Rapid Microbiology Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

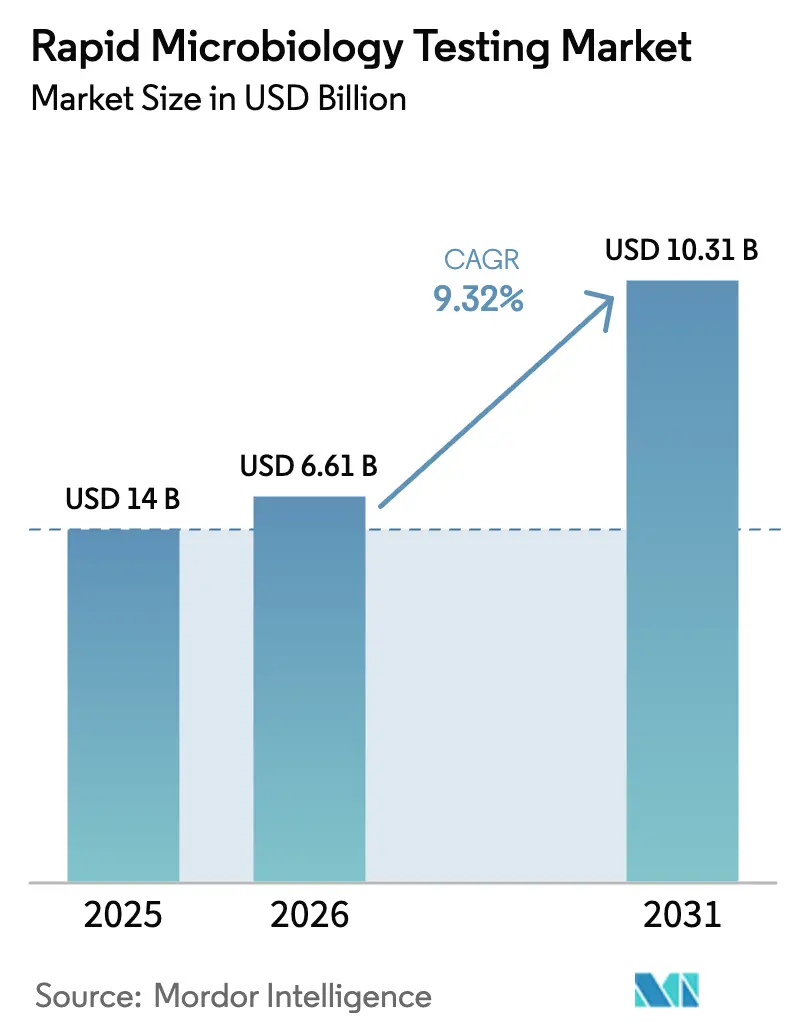

| Market Size (2026) | USD 6.61 Billion |

| Market Size (2031) | USD 10.31 Billion |

| Growth Rate (2026 - 2031) | 9.32% CAGR |

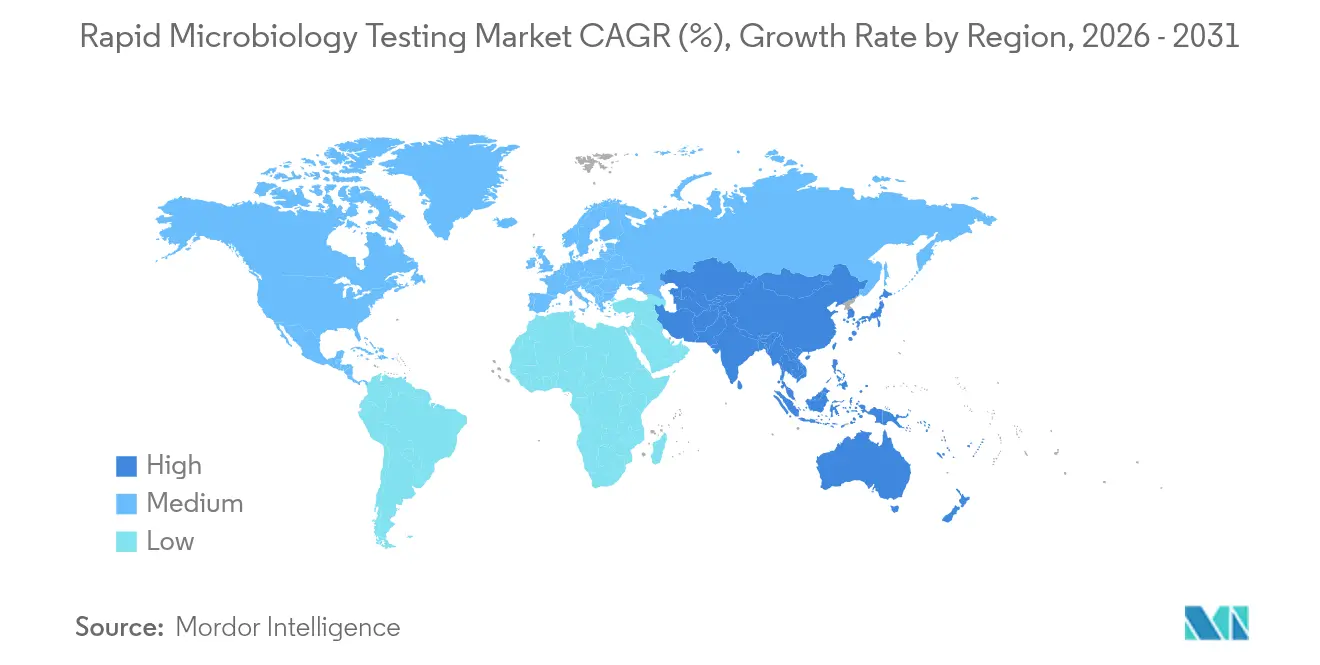

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rapid Microbiology Testing Market Analysis by Mordor Intelligence

The rapid microbiology testing market size was valued at USD 6.04 billion in 2025 and estimated to grow from USD 6.61 billion in 2026 to reach USD 10.31 billion by 2031, at a CAGR of 9.32% during the forecast period (2026-2031). A confluence of faster-release imperatives in pharmaceutical production, the healthcare sector’s demand for point-of-care diagnostics, and food processors’ need for real-time quality control sustain this brisk growth trajectory. Technologies such as MALDI-TOF mass spectrometry now achieve 95% bacterial identification accuracy within minutes, while automated sterility platforms like bioMérieux’s BACT/ALERT 3D cut testing cycles from 14 days to mere hours. Regulatory momentum also supports adoption: in 2025 the FDA re-classified clinical mass-spectrometry systems as Class II devices, trimming compliance barriers and widening access[1]U.S. Food and Drug Administration, “Class II Special Controls for Mass Spectrometry Systems,” fda.gov. Across laboratories, investments in total lab automation are accelerating; BD’s Kiestra systems report up to 46% higher bacterial recovery and markedly lower hands-on time. In food and beverage plants, rapid methods validated by AOAC and AFNOR shrink pathogen detection windows to under two hours, limiting costly production holds.

Key Report Takeaways

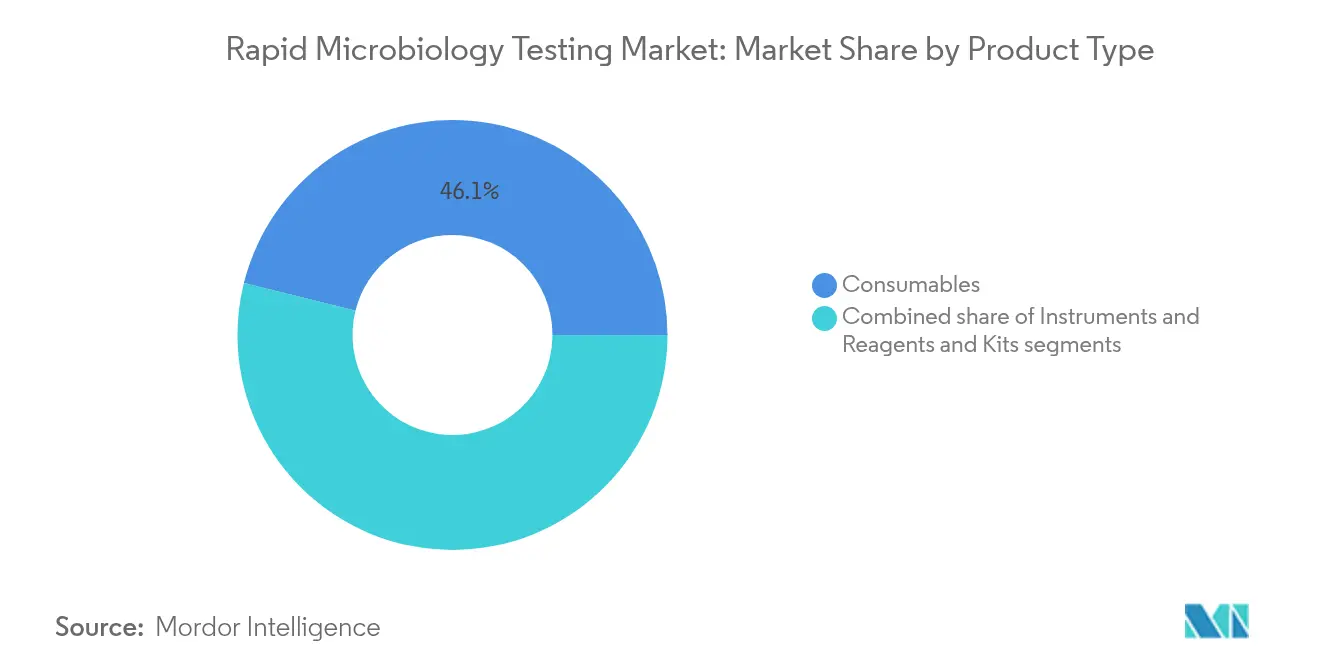

- By product type, consumables led with 46.12% of rapid microbiology testing market share in 2025; instruments are slated to expand at 10.78% CAGR through 2031.

- By method, nucleic acid-based technologies commanded 54.05% revenue in 2025, while immunological approaches are set to grow fastest at 10.6% CAGR to 2031.

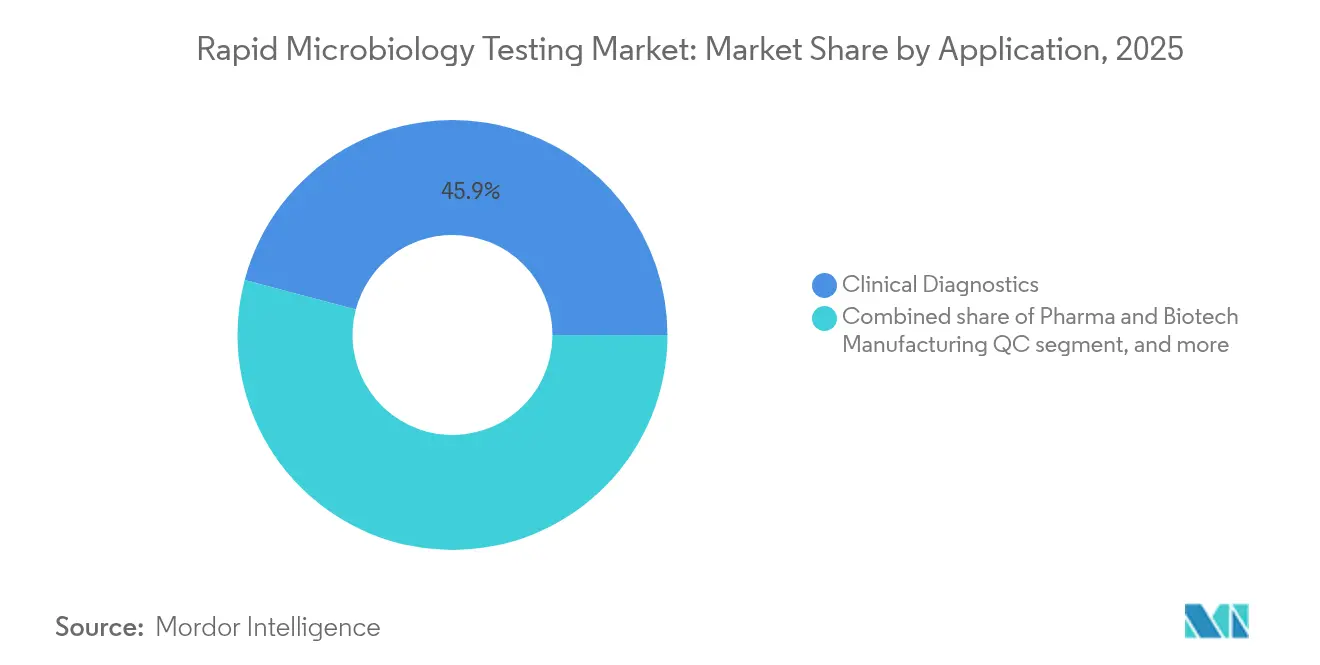

- By application, clinical diagnostics retained 45.88% share in 2025; pharmaceutical and biotech quality control will register the highest 12.05% CAGR through 2031.

- By end user, clinical laboratories accounted for 49.02% share in 2025; pharma and biotech companies are forecast to post a 11.9% CAGR through 2031.

- By geography, North America dominated with 39.12% revenue in 2025, yet Asia-Pacific is on track for a 10.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rapid Microbiology Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of infectious and chronic diseases | +2.1% | Global; acute in Asia-Pacific & Sub-Saharan Africa | Medium term (2-4 years) |

| Strengthening global food safety and quality regulations | +1.8% | North America & EU; expanding to APAC | Long term (≥4 years) |

| Continuous technological innovations in rapid diagnostics | +2.3% | Global; led by North America & Western Europe | Short term (≤2 years) |

| Increasing government and institutional funding for microbiology infrastructure | +1.4% | North America, EU & emerging APAC | Medium term (2-4 years) |

| Growing demand for in-process quality control in biopharmaceutical manufacturing | +1.7% | Global; biomanufacturing hubs | Short term (≤2 years) |

| Expansion of decentralized point-of-care testing networks | +1.9% | Global; rapid uptake in resource-limited areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Infectious and Chronic Diseases

Healthcare systems are prioritizing rapid pathogen identification to cut mortality and curb outbreaks. In U.S. hospitals, every hour of delay in targeted therapy for bloodstream infections lifts mortality by 7.6%, steering demand toward platforms that deliver species-level results in under 90 minutes. Resistant pathogens such as Candida auris further raise the stakes, with updated MALDI-TOF databases now posting 100% identification accuracy for this organism. The FDA’s 2025 clearance of Visby Medical’s at-home STI panel underscored growing confidence in near-patient molecular tools boasting up to 100% sensitivity. Aging demographics in developed regions and high infectious-disease prevalence elsewhere converge to keep test volumes high, while AI analytics sharpen sensitivity and reduce false positives.

Strengthening Global Food Safety and Quality Regulations

Tighter legislation is compelling processors to adopt rapid assays that satisfy compliance without lengthening production cycles. The U.S. Food Safety Modernization Act and the EU’s revised hygiene package require faster, validated methods, encouraging beverage firms such as Eckes-Granini to use bioMérieux’s D-COUNT to cut detection time to two hours. More than half of industrial food samples in the United States are now tested with rapid microbiological techniques rather than culture plates. Dairy plants employing Hygiena’s AOAC-certified assays verify product safety in under eight hours, freeing chilled storage capacity and lowering costs. Regulatory acceptance of AOAC and AFNOR validations thus aligns safety with speed.

Continuous Technological Innovations in Rapid Diagnostics

Advances in mass spectrometry, robotics, and AI are transforming laboratory economics and accuracy. Bruker’s sirius MALDI-TOF can process 600 samples an hour at 98.3% accuracy, rivaling 16S rRNA sequencing speed. Researchers at the Technical University of Munich trimmed identification time to minutes for 232 species using enhanced MS libraries. Full-lab robotics such as BD Kiestra automate plating, incubation, and imaging, raising throughput while slashing error rates. AI-assisted image analytics now outperform manual parasite screening five-fold on sensitivity metrics. NGS tie-ins for hospital hygiene mapping add epidemiological insight without delaying routine workflows.

Increasing Government and Institutional Funding for Microbiology Infrastructure

Public-sector capital injections underpin long-range demand for automated systems. Michigan allocated USD 326 million to a 300,000 sq ft public health lab equipped for 7 million annual tests, embedding rapid sterility and genomic surveillance capability[2]Michigan Department of Health and Human Services, “State Public Health Lab Modernization,” michigan.gov. The CDC’s Advanced Molecular Detection initiative funnels grants into state labs to mainstream NGS and bioinformatics. Academia-industry tie-ups such as QIAGEN’s partnership with McGill University channel resources into microbiome-driven diagnostic programs. Funding in emerging economies is also rising as donors seek to strengthen outbreak preparedness.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial capital investment requirements | −1.2% | Global; particularly acute in emerging markets | Short term (≤2 years) |

| Stringent validation and regulatory compliance procedures | −0.8% | North America & EU; spreading globally | Long term (≥4 years) |

| Limited integration with laboratory information systems | −0.6% | Global | Medium term (2-4 years) |

| Shortage of skilled workforce in advanced microbiology techniques | −0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Investment Requirements

Automated MS or incubation suites can demand seven-figure budgets, deterring small labs. Yet firms such as Biogen recoup outlays within 18 months via labor savings and quicker release cycles. Financing models now include leasing and pay-per-use contracts that cap upfront cash exposure. In emerging markets, currency risk complicates budgeting, but total cost of ownership analyses increasingly favor rapid systems thanks to lower reagent volumes and reduced inventory carry.

Stringent Validation and Regulatory Compliance Procedures

Regulators insist on exhaustive equivalency studies against culture methods. USP <1223> and PDA TR-33 stipulate multi-parameter validations that can last months and demand dedicated QA teams. Pharma firms must also perform method transfer packages for every site. Harmonization is improving: the FDA’s 2024 LDT framework and the EMA’s mutual recognition of AOAC validations shorten some timelines. Vendors now supply pre-validated workflows to ease customer burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automation Spurs Instrument Uptake

Consumables continued to generate steady annuity revenue, holding 46.12% of rapid microbiology testing market share in 2025 because every test run consumes reagents, media, and disposable kits. Growth, however, is shifting toward hardware; instruments are forecast to log an 10.78% CAGR through 2031 as labs pursue high-throughput automation and data integrity. The instruments wave is led by MALDI-TOF units that now cost less per test than biochemical panels, and by fully enclosed incubation-imaging systems that cut technician interventions. The rapid microbiology testing market size for instruments is projected to expand alongside pharmaceutical automation spending and hospital drive for lean staffing. Integrated solutions bundle readers with proprietary cartridges, securing high switching costs for vendors.

Reagents and kits remain indispensable, especially as suppliers launch pathogen-specific panels and resistance gene assays that command premium pricing. Fluorescence and bioluminescence reagents target sterility testing in biologics where every day saved equals working-capital relief. Bundled service contracts linking instrument placement with consumable minimums protect margins amid price competition. Nine of the top ten producers have added middleware to track lot numbers automatically, helping customers with 21 CFR 11 audit readiness.

By Method: Immunological Tools Gain Accessibility Edge

Nucleic acid-based techniques held 54.05% revenue in 2025 thanks to PCR’s unrivaled sensitivity. These assays detect slow-growing or non-culturable organisms, making them indispensable in clinical sepsis panels and environmental monitoring of water systems. Yet immunological formats, notably lateral-flow strips, are set for an 10.6% CAGR to 2031 because they require minimal infrastructure and deliver results that non-specialists can interpret. Point-of-care adoption accelerated after the FDA cleared an at-home triple STI test in 2025, proving consumer readiness.

Hybrid technologies are blurring boundaries: digital immunoassays embed microfluidics and fluorescence detection that push sensitivity near PCR levels. Meanwhile, MALDI-TOF bridges phenotypic and genotypic characterization, providing proteomic fingerprints in minutes. Cellular component assays such as ATP bioluminescence still dominate in-process hygiene control where absolute counts, not species ID, drive decisions. Vendors are integrating cloud analytics to harmonize outputs from multiple method types onto common dashboards.

By Application: Biopharma Quality Control Outpaces Clinical Testing

Clinical diagnostics generated 45.88% of spending in 2025 since hospital micro labs must report actionable results around the clock. Syndromic respiratory panels, bloodstream infection workflows, and antimicrobial stewardship programs keep throughput high. Yet pharmaceutical and biotech QC will be the fastest-rising use case at 12.05% CAGR through 2031 because regulators encourage real-time release testing. The rapid microbiology testing market size for pharmaceutical QC is fueled by continuous bioprocessing lines where each batch holds multi-million-dollar value. Automated endotoxin and sterility platforms mitigate inventory hold costs and plug seamlessly into electronic batch records.

Food and beverage processors enlarge their footprint as they swap traditional plating for rapid assays that align with tight just-in-time supply chains. Dairy and beverage facilities show the quickest conversions because chilled storage is expensive. Environmental monitoring in utilities and industrial water loops is another growth pocket as municipalities confront stricter pathogen limits. Across applications, the overarching trend is shifting from retrospective quality assurance toward real-time control.

By End User: Pharma & Biotech Laboratories Become Growth Engine

Clinical laboratories retained 49.02% share in 2025, leveraging centralized expertise and economies of scale. Reference networks integrate high-volume MALDI-TOF and total lab automation to keep cost per reportable low. However, pharma and biotech companies are projected to post a 11.9% CAGR to 2031 as they internalize rapid sterility and bioburden workflows to protect proprietary biologics pipelines. The rapid microbiology testing market size growth in this cohort reflects expanding CGMP cell and gene therapy suites that demand in-house contamination surveillance.

Hospitals are decentralizing tests to emergency departments via cartridge-based platforms that deliver pathogen ID in under an hour at the bedside. Food and beverage firms invest in on-line sampling stations to avoid shipment delays. Service laboratories in contract testing quickly adopt the latest validated methods to win outsourcing contracts from mid-tier manufacturers lacking capital to equip in-house labs.

Geography Analysis

North America captured 39.12% of 2025 revenue because of mature healthcare reimbursement, early FDA clearances, and a dense base of biologics manufacturers. Hospitals deploy rapid PCR panels such as Cepheid’s Xpert HCV, enabling same-visit diagnosis and treatment initiation. Major reference chains like Quest Diagnostics weave AI into digital microbiology to boost throughput without extra staff. State-level investments, exemplified by Michigan’s new public health laboratory, further broaden high-throughput capacity. While market-wide pricing pressure is intensifying, upgrades to cope with multidrug-resistant organisms sustain spending.

Asia-Pacific is forecast to log a 10.02% CAGR to 2031 as China and India expand biomanufacturing and harmonize validation standards with the FDA and EMA. Continuous bioprocessing lines for monoclonal antibodies and vaccines require in-line sterility assurance, creating robust new demand. Singapore’s cell and gene therapy hub collaborates with Charles River Laboratories to stand up CGMP testing that meets global release timelines. Decentralized healthcare initiatives funnel portable diagnostic kits into rural clinics, extending microbiology reach beyond tertiary centers.

Europe maintains steady momentum anchored by stringent food safety mandates and world-class pharma production clusters in Germany and Switzerland. bioMérieux’s EUR 25 million R&D expansion near Lyon underlines the region’s innovation depth. EU rules on sustainability dovetail with rapid tests’ lower plastic waste and energy use versus culture incubators. Latin America, the Middle East, and Africa remain nascent but are adopting validated rapid assays as multinational drug makers build fill-finish plants that must export to ICH markets.

Competitive Landscape

The rapid microbiology testing market shows moderate concentration. Top vendors blend organic R&D with targeted M&A to widen portfolios. bioMérieux posted 9% microbiology sales growth in 2024 on the back of automated ID and blood culture systems while rolling out the 3P ENTERPRISE platform that digitalizes pharmaceutical environmental monitoring. BD is spinning off its USD 3.4 billion biosciences and diagnostics arm to heighten focus and unlock shareholder value in life science instrumentation. Danaher opened two CLIA-certified labs to accelerate companion diagnostics, signaling intensifying cross-play between devices and therapeutics.

Emerging challengers exploit AI and novel optics. An AI-powered UV spectroscopy prototype from the Singapore-MIT Alliance detects contamination in 30 minutes, promising to disrupt culture-centric sterility workflows[3]Singapore-MIT Alliance for Research and Technology, “AI-Driven UV Spectroscopy Platform,” smart.mit.edu. Consolidation is evident: Mérieux NutriSciences paid EUR 360 million for Bureau Veritas’ worldwide food testing operations, instantly adding 34 labs across 32 nations. Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification unit strengthens upstream bioprocessing capabilities critical to rapid tests used in lot release.

R&D intensity is a key differentiator. Bruker is expanding into NGS-enabled hospital hygiene tracing via collaboration with Ridom GmbH. Vendors offering end-to-end solutions that combine hardware, reagents, analytics, and regulatory consulting capture share as customers favor single-provider ecosystems that simplify validation.

Rapid Microbiology Testing Industry Leaders

Abbott Laboratories

Becton, Dickinson & Company

Thermo Fisher Scientific, Inc.

Danaher

Biomerieux SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Nelson Labs launched rapid sterility testing services in the United States and Germany, shaving incubation periods from up to 20 days to six using bioluminescence technology while remaining USP-compliant.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, adding high-growth bioprocessing assets.

- February 2025: BD revealed plans to separate its Biosciences and Diagnostic Solutions unit, a USD 3.4 billion revenue segment, by fiscal 2026.

- January 2025: Charles River Laboratories unveiled Apollo for CRADL, a cloud platform that streamlines drug discovery workflows across safety and biologics management.

- November 2024: Biomerieux SA introduced 3P ENTERPRISE, integrating smart plates, connected software, and automated incubation for pharmaceutical environmental monitoring.

Global Rapid Microbiology Testing Market Report Scope

Rapid microbiology testing refers to the near-real-time analysis of a sample to determine the presence of a microbe of interest. Different companies have launched advanced kits to obtain accurate results through rapid microbiology testing.

The rapid microbiology testing market is segmented into product type, method, end-user, and geography. The market is segmented by product type into consumables, instruments, and reagents and kits. The instruments segment is further segmented into automated identification and testing systems, bioluminescence and fluorescence-based detection systems, mass spectrometers, and other instruments. The market is segmented by method into cellular component-based testing, nucleic acid-based testing, and other methods. Based on end user, the market is segmented into clinical laboratories, food and beverage industry, healthcare facilities, life science research and development facilities, and other end users. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also offers the market size and forecasts for 17 countries across the region. For each segment, the market sizing and forecasts were made on the basis of value (USD).

| Consumables | |

| Instruments | Automated Identification & Testing Systems |

| Bioluminescence & Fluorescence Detection Systems | |

| Mass Spectrometers | |

| Other Instruments | |

| Reagents & Kits |

| Cellular Component-Based Methods |

| Nucleic Acid-Based Methods |

| Immunological |

| Other Methods |

| Clinical Diagnostics |

| Pharmaceutical & Biotech Manufacturing QC |

| Food & Beverage Testing |

| Other Applications |

| Clinical Laboratories |

| Healthcare Facilities (Hospitals & POC) |

| Food & Beverage Companies |

| Pharma & Biotech Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Consumables | |

| Instruments | Automated Identification & Testing Systems | |

| Bioluminescence & Fluorescence Detection Systems | ||

| Mass Spectrometers | ||

| Other Instruments | ||

| Reagents & Kits | ||

| By Method | Cellular Component-Based Methods | |

| Nucleic Acid-Based Methods | ||

| Immunological | ||

| Other Methods | ||

| By Application | Clinical Diagnostics | |

| Pharmaceutical & Biotech Manufacturing QC | ||

| Food & Beverage Testing | ||

| Other Applications | ||

| By End User | Clinical Laboratories | |

| Healthcare Facilities (Hospitals & POC) | ||

| Food & Beverage Companies | ||

| Pharma & Biotech Companies | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the rapid microbiology testing market?

The market was valued at USD 6.61 billion in 2026 and is forecast to rise to USD 10.31 billion by 2031.

Which product category is growing fastest?

Instruments are projected to post the highest 10.78% CAGR through 2031 because laboratories are automating workflows to boost accuracy and throughput.

Why are pharmaceutical companies investing heavily in rapid microbiology testing?

Continuous manufacturing and real-time release protocols require faster sterility and bioburden results, driving a 12.05% CAGR in pharmaceutical and biotech quality control applications.

Which region is expected to see the strongest growth?

Asia-Pacific is slated for a 10.02% CAGR thanks to expanding biomanufacturing capacity and regulatory alignment with U.S. and EU standards.

How are regulatory changes affecting adoption?

The FDA’s re-classification of clinical mass-spectrometry systems to Class II and acceptance of AOAC-validated methods reduce compliance hurdles, promoting wider deployment.

What technological advances are shaping the next wave of rapid tests?

High-throughput MALDI-TOF, AI-enhanced image analysis, and NGS-based epidemiology tools are cutting turnaround times and adding strain-level insight to routine testing.

Page last updated on: