Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

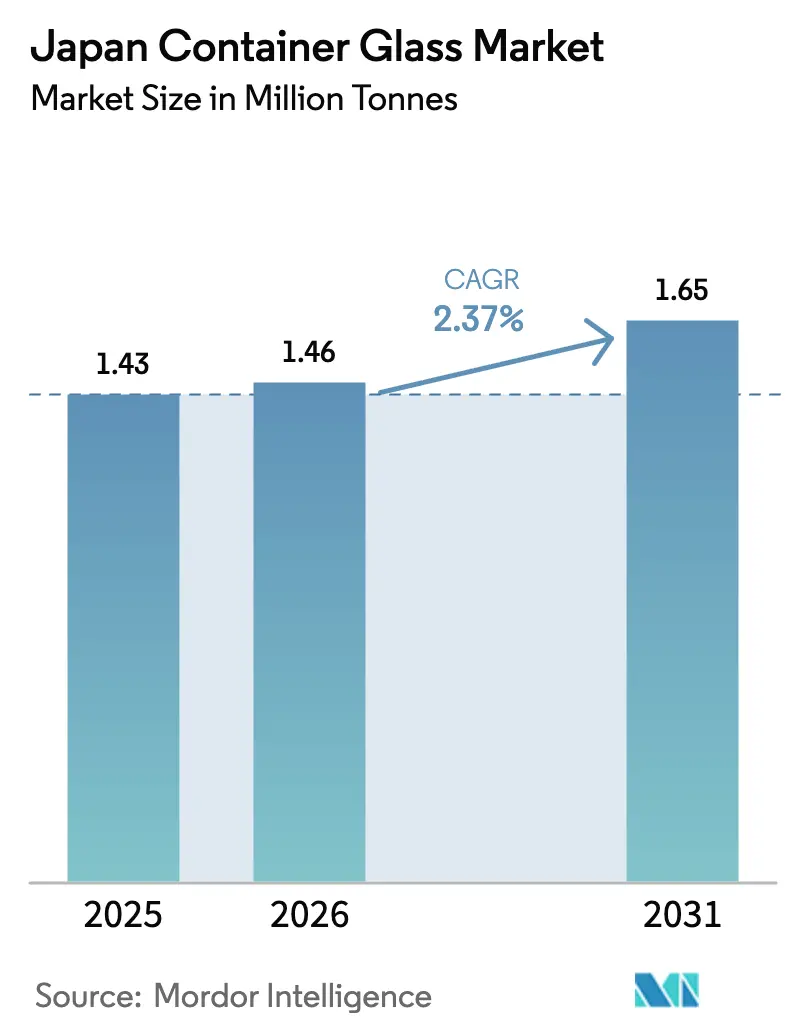

| Base Year Market Size (2025) | 1.43 Million tonnes |

| Market Volume (2026) | 1.46 Million tonnes |

| Market Volume (2031) | 1.65 Million tonnes |

| Growth Rate (2026 - 2031) | 2.37% CAGR |

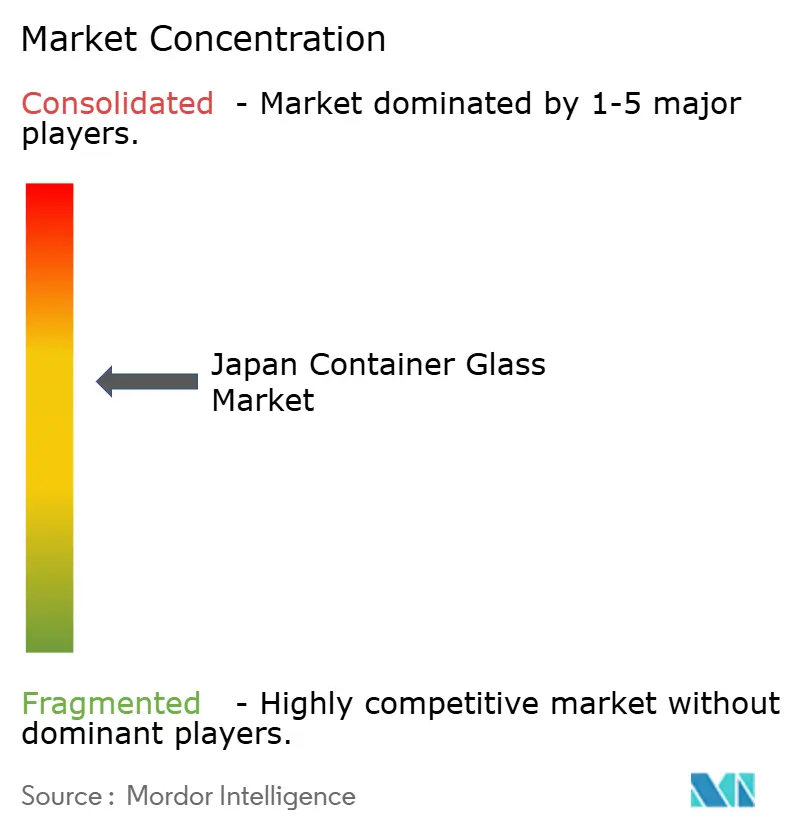

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Japan Container Glass Market Analysis by Mordor Intelligence

The Japan Container Glass Market size is expected to grow from 1.43 million tonnes in 2025 to 1.46 million tonnes in 2026 and is forecast to reach 1.65 million tonnes by 2031 at 2.37% CAGR over 2026-2031. Healthy volumes continue despite intense competition from lightweight polymers because glass delivers premium shelf appeal, meets stringent pharmaceutical quality norms, and aligns with Japan’s circular-economy policies. Premium alcoholic beverages and export-oriented brewers retain glass for brand authenticity, while regulatory scrutiny of per- and polyfluoroalkyl substances (PFAS) shifts some food-contact applications back toward glass. Manufacturers counter energy cost pressures through furnace electrification, hydrogen fuel trials, and lightweight bottle designs, which collectively stabilize margins. Meanwhile, a well-established glass-to-glass recycling loop supplies high-grade cullet that cushions raw-material inflation and supports national waste-reduction targets.

Key Report Takeaways

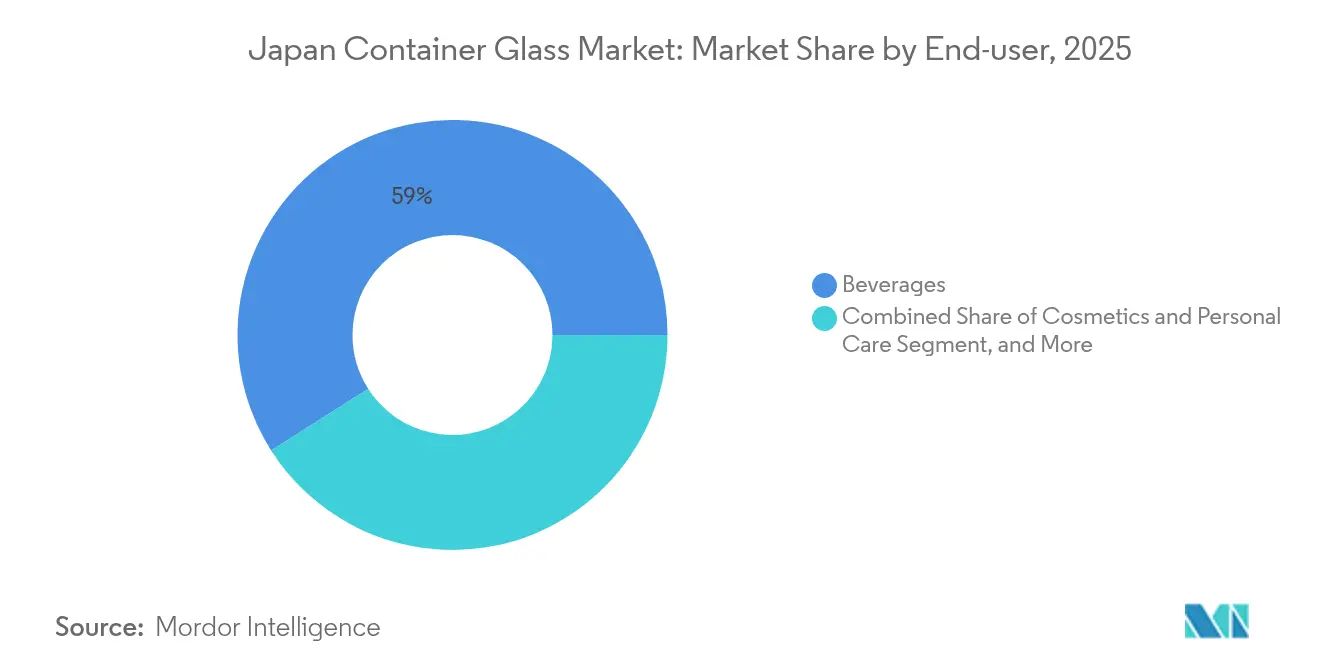

- By end-user, beverages captured 59.02% of the Japan container glass market share in 2025.

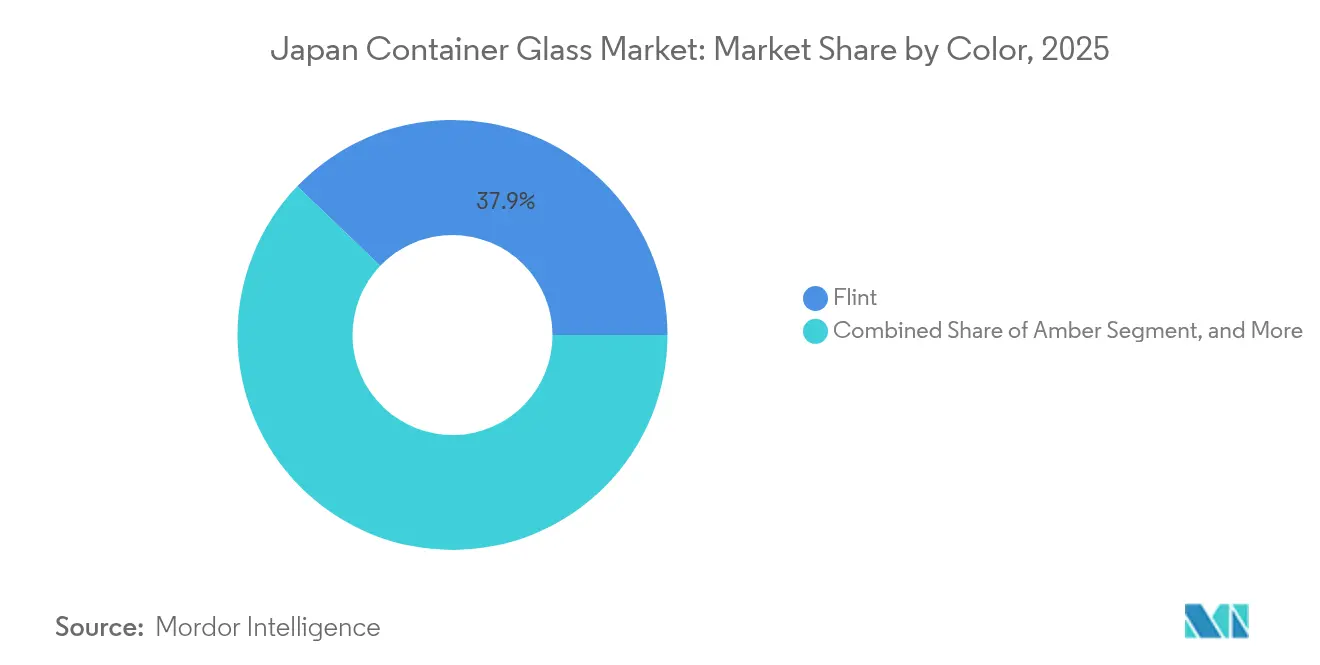

- By color, the Japan container glass market size for the amber glass segment is projected to grow at 4.42% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Japan Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Sustainability and Regulatory Support | +0.6% | National, with early gains in Tokyo, Osaka metropolitan areas | Medium term (2-4 years) |

| Premium Branding and Product Differentiation | +0.5% | National, concentrated in urban consumption centers | Long term (≥ 4 years) |

| Robust Growth in Beverage and Alcoholic Drink Segments | +0.4% | National, with export spillover effects | Short term (≤ 2 years) |

| Rising Demand in Pharmaceuticals and Personal Care | +0.3% | National, with manufacturing clusters in Kansai region | Medium term (2-4 years) |

| Technological Advancements in Glass Manufacturing - Energy Efficiency | +0.2% | National, focused at major production facilities | Long term (≥ 4 years) |

| Technological Advancements in Glass Manufacturing - Product Innovation | +0.2% | National, with R&D centers leading adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Sustainability and Regulatory Support

Japan’s glass producers benefit from a policy mix that elevates glass as the most circular rigid-packaging substrate. The Glass Bottle Recycling Mark scheme grows cullet recovery rates, and emerging PFAS controls accentuate glass’s inert nature in food contact settings.[1]AGC Inc., “AGC Glass Europe and ROSI Announce Strategic Partnership,” agc.com Nationwide waste-reduction targets encourage retailers to specify minimum recycled-content thresholds that glass can meet without quality loss. Energy-conservation mandates also incentivize furnace-rebuild projects that integrate electrical boosting, which cuts overall fuel intensity and unlocks carbon-price credits. Public sentiment favors plastic-waste reduction, creating an enduring demand pull that cushions the Japan Container Glass market against polymer substitution in sensitive categories.

Premium Branding and Product Differentiation

Brand owners leverage the tactile and visual cues of glass to justify premium shelf prices. Craft soft-drink maker Hata Kōsen revived its all-glass Ramune bottle after a 30-year hiatus, capitalizing on nostalgia and sensory ritual to command case prices of JPY 7,776 (USD 53.7). In cosmetics, small-batch glass jars enable intricate embossing and color-spray effects that mass-market plastics cannot replicate at low volumes. Breweries maintain heavy glass formats for flagship beers abroad because exporters note a direct link between glass bottling and perceived authenticity. The design latitude benefits specialty converters that offer limited-run, high-margin orders, supporting a bifurcated competitive landscape.

Robust Growth in Beverage and Alcoholic Drink Segments

Japan’s brewers pursue double-digit export growth while retaining glass to reinforce heritage cues in overseas markets. Sake export revenue climbed to JPY 43.47 billion (USD 0.30 billion) in 2024, a 5.8% year-over-year rise, with premium labels shipped almost exclusively in glass flasks. Domestically, craft beer, ready-to-drink cocktails, and artisanal kombucha broaden glass’s beverage footprint even as mainstream soft-drink lines migrate to bio-PET. These export-driven and niche-premium gains offset demographic headwinds from Japan’s aging population, maintaining a stable demand floor for the Japan Container Glass market.

Rising Demand in Pharmaceuticals and Personal Care

Stringent drug-stability requirements keep vials, cartridges, and ampoules firmly glass-anchored. SCHOTT Pharma recorded 54% growth in its drug-delivery division, underscoring global appetite for prefillable syringes made from specialized borosilicate glass.[2]SCHOTT Pharma, “SCHOTT Pharma Delivers on 2023 Targets,” schott-pharma.com Japanese vial converters adopt protective labeling systems such as Iwata Label’s VPP2 to reduce particulate shedding and uphold clean-room compliance. In personal care, sustainability-minded consumers accept heavier glass jars in exchange for perceived purity and recyclability. Together, these applications add incremental tonnage that cushions cyclical swings in food or beverage glass demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Energy and Production Costs | -0.4% | National, concentrated at major production facilities | Short term (≤ 2 years) |

| Intense Competition from Substitute Packaging Materials | -0.3% | National, with urban markets most affected | Medium term (2-4 years) |

| Fragility and Risk of Breakage During Handling and Transport | -0.2% | National, with higher impact in remote distribution areas | Medium term (2-4 years) |

| Supply Chain Vulnerabilities and Raw Material Constraints | -0.3% | National, with import-dependent facilities most exposed | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy and Production Costs

Fuel and electricity account for more than one-third of furnace operating expenses. Natural-gas import prices spiked after 2022, and a weak yen inflated soda-ash and additive costs, compressing margins for commodity bottle lines.[3]Statistics Bureau, “Statistical Handbook of Japan 2024,” stat.go.jp Furnace rebuilds that integrate oxy-fuel or electric-boosting technology demand capex outlays that can reach USD 400 million, prolonging payback horizons. Although some producers test hydrogen blends, supply-chain scale remains limited, and carbon-price offsets have yet to fully compensate higher fuel bills. These dynamics weigh on near-term profitability and could slow capacity additions within the Japan Container Glass market.

Intense Competition from Substitute Packaging Materials

Advances in bio-based and chemically recycled PET lower the environmental gap with glass while retaining weight and logistics advantages. Suntory’s bio-PET road-map targets 100% plant-derived resin for flagship drinks, and bottle weights now dip below 20 g for 500 mL formats. Lightweight plastics erode glass’s share in cost-sensitive, high-turnover categories such as economy tea and functional beverages. Although glass retains niches tied to prestige and product integrity, polymer innovators continuously close performance gaps, restraining volume growth trajectories in the Japan Container Glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Retain Scale as Cosmetics Accelerate

The beverages domain occupied 59.02% of the Japan Container Glass market share in 2025, illustrating how entrenched drinking rituals and export ambitions underpin bulk volumes. Alcoholic brands continue to favor glass for flavor neutrality and premium heft, while ready-to-drink cocktails and craft sodas adopt custom bottles that amplify visual storytelling. Non-alcoholic mainstream lines have partly migrated to PET, yet smaller artisanal players counterbalance this slide by choosing glass to convey heritage and authenticity. Pharmaceutical demand remains steady because injectable drugs and vita-liquids require inert, impermeable primary containers. Cosmetics and personal care advance at a 3.18% CAGR, propelled by consumer willingness to pay for refillable glass jars that enhance bathroom aesthetics and reduce plastic waste. Food applications are split between premium condiments, where transparency reinforces quality cues, and commodity sauces that lean on plastic to save on transport costs. Perfumery, although niche, adds high-margin tonnage because brand owners demand complex shapes and color effects that only glass can sustain.

Continued beverage dominance ensures base-load furnace utilization, yet margin growth shifts toward specialty segments. Cosmetics formulators increasingly specify color-spray coatings, electroplated finishes, and low-profile neck finishes that smaller converters can deliver with agile tooling. Pharmaceutical suppliers uphold top-tier clean-room standards and hero products such as Type I borosilicate vials, which carry price premiums over standard soda-lime bottles. Export-oriented brewers and sake producers blend traditional bottle silhouettes with lightweight structures, showing that even volume-centric categories aim for material reduction. The Japan Container Glass market therefore evolves from a single-segment powerhouse toward a diversified demand portfolio that balances volume stability with premium revenue streams.

By Color: Flint Commands Visibility While Amber Gains Pharmaceutical Momentum

Flint containers captured 37.85% of the Japan Container Glass market in 2025, their transparency showcasing liquid clarity in sake, shochu, craft sodas, and premium soy sauces. Brand managers leverage full-body shrink sleeves and direct-to-glass digital printing to add graphics without obscuring contents. Consumers equate visible product with freshness, sustaining Flint’s position despite light-exposure concerns. Amber bottles, meanwhile, post the highest 4.42% CAGR through 2031 as drug makers and craft breweries seek ultraviolet protection. Japan’s pharmacopoeia mandates amber vials for certain antibiotics and injectable vitamins, driving steady off-take. Craft beer exporters prefer amber to signal authenticity in Western markets, reinforcing aesthetic tradition while safeguarding hop-related compounds.

Green glass remains limited to wine and select liqueurs, where color harmonizes with brand heritage. Other hues cobalt, ruby, and frost finishes, serve high-end cosmetics and perfumery. Color choice plays into product storytelling: a smoky gray tint may suggest smoky whisky, while deep blue bottles evoke marine freshness in niche mineral waters. Production flexibility matters; multi-color forehearths allow rapid switchover without furnace idling, giving nimble producers a competitive edge. Overall, color dynamics illustrate how the Japan Container Glass market shifts from purely functional considerations toward marketing-driven aesthetics that motivate brand owners to absorb color-related cost uplifts.

Geography Analysis

The Kansai industrial corridor around Osaka and Hyogo hosts the lion’s share of melting capacity, capitalizing on proximity to recycled-glass processors, bottle decoration houses, and beverage fillers. Plants in this cluster enjoy integrated logistics, but elevated regional power tariffs prompt ongoing energy-efficiency upgrades. Tokyo and surrounding prefectures account for the largest consumption node, fueled by dense population, tourism inflows, and headquarters of cosmetics and pharmaceutical majors. Kanto-based fillers rely on high-speed rail and coastal shipping to draw bottles from Kansai, balancing inbound cullet flows from metropolitan recycling streams with outbound finished goods.

Kyushu and northern Honshu provide secondary melting sites that specialize in smaller bottle formats for regional craft breweries and shochu distilleries. These peripheral plants alleviate freight costs for fragile shipments and support local economies, yet their medium-scale furnaces face sharper cost exposure when energy prices spike. Coastal layouts near Kobe and Nagoya facilitate export containerization, enabling sake, beer, and soy sauce shippers to load palletized glass directly onto vessels bound for China, the United States, and Southeast Asia. Glass exports reached USD 649.28 million in 2024, underscoring the strategic importance of port-adjacent capacity.

Japan’s island geography complicates domestic distribution, prompting producers to favor regional depots and lightweight bottles to cut backhaul fuel burn. Urban recycling schemes supply a steady cullet stream, yet rural prefectures show lower collection yields, forcing long-haul cullet transport that dents sustainability metrics. Nonetheless, geographic concentration of technical know-how within traditional glass regions confers expertise advantages, even if it heightens local exposure to seismic events and labor shortages. The net outcome is a regionally balanced but capacity-dense network that supports the expansive needs of the Japan Container Glass market.

Competitive Landscape

Market concentration skews moderate: two integrated groups, Toyo Seikan Group Holdings and Nihon Yamamura Glass, anchor commodity supply, while a tier of specialists occupies cosmetics, pharma, and perfumery niches. Large players benefit from captive cap and label operations, enabling turnkey solutions that lock in beverage customers and mitigate margin erosion. Their scale supports multimillion-dollar furnace relines and hydrogen-trial pilots, positioning them favorably ahead of envisaged carbon-pricing schemes. Smaller converters such as Koa Glass, Ishizuka Glass, and Nipro’s vial division target high-complexity orders where agility outweighs scale, capturing premium margins through rapid design iterations and low minimum order quantities.

Strategic focus tilts toward sustainability. Yamamura Glass’s Reborn Cap project collects post-consumer closures, feeding them into recycled resin applications that complement glass’s circular narrative. Toyo Glass develops ultra-lightweight highball bottles, shaving up to 20% mass without compromising impact resistance, thereby reducing logistics emissions. Acquisition activity in adjacent substrates underscores wider packaging-sector consolidation: Sumitomo Bakelite’s purchase of AGC’s polycarbonate line signals broader material-agnostic portfolio building that could influence long-term competitive dynamics. Meanwhile, global mega-mergers such as the USD 15.7 billion Amcor-Berry deal raise the bar on purchasing power and R&D budgets, pressuring mid-sized Japanese players to differentiate or consolidate.

Customer intimacy and technical service remain decisive. Breweries demand on-site bottle-quality audits and rapid defect analysis, services that incumbent glassmakers have embedded within multi-decade relationships. Cosmetics brands seek custom molds with intricate embossing delivered within weeks; converters with 3D-printing prototyping equipment meet these expectations and lock in higher tooling fees. Pharmaceutical buyers insist on flawless inner-surface chemistry; suppliers respond with low-alkali borosilicate recipes and post-forming annealing controls. These specialized capabilities collectively sustain a competitive equilibrium where scale players guarantee volume security while niche firms supply high-value custom solutions, shaping the performance trajectory of the Japan Container Glass market.

Japan Container Glass Industry Leaders

Nihon Yamamura Glass Co. Ltd

Japan Seiko Glass Co., Ltd.

KOA Glass Co., LTD

Nihon Taisanbin Glass Bottle MFG, Co., Ltd.

Toyo Glass Co., Ltd. (Toyo Seikan Group Holdings, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nihon Yamamura Glass joined the Osaka-Kansai Expo 2025 TEAM EXPO Pavilion, highlighting its RIN plastic-recycling initiative that broadens the firm’s circular-economy services portfolio.

- July 2025: Sumitomo Bakelite agreed to acquire AGC Corporation’s polycarbonate business, strengthening its mobility materials offering and unlocking synergies in optical sheets.

- July 2025: Mitsuuroko Group Holdings commissioned a new mineral-water line in Shizuoka with PFAS-removal capability and throughput of 300 bottles per minute, doubling its packaged-water capacity.

- May 2025: Hata Kōsen launched HATA PREMIUM, returning all-glass Ramune bottles to Japan for the first time since 1989 and targeting premium on-premise channels.

Japan Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

The Japan container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What is the current size of the Japan Container Glass market?

The Japan Container Glass market size is 1.46 million tonnes in 2026 and is projected to reach 1.65 million tonnes by 2031.

Which end-user segment leads demand?

Beverages lead the market with 59.02% share in 2025, driven by premium alcoholic and export-oriented brands.

Which color segment is growing fastest?

Amber bottles post the highest 4.42% CAGR through 2031 thanks to pharmaceutical and craft-beverage adoption.

How are energy costs influencing producers?

Elevated gas and electricity prices push manufacturers toward furnace electrification and hydrogen-fuel trials to contain operating expenses.

Why do cosmetics brands prefer glass packaging today?

Glass conveys premium quality, supports refillable formats, and aligns with consumer sustainability expectations, enabling brands to charge higher prices.

What is the market concentration level in this sector?

The market scores 6 on a 10-point concentration scale because the top five players control slightly more than 60% of domestic container-glass volume.

Page last updated on: