South Korea Government And Education Logistics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

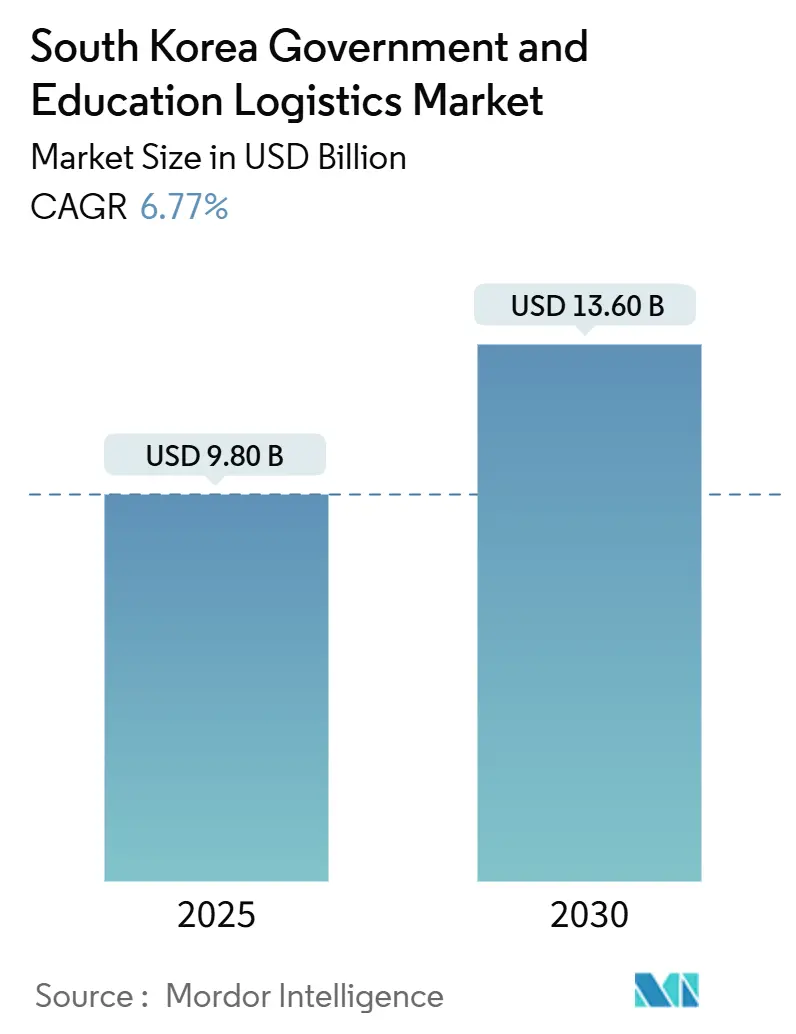

| Market Size (2025) | USD 9.80 Billion |

| Market Size (2030) | USD 13.60 Billion |

| Growth Rate (2025 - 2030) | 6.77% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Government And Education Logistics Market Analysis by Mordor Intelligence

The South Korea Government And Education Logistics Market size is estimated at USD 9.80 billion in 2025, and is expected to reach USD 13.60 billion by 2030, at a CAGR of 6.77% during the forecast period (2025-2030).

The steady expansion is underpinned by the government’s digital-first procurement architecture, aggressive smart-campus investments, and defense-oriented stockpiling programs that elevate demand for technology-enabled, multimodal logistics services. New carbon-neutral contracting rules accelerate fleet electrification and warehouse decarbonization, while demographic labor shortages propel wide-scale automation of transport, material‐handling, and last-mile activities. Together, these trends create a high-entry-barrier environment in which providers with advanced IT platforms, secure facilities, and sustainability credentials command stronger negotiating power with public agencies. Intensifying competition around value-added services—kitting, device staging, and reverse flows—opens revenue pools well beyond conventional freight haulage, linking logistics spending more closely to government innovation mandates.

Key Report Takeaways

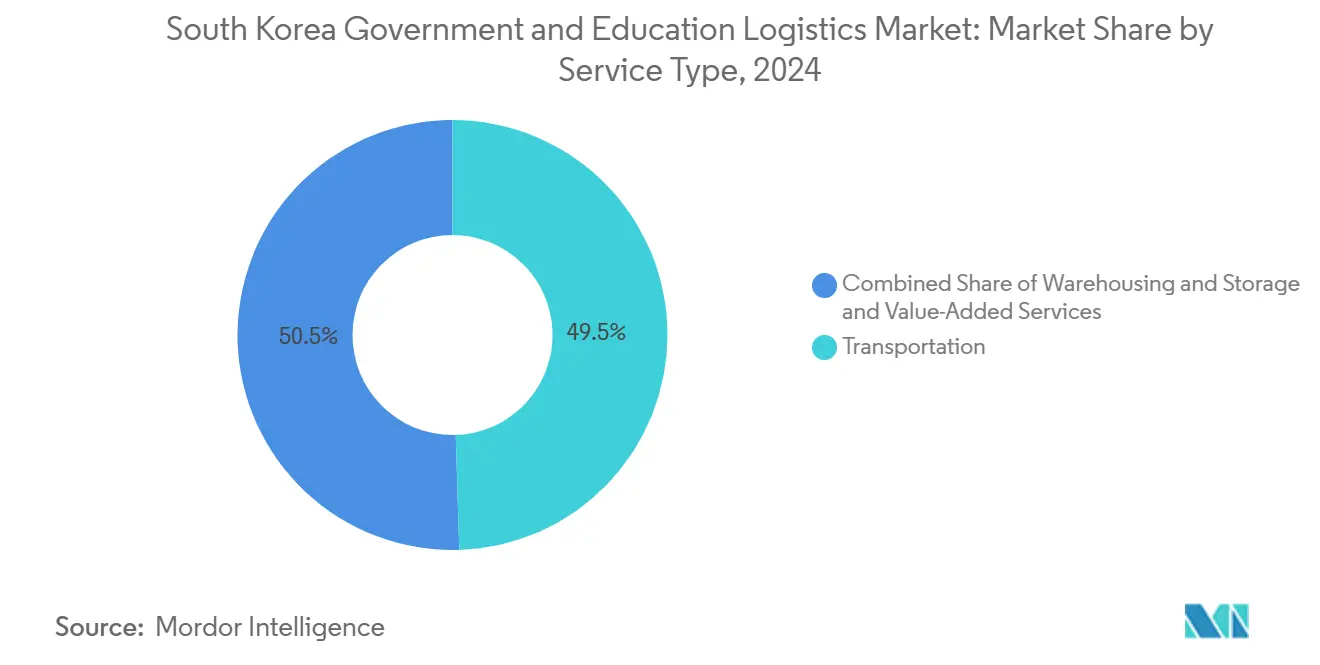

- By service type, transportation led with 49.50% of the South Korea government and education logistics market share in 2024; value-added services are projected to expand at an 8.20% CAGR through 2030.

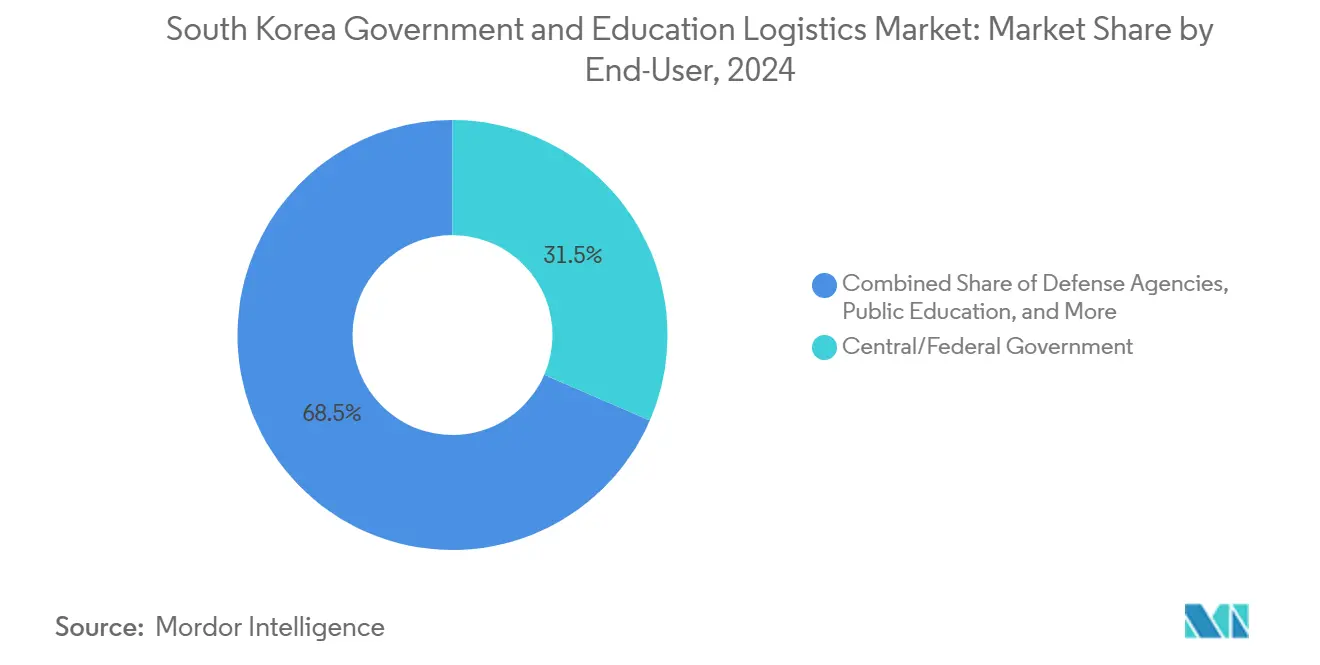

- By end-user, the Central/Federal government held 31.50% of the South Korea government and education logistics market size in 2024, while higher-education institutions are expected to record the highest projected 8.40% CAGR to 2030.

Worldwide industry scale is not derived from any single country or region but from the combination of national and regional inputs. The government and education logistics market size of Mordor Intelligence integrates these into one global valuation.

South Korea Government And Education Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public-sector digital-first procurement | +1.8% | Seoul Capital Area and other large metros | Short term (≤ 2 years) |

| Expansion of school meal & textbook delivery | +1.2% | Higher impact in rural provinces | Medium term (2–4 years) |

| Defense stockpiling & readiness logistics | +0.9% | Near DMZ and major military installations | Long term (≥ 4 years) |

| Smart-campus micro-fulfillment pilots | +0.7% | Premier universities and research institutions | Medium term (2–4 years) |

| Aggregated provincial e-commerce returns | +0.5% | Seoul–Gyeonggi growth corridor | Short term (≤ 2 years) |

| Commercial drone corridors for islands | +0.4% | Jeju, Ulleungdo, and southwestern coastal islands | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public-Sector Digital-First Procurement Revolutionizes Market Architecture

Korea’s AI-enabled procurement portal eliminates paper workflows and brokers real-time vendor matching, obliging service providers to publish live performance data and blockchain-validated records. Logistics firms that operate cloud-native transport-management systems and API-ready fleet telemetry gain preferential scores, while analog operators risk disqualification under new compliance filters. Early contracts show double-digit cycle-time reductions, confirming that digital readiness now functions as a de facto threshold for entry into the South Korea government and education logistics market[1]Ministry of Economy and Finance, “National Digital Procurement Framework 2025,” moef.go.kr.

Educational Institution Logistics Mandates Create Specialized Service Ecosystems

Unified national standards for meal, device, and learning-material deliveries compel carriers to master HACCP-grade cold chains, bulk device staging, and on-campus reverse flows. Providers embed directly with school ERPs, scheduling routes against class timetables and nutrition audits. The complexity consolidates spending toward integrated operators that can manage every node from the central warehouse to the classroom locker, expanding the South Korea government and education logistics market well beyond basic transport[2]Ministry of Education, “Smart Campus Roadmap 2025,” moe.go.kr

Defense Logistics Modernization Accelerates Strategic Infrastructure Development

The Ministry of National Defense requires tamper-evident seals, SCADA-secured depots, and encrypted data interchange for all classified consignments. Domestic firms benefit from local-content rules and proximity to shipyards and munitions plants, while foreign entrants confront higher security vetting costs. Multi-year contracts guarantee stable volumes, but demand cyber-resilient networks and redundant nodes, making capital-intensive investments essential for sustained participation in the South Korea government and education logistics market[3]Ministry of National Defense, “Strategic Logistics Modernization Plan,” mnd.go.kr.

Smart-Campus Initiatives Drive Technology Integration Imperatives

Universities deploy micro-fulfillment hubs, autonomous robot runners, and app-based parcel lockers, shrinking delivery windows from days to hours. Logistics partners must integrate ID verification with student information systems and route battery-electric vans inside emission-controlled “green rings,” reinforcing the premium placed on clean fleets. These pilots increase value density per drop and reinforce the South Korea government and education logistics market’s migration toward data-rich, tech-heavy workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight green-procurement carbon thresholds | −1.4% | Strongest in Seoul metropolitan area | Short term (≤ 2 years) |

| Aging driver & warehouse labor pool | −0.8% | National; acute in rural provinces | Medium term (2–4 years) |

| Centralized price-cap rules on 3PL fees | −0.6% | Uniform across public contracts | Short term (≤ 2 years) |

| Oligopolistic pallet & crate supply | −0.3% | Weighted toward small-scale operators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Green Procurement Mandates Transform Operational Paradigms

The government tenders now rate carbon intensity alongside cost and service. Fleets must convert to electric or hydrogen powertrains, depots must run on certified renewables, and dashboards must expose real-time emissions. Initial retrofits inflate operating costs by 5–7%, suppressing margins for asset-heavy carriers and tightening credit needs. Providers that achieve early net-zero certification secure contract multipliers, supporting their share of the South Korea government and education logistics market[4]Environmental Management Corporation, “Public-Sector Carbon Threshold Guidelines,” keco.or.kr.

Workforce Demographics Challenge Operational Sustainability

The median driver age surpasses 53 years, and turnover exceeds 20% annually. Wage guarantees raise direct labor costs while shrinking applicant pools in remote counties. Autonomous forklifts and robotic sorters offset shortages but require multimillion-dollar capital programs that only large operators can sustain. Over the medium term, labor scarcity restrains fleet utilization and flattens growth potential in segments of the South Korea government and education logistics market that remain manual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Transportation Dominance Faces Technology-Driven Disruption

Transportation accounted for 49.50% of overall revenue in 2024, confirming its foundational role in the South Korea government and education logistics market. Road haulage benefits from digitized tolling and high-capacity motorways, while rail gains dedicated government cargo slots for school and defense consignments. Airfreight covers time-critical military spares and exam materials, and sea lanes move bulk food reserves. Growing regulatory insistence on track-and-trace upgrades requires 5G-enabled IoT sensors and predictive analytics, steering contracts toward carriers that can deliver verified, real-time milestones.

Value-added services expand at an 8.20% CAGR as agencies outsource kitting, device flashing, and sustainability-linked reverse flows. These activities lift margins and embed providers deeper in agency workflows. Warehousing maintains mid-single-digit growth, underpinned by stockpiling initiatives. Autonomous pallet movers, temperature-controlled micro-zones, and AI-directed slotting enhance throughput and differentiate modern facilities inside the South Korea government and education logistics market.

By End-User: Federal Dominance Shifts Toward Education-Driven Growth

The Central/Federal Government contributed 31.50% of the South Korea government and education logistics market size in 2024 due to bulk procurement power and system-wide digitization projects. Ministries contract long-haul trunking, bonded storage, and customs brokering under five-year master agreements that reward ISO 9001 and ISO 14001 compliance.

Higher Education Institutions grow fastest at an 8.40% CAGR on the back of smart-campus automation, research-grade cold chains, and grant-funded technology pilots. K-12 public schools remain stable but large, anchoring daily meal deliveries and tablet rotations. Defense agencies continue to command premium rates for secure, clearance-bound moves. State and local bodies widen participation via decentralized e-tendering, spreading the South Korea government and education logistics market to secondary cities and creating business for mid-tier regional operators.

Geography Analysis

The Seoul Capital Area captures the largest slice of contracting value, reflecting dense clusters of ministries, headquarters, and flagship universities. Five international airports, two smart ports, and a 24-hour rail shuttle grid enable sub-24-hour lead times nationwide, reinforcing volume concentration. Yet balanced regional development policy now channels funds to Busan, Daejeon, and Gwangju, diluting share-of-spend and inviting logistics firms to build satellite depots for next-day service.

Busan anchors maritime flows and defense cargo, processing outsized project shipments through its new port eco-complex. Proximity to shipyards and naval bases demands high-tonnage crane capacity and specialized rigging crews. Jeju Province pioneers unmanned aerial vehicle corridors that fly medical supplies and exam scripts to island schools, making the archipelago a testbed for drone service models within the South Korea government and education logistics market.

Rural provinces grapple with sparse infrastructure and shrinking workforces, yet statutory service-level parity obliges operators to cover last-mile routes at higher per-drop cost. Government fuel-surcharge relief and cross-subsidy pools cushion margins, while carbon-credit rewards offset parts of the expense of low-emission vans. Collectively, these dynamics balance geographic equity with operational feasibility, sustaining cohesive national coverage.

Mordor Intelligence tracks the government and education logistics market across other major regions such as Africa, Asia, and North America, with additional country-level coverage spanning Japan, China, Canada, United Kingdom, Mexico, and France, each reflecting localized structural drivers, restraints and more.

Competitive Landscape

Domestic incumbents such as CJ Logistics, Korea Express, and LX Pantos leverage established security clearances, nationwide depots, and deep compliance teams to anchor multi-year government frameworks. Technology investment supersedes price discounting as the primary battleground. Leaders deploy AI route optimizers, blockchain verifiers, and carbon dashboards that feed directly into ministry oversight portals.

Automated sortation raises throughput, while digital twins cut contingency stock by 10–15%, reinforcing incumbents’ hold on high-complexity contracts within the South Korea government and education logistics market.

New entrants pursue white-space niches: Hanwha Systems Logistics targets defense-grade cyber-secure freight; university spin-offs pilot autonomous indoor deliveries; and drone operators test BVLOS services for remote island resupply. Success hinges on aligning with government sandbox programs that lower regulatory friction and provide early-stage revenue bridges.

South Korea Government And Education Logistics Industry Leaders

CJ Logistics

Korea Post

LX Pantos

Hyundai Glovis

Samsung SDS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: LX Pantos broke ground on the New Port Eco Logistics Center in Busan’s hinterland complex, expanding import–export capacity for public-sector cargo.

- June 2025: FedEx launched a direct South Korea–Taiwan freighter link, cutting transit for critical medical and infrastructure components destined for public projects.

- April 2025: DSV completed its acquisition of DB Schenker, enlarging multimodal offerings for Korean government agencies seeking global reach.

- October 2024: Scan Global Logistics invested USD 25 million to establish a government services unit focused on security-cleared contracts.

South Korea Government And Education Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea and Inland Waterway | |

| Warehousing & Storage | |

| Value-Added Services |

| Central/Federal Government |

| State & Local Government |

| Defense Agencies |

| Public Education (K-12) |

| Higher Education Institutions |

| Others |

| By Service Type | Transportation | Road |

| Rail | ||

| Air | ||

| Sea and Inland Waterway | ||

| Warehousing & Storage | ||

| Value-Added Services | ||

| By End-User | Central/Federal Government | |

| State & Local Government | ||

| Defense Agencies | ||

| Public Education (K-12) | ||

| Higher Education Institutions | ||

| Others |

Key Questions Answered in the Report

How large will government and education logistics spending in South Korea be by 2030?

Aggregate outlays are projected to reach USD 13.6 billion, reflecting a 6.77% CAGR from 2025 levels.

Which service line is expanding fastest under Korean public contracts?

Value-added services—packaging, kitting, and reverse flows—are forecast to grow at 8.20% CAGR through 2030.

Why are higher-education institutions reshaping logistics demand?

Smart-campus automation and research material handling lift complexity, pushing the segment toward an 8.40% CAGR.

What role do carbon rules play in contract awards?

Tenders now score emissions alongside price and service, favoring providers with electric fleets and real-time carbon dashboards.

How is defense modernization influencing private logistics firms?

Military stockpiling and cyber-secure freight needs open long-term, high-margin contracts for operators with security clearance.

Page last updated on: