Legionella Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

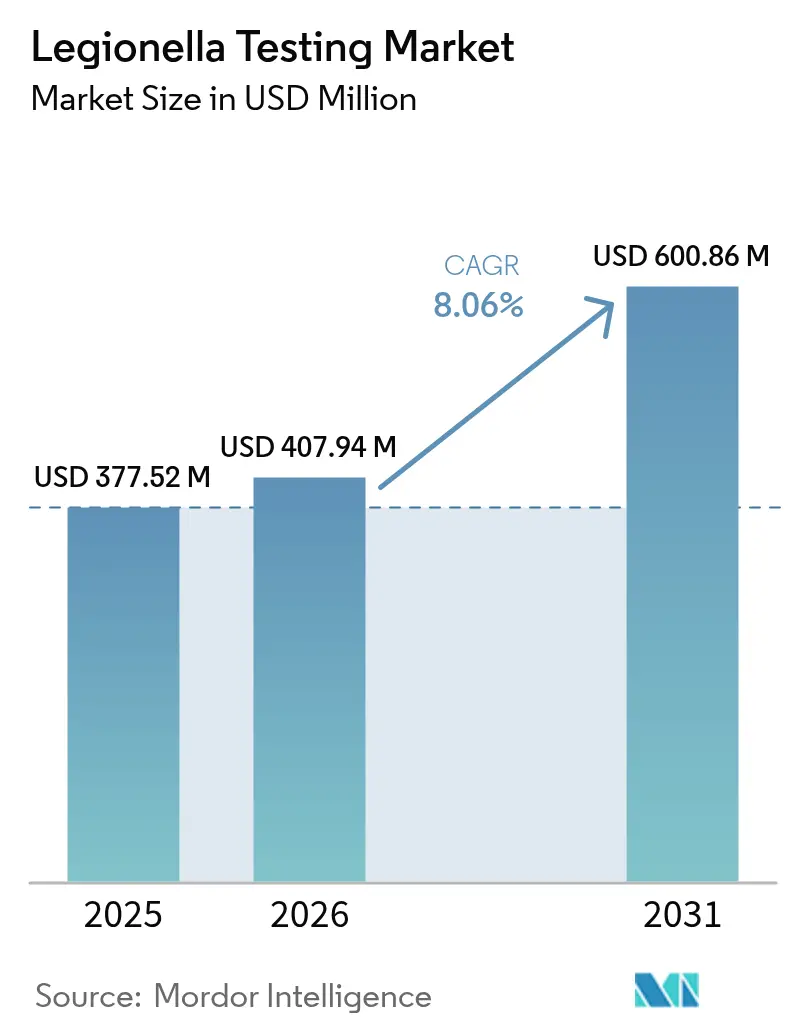

| Market Size (2026) | USD 407.94 Million |

| Market Size (2031) | USD 600.86 Million |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Legionella Testing Market Analysis by Mordor Intelligence

The legionella testing market size was valued at USD 377.52 million in 2025 and estimated to grow from USD 407.94 million in 2026 to reach USD 600.86 million by 2031, at a CAGR of 8.06% during the forecast period (2026-2031). Stricter building-water regulations, heightened post-pandemic vigilance, and rapid advances in molecular diagnostics are sustaining double-digit demand growth. Mandatory CMS rules that link Medicare funding to implementation of ASHRAE-compliant water management programs keep hospitals and long-term-care facilities on a continuous testing cycle[1]Centers for Medicare & Medicaid Services, “Legionella Water Management Initiative,” cms.gov. Rising legal liability and insurance stipulations have extended this compliance mindset to hotels, commercial real estate, and manufacturing plants. Technology migration toward PCR platforms has shortened result turnaround from 7–14 days to under 48 hours, enabling early intervention protocols that limit outbreak scale.

Key Report Takeaways

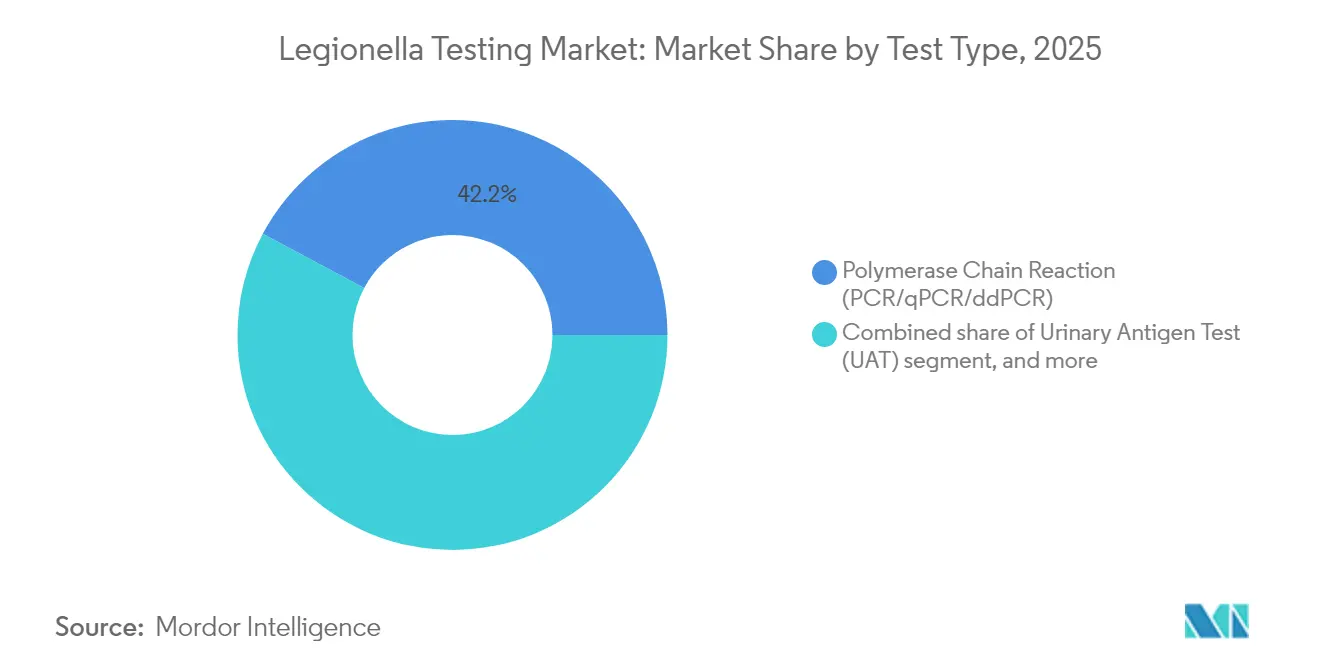

- By test type, PCR/qPCR/ddPCR held 42.20% of Legionella testing market share in 2025, whereas urinary antigen tests are projected to grow at a 10.41% CAGR through 2031.

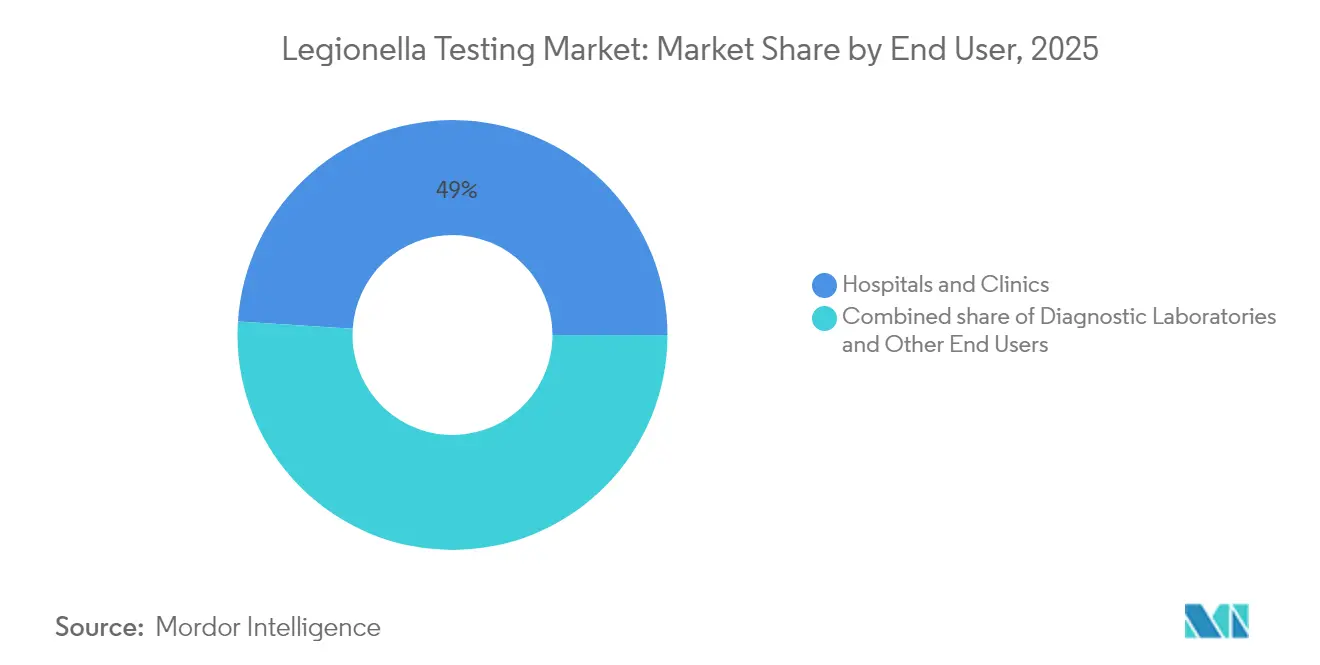

- By end user, hospitals and clinics controlled 49.00% revenue in 2025; diagnostic laboratories lead growth at an 11.38% CAGR to 2031.

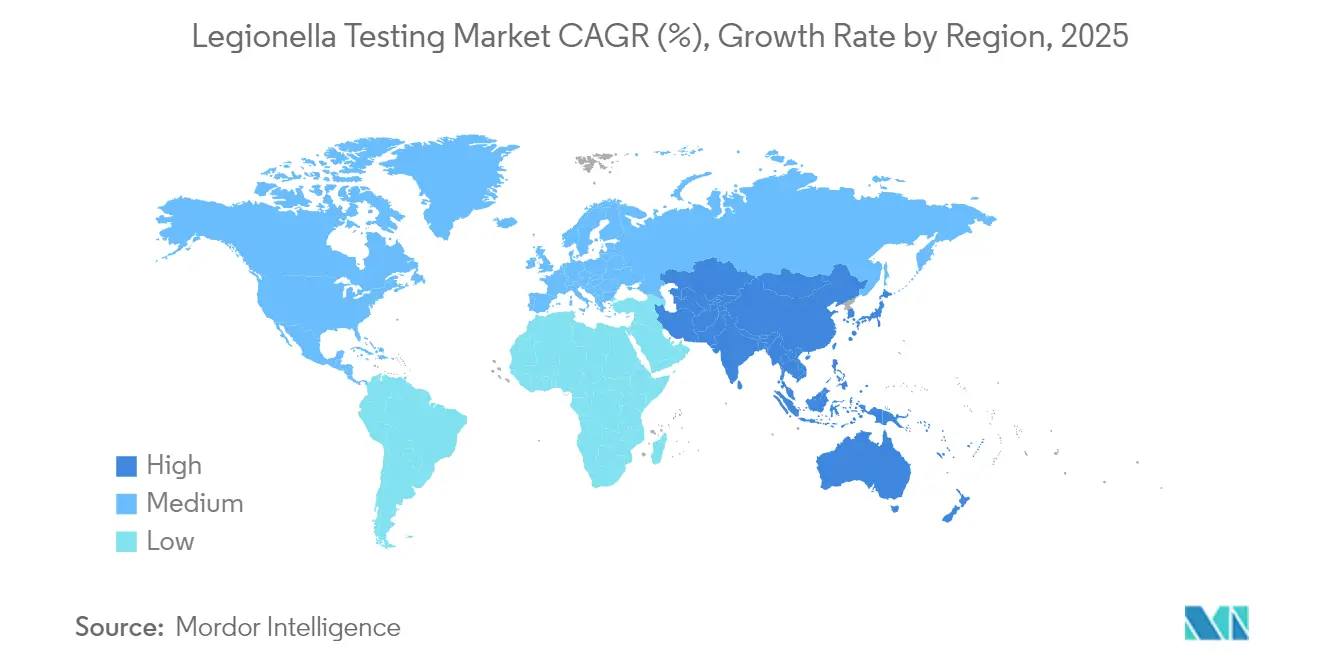

- By geography, North America contributed 43.00% revenue in 2025, while Asia-Pacific is expected to expand at a 9.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Legionella Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of pneumonia & Legionella-linked illness | +1.8% | Global urban centers | Medium term (2-4 years) |

| Increasing demand for rapid & advanced diagnostics | +2.1% | North America & Europe; expanding APAC | Short term (≤ 2 years) |

| Technological innovations in molecular & IMS methods | +1.5% | Developed markets worldwide | Long term (≥ 4 years) |

| Stricter building-water regulations & ASHRAE-188 adoption | +2.3% | North America; spreading globally | Medium term (2-4 years) |

| Post-COVID re-occupancy of buildings elevating risk | +1.2% | Global commercial properties | Short term (≤ 2 years) |

| Insurance carriers mandating Legionella risk audits | +0.9% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Pneumonia and Legionella-Linked Illness

Reported U.S. Legionnaires’ disease cases tripled from 2000-2011 and have continued climbing through 2024, a pattern mirrored in several OECD countries. Melbourne’s 2024 outbreak produced 77 cases, 75 hospitalizations, and 2 deaths, underscoring how rapidly contaminated aerosols can infect dense urban populations. With mortality in severe cases ranging from 20-40%, health systems recognize that routine surveillance lowers overall treatment costs. Employers also see productivity savings when preventive testing keeps staff from illness. Consequently, sustained epidemiological pressure is translating into baseline demand for both clinical and environmental testing.

Increasing Demand for Rapid and Advanced Diagnostics

Clinicians seek actionable results within 24 hours; culture’s 7-14-day lag is now viewed as clinically unacceptable for severe pneumonia management. PCR platforms provide same-day answers with 99.95% negative predictive value at clinically relevant thresholds. Post-COVID facility re-openings exposed stagnant pipes that intensified bacterial growth, accelerating adoption of rapid molecular panels. Environmental managers likewise favor quick tests so they can adjust disinfection protocols before bacteria levels cross regulatory limits. The push for turnaround times under 48 hours therefore remains a defining feature of the Legionella testing market.

Technological Innovations in Molecular and IMS Methods

Droplet digital PCR detects very low Legionella concentrations that evade conventional assays, improving early-warning reliability in large plumbing networks. Immunomagnetic separation distinguishes viable from non-viable cells, sharpening risk assessments when biocides create cellular debris that would otherwise yield false positives[2]Frontiers in Microbiology, “Advances in Immunomagnetic Separation for Legionella Detection,” frontiersin.org. LAMP paired with lateral-flow strips now delivers field-deployable results in 75 minutes, expanding testing to cooling towers and fountains without lab infrastructure. AI-driven image analytics and automated sample preparation further cut technician time and error rates. Collectively, such innovations enhance sensitivity while lowering per-sample hands-on time.

Stricter Building-Water Regulations and ASHRAE-188 Adoption

ASHRAE-188 turned voluntary guidelines into enforceable codes, reaching more than 5 million U.S. buildings by 2025. The 2024 release of ANSI/ASHRAE-514 imposed facility-wide hazard analyses for hospital water, making quarterly Legionella testing routine. European Union member states have started aligning risk-assessment rules with these U.S. precedents. Insurance underwriters now factor Legionella compliance into premiums, further incentivizing program adoption. The result is a predictable, recurring revenue stream for qualified testing providers.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-optimal sensitivity/specificity of legacy tests | -1.4% | Global cost-sensitive markets | Medium term (2-4 years) |

| High cost of PCR/qPCR & ddPCR panels | -2.1% | Emerging markets; smaller facilities | Short term (≤ 2 years) |

| Fragmented global compliance standards increase burden | -1.3% | Global | Medium term (2-4 years) |

| Litigation risk from PCR false positives hindering uptake | -1.0% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sub-Optimal Sensitivity and Specificity of Legacy Tests

Culture yields 70-90% sensitivity depending on sample type and requires repeat sampling when non-Legionella flora overgrow plates. Urinary antigen assays detect only L. pneumophila serogroup 1, missing the 8-30% of cases caused by other serogroups. Each missed detection invites continued exposure and potential litigation, yet budget-limited facilities still opt for these older methods. Widespread reliance on legacy tests therefore slows universal migration to faster, broader-spectrum diagnostics.

High Cost of PCR/qPCR and ddPCR Panels

PCR workstations cost USD 50,000–200,000 and reagents run USD 15–50 per test; culture plates cost USD 5–15. Budget-constrained hospitals and small labs often postpone molecular upgrades despite recognized performance gains. Quality-assurance protocols, personnel training, and maintenance contracts add hidden expenses. Reimbursement gaps in several national health systems leave providers bearing most of the incremental cost, limiting uptake in emerging economies and rural areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Rapid PCR Drives Molecular Shift

PCR/qPCR/ddPCR platforms captured 42.20% Legionella testing market share in 2025 because hospitals value 24-hour turnaround when treating severe pneumonia. Within the USD 377.52 million Legionella testing market size logged in 2025, PCR assays generated the largest revenue slice by combining high sensitivity with broad serotype coverage. Laboratories also rely on molecular methods to validate water treatment efficacy faster than culture. Culture remains essential for viability confirmation and antimicrobial susceptibility, but its use is shifting toward confirmatory rather than frontline testing. Direct fluorescent antibody staining fills immediate visualization niches yet accounts for a modest revenue contribution. Urinary antigen tests lead growth at a 10.41% CAGR by offering 15-minute point-of-care results that support emergency-department triage decisions. Technology refinements have pushed UAT sensitivity past 95%, and multiplex versions now detect several Legionella species in a single cartridge. As reagent costs fall, UAT kits are penetrating occupational health programs and cruise-ship medical units. Market participants therefore maintain balanced portfolios that cover both rapid molecular and decentralized antigen formats to maximize reach across diverse end-user budgets.

Second-generation ddPCR instruments are expected to erode culture share further by identifying sub-detectable colony counts in large plumbing systems. Field technicians equipped with portable LAMP-lateral-flow kits can now screen spa water during routine maintenance visits, creating new revenue lines for HVAC and water-treatment contractors. Although reagent pricing remains higher than agar media, volume purchasing and reagent rental contracts are narrowing the gap, especially for regional reference labs processing thousands of samples weekly. Over the forecast period, technology convergence will likely see labs combine ddPCR quantification with culture confirmation in a single workflow, cementing molecular dominance across the Legionella testing market.

By End User: Compliance Culture Sustains Laboratory Outsourcing

Hospitals and clinics accounted for 49.00% revenue in 2025, reflecting CMS mandates that tie funding to ASHRAE-aligned water management. Facilities employ a layered strategy of routine water sampling, high-risk patient screening, and post-remediation confirmation to minimize liability. Constant construction, aging piping, and immunocompromised wards amplify testing frequency inside acute-care environments, locking in a large share of recurring demand. Nevertheless, many community hospitals outsource work to commercial reference labs rather than investing in on-site molecular instruments. That shift pushes diagnostic laboratories toward the fastest growth trajectory at an 11.38% CAGR through 2031.

National and regional lab chains leverage economies of scale, ISO 17025 accreditation, and courier networks to deliver two-day water-sample results at predictable prices. Bundled service contracts now combine Legionella testing with chemical parameter monitoring, giving property managers a single compliance partner. Outside healthcare, industrial facilities, hotels, and universities represent untapped potential as insurers and local codes impose more stringent control plans. Over the forecast horizon, integrated lab-plus-field sampling services are expected to attract smaller building operators unable to maintain dedicated water-safety staff, extending the Legionella testing market footprint into new verticals.

Geography Analysis

North America generated 43.00% of global revenue in 2025, underpinned by a robust regulatory network that spans CMS rules for healthcare, OSHA guidelines for workplaces, and insurer-driven audits for commercial property owners. Large diagnostic firms headquartered in the United States supply most PCR reagents, while hundreds of accredited laboratories offer same-day test logistics. Canada’s public-health agencies have mirrored U.S. standards, and Mexico’s private hospital expansions are aligning procurement policies accordingly. High litigation exposure also keeps routine testing budgets intact, even during broader healthcare cost pressures.

Asia-Pacific is the fastest-growing region at a 9.22% CAGR, propelled by urbanization and infrastructure investment. Japan’s Expo 2025 detected Legionella counts 50-times above safety limits, prompting nationwide awareness campaigns and stricter municipal codes. China’s hospital-building boom and India’s PPP hospital projects necessitate comprehensive water-safety plans that incorporate quarterly testing. Hong Kong’s cooling-tower surveillance, which analyzed 115 samples in July 2024 alone, showcases government-led vigilance. Australia’s state health departments continue to enforce monthly cooling-tower checks, setting a compliance example for Southeast Asian neighbors.

Europe presents a fragmented picture shaped by differing national laws and energy-conservation goals. Germany’s high legionellosis incidence has moved laboratories toward the IDEXX Legiolert method, regarded as more sensitive than ISO plates. France continues to subsidize UAT kits for nursing homes, whereas the United Kingdom mandates quarterly risk assessments under HSE guidance. Green-building initiatives sometimes reduce hot-water storage temperatures, requiring sophisticated control strategies that maintain energy efficiency without fostering bacterial growth. Testing providers capable of navigating multiple regulatory frameworks enjoy a competitive edge across the European Union.

Regulatory Landscape

Legionella testing demand is anchored in enforceable rules and widely adopted standards that translate water-safety plans into recurring sampling, verification, and documentation. In the United States, healthcare compliance is reinforced by Centers for Medicare & Medicaid Services requirements tied to ASHRAE-aligned water management programs, while CDC guidance provides a structured toolkit for routine testing decisions across building-water systems. In August 2024, the US Environmental Protection Agency finalized guidance and test methods for antimicrobial products used in cooling-tower water to control planktonic L. pneumophila, adding more emphasis on quantifiable efficacy claims and the supporting monitoring evidence.

Across Europe, the regulatory picture combines workplace safety guidance and drinking-water requirements. The EU Drinking Water Directive (Directive (EU) 2020/2184) includes Legionella monitoring in risk-based water quality management with a target value referenced in the directive annexes, which pushes public and private operators toward documented surveillance. In the UK, the Health and Safety Executive guidance directs that water samples be analyzed by UKAS-accredited laboratories, typically referencing established methods and standards (for example BS 7592 and culture-based approaches aligned with ISO 11731:2017 as a widely used international baseline). This supports demand for accredited laboratory services and standardized reporting formats.

Competitive Landscape

The legionella testing market shows moderate fragmentation, with molecular-biology multinationals competing alongside niche water-safety specialists. bioMérieux, Thermo Fisher Scientific, and Qiagen exploit broad reagent catalogs and automated PCR platforms to serve hospital laboratories worldwide. IDEXX Laboratories targets environmental customers with the Legiolert method, while Phigenics sells combined consulting and testing packages that help property owners draft ASHRAE-compliant plans. Market rivalry is increasingly technology-centric: companies race to launch faster assays, cloud-based data dashboards, and automated sampling robots that collect pipe biofilm without technician exposure.

Vertical integration is gaining momentum. Ecolab’s November 2024 purchase of Barclay Water Management added proprietary iChlor monochloramine systems to its testing services, positioning the firm as a one-stop water-safety supplier. Similar moves are expected as treatment firms acquire diagnostics players to secure recurring reagent revenue. Start-ups are also active, offering smartphone-linked biosensors that push real-time alerts to building managers. Large diagnostic houses respond by embedding AI-powered interpretation into instrument software, reducing the skill threshold for lab operators.

Price competition remains muted for premium molecular tests, where intellectual-property protection and regulatory approvals create entry barriers. In contrast, commoditized culture media see tighter margins, prompting vendors to bundle consumables with technical support. Regional laboratories differentiate through ISO accreditation, fast courier pick-ups, and customizable reporting formats that feed data directly into client compliance dashboards. Over the forecast period, laboratories that pair high-throughput ddPCR capacity with consulting services are likely to consolidate share, especially in regions adopting stringent water-management legislation.

Legionella Testing Industry Leaders

Thermo Fisher Scientific Inc.

BioMérieux SA

Becton, Dickinson and Company

Aquacert Ltd

Qiagen NV

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Faster environmental decision-making is tightening the gap between sampling and corrective action, while still relying on accredited laboratory confirmation. The market already reflects a shift toward rapid molecular workflows (PCR/qPCR/ddPCR leading test-type revenue share in 2025) alongside field-deployable formats. That combination creates space for providers that bundle on-site screening with confirmatory ISO-aligned laboratory testing and compliance documentation for hospitals, long-term care, hotels, and industrial sites managing large plumbing and cooling-tower networks. CDC water management toolkit modules and UK HSE guidance support structured routine testing and monitoring practices, which helps service models integrate sampling logistics, chain-of-custody handling, and standardized reporting across building portfolios.

Opportunities also come from under-detection and diagnostic bias tied to legacy approaches that miss non-pneumophila Legionella or provide limited serogroup coverage, pushing clinical and environmental stakeholders toward broader panels and species-level resolution. Recent product activity indicates continued investment in the consumables and workflow layer of Legionella testing: in March 2026, AnalytiChem launched Redipor Legionella selective agar plates designed to support ISO 11731-compliant workflows, supporting labs scaling culture confirmation and outbreak investigations. Emerging rapid on-site tools and ongoing molecular method refinements, including newer sequencing approaches discussed in current literature, expand addressable use cases for screening and surveillance, while accreditation and method harmonization remain central buying criteria for regulated end users.

Recent Industry Developments

- March 2026: AnalytiChem launched a new range of Redipor Legionella selective agar plates designed to support ISO 11731-compliant workflows. The release targets laboratories that need standardized culture media for routine monitoring and confirmatory testing alongside rapid methods. It also strengthens the consumables supply layer as facilities maintain regular sampling cycles driven by building-water programs.

- April 2025: bioMerieux launched the WATCHFIRE molecular testing solution, including the WATCHFIRE Respiratory (R) Panel for detecting pathogens in wastewater, expanding into environmental surveillance. The move extends molecular infrastructure that can be applied across environmental monitoring use cases beyond traditional clinical diagnostics. It also indicates continued investment in data-centric, molecular workflows aligned with faster turnaround requirements.

- November 2024: Ecolab acquired Barclay Water Management, adding continuous digital monitoring and monochloramine generation technology (including iChlor systems) to its water-safety portfolio. Combining treatment capabilities with monitoring and program services supports integrated offerings for building-water risk management. The deal increased competitive pressure on standalone testing and consulting providers by strengthening a one-stop compliance partner model.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from legionella testing done on water and clinical samples, including laboratory services plus the kits and consumables used to detect Legionella species.

Scope exclusions: Revenue from water system remediation, disinfection services, and sensor-based real-time monitoring devices is excluded from our sizing.

Segmentation Overview

- By Test Type

- Culture Method

- Urinary Antigen Test (UAT)

- Direct Fluorescent Antibody (DFA)

- Polymerase Chain Reaction (PCR/qPCR/ddPCR)

- Other Test Types

- By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer frame of demand and to understand the regulatory triggers that keep testing cycles active in buildings and care facilities. We referenced public sources such as the US Centers for Disease Control and Prevention (surveillance and guidance), the US Environmental Protection Agency (water system context), the World Health Organization (water safety guidance), and standards bodies that publish water management and testing practices.

To turn these signals into workable inputs, we also reviewed company annual reports, investor presentations, product literature, and reputable press articles that describe method adoption and lab workflows. Where needed, paid subscriptions for company financials and news intelligence were used to confirm business lines and geographic exposure, and patent databases were used to track test-method activity over time. These desk sources are illustrative, and additional public sources were also consulted for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on validating which legionella testing methods are actually purchased, how often sampling is repeated, and how pricing behaves across routine monitoring versus outbreak-driven testing. We spoke with a mix of laboratories, test-kit and consumables suppliers, facility water safety stakeholders, and channel participants across major regions so the assumptions could be stress-tested and corrected where gaps showed up.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 50% |

| Mid tier: 54% | Functional/Unit leaders: 30% | EMEA: 29% |

| Smaller Players: 14% | Managers: 58% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing starts with a top-down build where outbreak incidence, building water management adoption, and testing frequency patterns are translated into an addressable testing demand pool, which is then valued using method-level pricing logic. Since public data can be uneven by country, totals were corroborated with selective bottom-up approximations like sampled lab throughput checks and supplier-side volume indicators, and then adjusted where gaps were repeatedly flagged.

Key inputs were treated as practical drivers including the split between environmental and clinical testing, the mix of culture versus rapid methods (for example UAT and PCR), typical re-test intervals for high-risk facilities, the share of outsourced lab testing versus in-house capacity, and ASP movements for kits and consumables as volumes scale. Forecasts were built using scenario analysis, because regulation intensity and adoption of faster molecular tests can shift quickly by region. Experts helped set realistic ranges for each driver before the final trend line was chosen. When a bottom-up cross-check could not be built for a smaller geography, proxy ratios from similar markets were applied and then sanity-checked against population, facility stock, and lab network maturity.

Data Validation & Update Cycle

Outputs are validated through several checks so the final totals do not rely on one data stream. We compare model results against independent signals such as method adoption direction, regional testing cycle requirements, and observable shifts in lab service activity, and then anomalies are reworked until the variance is explainable. A second analyst review is completed before sign-off, and follow-up calls are triggered when an assumption drives an outlier result.

The report is refreshed annually, and interim updates are added when material events occur, such as major guideline changes or step shifts in test-method uptake. Before delivery, a final freshness pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Legionella Testing Market Sizing Compared With Other Published Estimates

Published market sizes for legionella testing can look close at first glance, but they still differ because firms do not count the same revenue lines and they do not apply the same test-mix and pricing assumptions. Timing also matters, since base-year exchange rates, inflation handling, and method adoption updates can shift totals even when the end market sounds identical.

The main gap comes from whether adjacent water safety activities are counted, where Mordor Intelligence only counts diagnostic kits, consumables, and laboratory testing services, and leaves out remediation work and sensor-based monitoring devices. Differences also come from how culture testing versus rapid methods are weighted, whether routine building monitoring is valued using repeat sampling cycles or a one-time event view, and how regional price differences are applied when converting local revenues into USD.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 377.52 M (2025) | |

| Global Consultancy A | USD 369.90 M (2025) | Uses a slightly lower 2025 base that appears to smooth pricing and method mix across regions, which can understate higher-cost compliance testing cycles in mature markets. |

| Industry Publisher B | USD 379.30 M (2025) | Builds a similar total-year view but may apply a faster shift toward premium rapid methods in the base year, which can lift revenue even if test volumes are comparable. |

The spread in the table is explained mostly by scope edges and by how method mix and pricing are handled in the base year. By keeping assumptions tied to observable testing cycles, method usage patterns, and region-level pricing checks, our estimate stays traceable to clear steps that can be repeated during updates.

Key Questions Answered in the Report

What is the current size of the Legionella testing market?

The Legionella testing market was valued at USD 407.94 million in 2026 and is projected to grow at an 8.06% CAGR to 2031.

Which test method generates the largest revenue?

PCR-based molecular diagnostics hold 42.20% Legionella testing market share because they deliver results within 24-48 hours.

Which region is expanding fastest?

Asia-Pacific is forecast to grow at a 9.22% CAGR through 2031, driven by new building construction and heightened public-health oversight.

Why are diagnostic laboratories growing so quickly?

Outsourcing by smaller hospitals and commercial properties supports an 11.38% CAGR for specialized laboratories that offer high-throughput molecular testing.

What regulations drive demand in the United States?

CMS requires healthcare facilities to implement ASHRAE-compliant water-management plans, which mandate routine Legionella testing for compliance.

How are technology trends influencing test choices?

Advances such as droplet digital PCR and LAMP-lateral-flow kits are reducing turnaround times and detecting lower bacterial counts, prompting many facilities to upgrade from legacy culture methods.

Page last updated on: