Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

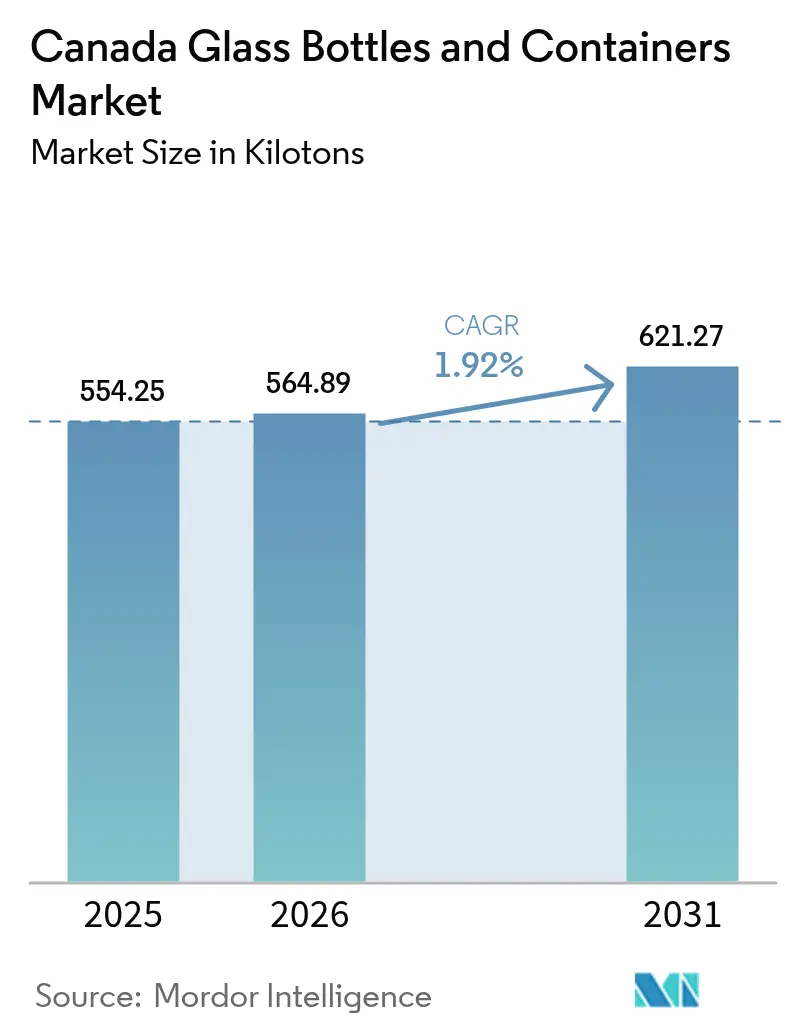

| Base Year Market Size (2025) | 554.25 kilotons |

| Market Volume (2026) | 564.89 kilotons |

| Market Volume (2031) | 621.27 kilotons |

| Growth Rate (2026 - 2031) | 1.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Glass Bottles And Containers Market Analysis by Mordor Intelligence

The Canada glass bottles and containers market size is expected to grow from 554.25 kilotons in 2025 to 564.89 kilotons in 2026 and is forecast to reach 621.27 kilotons by 2031 at 1.92% CAGR over 2026-2031. Demand growth rests on rising provincial recycling mandates, premium-product packaging needs, and incremental furnace-efficiency gains that offset raw-material inflation. Brand owners continue shifting to glass to comply with extended producer responsibility (EPR) rules and to reinforce sustainability narratives that resonate with urban consumers willing to pay a 15–25% packaging premium. Deposit-return expansion in Quebec and British Columbia is tightening closed-loop supply chains, spurring investment in cullet processing even as contamination shortfalls keep roughly 20,000 tonnes of glass out of recycling streams annually. Cost pressures persist: Statistics Canada reported a 4.5% year-to-date hike in producer price indexes for glass manufacturing in 2024, prompting furnace lightweighting and higher cullet ratios to reduce melting energy requirements. Meanwhile, Canada’s Clean Electricity Regulations (CER) compel plants to begin decarbonization planning that favors electric furnaces and renewable-power procurement, reshaping long-term capital-allocation decisions.

Key Report Takeaways

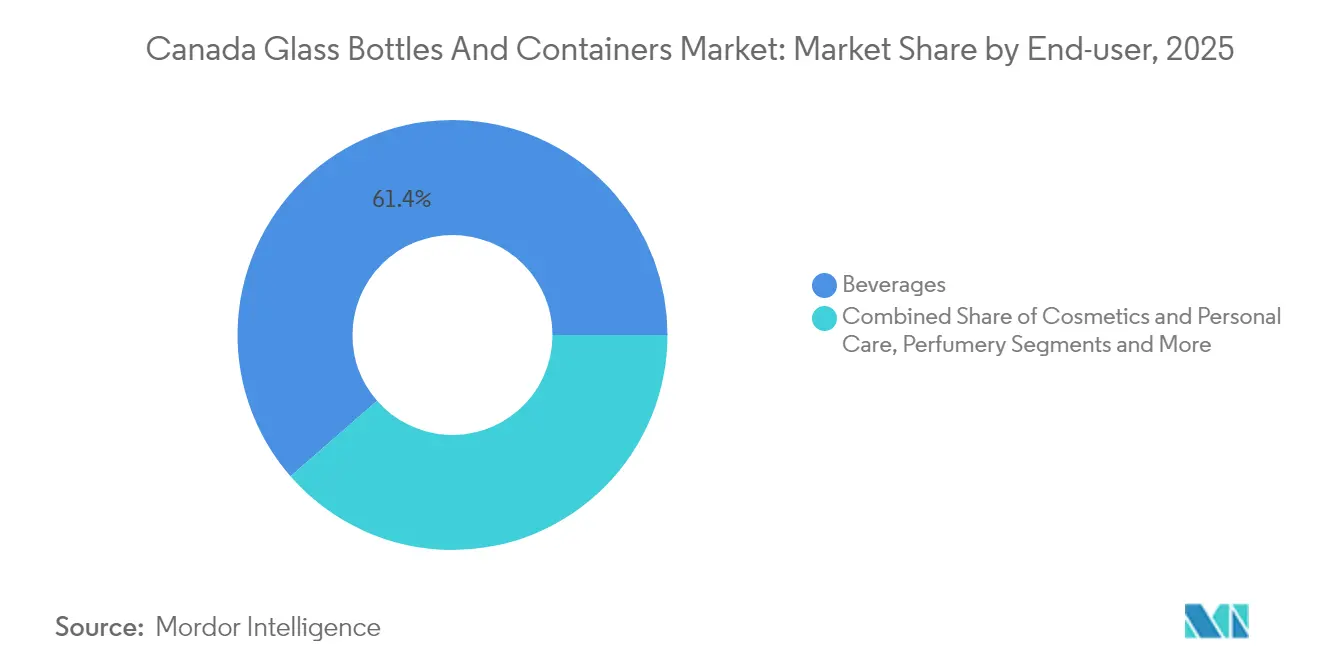

- By end-user, beverages captured 61.42% of the Canada glass bottles and containers market share in 2025.

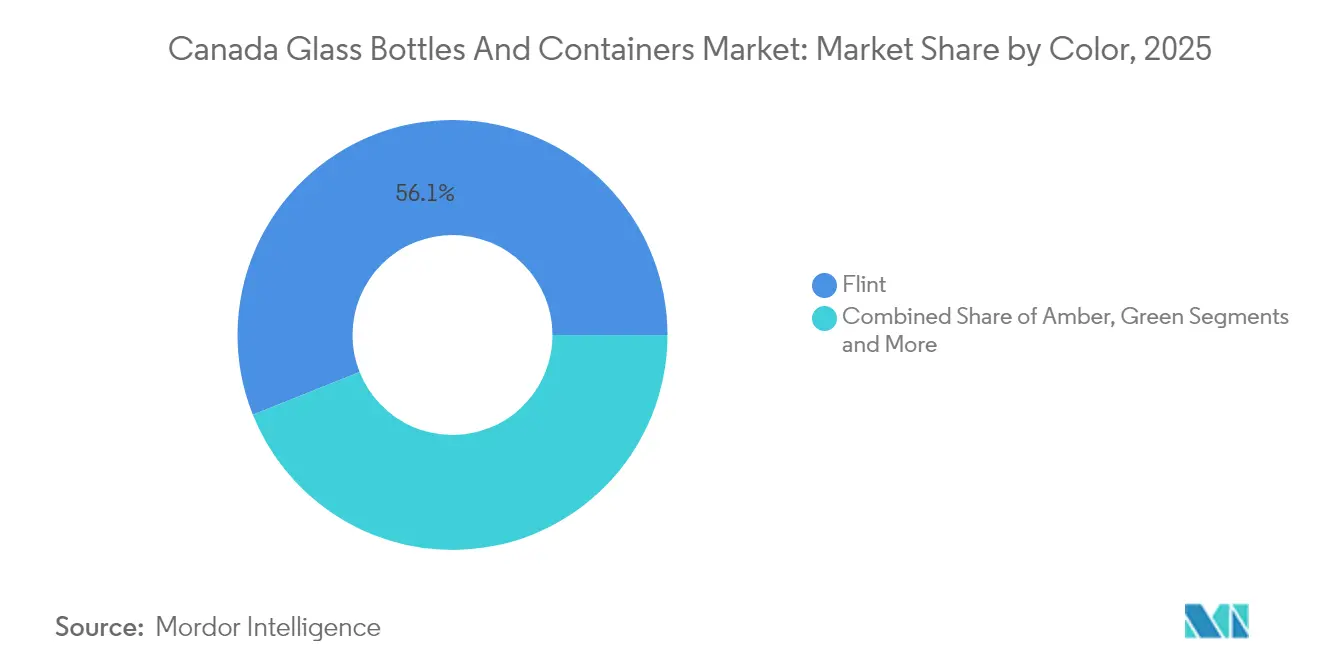

- By color, the Canada glass bottles and containers market for amber glass is projected to grow at a 2.51% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Glass Bottles And Containers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer and regulatory pressure for eco-friendly packaging | +0.6% | National, with early gains in Quebec, Ontario, British Columbia | Medium term (2-4 years) |

| Growth in premium beverages and luxury cosmetics | +0.4% | National, concentrated in urban markets | Short term (≤ 2 years) |

| Recyclability and Circular Economy | +0.3% | National, spill-over to export markets | Long term (≥ 4 years) |

| Technological Advancements in Glass Manufacturing | +0.2% | National, focused on major production centers | Medium term (2-4 years) |

| Rise in Craft and Artisanal Product Segments | +0.3% | National, with concentration in Ontario, Quebec, British Columbia | Short term (≤ 2 years) |

| Government Regulations Favoring Glass Packaging | +0.4% | National, with provincial variations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer and Regulatory Pressure for Eco-Friendly Packaging

British Columbia’s 2024 amendment broadening producer liability and the March 2025 Quebec deposit-return expansion have pushed brand owners to accelerate glass adoption across beverages, food, and personal care categories. Surveys show that in major cities, consumers now accept 15–25% price premiums for products in glass rather than plastic without volume declines. The same legislation embeds design-for-recyclability requirements that favor glass, whose infinite recyclability delivers regulatory certainty. Growing EPR targets across Atlantic provinces further ratchet compliance costs for non-recyclable formats, reinforcing glass’s attractiveness. Together these measures underpin steady demand growth for the Canada glass bottles and containers market.

Growth in Premium Beverages and Luxury Cosmetics

Custom mold fees ranging from USD 15,000 to USD 75,000 illustrate how craft distillers and high-end personal-care brands treat glass as a centerpiece of product storytelling. Cosmetics now represent the fastest-growing end-use, expanding at a 2.46% CAGR on the back of Health Canada sealing requirements and consumer perceptions linking glass with formulation purity. Spirits, kombucha, and functional beverages use bespoke bottle geometries and decoration to justify higher shelf prices, shifting competitive focus from volume to design services. This value-added pivot helps buffer producers against commodity price swings while bolstering revenue per ton for the Canada glass bottles and containers market.

Recyclability and Circular Economy Commitments

Large producers have pledged cullet utilization rates far above the North American average. O-I Glass’s 2024 partnerships allow 80–90% recycled content in new containers, versus a regional mean nearer to 35%. Enhanced optical-sorting and AI-vision systems improve color purity and contamination control, lowering furnace energy use by roughly 2-3% for every 10% cullet increment. Government procurement frameworks outlined in PRIMA Québec’s 2035 Roadmap incentivize circular-design specifications, reinforcing end-market demand for high-recycled-content bottles. The outcome is a structural pull on post-consumer glass streams that supports long-run expansion of the Canada glass bottles and containers market.

Technological Advancements in Glass Manufacturing

Early pilots of electric furnaces cut direct CO₂ by about 0.7 t per ton of cullet melted and extend furnace life, positioning adopters for forthcoming CER compliance. Lightweighting initiatives have trimmed bottle mass by 10-15% since 2024, reducing logistics costs while retaining tactile quality. Digital twins and fast-cycle prototyping shorten design timelines for premium segments, letting manufacturers capture higher-margin custom work. These improvements underpin productivity gains and margin resilience for the Canada glass bottles and containers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Domestic Production Capacity | -0.4% | National, concentrated in Ontario manufacturing centers | Short term (≤ 2 years) |

| High Raw Material and Energy Costs | -0.5% | National, with regional energy cost variations | Medium term (2-4 years) |

| Competition from Alternative Packaging | -0.3% | National, varying by application segment | Long term (≥ 4 years) |

| Fragility and Transportation Risks | -0.2% | National, amplified by geographic distances | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Domestic Production Capacity

Only a handful of plants, including O-I Glass in Brampton, Stanpac in Smithville, and Richards Packaging in Maple, cover most national demand, pushing utilization close to nameplate limits during peak seasons. Import dependence for specialty colors and custom runs exposes buyers to U.S. dollar swings and logistics bottlenecks. New furnaces entail USD 180 million–USD 220 million outlays with decade-plus payback horizons, delaying expansion even as premium-segment demand rises. Until new investments materialize, capacity tightness will temper growth for the Canada glass bottles and containers market.

High Raw-Material and Energy Costs

Energy accounts for roughly 17% of finished-glass costs, and 2024 saw a 4.5% spike in producer-price indexes for the sector. Soda ash, silica sand, and limestone price inflation compressed margins because producers could not fully pass through surcharges instantly. As CER drives utilities toward costlier renewable mixes, electricity rates are expected to remain above historical averages, challenging profitability. These dynamics curb near-term momentum in the Canada glass bottles and containers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Anchor Volume While Cosmetics Drive Margins

Beverages retained 61.42% of Canada glass bottles and containers market share in 2025, buoyed by entrenched wine and spirits usage and burgeoning craft categories. Cosmetics and personal care, while smaller in tonnage, achieved the fastest 2.33% CAGR and now command premium unit revenues, reflecting stricter hermetic-seal rules under Health Canada and consumer affinity for prestige packaging.

Growth in the beverage segment remains linked to deposit-return expansion and craft innovation, but margin uplift is increasingly tied to high-design cosmetics jars and droppers that leverage decoration and embossing services. Premium juice, kombucha, and functional drinks also shift toward glass to spotlight freshness, reinforcing downstream demand stability for the Canada glass bottles and containers market.

By Color: Flint Dominance Meets Rapid Amber Uptake

Flint bottles accounted for 56.05% of 2025 volume thanks to universal applicability and easier cullet sorting. Amber containers, favored by craft beer and premium spirits for UV protection, are set to outpace overall demand at a 2.51% CAGR through 2031, signaling design differentiation as a lasting competitive lever.

Investments in small-batch color runs and hybrid coating technologies allow producers to serve niche green, cobalt, and graduated-tint demands without sacrificing recyclability. These advancements widen the addressable opportunity set for the Canada glass bottles and containers market while supporting higher average-selling prices.

Geography Analysis

Ontario and Quebec comprise the manufacturing nucleus and the bulk of demand, underpinned by population density and provincial EPR leadership. O-I’s Brampton hub supplies national beverage fillers clustered in the Greater Toronto Area, lowering freight-to-value ratios.

Quebec’s March 2025 deposit-system overhaul effectively monetizes cullet retrieval, spurring innovation in automated sort lines and pilot traceability apps that may become national blueprints. Western provinces, though smaller, show outsized growth tied to thriving craft beverage ecosystems in Vancouver, Victoria, and Edmonton; lacking local furnaces, these markets depend on inbound rail shipments or U.S. imports.

Atlantic Canada leverages unified EPR frameworks to pool collection volumes, creating scale for cullet processing while port proximity eases export logistics for specialty containers.Collectively, these regional variations keep the Canada glass bottles and containers market firmly oriented around policy shifts and freight economics.

Competitive Landscape

The market exhibits moderate concentration. O-I Glass leads with large-scale furnace capacity and vertically integrated cullet networks, while Verallia North America supplies niche wine bottles through cross-border flows. Mid-tier contenders Richards Packaging, Stanpac, and TricorBraun focus on premium and custom niches, often augmenting design services via acquisitions such as TricorBraun’s 2024 purchase of Veritiv Containers.

Technology adoption is rising: Richards Packaging is piloting AI-enabled sorters that boost cullet purity for flint flasks sold to artisanal gin producers. Stanpac, aided by provincial funding, doubled milk-bottle output on a new low-carbon annealing line in 2024.[3]Stanpac Inc., “Corporate Information and Government Partnerships,” stanpac.com These moves reflect a shift from tonnage-driven competition to differentiated service models supporting the Canada glass bottles and containers market.

Importantly, decarbonization spend is emerging as a moat. Early electric-furnace adopters lock in CER compliance cost advantages, whereas laggards face potential carbon surcharges post-2030. Access to recycled feedstock and lightweighting IP will therefore help define leadership over the forecast horizon.

Canada Glass Bottles And Containers Industry Leaders

O-I Glass, Inc.

Vitro, S.A.B de C.V

Verallia North America

Roy + LeClair Inc.

Richards Packaging Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: O-I Glass launched regional collection partnerships that target 90% recycled-content bottles by 2027.

- December 2024: PRIMA Québec published its 2035 advanced-materials roadmap, prioritizing glass traceability pilots and circular-economy accelerators.

- December 2024: Environment and Climate Change Canada finalized CER, mandating net-zero electricity generation by 2050.

- June 2024: TricorBraun completed the Veritiv Containers acquisition to scale its Canadian distribution footprint.

- January 2024: British Columbia broadened Recycling Regulation producer definitions, elevating compliance stakes for glass packagers.

Canada Glass Bottles And Containers Market Report Scope

Glass containers are vessels made from glass used to store and protect products such as food, beverages, pharmaceuticals, cosmetics, and chemicals. Available in diverse shapes and sizes, such as bottles, jars, and vials, these containers provide airtight seals and protect contents from external contaminants. Glass packaging is valued for its non-reactive nature, preservation of product quality, and high recyclability. These attributes make glass containers a preferred choice for packaging across multiple industries.

The Canada ccontainer glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The market sizes and forecasts are provided in terms of volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Canada glass bottles and containers market in 2026?

The market reached 564.89 kilotons in 2026 and is forecast to rise to 621.27 kilotons by 2031.

Which end-use segment grows fastest through 2031?

Cosmetics and personal care lead with a 2.33% CAGR, outpacing beverages and food.

Why is amber glass demand accelerating?

Craft breweries and premium spirits prioritize amber for UV protection and brand differentiation, driving a 2.51% CAGR for amber containers.

What regulations most influence future glass demand?

Quebec’s expanded deposit-return system and Canada’s Clean Electricity Regulations shape recovery incentives and manufacturing costs.

How concentrated is domestic production capacity?

A handful of plants chiefly O-I Glass in Brampton and regional players like Richards Packaging supply most national demand, yielding a concentration score of 6.

What role does cullet play in cost control?

Each 10% rise in cullet reduces furnace energy needs by 2-3%, helping plants offset energy-price volatility while meeting sustainability targets.

Page last updated on: