same-shift assays can satisfy. Providers offering bundled compliance support rather than single kits gain a premium position.

Rising Incidence of Salmonellosis in Poultry & Eggs

CDC confirmed 79 U.S. cases tied to a single egg brand in 2025, reinforcing why processors double internal test frequencies.[2]Centers for Disease Control and Prevention, “Investigation Update: Salmonella Outbreak, Eggs, June 2025,” Centers for Disease Control and Prevention, cdc.gov The spread of multidrug-resistant S. Typhimurium ST213 heightens urgency for early detection.[3]José L. Puente, “Population Structure and Ongoing Microevolution of the Emerging Multidrug-Resistant Salmonella Typhimurium ST213,” Nature, nature.com Voluntary pre-harvest programs fill gaps left by delayed federal sampling of breaded stuffed chicken, further stimulating the Salmonella testing market.

Shift From Culture to Rapid PCR/LAMP Assays

Real-time PCR now detects as low as 220 fg/µL DNA, while LAMP delivers results in 20 minutes with 100% specificity, making both ideal for high-throughput or field settings. Pairing propidium monoazide with LAMP confirms cell viability, overcoming a key molecular limitation. OEMs pursuing AOAC approvals for plant-based matrices expand addressable end-markets.

National Genomic-Surveillance Roll-Outs

Australia’s integrated sequencing network speeds outbreak source tracing, cutting recall timeframes and encouraging other Asia-Pacific countries to invest in similar infrastructures. Large data sets expose transmission pathways, and machine learning now pinpoints clinical versus environmental isolates automatically.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Rapid Molecular Kits For SMEs | -0.8% | Global, particularly emerging markets | Short term (≤ 2 years) |

| Shortage Of Skilled Microbiologists In Emerging Markets | -0.6% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Cross-Reactivity False Positives In Spice & Cocoa Matrices | -0.4% | Global, concentrated in tropical regions | Medium term (2-4 years) |

| Regulatory Uncertainty On Salmonella "Adulterant" Status Outside Poultry | -0.5% | North America, with spillover to global markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost of Rapid Molecular Kits for SMEs

PCR platforms can exceed USD 50,000 while per-test costs run 3-5 times above culture, deterring small processors in price-sensitive markets. Vendors respond with compact, entry-level instruments and reagent-rental models, but adoption among micro-plants remains slow.

Shortage of Skilled Microbiologists in Emerging Markets

Whole-genome sequencing and AI analytics need cross-trained staff who are scarce in growing regions. Manufacturer-led academies and virtual training help, yet the talent pipeline lags behind the Salmonella testing market’s growth, especially for interpreting resistome data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Momentum Amid Reagent Dominance

The Salmonella testing market size for test kits and reagents stood at USD 2.23 billion in 2024, translating into 64.32% of total revenue. Services, however, are on pace for 11.23% CAGR as more firms outsource next-generation sequencing and in-silico serotyping that require advanced bioinformatics. Market leaders bundle analytics dashboards with traditional assays, strengthening client stickiness and raising switching costs.

Integrated platforms drive demand for instruments, too. bioMérieux posted 13% reagent sales growth in H1 2024, an indicator that users value closed-system ecosystems that minimize cross-contamination and speed workflows. Mérieux NutriSciences’ EUR 360 million acquisition of Bureau Veritas’ food-testing arm instantly added 34 labs, showing how consolidation fast-tracks geographic coverage while boosting overall Salmonella testing market share.

By Test Type: Isothermal Solutions Challenge PCR

PCR held the largest Salmonella testing market share at 37.48% in 2024 due to deep validation history and broad instrument installed bases. Yet isothermal methods, chiefly LAMP, clock a 10.58% CAGR through 2030. Their ability to operate on battery-powered heaters lowers capital thresholds and suits on-farm or border-inspection contexts.

Multiplex LAMP panels now detect multiple serovars simultaneously, addressing lab throughput concerns. FDA reviews of plant-based matrices continue, but early adopters report shorter product-release cycles thanks to 20-minute turnaround times. Conventional culture remains indispensable for regulatory confirmation, and sequencing accelerates for source-tracking and resistance surveillance, adding layers rather than replacing methods.

By Sample Type: Feed Testing Surges Beyond Traditional Food Matrices

Feed & pet food preserved the lion’s share—44.78%—of Salmonella testing market size in 2024 because of ongoing USDA verification sampling. The fastest ascent comes from feed & pet food at 11.46% CAGR as post-antibiotic regulations require quantitative load tracking from raw ingredients to finished feed. Environmental swabbing gains traction within HACCP plans, while clinical and veterinary testing expands due to zoonotic surveillance.

Phytogenic additives and organic acids used in antibiotic-free feed strategies necessitate precise monitoring to confirm pathogen-reduction efficacy. Quantitative assays such as Neogen’s new MDA2 platform grant poultry integrators a data-driven view of intervention success, underscoring how feed applications widen the Salmonella testing market.

By End-user: Contract Labs Capture Complexity-Driven Growth

Food & beverage manufacturers generated 33.44% of value in 2024, driven by in-house PCR and culture workflows integrated into QA programs. Contract labs are slated for 9.47% CAGR as they absorb tasks that demand advanced analytics, such as whole-genome SNP comparisons and resistome mapping.

Mérieux NutriSciences’ acquisition extends its global laboratory network, letting multinational clients centralize testing protocols and data management. Government and research institutes continue to pilot new methods—like nanopore sequencing—for outbreak forensics, indirectly stimulating commercial uptake via published validations.

Geography Analysis

North America retained 31.72% of revenue in 2024. Mature FSMA enforcement drives routine testing, but growth is moderating as infrastructure is largely installed. The April 2025 withdrawal of the Salmonella framework created short-term uncertainty; nevertheless, many processors escalated voluntary testing rather than scale back, sustaining demand. Innovation leadership remains high, illustrated by Spore.Bio’s AI-enabled inline detectors that promise instant alerts.

Asia-Pacific posts the fastest rise at 9.41% CAGR. China’s 47 new national food-safety standards, including 16 microbial methods, expand market scope and formalize procurement budgets. Australia’s genomic-surveillance grid shortens outbreak investigations, demonstrating tangible ROI that neighboring countries now seek to replicate. Resistance hot spots, such as Shanghai’s outpatient isolates showing fluoroquinolone insensitivity, push hospitals and regulators to broaden testing panels.

Europe delivers steady gains on consistent enforcement of microbiological criteria. The UK Health Security Agency’s 2024 ready-to-eat guidance cements demand for rapid, on-site screening. Brexit adds documentation complexity for pan-EU labs, indirectly lifting service revenues. Sweden’s outbreak-driven Salmonella case surge confirms ongoing vigilance needs even in high-compliance settings.

Middle East & Africa and South America together remain smaller but opportunity-rich. Egypt’s detection of pan-drug-resistant strains in cattle underscores an urgent need for robust diagnostics. Water-borne contamination across South American rivers positions environmental-testing vendors for volume growth as utilities adopt proactive surveillance.

Competitive Landscape

The Salmonella testing market shows moderate concentration. bioMérieux, Mérieux NutriSciences, Neogen, QIAGEN, and Bio-Rad hold leading positions through method validations, proprietary reagents, and acquisitions. Mérieux NutriSciences’ purchase of Bureau Veritas’ food unit instantly broadened its geographic footprint and doubled Asian capacity. bioMérieux’s buyout of Neoprospecta folds advanced genomics into its portfolio and supports double-digit organic revenue in microbiology.

QIAGEN is rolling out three automated sample-prep instruments by 2026 to cover low-, mid-, and high-throughput labs, aiming to tie customers to its chemistry ecosystem. Neogen’s quantitative enrichment media signal a pivot from purely qualitative detection to load monitoring, differentiating its pipeline. Start-ups like Spore.Bio target ultra-rapid detection; if proven at scale, such AI-linked optical sensors could upend conventional lab-based workflows and redistribute Salmonella testing market share toward inline systems.

Salmonella Testing Industry Leaders

Thermo Fisher Scientific

bioMérieux

Merck KGaA

Solventum

Eurofins Scientific

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: USDA-FSIS withdrew its proposed Salmonella framework for raw poultry, spurring voluntary private-sector testing investments.

- March 2025: Bio-Rad launched XP-Design Assay Salmonella Serotyping Solution for rapid detection and fine-scale strain characterization in foods and environmental samples.

- March 2025: BioAlert raised USD 2.5 million to develop water-safety pathogen detectors, signaling cross-sector expansion of Salmonella testing technology.

- January 2025: Neogen introduced the Molecular Detection Assay 2 Quantitative Salmonella kit, enabling producers to measure pathogen loads alongside qualitative screens.

Global Salmonella Testing Market Report Scope

| Instruments & Automation Platforms |

| Test Kits & Reagents |

| Services |

| Conventional Culture Methods |

| Immunoassay |

| PCR-based |

| Isothermal |

| Next-Generation Sequencing |

| Food |

| Feed & Pet Food |

| Clinical & Veterinary |

| Environmental |

| Food & Beverage Manufacturers |

| Contract Testing Laboratories |

| Healthcare & Clinical Labs |

| Veterinary & Animal Health Facilities |

| Government & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Instruments & Automation Platforms | |

| Test Kits & Reagents | ||

| Services | ||

| By Test Type | Conventional Culture Methods | |

| Immunoassay | ||

| PCR-based | ||

| Isothermal | ||

| Next-Generation Sequencing | ||

| By Sample Type | Food | |

| Feed & Pet Food | ||

| Clinical & Veterinary | ||

| Environmental | ||

| By End-user | Food & Beverage Manufacturers | |

| Contract Testing Laboratories | ||

| Healthcare & Clinical Labs | ||

| Veterinary & Animal Health Facilities | ||

| Government & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the Salmonella testing market?

The Salmonella testing market size stands at USD 3.47 billion in 2025.

How fast is the market expected to grow through 2030?

Revenue is projected to rise at a 7.47% CAGR, reaching USD 4.97 billion by 2030.

Which region is expanding the fastest?

Asia-Pacific leads growth with a 9.41% CAGR, propelled by new national standards and genomic-surveillance investments.

What testing method is gaining traction over PCR?

Loop-mediated isothermal amplification (LAMP) is the fastest-growing method, offering results in 20 minutes with minimal equipment.

Why are services growing faster than reagents?

Outsourcing of complex analyses such as whole-genome sequencing drives double-digit growth for contract laboratories.

How is regulatory change affecting demand?

Even with the withdrawal of proposed U.S. poultry rules, manufacturers have raised voluntary testing to manage liability, keeping demand strong.

Page last updated on: