Escherichia Coli Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

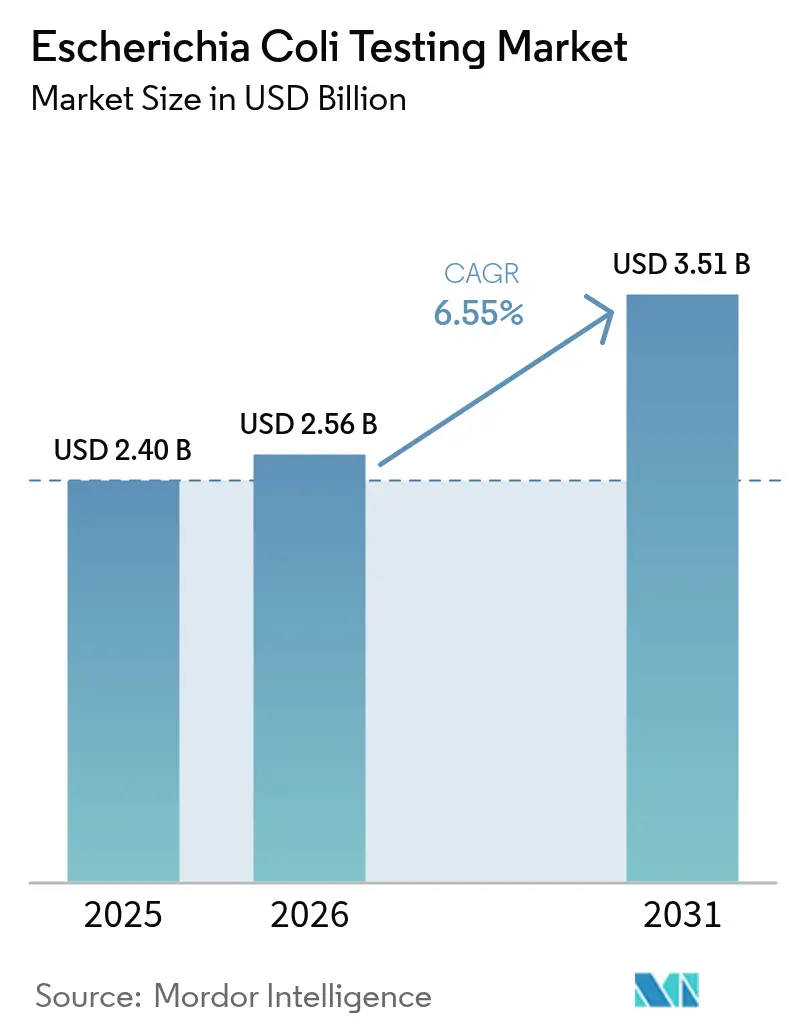

| Market Size (2026) | USD 2.56 Billion |

| Market Size (2031) | USD 3.51 Billion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Escherichia Coli Testing Market Analysis by Mordor Intelligence

Escherichia Coli Testing market size in 2026 is estimated at USD 2.56 billion, growing from 2025 value of USD 2.40 billion with 2031 projections showing USD 3.51 billion, growing at 6.55% CAGR over 2026-2031. Market expansion benefits from stricter food-borne outbreak surveillance, rising water-quality monitoring, and clinical adoption of rapid molecular diagnostics. Growth also reflects investment in portable biosensor platforms that shorten time-to-result, as well as AI-enhanced culture workflows that automate colony enumeration. While capital requirements for fully automated PCR workstations temper near-term demand among smaller laboratories, continued regulatory tightening and antimicrobial-resistance monitoring offset this restraint. The Escherichia Coli Testing market therefore demonstrates resilient momentum as users transition from culture-based techniques toward integrated molecular and digital solutions.

Key Report Takeaways

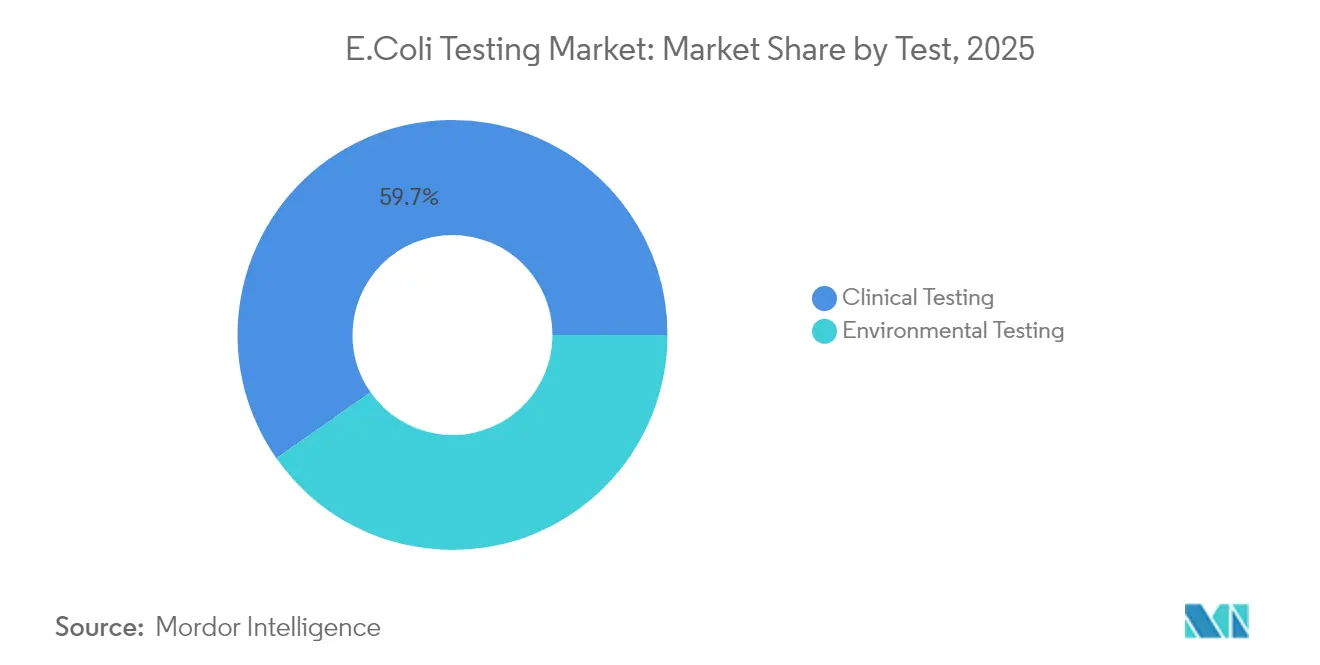

- By application, clinical testing held 59.72% of Escherichia Coli Testing market share in 2025; food and beverage testing is projected to grow at a 10.02% CAGR to 2031.

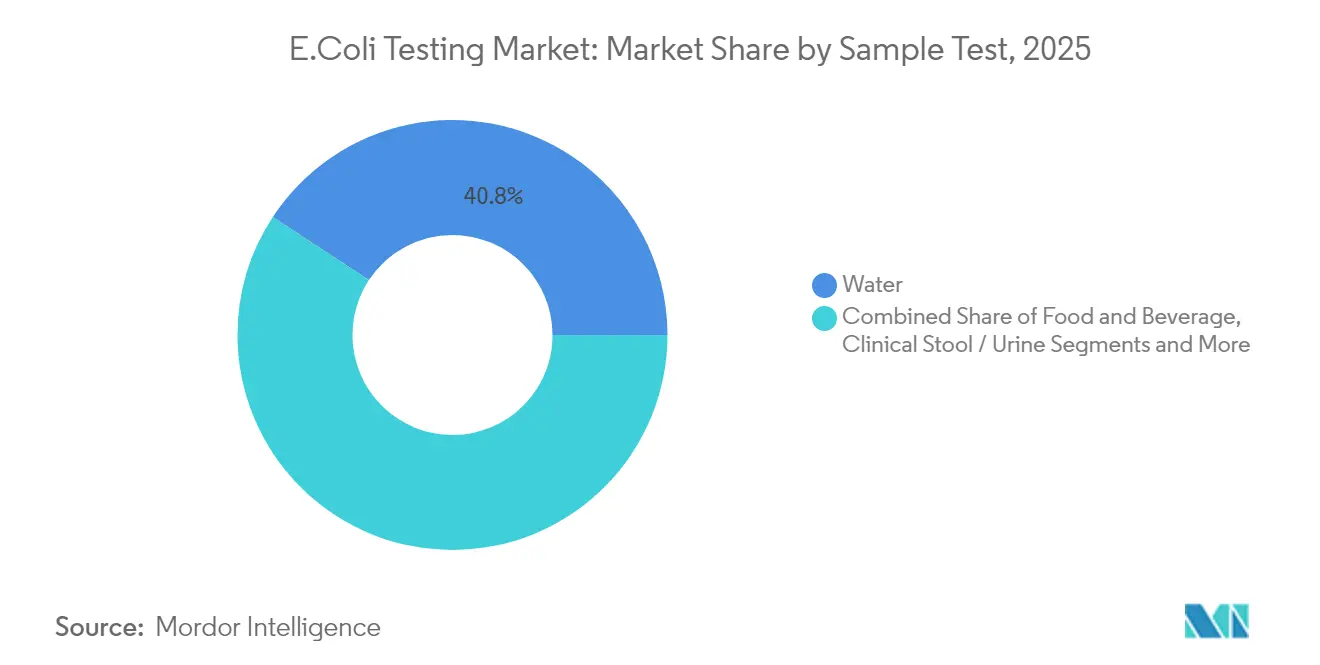

- By sample type, water testing accounted for 40.75% of the Escherichia Coli Testing market size in 2025, while food and beverage samples represent the fastest-growing category at 10.02% CAGR.

- By end user, diagnostic laboratories commanded 32.98% of the Escherichia Coli Testing market in 2025; water utilities and wastewater plants are expanding at an 8.54% CAGR through 2031.

- By geography, North America led with 37.12% revenue share in 2025; Asia Pacific is forecast to record the highest regional CAGR of 8.92% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Escherichia Coli Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multiplex molecular PCR panels | +1.8% | Global, early uptake in North America and EU | Medium term (2-4 years) |

| Food-borne outbreak surveillance mandates | +1.2% | Global, stringent in North America and EU | Short term (≤ 2 years) |

| Decentralized water-quality testing at utilities | +1.0% | Core demand in Asia Pacific, spill-over to MEA | Medium term (2-4 years) |

| Livestock antimicrobial-resistance monitoring | +0.8% | Global, focus on EU and North America | Long term (≥ 4 years) |

| Portable biosensor-on-chip innovations | +0.6% | Global, early gains in developed markets | Long term (≥ 4 years) |

| AI-augmented image analytics in culture media | +0.4% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Molecular-PCR Adoption for Multiplex Diarrheal Panels

Healthcare networks are moving from single-pathogen assays to multiplex panels that detect several gastrointestinal organisms in a single test, cutting diagnostic time from days to hours. Platforms such as the FilmArray GI panel provide results for 22 pathogens, including E. coli O157, within 1 hour, allowing physicians to tailor therapy quickly. Artificial intelligence further refines specificity by distinguishing true positives from background noise, and studies show hospital stays fall when rapid PCR replaces culture. The trend supports premium pricing, particularly in emergency departments where rapid answers improve antimicrobial stewardship.[1]Siu-Tung Yau, “Rapid Diagnosis of Bloodstream Infections Using a Culture-Free Phenotypic Platform,” Nature Communications Medicine, nature.com

Food-Borne Outbreak Surveillance Mandates

Revisions to the Food Safety Modernization Act, effective July 2024, compel stronger pre-harvest agricultural water testing. High-profile incidents, such as the 2024 fast-food outbreak, triggered adoption of on-site, portable assays so processors verify cleanliness before distribution. Automated systems capable of analysing diverse matrices enable compliance while controlling costs, and AI-driven risk models prioritise sampling based on weather and historical contamination patterns.[2]Food and Drug Administration, “Standards for the Growing, Harvesting, Packing, and Holding of Produce for Human Consumption Relating to Agricultural Water,” Federal Register, federalregister.gov

Growth in Decentralized Water-Quality Testing at Utilities

Updated EPA Clean Water Act methods endorse modified membrane filtration and molecular detection, allowing utilities to shift from batch culture to near-real-time monitoring. Integration of IoT sensors with lab automation delivers predictive analytics for treatment optimisation, while membrane bioreactors linked to AI achieve energy-positive operations.[3]Environmental Protection Agency, “Clean Water Act Methods Update Rule for the Analysis of Effluent,” Federal Register, federalregister.gov

Expansion of Livestock AMR Monitoring Programs

One Health policies encourage coordinated antibiotic-resistance surveillance, expanding E. coli testing in feed and livestock. Field-deployable LAMP assays now detect resistance genes without complex equipment, supporting precision agriculture that adjusts antibiotic use in real time.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital intensity of fully automated PCR work-cells | -1.4% | Global, affecting smaller labs | Short term (≤ 2 years) |

| Reagent stock-outs in low-resource public labs | -0.8% | Asia Pacific and MEA, rural spill-over worldwide | Medium term (2-4 years) |

| Regulatory lag in validating next-gen microfluidics | -0.6% | Global, timelines vary by region | Medium term (2-4 years) |

| False-positive inflation from matrix inhibitors | -0.4% | Global, prominent in complex samples | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital Intensity of Fully Automated Stool PCR Work-Cells

Acquiring an end-to-end stool PCR robot costs between USD 500,000 and USD 2 million. Beyond purchase price, facilities must add dedicated space, ventilation, and backup power. Smaller diagnostic centres struggle to justify investment given limited volumes and ongoing maintenance.

Reagent Stock-Outs in Low-Resource Public Labs

Public-sector labs often depend on imported proprietary reagents. Procurement delays and currency constraints cause months-long supply gaps that halt molecular testing. Diversifying platforms increases resilience but raises costs. Local reagent production can help, yet must still pass regulatory review.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test: Diagnostic Focus Spurs Molecular Innovation

Escherichia Coli Testing market data show clinical applications held 59.72% share in 2025, and this segment is forecast to advance at 9.12% CAGR through 2031. Polymerase chain reaction remains the workhorse in hospitals because it returns results within hours and detects low bacterial loads. The Escherichia Coli Testing market size for clinical PCR solutions continues to rise as stool and urine diagnostics expand beyond tertiary centres into urgent-care clinics. LAMP kits, which operate at a single temperature, appeal to point-of-care sites where instrumentation budgets are constrained. Enzyme immunoassays still serve cost-sensitive programs, but their share erodes as molecular platforms become cheaper per test.

Environmental assays, spanning water, soil, and wastewater matrices, rely on membrane filtration for regulatory reporting, yet demand for automated enzyme-substrate methods grows where rapid decisions are required. Chromogenic culture media now visualise suspect colonies within 24 hours, trimming confirmation cycles. Rapid biosensor-based tests hold the highest incremental growth because they combine nanostructured surfaces with microfluidics, delivering results in minutes for on-site responders. This shift positions the Escherichia Coli Testing market to embrace hybrid workflows that blend culture validation with molecular speed.

By Sample Type: Water Dominates Volume while Food Safety Accelerates

Water made up 40.75% of total test volume in 2025, reflecting long-standing regulation that treats E. coli as a sentinel for faecal contamination. Utilities deploy online monitors tied to supervisory-control systems that trigger real-time disinfection adjustments. At the same time, food and beverage testing posts the fastest 10.02% CAGR, a sign that brand owners cannot risk recall costs. The Escherichia Coli Testing market share for food producers expands as regulations now require pre-harvest water checks and finished-product release holds.

Clinical specimens maintain stable demand for differential diagnosis of diarrhoeal disease, while livestock samples grow due to antimicrobial-resistance surveillance. Manufacturers compete by creating universal extraction kits that accommodate water turbidity, fatty food matrices, and faecal solids in one workflow. Standardising across matrices lowers operator training demands and widens adoption of integrated instruments.

By End User: Labs Lead but Utilities Climb

Diagnostic laboratories captured 32.98% of revenue in 2025, benefiting from established quality-management systems that facilitate rapid uptake of new chemistry. Consolidation among national chains increases purchasing power for high-throughput PCR lines, yet decentralisation trends push innovation toward portable devices for community clinics. Water utilities, advancing at 8.54% CAGR, invest in continuous monitoring to comply with updated effluent standards. Hospitals turn to point-of-care cartridges that cut emergency-department turnaround by hours, supporting prompt antimicrobial therapy.

Food processors upgrade to automated sampling robots that integrate hazard analysis critical control point workflows. Government agencies remain steady buyers for outbreak investigation, though budgets fluctuate. Cloud-based data portals let smaller utilities and regional labs access analytics once limited to large corporations, broadening Escherichia Coli Testing market penetration into underserved settings.

Geography Analysis

North America held 37.12% of Escherichia Coli Testing market revenue in 2025 owing to robust EPA and FDA mandates that require routine testing across drinking water and produce supply chains. AI-ready culture imagers and fully automated PCR work-cells see strong uptake in the United States as laboratories chase productivity gains and tighter turnaround targets. The 2024 FDA Laboratory Developed Tests rule raises the compliance bar, favouring companies with established quality systems.

Asia Pacific posts the highest 8.92% regional CAGR through 2031, driven by rapid urbanisation and investments in water infrastructure. Low-cost membrane filtration kits and smartphone-enabled biosensors close testing gaps in peri-urban areas. Governments in India and Southeast Asia add water testing to smart-city programs, while China’s five-year plan prioritises safe food supply chains, boosting demand for high throughput immunoassay lines. Regional reagent manufacturing lowers freight and cold-chain costs, further fuelling Escherichia Coli Testing market growth.

Europe maintains steady contribution, supported by stringent food and water directives and a mature network of accredited laboratories. The region’s focus on sustainability drives adoption of energy-positive water treatment combined with continuous microbial monitoring. Collaborative projects like the bioMérieux-Illumina agreement illustrate Europe’s leadership in next-generation sequencing surveillance, merging epidemiological insight with routine testing.

The Middle East and Africa represent emerging frontiers where infrastructure investment and donor-funded public-health programs underpin incremental market demand, particularly for portable kits capable of withstanding high ambient temperatures and intermittent power.

Regulatory Landscape

In the United States, E. coli testing demand is shaped by food, drinking-water, and clinical IVD oversight. FDA revisions to the Food Safety Modernization Act agricultural-water requirements, effective July 2024, increased emphasis on pre-harvest water assessment and use of generic E. coli results for risk management decisions in produce supply chains. In clinical testing, the FDA final rule on Laboratory Developed Tests (LDTs) took effect July 5, 2024, with a staged, multi-year phaseout of enforcement discretion that began with Stage 1 on May 6, 2025, raising compliance and documentation requirements for laboratories that historically relied on in-house assays.

In Europe, Regulation (EU) 2017/746 (IVDR) continues to tighten market access pathways for higher-risk IVDs, including more stringent conformity assessment expectations for Class D assays via notified bodies and, where applicable, EU reference laboratory involvement. Standardization is also advancing in food-chain microbiology and molecular methods, with ISO 7218:2024 (general requirements for microbiological examination of the food chain) published in June 2024 and ISO 24914:2026 (requirements for LAMP in pathogen detection in the food chain) published in January 2026. These publications support harmonized validation approaches across laboratories and manufacturers.

Value Chain Analysis

The value chain for E. coli testing spans assay and consumable inputs (primers/probes, enzymes, antibodies, chromogenic substrates, membranes, culture media, and sample-prep plastics), instrument and software platforms (PCR and isothermal amplification systems, culture readers/imagers, and automation), method validation and quality systems, and downstream distribution via direct sales, national distributors, and laboratory procurement frameworks. Demand is executed primarily through diagnostic laboratories, hospitals and clinics, food processors and contract testing labs, and water utilities and wastewater plants, with surveillance programs creating recurring volumes and driving requirements for traceability, proficiency testing, and data reporting.

Recent evidence highlights operational dependencies and bottlenecks that affect testing availability and continuity. Supply-chain assessments in South and Southeast Asia point to long procurement lead times for equipment and sustained resupply cycles for reagents, with customs clearance and duty/tax complexity extending deployment timelines. Separately, laboratories have shown vulnerability to essential consumable shortages, illustrated by workflow disruptions linked to the 2024 global shortage of BD BACTEC blood culture bottles that forced temporary shifts to manual alternatives. This reinforces multi-vendor sourcing, validated contingency workflows, and local stocking strategies as key procurement and distributor priorities for E. coli testing.

Competitive Landscape

The Escherichia Coli Testing market is moderately fragmented. Global leaders such as Abbott, Thermo Fisher, bioMérieux, and Roche rely on scale, broad reagent portfolios, and regulatory expertise to defend share. Roche’s USD 350 million purchase of LumiraDx’s point-of-care platform adds multi-assay capability in primary care, underscoring the push toward decentralised diagnostics. Thermo Fisher enhances differentiation by embedding AI into culture readers, while Abbott leverages integrated immuno-PCR technology to broaden menu coverage.

Start-ups focusing on graphene biosensors and microfluidic cartridges challenge incumbents with ultrafast, low-volume tests. Many partner with automation specialists or cloud-analytics vendors to add value beyond consumables. Patent filings surge in nanopore detection, universal inhibitor-resistant chemistries, and sample-to-answer cartridges, signalling active innovation. Mid-tier firms pursue regional partnerships to penetrate high-growth Asia Pacific markets without heavy direct-sales investment. Competitive intensity is expected to rise as reimbursement frameworks begin recognising the clinical utility of rapid multiplex panels, allowing premium pricing that rewards innovation.

Escherichia Coli Testing Industry Leaders

Abbott Laboratories

BioMerieux Inc

Thermo Fisher Scientific

Becton, Dickinson and Company

Danahar

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven monitoring programs create clear whitespace for decentralized and faster time-to-result solutions across water and food testing, where users balance compliance, throughput, and field logistics. The FDA agricultural-water provisions effective July 2024 reinforce routine decision-making around generic E. coli indicators in produce supply chains. In the US, bottled water and drinking-water compliance frameworks keep E. coli as a critical trigger organism, supporting demand for quantitative methods and auditable workflows. These needs align with opportunities for portable systems that combine simplified sample preparation, rapid readouts, and digital recordkeeping for utilities, contract labs, and on-site food safety teams.

Technology pipelines also point to continued expansion of rapid molecular and biosensor modalities that can complement, or reduce reliance on, slower culture confirmation steps. In 2026, peer-reviewed work described multiple field-adaptable formats, including RPA-CRISPR lateral-flow assays for on-site multiplex pathogen detection and electrochemical biosensing approaches that apply machine learning to improve signal interpretation for E. coli O157:H7 screening. Separately, external quality assessment initiatives such as EQAsia continue to emphasize inter-laboratory comparability and proficiency, supporting adoption of standardized, kit-based workflows and data systems that reduce operator variability across decentralized testing networks.

Recent Industry Developments

- July 2026: R-Biopharm expanded its RIDA UNITY portfolio with E. coli Stool Panel I and III to differentiate pathogenic E. coli strains in a consolidated workflow. The addition strengthens syndromic stool testing menus for diagnostic laboratories seeking standardized, multi-target molecular panels without building separate in-house assays.

- November 2025: BD received FDA 510(k) clearance and CE-IVDR certification for high-throughput Enteric Bacterial Panels on the BD COR System, including targets relevant to Shiga toxin-producing E. coli and enterotoxigenic E. coli. Dual US and EU clearances support broader deployment in high-volume settings and add competitive pressure on integrated sample-to-answer enteric testing platforms.

- July 2024: bioMerieux reported that USDA-FSIS awarded the GENE-UP Pathogenic E. coli assay suite as a primary method for STEC detection in its laboratories. Selection by a national food-safety authority reinforces method credibility for processors and contract labs, and it can accelerate standardization around validated commercial assays in routine monitoring programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from testing solutions used to detect Escherichia coli in clinical, food, water, and environmental samples. It includes organism specific assays run through culture based methods, immunoassays, and molecular platforms, counted in value terms.

Scope exclusions: We exclude general microbiology systems and lab workflows where organism specific E. coli results are not reported.

Segmentation Overview

- By Test

- Clinical Testing

- Polymerase Chain Reaction (PCR)

- Loop-mediated Isothermal Amplification (LAMP)

- Enzyme Immunoassays (EIA/ELISA)

- Chromogenic Culture Media

- Rapid Biosensor-based Assays

- Environmental Testing

- Membrane Filtration

- Multiple Tube Fermentation

- Enzyme Substrate Method

- Clinical Testing

- By Sample Type

- Water

- Food & Beverage

- Clinical Stool / Urine

- Animal Feed & Livestock

- By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Water Utilities & Waste-Water Treatment Plants

- Food Processing Companies

- Government & Public-Health Agencies

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We first built a clean fact base around demand triggers and testing intensity, since E. coli testing spans public health programs, food safety monitoring, and water compliance. Public sources were used to understand outbreak burden, regulatory testing requirements, and typical lab workflows, then translated into realistic testing volumes and replacement cycles.

Sources we referred to included public health surveillance and outbreak reporting from agencies such as the US CDC, food safety and recall alerts from USDA and FDA, and drinking water and recreational water standards and monitoring references from the US EPA. We also reviewed guidance and method references from international bodies such as WHO, plus peer reviewed microbiology and diagnostics journals for changes in method adoption (culture, immunoassay, PCR) and time to result trends. To ground company presence and product footprints, we used annual reports, regulatory or method listings on official portals, reputable press, and patent databases, and we supplemented this with paid subscriptions for company financials and news intelligence where needed. These examples are not exhaustive, and we also used additional public sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Our primary work focused on the practical parts that desk sources do not fully explain, such as how often E. coli panels are run, what drives repeat testing, and how purchasing shifts between kits, reagents, and dedicated instruments. We spoke with a mix of diagnostic labs, food and beverage quality teams, water testing labs, and channel participants across APAC, EMEA, and the Americas, so assumptions on pricing and adoption could be checked for both routine and outbreak driven periods.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 12% | APAC: 47% |

| Mid tier: 59% | Functional/Unit leaders: 42% | EMEA: 32% |

| Smaller Players: 14% | Managers: 46% | Americas: 21% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where public health incidence, food testing frequency, and water monitoring programs are translated into a test demand pool, then applied to method mix and average selling price assumptions for kits, reagents, consumables, and dedicated instruments. Where the market is fragmented, we ran selective bottom-up checks using sampled product pricing, channel feedback on volumes, and a limited roll up of visible supplier revenues to see if totals stayed reasonable.

Key inputs included reported foodborne outbreak and recall patterns that can create testing spikes, routine water compliance testing cadence, clinical lab throughput and turnaround time needs, and the shift in mix between culture based workflows and faster molecular or immunoassay methods. Pricing was handled through a blended ASP curve that accounts for consumables share, instrument replacement cycles, and regional currency conversion timing. For forecasting, we used scenario analysis and then anchored it with expert views on regulation tightening, method adoption speed, and lab automation uptake, since those factors can change both test volumes and value per test. When country level bottom-up signals were thin, we used proxy indicators like lab density and compliance intensity, then normalized those estimates during the review step.

Data Validation & Update Cycle

We validate the model by comparing outputs with independent signals such as public testing mandates, outbreak reporting trends, and observed shifts in method adoption from labs and published guidance. Outliers are investigated at the country and application level, and assumptions are rechecked when a price, share, or volume change looks too steep versus the historical pattern.

Before sign-off, the work goes through multiple analyst reviews where key drivers, math logic, and conversion factors are re-tested. Follow-up calls are triggered when gaps remain in a high impact segment. The report is refreshed annually, and interim updates are made when material events occur, such as a major regulation change or a step change in testing practice. Right before delivery, a final pass is done so clients receive the latest view of market size and growth.

Mordor Intelligence's Escherichia Coli Testing Market Sizing Compared With Other Published Estimates

Published market numbers for E. coli testing often look different because the included revenue streams are not identical, and some studies treat outbreak related testing surges as a steady run rate. Differences also show up in how prices are blended across consumables and instruments, and whether clinical, food, and water testing are counted together.

The main gap comes from whether broad microbiology platforms and non specific pathogen workflows are included. Mordor Intelligence counts only assays and dedicated systems that report organism specific E. coli results across clinical, food, water, and environmental use. Another common driver is the base year and forecast window, since some estimates quote 2023 to 2024 values while others start later and reflect higher penetration of molecular methods. Currency conversion timing and how ASP erosion is modeled for mature consumables can also push totals up or down when the model is rolled across regions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.56 B (2026) | |

| Trade Publisher A | USD 2.30 B (2024) | Uses an earlier base year and appears to apply a broad test type view that can blend clinical and environmental volumes without clearly separating organism specific assays from general microbiology workflows, which can change the value mix and pricing averages. |

| Industry Analyst B | USD 1.94 B (2023) | Starts from a lower base year and frames the market around technology groupings, which can miss the uplift from later adoption of rapid methods and may not fully reflect the shift in spending toward higher frequency consumables in routine food and water compliance testing. |

The table shows that year choice and what is counted as an E. coli test solution are the biggest reasons the numbers spread. By tying the model to a defined demand pool across food, water, environmental, and clinical testing, then checking it with pricing and adoption inputs from field conversations, the final value stays traceable to clear steps that can be repeated each update cycle.

Key Questions Answered in the Report

What is the current size of the Escherichia Coli Testing market?

The market is valued at USD 2.56 billion in 2026.

How fast is the Escherichia Coli Testing market expected to grow?

It is projected to expand at a 6.55% CAGR, reaching USD 3.51 billion by 2031.

Which application segment leads revenue?

Clinical testing dominates with 59.72% share due to hospitals prioritising rapid PCR diagnostics.

Which region shows the highest growth potential?

Asia Pacific is forecast to post a 8.92% CAGR, driven by urbanisation and stricter water-safety enforcement.

What technology trends are reshaping the market?

Key shifts include multiplex PCR panels, portable graphene biosensors, and AI-enhanced culture-plate imaging.

Page last updated on: