United Kingdom Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

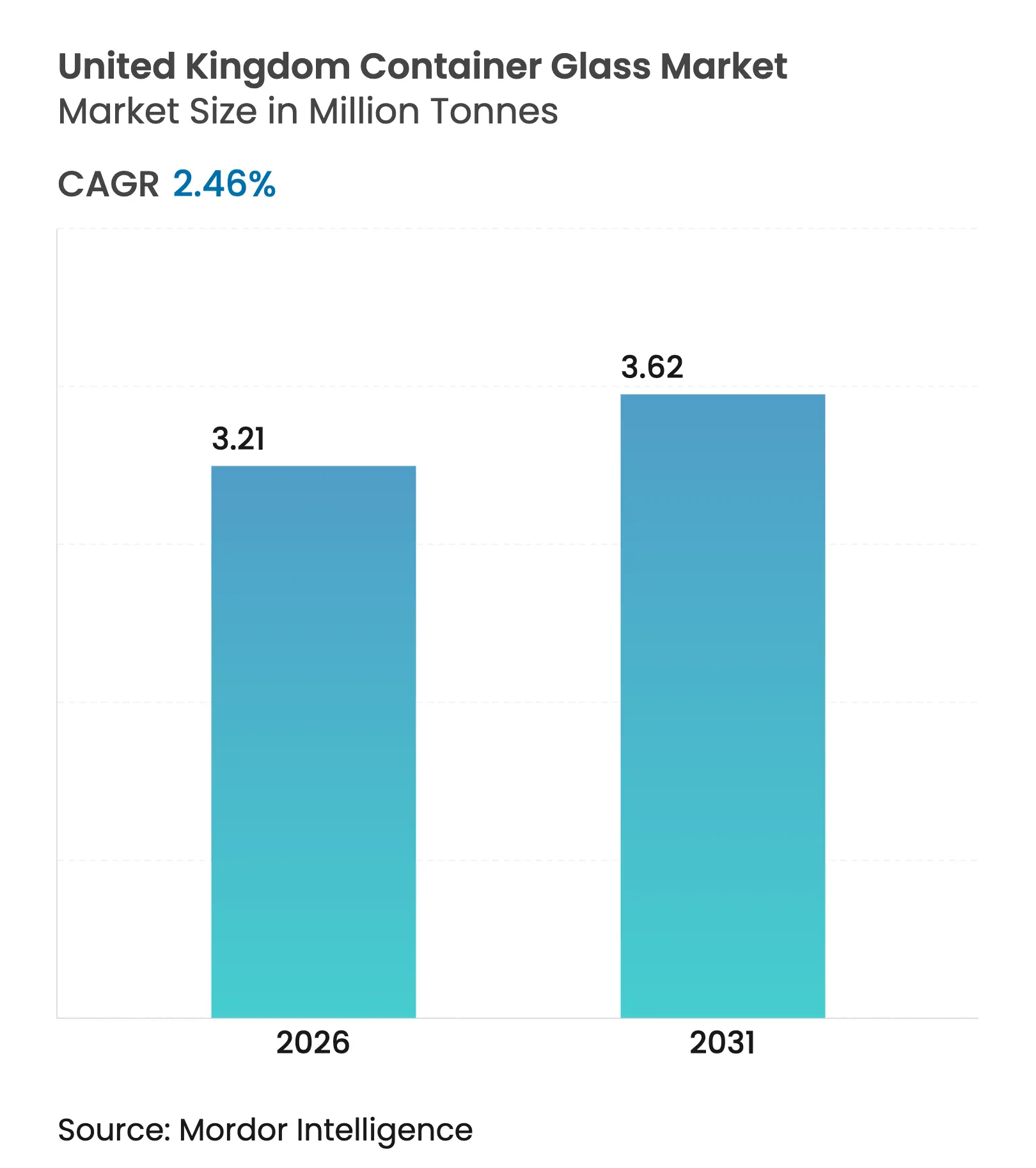

| Market Volume (2026) | 3.21 Million tonnes |

| Market Volume (2031) | 3.62 Million tonnes |

| CAGR | 2.46 % |

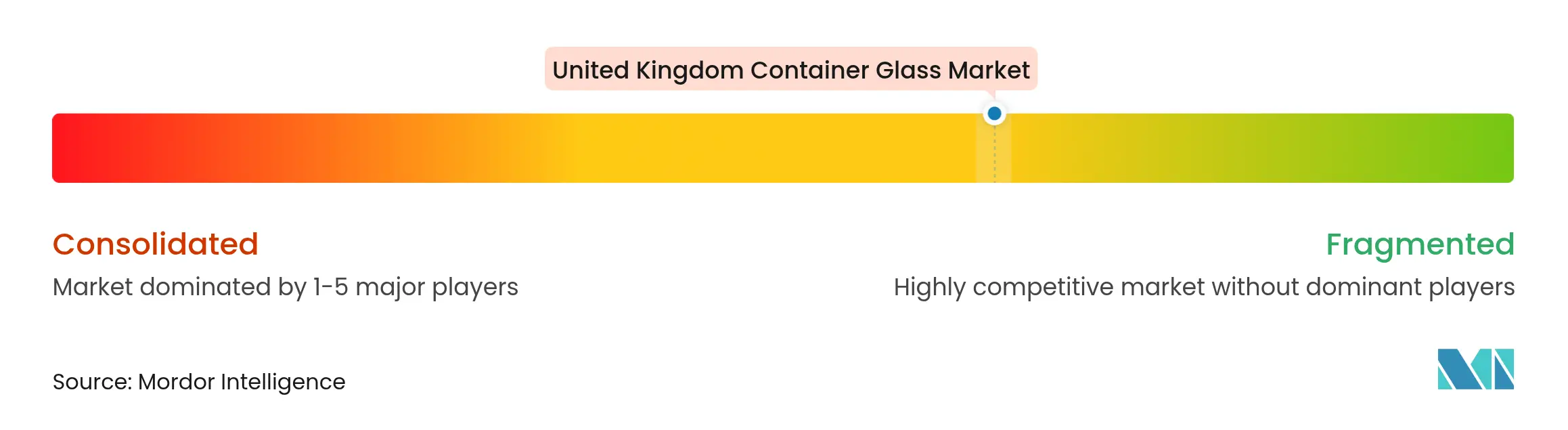

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

United Kingdom Container Glass Market Analysis by Mordor Intelligence

The United Kingdom Container Glass Market size in 2026 is estimated at 3.21 Million tons, growing from 2025 value of 3.13 Million tons with 2031 projections showing 3.62 Million tons, growing at 2.46% CAGR over 2026-2031. The modest growth trajectory underscores a mature landscape in which premium beverage demand, rising sustainability targets, and investments in lightweight technology collectively sustain momentum. Expansion of craft spirits and microbreweries, higher recycling-rate mandates, and retailer commitments to circular packaging amplify the sector’s resilience despite soft macroeconomic conditions. At the same time, elevated energy prices and competition from PET and aluminum cans pressure margins, prompting manufacturers to accelerate furnace upgrades, hybrid-fuel trials, and cullet utilization programs. Against this backdrop, brand owners increasingly emphasize premium aesthetics and climate credentials, creating an opportunity for suppliers that offer design flexibility, low-carbon production routes, and reliable national distribution.

Key Report Takeaways

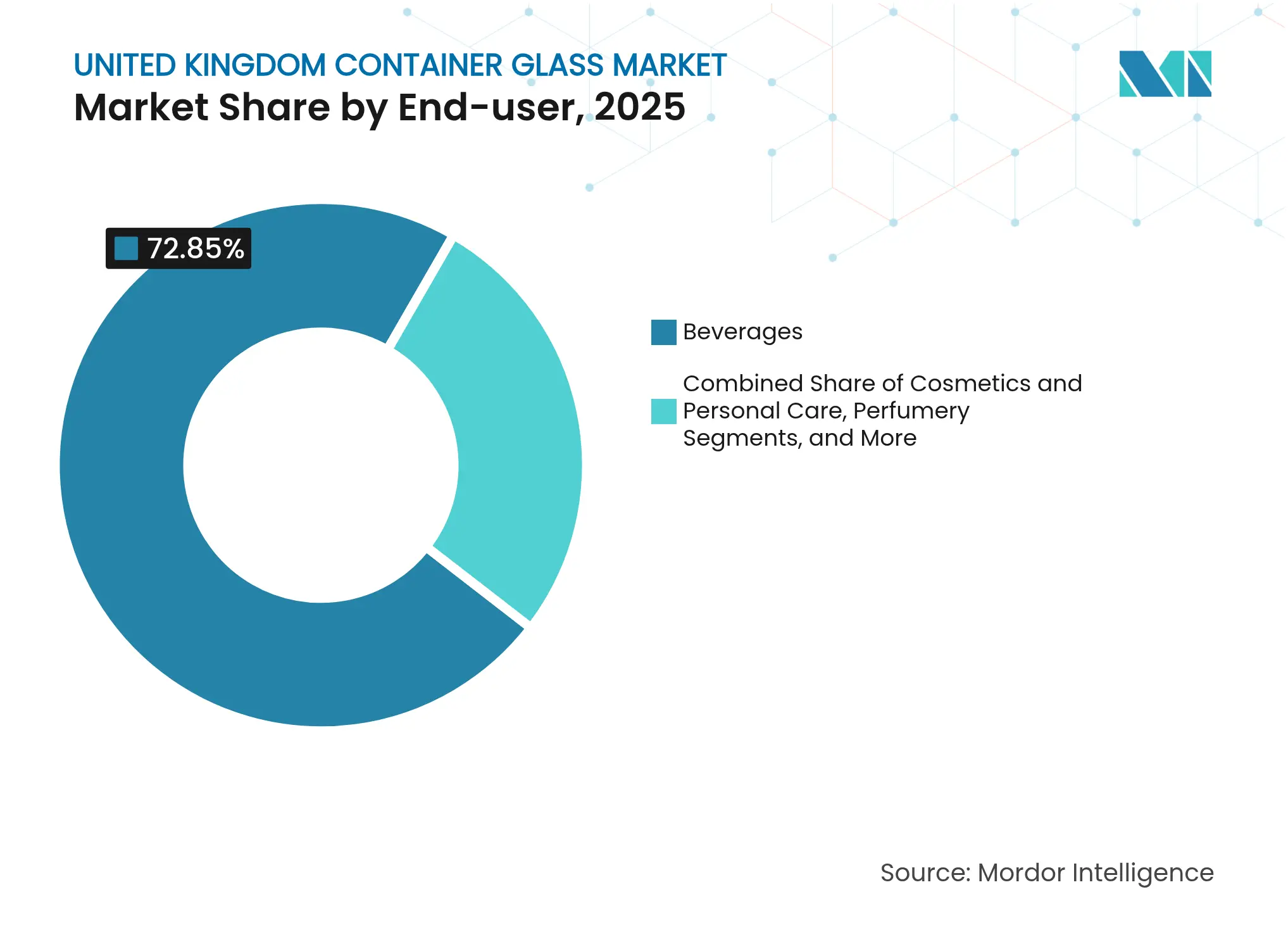

- By end-user, beverages captured 72.85% of the United Kingdom container glass market share in 2025.

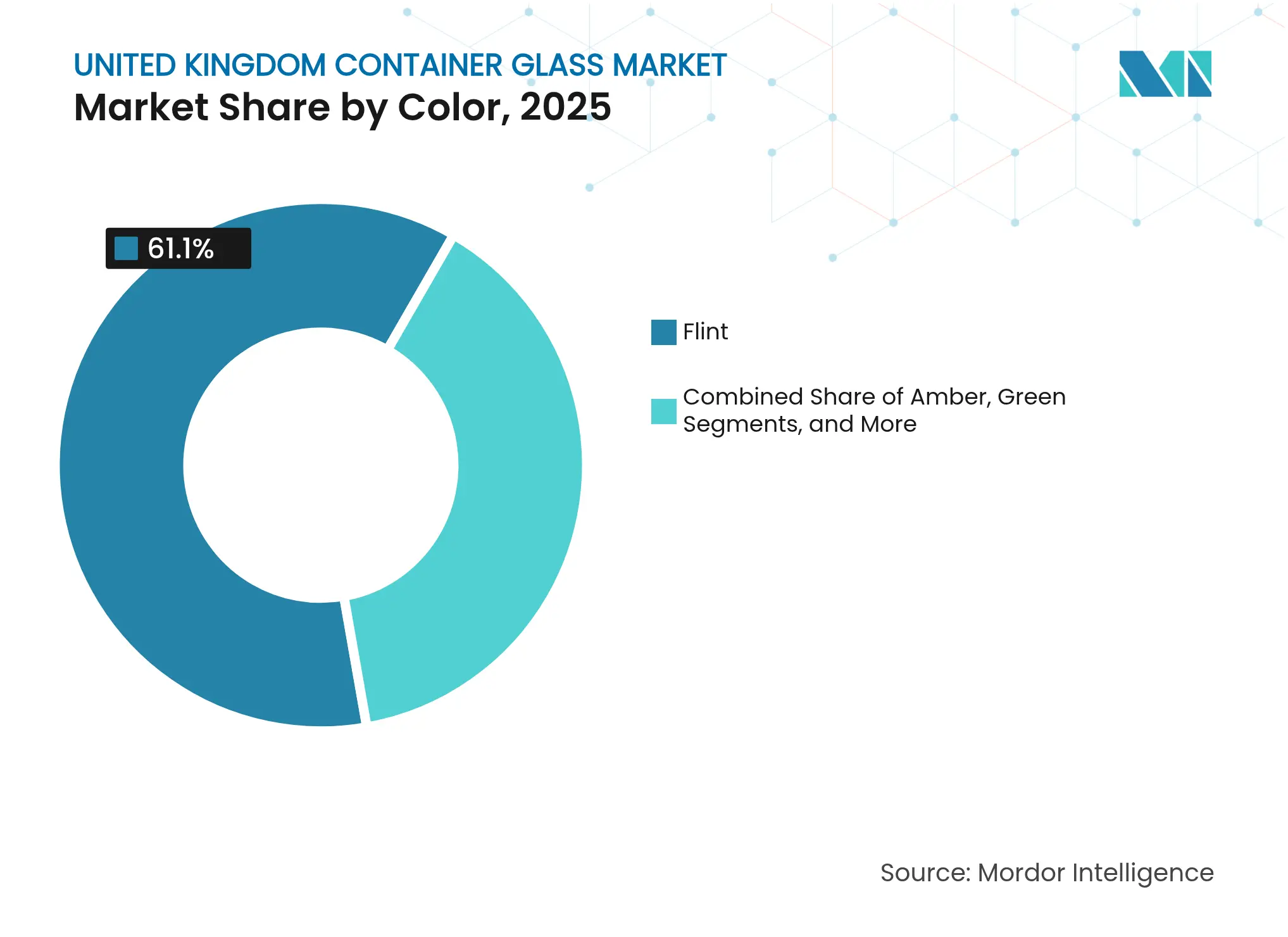

- By color, the United Kingdom container glass market for amber glass is projected to grow at a 4.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Container Glass Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Increased demand for premium alcoholic beverages Increased demand for premium alcoholic beverages | +0.8% | Scotland, London metropolitan area | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+0.8% | Geographic Relevance:Scotland, London metropolitan area | Impact Timeline:Medium term (2-4 years) |

Shift toward recyclable packaging by major UK retailers Shift toward recyclable packaging by major UK retailers | +0.6% | Nationwide retail networks | Long term (≥ 4 years) | |||

Growth of craft spirits and micro-breweries Growth of craft spirits and micro-breweries | +0.5% | Scotland, Northern England, Southwest | Medium term (2-4 years) | |||

Adoption of lightweight glass technology Adoption of lightweight glass technology | +0.4% | UK production hubs, export channels | Long term (≥ 4 years) | |||

Government recycling-rate targets for 2030 Government recycling-rate targets for 2030 | +0.3% | UK-wide regulatory framework | Long term (≥ 4 years) | |||

Rise in e-commerce demand for durable primary packaging Rise in e-commerce demand for durable primary packaging | +0.2% | UK-wide, concentrated in urban areas | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Increased Demand for Premium Alcoholic Beverages

Craft distilleries added more than 50 new sites in 2023, 42.8% above pre-pandemic levels, lifting the spirits category to a GBP 16.8 billion valuation (USD 20.6 billion) and stimulating customised glass bottle orders that accentuate brand storytelling. Diageo trimmed 3,000 tonnes of glass via ultra-lightweight formats yet retained premium cues, illustrating how cost, carbon, and cachet converge in a single design brief. Premium gin, whisky, and small-batch rum producers treat bottle shape and embossing as integral to shelf differentiation, generating higher average unit margins for container suppliers able to deliver short production runs. The same premiumisation logic extends to boutique wine and hop-forward craft beer SKUs that warrant amber or flint clarity to showcase liquids. The net effect is durable volume visibility for high-value bottle specifications within the UK container glass market, even as mainstream beer migrates to cans.

Shift Toward Recyclable Packaging by Major UK Retailers

Extended Producer Responsibility charges that entered staging in 2024 oblige brand owners to fund post-consumer recovery, driving supermarket groups including Tesco, Sainsbury’s, and ASDA to specify infinitely recyclable glass for premium private-label offerings. National recycling rates for packaging glass hit 76% in 2024, giving retailers confidence that material recovery loops function at scale. Procurement teams increasingly weigh ISO 14001 requirements and scope-3 footprint disclosure when selecting packaging substrates, advantaging glass over plastic for upmarket categories such as organic sauces and cold-pressed juices. As retailer scorecards tighten, suppliers that furnish closed-loop cullet backhauls and track-and-trace analytics gain competitive currency. These dynamics broaden the addressable base for container glass beyond core alcohol channels and embed multi-year demand visibility aligned with retailer road maps to 2030.

Growth of Craft Spirits and Micro-Breweries

Regional clusters in Speyside, Manchester, and Cornwall nurture hundreds of micro-producers whose brand identities hinge on bespoke bottle silhouettes, heavy bases, and tactile embossment that justify premium shelf pricing. Amber bottles dominate hop-intensive ales where UV protection preserves aroma integrity, and incremental orders compound as brewers expand into mixed-fermentation, barrel-aged, and low-alcohol variants. Direct-to-consumer e-commerce amplifies demand for robust yet aesthetically refined primary packaging that withstands courier networks yet arrives “gift-ready.” This convergence of small-batch growth and omnichannel distribution incentivises glassmakers to maintain agile production cells and collaborative design studios capable of 12-week concept-to-shelf cycles, cementing craft as a structural rather than cyclical driver of the UK container glass market.

Adoption of Lightweight Glass Technology

O-I Glass commissioned a hybrid-fuel furnace in Alloa that enables 180-gram spirits bottles a 28% weight cut relative to legacy formats while reducing energy intensity 5-7% per tonne. Verallia’s ECOVA line applies finite element modelling to decrease flint bottle mass by up to 15% yet preserves tactile quality prized by luxury brands. Encirc leverages its proximity to a hydrogen hub at Stanlow to explore H2-ready furnaces that could halve Scope 1 emissions by 2030. These technology pathways converge on a narrative where glass competes not only on recyclability but also on shipping efficiency and lower cradle-to-gate emissions, reinforcing its relevance within carbon-constrained supply chains.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Competition from PET and aluminium cans Competition from PET and aluminium cans | -0.7% | Beverage segments nationwide | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:Beverage segments nationwide | Impact Timeline:Medium term (2-4 years) |

High energy costs and carbon-emission levies High energy costs and carbon-emission levies | -0.5% | Furnace clusters in Northwest & Yorkshire | Short term (≤ 2 years) | |||

Raw-material supply-chain disruptions (soda ash, cullet) Raw-material supply-chain disruptions (soda ash, cullet) | -0.4% | UK-wide, import-dependent regions | Medium term (2-4 years) | |||

Furnace-maintenance downtime causing periodic shortages Furnace-maintenance downtime causing periodic shortages | -0.2% | Regional manufacturing clusters | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Competition from PET and Aluminum Cans

Aluminium captured further share in 2024 as rapid-chill convenience and 100% curbside recyclability aligned with brewer marketing for sessionable formats, eroding glass demand in mainstream lager and RTD cocktails. PET dominates soft drinks where unbreakable handling, ultralight logistics, and bottle-to-bottle recycling streams unlock two-digit cost savings versus glass.[1]Competition and Markets Authority, “State of UK Competition,” gov.uk These substrates intensify pricing discipline throughout retail beer and CSD aisles, diluting negotiating leverage for glassmakers on commodity-grade bottle SKUs. Glass retains a stronghold in whisky, gin, premium table wine, and artisan food but must concede volume positions in high-turn, grab-and-go channels where functional value supersedes shelf theatre.

High Energy Costs and Carbon-Emission Levies

Furnace fuel accounted for 23% of the cost of sales in 2024, and spot gas spikes forced day-scale production throttling at several UK sites. The UK Emissions Trading Scheme levies GBP 80-90 per tonne CO2e, a burden that manufacturers cannot fully pass to price-sensitive categories. British Glass cautioned that without relief, two legacy furnaces could shutter by 2026, potentially eliminating 8% of domestic capacity. Shorter tank rebuild cycles, hydrogen pilot retrofits, and electric boosting projects demand CAPEX at a pace outstripping near-term free cash generation, further squeezing smaller independents. Those pressures elevate strategic value for producers with diversified European networks capable of flexing cross-border supply.

Segment Analysis

By End-user: Premium Beverages Sustain Dominance

The beverages category represented 72.85% of the UK container glass market share in 2025, reaffirming glass as the default vessel for spirits, wine, and high-end beer. Within this group, spirits advanced at 3.78% annually, underpinned by craft labels demanding intricate embossment and unusually short lead times. The UK container glass market size for spirits bottles is projected to reach 1.25 thousand kilotons by 2031, delivering outsized margin contribution to suppliers able to balance customised mould costs with furnace utilisation. In parallel, beer packaging faces aluminium encroachment; however, on-premise craft brewers and heritage lager brands still value glass for flavor preservation and brand nostalgia, sustaining mid-single-digit growth in specialty formats. Non-alcoholic beverages contribute a steady baseline demand through premium juices and kombuchas, offsetting soft drink commoditisation.

A faster clip emerges in cosmetics and personal care as luxury skincare, high-dosage serums, and refillable fragrance lines favour glass’s inert barrier properties and upmarket visual cues. The sub-sector, currently <6% of tonnage, is forecast to add 3.92% CAGR through 2031, aided by refill station rollouts in flagship department stores that position glass jars as durable assets. Food applications such as artisanal jams, cold-pressed rapeseed oils and ambient sauces rely on glass’s oxygen impermeability, though plastic pouches pressure unit pricing in mass channels. Pharmaceutical demand remains stable, guided by pharmacopoeia requirements for inertness and opacity, while perfumery holds niche status but commands premium per-unit pricing aligned with brand storytelling imperatives.

Note: Segment shares of all individual segments available upon report purchase

By Color: Flint Clings to Leadership While Amber Accelerates

Flint maintained 61.10% UK container glass market share in 2025 on the strength of clear spirits, white wine, and personal-care adoption, where product visibility is non-negotiable. Lightweighting progress now allows 700 mL gin bottles under 200 g, narrowing logistics cost gaps with PET and reinforcing flint’s commercial viability for mid-price SKUs.

At the same time, the UK container glass market size for amber bottles is set to climb from 840 kilotons in 2026 to 1.03 kilotons by 2031, delivering a 4.08% CAGR fuelled by hop-intensive craft beer and vitamin-infused oils that demand UV filtration. Green glass preserves its role in traditional claret, Burgundian, and sparkling wine supply chains but records minimal share gains as producers trial lighter tint options. Niche colors cobalt, matte black, and frosted pastel surface in limited-edition spirits and indie beauty launches, underscoring how glass coloration operates as a storytelling canvas rather than a pure functional decision.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Production capacity clusters around historical glass corridors in Northwest England, Yorkshire, and central Scotland, collectively accounting for more than two-thirds of domestic output. Encirc’s dual-furnace facility in Chester handles bulk beer and food jars, leveraging multimodal rail links to reduce inbound cullet freight distances. Verallia UK operates four furnaces across Leeds and Knottingley that specialise in short-run premium spirits packaging for Scotch whisky houses, gin startups, and CBD oil fillers, creating high-margin niches insulated from continental import competition.

Scotland itself drives disproportionate demand via its GBP 7.8 billion whisky export engine, spurring bottle design partnerships that often involve Gaelic motifs and provenance calligraphy. Northern England, specifically St Helens, hosts NSG Group’s hydrogen-ready pilot tank, positioning the region at the forefront of low-carbon glass R&D. London and the Southeast serve as the UK’s primary consumption basin, channeling luxury imports and e-commerce fulfilment that require robust, aesthetically appealing bottles for same-day delivery services.

Wales and Southwest England witness an upsurge in boutique gin distilleries and cider mills, translating to hyper-localised bottle orders and a dispersal of demand beyond historical industrial heartlands. Post-Brexit logistics realignments have increased customs friction on continental glass imports, yet standard wine bottle flows from France and Spain remain cost-competitive for volume SKUs due to freight efficiencies on return lanes. This dichotomy reinforces domestic manufacturing relevance for bespoke, brand-critical containers while import corridors satisfy commodity demand.

Competitive Landscape

Market Concentration

The competitive field comprises four multinationals controlling 68% of tonnage alongside agile independents focusing on niche design and regional service. Ardagh Group reported a 7-8% revenue decline in its European glass division for 2024 amid energy price spikes and restructuring charges that triggered covenant negotiations with bondholders.[3]Ardagh Group, “Financial Results Q2 2024,” ardaghgroup.com O-I Glass trimmed UK headcount by 8% yet ploughed GBP 46 million (USD 58 million) into Alloa’s hybrid furnace upgrade that cuts gas consumption by 20%, signalling a strategy of shuttering non-core capacity while doubling down on sites with retrofit potential.

Verallia’s 2022 acquisition of Allied Glass rebranded the operation as Verallia UK and sharpened strategic focus on premium spirits, though first-half 2024 volumes lagged due to whisky destocking cycles. Encirc benefits from adjacency to a hydrogen cluster that could unlock meaningful carbon abatement and preferential buyer agreements once scope-3 criteria tighten. Independents such as Croxsons and Beatson Clark exploit service agility, offering mid-thousand-unit MOQ and integrated closure sourcing to craft producers that often feel underserved by conglomerates.

Innovation priorities across the cohort concentrate on glass foam cushioning, digital embossing for anti-counterfeit features, and cloud-linked cullet traceability that feeds EU CSRD reporting needs. Competitive success in the UK container glass market, therefore, hinges as much on ESG credentials and design responsiveness as on melting capacity, creating a strategic landscape where lean yet technologically progressive players can rival scale-driven incumbents.

United Kingdom Container Glass Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Stoelzle UK experienced a major furnace fire that halted output for five weeks, prompting spirits bottlers to revisit dual-sourcing strategies.

- March 2024: Verallia commissioned the world’s first 100% electric furnace in Cognac, trimming CO2 emissions 60% versus gas-fired benchmarks.

- February 2024: Verallia agreed to acquire Vidrala’s Italian assets for EUR 230 million (USD 248 million), signalling pan-European consolidation and potential bottle cross-supply into the UK.

- February 2024: Diageo achieved a cumulative 3,000-tonne glass reduction across flagship whisky lines through bottle light-weighting.

Table of Contents for United Kingdom Container Glass Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Increased demand for premium alcoholic beverages

- 4.2.2Shift toward recyclable packaging by major UK retailers

- 4.2.3Growth of craft spirits and micro-breweries

- 4.2.4Adoption of lightweight glass technology

- 4.2.5Government recycling‐rate targets for 2030

- 4.2.6Rise in e-commerce demand for durable primary packaging

- 4.3Market Restraints

- 4.3.1Competition from PET and aluminium cans

- 4.3.2High energy costs and carbon-emission levies

- 4.3.3Raw-material supply-chain disruptions (soda ash, cullet)

- 4.3.4Furnace-maintenance downtime causing periodic shortages

- 4.4PESTEL Analysis

- 4.5Industry Supply-Chain Analysis

- 4.6Container Glass Furnace Capacity and Locations in United Kingdom

- 4.6.1Plant Locations and Year of Commencement

- 4.6.2Production Capacities

- 4.6.3Types of Furnaces

- 4.6.4Color of Glass Produced

- 4.7Export-Import Data of Container Glass - Covering Key Import and Export Destinations

- 4.7.1Import Volume and Value, 2021-2024

- 4.7.2Export Volume and Value, 2021-2024

- 4.8Porter’s Five Forces Analysis

- 4.8.1Threat of New Entrants

- 4.8.2Bargaining Power of Suppliers

- 4.8.3Bargaining Power of Buyers

- 4.8.4Threat of Substitutes

- 4.8.5Competitive Rivalry

- 4.9Raw Material Analysis

- 4.10Recycling Trends for Glass Packaging

- 4.11Demand vs Supply Analysis for Glass Packaging

5. MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1By End-user

- 5.1.1Beverages

- 5.1.1.1Alcoholic

- 5.1.1.1.1Beer

- 5.1.1.1.2Wine

- 5.1.1.1.3Spirits

- 5.1.1.1.4Other Alcoholic Beverages (Cider and Other Fermented Drinks)

- 5.1.1.2Non-Alcoholic

- 5.1.1.2.1Juices

- 5.1.1.2.2Carbonated Drinks (CSDs)

- 5.1.1.2.3Dairy Product Based Drinks

- 5.1.1.2.4Other Non-Alcoholic Beverages

- 5.1.2Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles)

- 5.1.3Cosmetics and Personal Care

- 5.1.4Pharmaceuticals (excluding Vials and Ampoules)

- 5.1.5Perfumery

- 5.2By Color

- 5.2.1Green

- 5.2.2Amber

- 5.2.3Flint

- 5.2.4Other Colors

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves and Developments

- 6.3Company Market Share Analysis, (Based on Latest Production Capacity)

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Ardagh Group S.A.

- 6.4.2Encirc Limited

- 6.4.3O-I Glass Limited

- 6.4.4Beatson Clark Limited

- 6.4.5Verallia UK Limited

- 6.4.6Vidrala S.A.

- 6.4.7Stoelzle Flaconnage Limited

- 6.4.8Ciner Glass Ltd

- 6.4.9Glassworks International Limited

- 6.4.10Berlin Packaging UK Ltd

- 6.4.11Gaasch Packaging Ltd

- 6.4.12Gerresheimer UK Ltd

- 6.4.13Frigoglass UK Ltd

- 6.4.14Consol Glass UK Ltd

- 6.4.15LuxGlass Ltd

- 6.4.16Vetropack UK Ltd

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-space and Unmet-Need Assessment

United Kingdom Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

United Kingdom container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery), by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.