Cobalt Alloy Powder Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

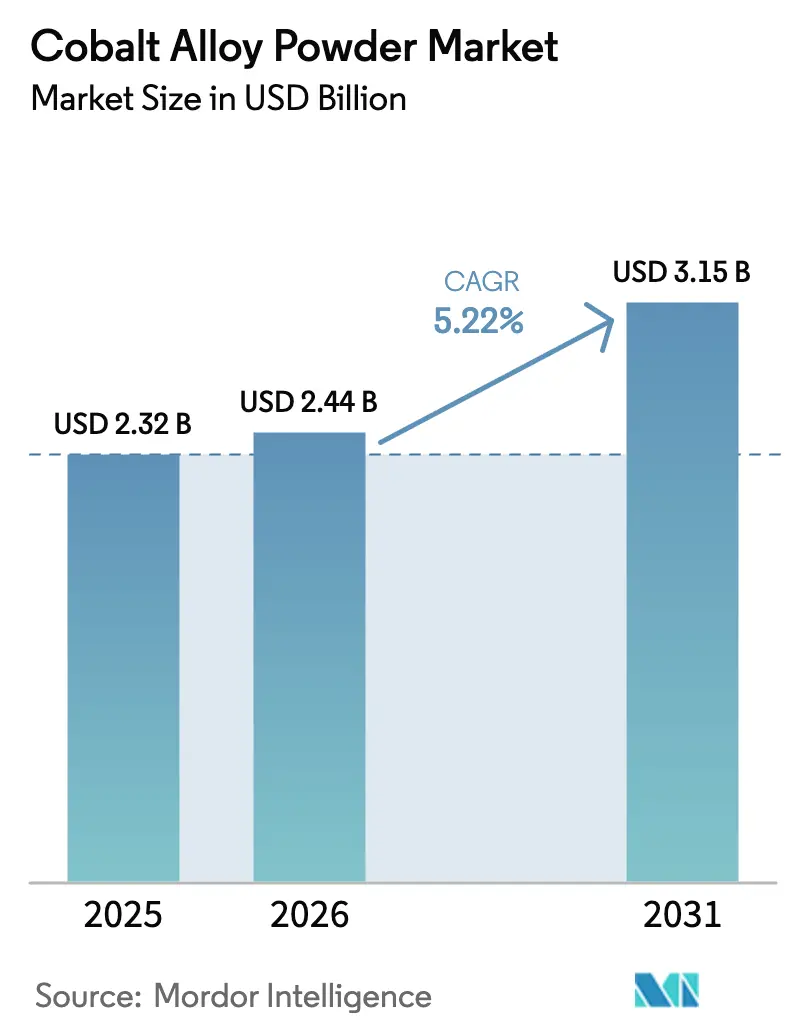

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cobalt Alloy Powder Market Analysis by Mordor Intelligence

The Cobalt Alloy Powder Market size was valued at USD 2.32 billion in 2025 and is estimated to grow from USD 2.44 billion in 2026 to reach USD 3.15 billion by 2031, at a CAGR of 5.22% during the forecast period (2026-2031). Producers with vertical integration have dominated the market for turbine hot-section parts, orthopedic implants, and wear-resistant tooling. They leverage captive atomization capacity, proprietary alloy chemistries, and secure multiyear contracts with aerospace and medical OEMs. Advances in plasma atomization, which achieve high sphericity and low oxygen levels, have facilitated the use of circular-economy feedstocks and larger powder bed fusion build envelopes. Meanwhile, Europe’s Critical Raw Materials Act and the Democratic Republic of Congo’s 2025 export ban have heightened raw-material risks. As a result, procurement has shifted toward Indonesian mixed hydroxide precipitate and certified recycled scrap. Although high-entropy alloys (HEAs) and AI-driven composition design present long-term competitive challenges, the decade-long qualification timelines have allowed established cobalt-chromium systems to retain their leadership position in the near term.

Key Report Takeaways

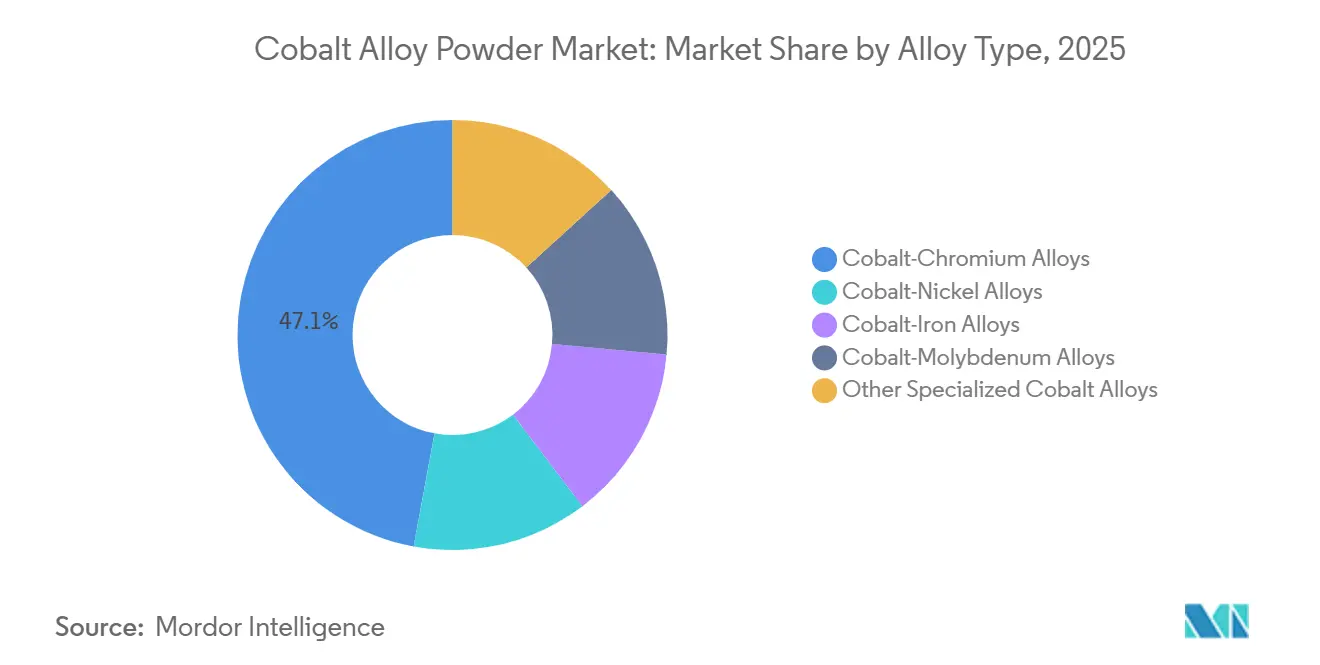

- By alloy type, cobalt-chromium commanded 47.11% of the cobalt alloy powder market share in 2025 and is growing fastest at 5.76% CAGR in the 2026 to 2031 period.

- By production method, atomization held 73.22% of the cobalt alloy powder market share in 2025 and is projected to expand at 6.03% CAGR in the 2026 to 2031 period.

- By application, additive manufacturing accounted for 32.56% of the cobalt alloy powder market size in 2025 and leads growth at 6.11% CAGR in the 2026 to 2031 period.

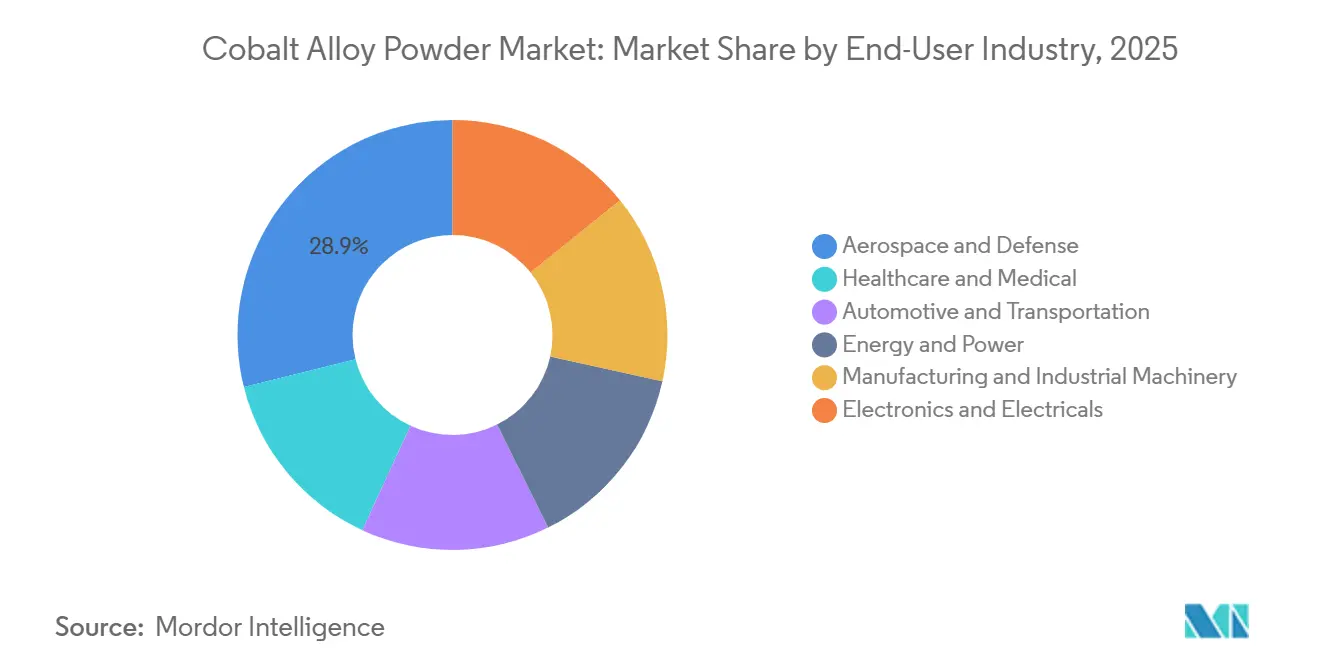

- By end-user industry, aerospace and defense generated 28.89% revenue in 2025 and shows the highest 6.12% CAGR between 2026 and 2031.

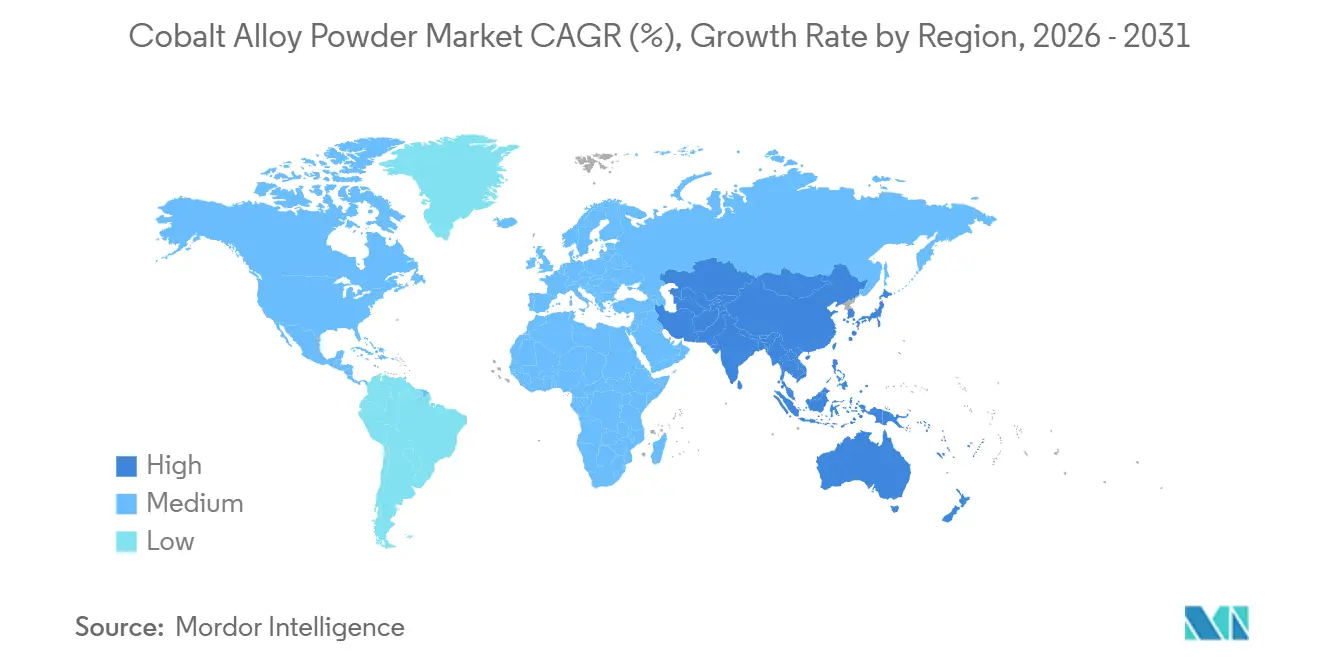

- By geography, Asia-Pacific captured 36.67% of 2025 revenue and is forecast to advance at a 6.03% CAGR in the 2026 to 2031 period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cobalt Alloy Powder Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aerospace/medical high-performance needs | +1.4% | Global, concentrated in North America & Europe aerospace hubs, APAC medical device manufacturing | Medium term (2-4 years) |

| Wear and corrosion-resistant tooling demand | +0.9% | Global, strongest in APAC manufacturing clusters (China, Japan, South Korea) and European automotive tooling | Long term (≥ 4 years) |

| Hydrogen-turbine material requirements | +1.1% | Europe (hydrogen infrastructure leaders), North America (industrial decarbonization), emerging APAC | Long term (≥ 4 years) |

| Cold-spray repair adoption in MRO | +0.7% | North America & Europe (mature MRO networks), APAC growth in commercial aviation aftermarket | Medium term (2-4 years) |

| AI-accelerated custom alloy design | +0.8% | Global, led by North America and Europe R&D centers, rapid adoption in APAC contract manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aerospace/Medical High-Performance Needs

Next-gen commercial engines are now pushing turbine inlet temperatures beyond 1,650 °C. This surge is driving up the demand for cobalt-chromium powders, celebrated for their oxidation resistance, especially in scenarios where nickel systems falter. In a move that underscores its scaling momentum, ATI inaugurated a large additive facility in 2025. At this facility, they print cobalt superalloy parts with heights of up to 1.5 m, tailored specifically for U.S. naval reactors. In the medical device arena, while ASTM F75-compliant CoCrMo remains the preferred choice for hip stems, the EU Medical Device Regulation has recently flagged cobalt as a CMR. This designation mandates warning labels for cobalt content surpassing a specific threshold and has spurred trials for titanium-only junctions. ECRI reviews highlighted no significant difference in target-lesion revascularization between cobalt-chromium stents and their counterparts, reducing the urgency for alternatives. In response to these regulatory hurdles, Carpenter Technology introduced BioDur 108. This innovative grade, free from both nickel and cobalt, is an austenitic stainless steel with impressive tensile strength, cleverly avoiding MDR labels. However, consumption data from 2024 reveals that superalloys accounted for a significant share of global cobalt usage, spotlighting the unwavering demand from both aerospace and implant industries.

Wear and Corrosion-Resistant Tooling Demand

Stellite and Tribaloy families are now used in applications such as cutting tools, oil-and-gas valves, and hot-forming dies, where carbides previously underperformed. In tests conducted at 600 °C, thermal-sprayed cobalt-oxide coatings, applied through a suspension plasma spray, exhibited the lowest wear rates. This superior performance is attributed to CoO-to-Co₃O₄ phase transitions, which form lubricious glaze layers. Kennametal’s Infrastructure division operates powder plants in Nevada, North Carolina, Germany, and China, supplying cobalt-bonded carbides for these advanced applications. Japan has increased its metal powder production in recent years, driving a surge in demand for spherical CoCrMo feedstock, which is crucial for refurbishing valves and dies. Additionally, high-velocity oxy-fuel and air-fuel jets have adopted digital powder passports, improving traceability and reducing scrap in the tooling supply chain.

Hydrogen-Turbine Material Requirements

OEMs are now qualifying cobalt-chromium-molybdenum liners and nozzles for their superior scale resistance. This qualification is essential as burning hydrogen produces high-pressure steam, which degrades nickel superalloys[1]Fraunhofer, “Recreating Cobalt-Based Glaze Layers Through Thermal Spraying for Extreme Environments,” Fraunhofer, fraunhofer.de. Additionally, machine-learning-guided HEAs in Ni-Co-Cr-Al-Fe systems have improved oxide spallation behavior. Furthermore, FOMAS/3D Energy has introduced the MIMETE N 75 powder for hydrogen gas valves. This powder features an eight-week lead time and is priced lower than traditional cast components. With Europe's Green Deal funding and manufacturing credits from the U.S. Inflation Reduction Act, pilot turbine builds have gained momentum, underscoring the pivotal role of cobalt alloys in advancing low-carbon power initiatives.

Cold-Spray Repair Adoption in MRO

High-temperature friction tests reveal that air-fuel thermal spraying of cobalt alloys on CMSX-4 substrates not only prolongs turbine blade life but also surpasses alternative overlays. ATI, blending materials science with laser powder bed fusion, now offers AS9100D-certified repairs, drastically cutting aircraft downtime and reducing scrap rates. With aftermarket volumes booming in China and Singapore, Asia-Pacific maintenance, repair, and overhaul shops are licensing cold-spray intellectual property, creating a secondary demand stream for fine cobalt powders.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and ethical mining issues | -0.6% | Global supply chains sourcing from DRC; compliance pressure strongest in EU and North America | Medium term (2-4 years) |

| EU critical-materials limits in implants | -0.4% | Europe (MDR enforcement), spillover to export markets requiring CE marking | Short term (≤ 2 years) |

| Emerging high-entropy alloy substitutes | -0.3% | Global, led by North America and Europe, research and development, early adoption in aerospace prototyping | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Ethical Mining Issues

In 2025, the Democratic Republic of Congo (DRC) maintained its position as the dominant player in the cobalt market, accounting for the majority of the world's mined cobalt[2]Sandvik, “Responsible Sourcing Report 2024,” Sandvik, sandvik.com. However, despite efforts to enhance traceability, artisanal operations in the DRC continued to face allegations of child labor. A four-month export freeze in the DRC during 2026 caused a significant increase in cobalt prices. This price surge tightened margins for atomizers, prompting a shift toward Indonesian HPAL precipitate. At the same time, audits of smelters for RMAP compliance highlighted the growing importance of ESG premiums, which many price-sensitive tooling segments have been reluctant to adopt.

EU Critical-Materials Limits in Implants

Patient concerns and insurer oversight have increased due to the EU MDR's CMR label on cobalt exceeding a specific threshold. Data revealed that Profemur modular neck hips underwent frequent revisions, amplifying calls for reformulation. Carpenter's BioDur 734, a nitrogen-strengthened steel, completely avoids cobalt while meeting fatigue limits, signaling a material shift in European orthopedics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Alloy Type: Cobalt-Chromium Dominates Across Applications

In 2025, cobalt-chromium alloys, driven by demand for turbine blades and orthopedic implants, accounted for 47.11% of the cobalt alloy powder market. These powders, forecasted to grow at a 5.76% CAGR during the 2026–2031 period, resist oxidation at temperatures exceeding 800 degrees Celsius and protect against wear on articulating surfaces. However, the EU's MDR CMR labeling could steer some implants toward titanium and stainless steel alternatives. Meanwhile, second-tier systems such as cobalt-nickel are used in combustor liners, while cobalt-iron is directed toward soft-magnetic components. Specialized grades, including Tribaloy and CoCrAlY bond coats, serve niche wear and coating applications.

Additive manufacturing highlights the importance of cobalt-chromium, enabling intricate cooling passages and customized patient geometries. The FOMAS group's MIMETE N 75 powder demonstrates its versatility, finding application in industrial gas turbines. Conversely, HEA prototypes with yields exceeding 755 MPa may pose a potential market threat in the mid-2030s. However, with a decade-long approval process in aerospace and elevated raw material costs, cobalt-chromium continues to dominate the spotlight for the time being.

By Production Method: Atomization Leads, Plasma Accelerates

By 2025, cobalt alloy powder production saw atomization dominate with a 73.22% share. For LPBF feedstocks, gas and vacuum induction melting gas atomization (VIGA) became the top choice. Meanwhile, water atomization found its niche in press-and-sinter parts, where its unique morphology did not hinder flowability. Atomization has been on a growth trajectory, expanding at a 6.03% CAGR during the forecast period of 2026–2031. This surge is largely attributed to ultrasonic variants, which recycle scrap into a 95%-spherical powder, maintaining an oxygen content below 500 ppm to meet ISO/ASTM 52907 standards.

A 2025 pilot showcased the recycling of FeCoNi, eliminating the need for virgin feedstock. In a similar vein, the Powder2Powder system was crafted to approach near-net-zero supply chains. While mechanical alloying is predominantly a research domain due to contamination concerns, electrolytic methods successfully address the ultrahigh-purity niche grade demand. Moreover, innovations like digitized powder passports and AI-enhanced inline sensors are transforming the landscape. These advancements facilitate real-time monitoring of particle distribution, leading to a notable decrease in batch reject rates for both VIGA and plasma production lines.

By Application: Additive Manufacturing Leads Growth

In 2025, the cobalt alloy powder market saw additive manufacturing taking a commanding lead with a 32.56% share. Projections indicate a growth trajectory, estimating a 6.11% CAGR during the forecast period of 2026–2031. This optimistic outlook is supported by significant advancements, such as laser powder bed fusion machines crafting 1.5-meter-tall naval propulsion components. In the aerospace sector, innovations like internal cooling channels are being deployed to enhance turbine efficiency. In the medical field, Original Equipment Manufacturers are utilizing 3D printing to produce porous osseointegrative implants, leading to significantly faster patient recovery times.

Thermal spray coatings have emerged as a key application, employing techniques such as high-velocity oxygen fuel (HVOF) and suspension plasma spray. By utilizing cobalt-oxide and CoCrMo overlays, these methods protect valves and chemical reactors from temperatures reaching up to 600 degrees Celsius. In the aviation aftermarket, cold-spray repairs are rejuvenating components, significantly extending their operational lifespans. The tooling industry is leveraging binder-jet and direct energy deposition methods to rapidly produce conformal-cooled dies, surpassing the efficiency of traditional electrical discharge machining (EDM). The energy sector is integrating cobalt alloys into hydrogen-ready turbines and components for nuclear steam generators, ensuring robust and sustained demand over extended operational cycles.

By End-User Industry: Aerospace and Defense Fastest

In 2025, the aerospace and defense sectors accounted for 28.89% of the cobalt alloy powder market. This segment is projected to grow at a 6.12% CAGR during the forecast period of 2026–2031, driven by increased production rates for Boeing and Airbus narrow-body aircraft. Furthermore, defense programs such as the B-21 and NGAD specify CoCrMo for operations at 1,200 °C in hot sections. The healthcare sector also plays a significant role. However, while global implants remain steady, the European Union's CMR labeling introduces an element of uncertainty.

The automotive industry utilizes cobalt-iron magnets and exhaust valves. However, changes in magnet chemistry for electric vehicles could temper this growth. On the other hand, the energy and power sectors are gaining momentum, particularly with advancements in hydrogen infrastructure. Various manufacturing industries rely on cobalt-bonded carbides for wear parts, with notable demand in oil-and-gas and pulp mills. Lastly, the electronics sector, although a smaller contributor, utilizes soft-magnetic powders for high-frequency inductors.

Geography Analysis

In 2025, the Asia-Pacific region, buoyed by China's refining dominance and a 2024 uptick in powder metallurgy output, commanded 36.67% of global revenues, expanding at a robust 6.03% CAGR (2026-2031). South Korea's heightened aerospace spending spurred domestic demand for CoCr turbine disks. Concurrently, while plasma recycling pilots in Singapore and India's budding AM clusters offered a boost, both regions remained reliant on imported powder.

North America closely followed, leveraging expansive additive hubs and powder plants in pivotal states, both benefiting from the Inflation Reduction Act credits. Canada's MRO ecosystem and Mexico's tier-one automotive suppliers bolstered demand, yet both faced potential supply shocks from the DRC.

Europe enjoyed strong demand from the aerospace and medical sectors but contended with the continent's stringent regulations. Major suppliers established bases in Germany, the U.K., and France. However, challenges persist: the MDR CMR labeling threatens cobalt implant volumes, and the Critical Raw Materials Act emphasizes the urgency for on-continent refining. Yet, with Nordic hydrogen projects and offshore wind initiatives gaining traction, they could counterbalance potential orthopedic setbacks.

South America and the MEA regions contributed modestly. Brazil tapped into platform pipelines, and Saudi Arabia channeled Vision 2030 funds to bolster gas turbine capabilities. An export moratorium from the DRC, lifted in late 2025, underscored Africa's dependency on Asia for feedstock. This insight catalyzed swift expansions in Indonesian HPAL capacities, now achieving notable totals through strategic partnerships.

Competitive Landscape

The cobalt alloy powder market remains moderately fragmented. Success today hinges on innovations such as AI-driven alloy design, plasma atomization for scrap recycling, and digital traceability to meet customer ESG audits. Players lacking in transparency or quick custom-alloy adjustments risk falling behind, particularly as aerospace and medical sectors refine their supplier choices.

Cobalt Alloy Powder Industry Leaders

CRS Holdings, LLC.

Sandvik AB

Höganäs AB

ATI

GKN Powder Metallurgy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: KoBold Metals signed a mineral exploration agreement with the Democratic Republic of Congo to improve U.S. access to critical minerals. Backed by investors, this initiative aims to reduce reliance on Chinese-controlled cobalt processing. Diversifying supply chains is expected to support the production of cobalt alloy powder, essential in advanced manufacturing.

- May 2025: The EU's Critical Raw Materials Act took effect, establishing frameworks to strengthen supply chain resilience for critical materials, including cobalt, with notable implications for global sourcing strategies.

Global Cobalt Alloy Powder Market Report Scope

Cobalt alloy powder is a finely divided cobalt-based material engineered with elements such as chromium, nickel, and molybdenum, designed to provide superior high-temperature strength, wear resistance, and biocompatibility. It is essential for high-stakes applications, including aerospace turbine blades and medical implants, and is typically produced through gas atomization for use in 3D printing.

The cobalt alloys market is segmented by alloy type, production method, application, end-user industry, and geography. By alloy type, the market is segmented into cobalt-chromium alloys, cobalt-nickel alloys, cobalt-iron alloys, cobalt-molybdenum alloys, and other specialized cobalt alloys. By production method, the market is segmented into atomization (gas, water, plasma), chemical reduction, electrolytic methods, and mechanical alloying. By application, the market is segmented into additive manufacturing/3D printing, aerospace components, medical implants and devices, tooling and wear parts, thermal spray coatings, energy and power generation, and others (automotive, defense, electronics). By end-user industry, the market is segmented into aerospace and defense, healthcare and medical, automotive and transportation, energy and power, manufacturing and industrial machinery, and electronics and electricals. The report also covers the market size and forecasts for the market in 17 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Cobalt-Chromium Alloys |

| Cobalt-Nickel Alloys |

| Cobalt-Iron Alloys |

| Cobalt-Molybdenum Alloys |

| Other Specialized Cobalt Alloys |

| Atomization (Gas, Water, Plasma) |

| Chemical Reduction |

| Electrolytic Methods |

| Mechanical Alloying |

| Additive Manufacturing/3D Printing |

| Aerospace Components |

| Medical Implants and Devices |

| Tooling and Wear Parts |

| Thermal Spray Coatings |

| Energy and Power Generation |

| Others (Automotive, Defense, Electronics) |

| Aerospace and Defense |

| Healthcare and Medical |

| Automotive and Transportation |

| Energy and Power |

| Manufacturing and Industrial Machinery |

| Electronics and Electricals |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Alloy Type | Cobalt-Chromium Alloys | |

| Cobalt-Nickel Alloys | ||

| Cobalt-Iron Alloys | ||

| Cobalt-Molybdenum Alloys | ||

| Other Specialized Cobalt Alloys | ||

| By Production Method | Atomization (Gas, Water, Plasma) | |

| Chemical Reduction | ||

| Electrolytic Methods | ||

| Mechanical Alloying | ||

| By Application | Additive Manufacturing/3D Printing | |

| Aerospace Components | ||

| Medical Implants and Devices | ||

| Tooling and Wear Parts | ||

| Thermal Spray Coatings | ||

| Energy and Power Generation | ||

| Others (Automotive, Defense, Electronics) | ||

| By End-User Industry | Aerospace and Defense | |

| Healthcare and Medical | ||

| Automotive and Transportation | ||

| Energy and Power | ||

| Manufacturing and Industrial Machinery | ||

| Electronics and Electricals | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the cobalt alloy powder market in 2031?

It is expected to reach USD 3.15 billion by 2031 from USD 2.44 billion in 2026, growing at a 5.22% CAGR (2026-2031).

Which segment leads growth within this market?

Additive manufacturing is the fastest-expanding application, advancing at a 6.11% CAGR (2026-2031).

Why is Asia-Pacific gaining share?

China’s refining dominance, Daido Steel’s powder output rise, and expanding aerospace programs in Japan and South Korea lift regional demand.

How are regulations affecting cobalt powders for implants?

EU MDR classifies cobalt as a CMR substance above 0.10 wt%, forcing warning labels or alloy substitution in orthopedic devices.

What technologies are reshaping powder production?

Ultrasonic plasma atomization for recycled feedstock and AI-driven alloy design are cutting costs and development time while improving sustainability.

Page last updated on: