Bare Metal Switch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

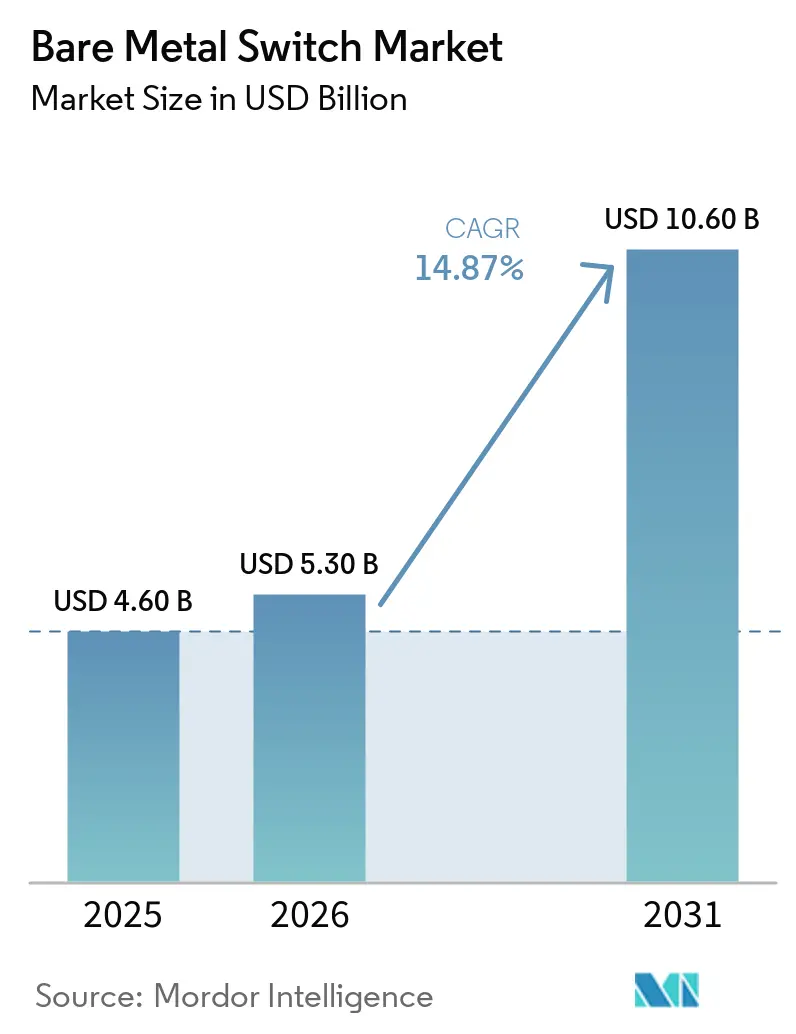

| Market Size (2026) | USD 5.30 Billion |

| Market Size (2031) | USD 10.60 Billion |

| Growth Rate (2026 - 2031) | 14.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bare Metal Switch Market Analysis by Mordor Intelligence

The bare metal switch market size is expected to grow from USD 4.6 billion in 2025 to USD 5.3 billion in 2026 and is forecast to reach USD 10.6 billion by 2031 at 14.87% CAGR over 2026-2031. Rising hyperscale data-center builds, wider availability of 400 Gbps and 800 Gbps merchant-silicon ports, and government-backed open-hardware mandates are accelerating disaggregation across spine-leaf fabrics. Cloud and telecom operators now treat the switch as a programmable commodity, shifting value toward network operating system innovation and silicon roadmap control. Price gaps of 30%-40% versus proprietary appliances continue to motivate large-scale refresh cycles, while sustainability rules in Europe and North America reward energy-efficient designs that cut rack power budgets.

Key Report Takeaways

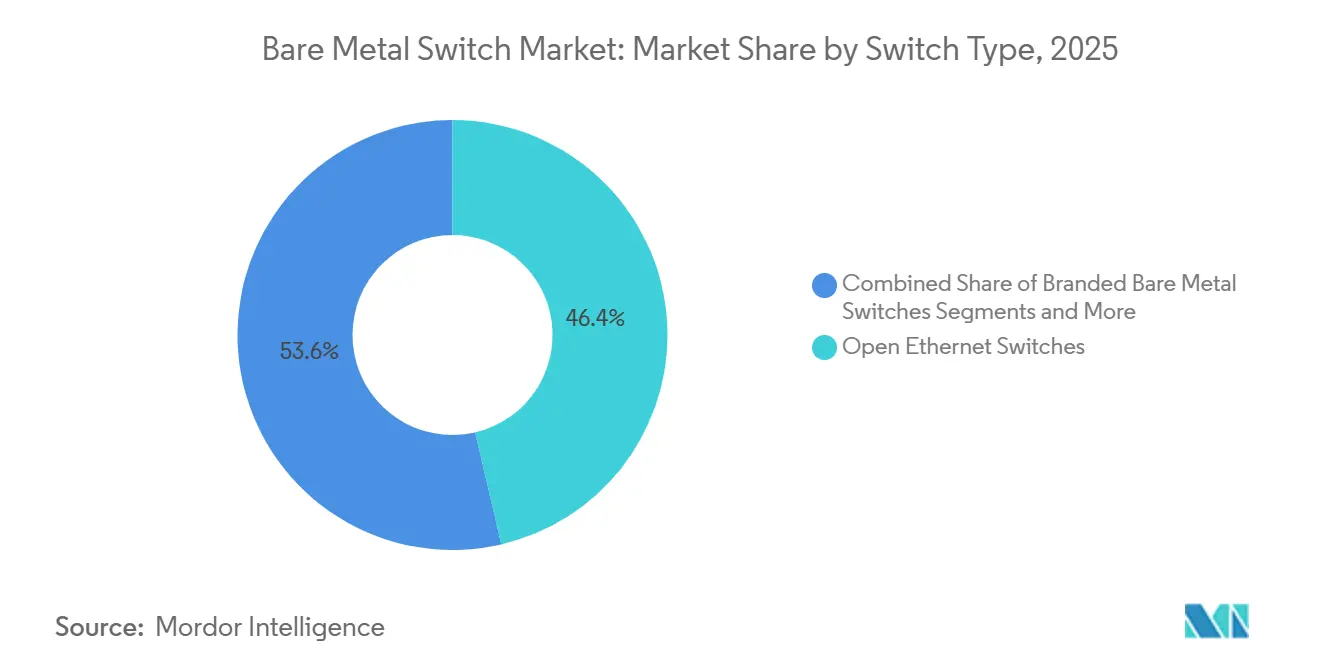

- By switch type, open Ethernet switches led with 46.36% of the bare metal switch market share in 2025.

- Branded bare metal switches are projected to post the fastest 18.53% CAGR through 2031.

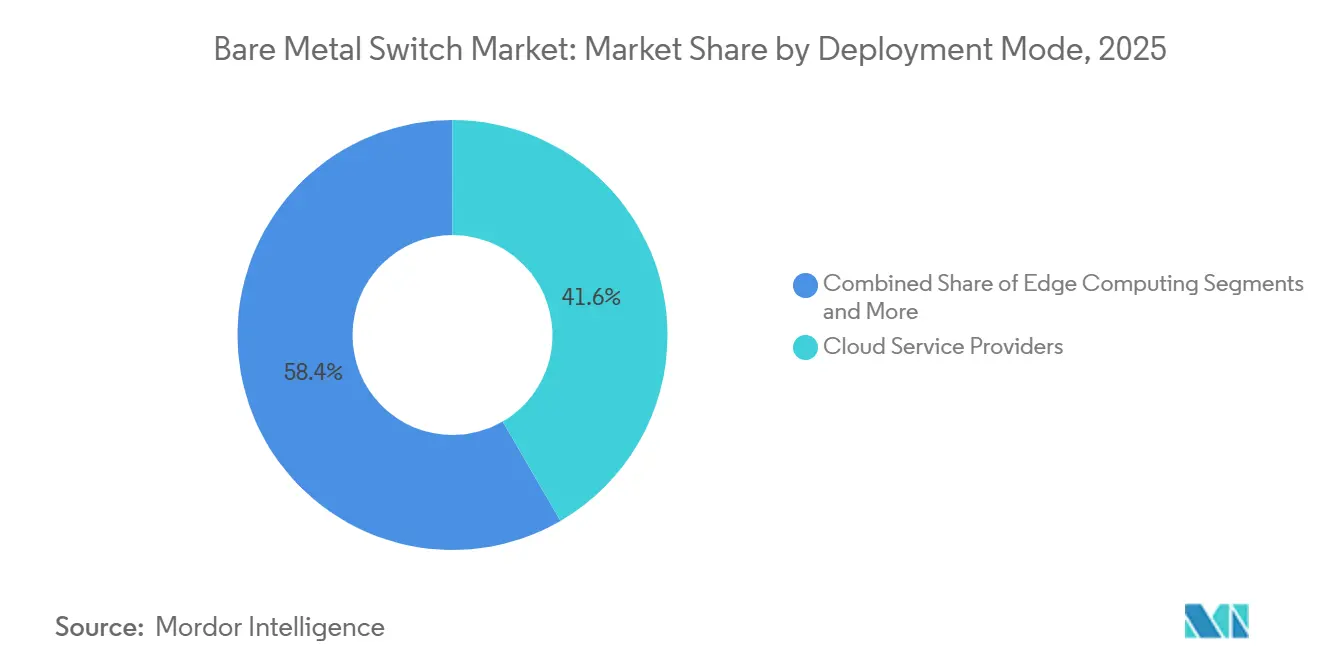

- By deployment mode, cloud service providers held 41.63% revenue share in 2025, whereas edge computing sites are advancing at a 20.32% CAGR between 2026 and 2031.

- By port speed, the 25/40 Gbps tier accounted for 38.49% of the bare-metal switch market in 2025, while the 200+ Gbps segment is expanding at a 25.26% CAGR through 2031.

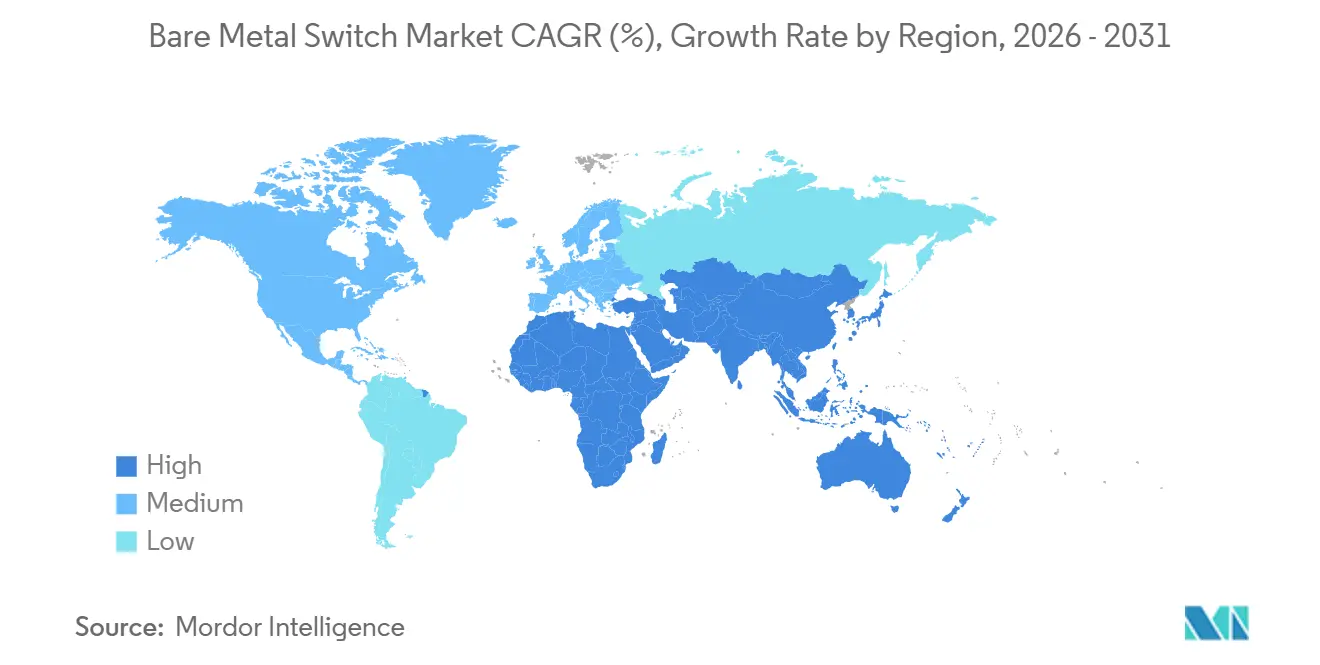

- Asia-Pacific captured 32.97% of 2025 revenue, yet the Middle East is forecast to register the fastest CAGR of 17.12% through 2031.

- Cloud providers represented 44.64% of end-user sales in 2025, but government and public-sector installations are growing at a 19.22% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bare Metal Switch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Disaggregated Networking in Hyperscale Data Centers | 4.20% | Global, concentration in North America and Asia-Pacific clusters | Medium term (2-4 years) |

| Cost Optimization Over Proprietary Switches | 3.10% | Global, acute in South America, Middle East and Africa | Short term (≤ 2 years) |

| Rapid Scalability Needs for Cloud-Native 5G Core Networks | 2.80% | Asia-Pacific core, spillover to Europe and Middle East telcos | Medium term (2-4 years) |

| Emergence of Telco Open RAN Fronthaul Transport Requirements | 2.30% | Global telcos, early traction in North America and Asia-Pacific | Long term (≥ 4 years) |

| Sustainability Mandates Driving Energy-Efficient Network Fabric Upgrades | 1.90% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Government-Backed Open Hardware Initiatives in Asia-Pacific | 1.40% | Asia-Pacific national programs, secondary influence in Middle East | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Disaggregated Networking in Hyperscale Data Centers

Hyperscale operators are embedding disaggregated networking into long-term capex models, treating switches as interchangeable building blocks rather than differentiated systems. Large-scale deployments of open NOS across more than 1 million devices have standardized ASIC platforms such as Broadcom Tomahawk and Marvell Teralynx across multiple global regions. Bare metal fabrics have reduced per-rack networking costs by approximately 38% while improving mean-time-to-repair through modular, hot-swappable components. High-performance architectures now achieve up to 1.6 Tbps per-rack throughput, matching the throughput of proprietary systems. These outcomes are accelerating ODM and cloud-provider co-development, shortening innovation cycles and reinforcing scale-driven cost efficiencies across the bare-metal switch market.[1]Meta Platforms, “2025 Infrastructure Update: Building for the Next Decade,” investor.fb.com

Cost Optimization Over Proprietary Switches

Enterprises and telecom operators are quantifying the total cost of ownership savings that extend beyond initial capex. A 2025 industry study indicates up to 42% lower five-year TCO with self-managed network operating systems, narrowing to about 18% when third-party support is included. Large telecom deployments have reported unit transport cost reductions of around USD 1200 per 100 Gbps port after shifting to open Ethernet switches. Pricing gaps widen significantly in the 200+ Gbps segment, where proprietary systems carry 60% to 80% premiums. This cost differential is accelerating migration toward 400 Gbps and 800 Gbps architectures, supporting sustained double-digit growth in the bare-metal switch market through 2031.[2]Bharti Airtel, “Annual Report 2024-2025,” airtel.in

Rapid Scalability Needs for Cloud-Native 5G Core Networks

Telecom operators are restructuring their core networks around containerized user-plane functions that scale horizontally. Large-scale deployments across hundreds of cities have demonstrated sub-5 ms latency while reducing power consumption per subscriber by about 22% compared with legacy circuit-switched systems. Fully virtualized mobile networks are achieving 99.99% uptime for millions of users, validating carrier-grade reliability on disaggregated hardware. European operators are standardizing on open NOS frameworks, such as SONiC, for 5G standalone cores to support multi-cloud orchestration. These proven deployment models are accelerating the adoption of bare-metal switches, particularly in the Asia Pacific and Europe, strengthening demand in the telecom segment.[3]Edgecore Networks, “Enterprise SONiC Distribution Launch,” edge-core.com

Emergence of Telco Open RAN Fronthaul Transport Requirements

Open RAN requires deterministic latency and precise time synchronization across distributed radio units, creating a segment where programmable bare-metal switches offer clear advantages. Large-scale deployments using IEEE 1588v2-capable switches have achieved sub-200 ns timing variance while reducing site transport costs by about 47% compared with CPRI architectures. Multi-country rollouts have integrated thousands of Open RAN sites, using bare-metal switches to support 25 Gbps fronthaul links. Field trials in dense urban environments have demonstrated massive MIMO readiness without proprietary timing hardware, lowering base-station bill of materials by roughly USD 3,400 per unit. These validated outcomes are strengthening long-term demand for bare metal switches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited In-House Integration Expertise Among Enterprises | -2.70% | Global, acute in SMEs across Europe, South America and Africa | Short term (≤ 2 years) |

| Vendor Accountability and Single Point of Support Concerns | -1.90% | Global enterprises, especially regulated verticals | Medium term (2-4 years) |

| Interoperability Challenges with Legacy Network Management Systems | -1.40% | North America and Europe installed bases | Medium term (2-4 years) |

| Supply Chain Volatility for Merchant Silicon Chipsets | -1.10% | Global, heightened risk in Taiwan and South Korea fabs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited In-House Integration Expertise Among Enterprises

Outside hyperscale environments, many organizations lack Linux networking expertise, constraining adoption of disaggregated switches. Industry data shows about 68% of European enterprises cite skills gaps as the primary barrier. Capability ramp up typically takes 12 to 18 months as teams learn platforms such as SONiC and DENT, delaying ROI and increasing execution risk. Smaller cloud providers in South America and Africa often pay 25% to 40% premiums to system integrators, reducing cost advantages. Financial services firms remain cautious due to strict change control processes tied to vendor supported systems. Until training pipelines scale, integration capability will limit near term penetration in the bare metal switch market.

Vendor Accountability and Single Point of Support Concerns

Risk-averse enterprises prefer single vendor accountability when networks fail. A 2025 industry study found that about 54% of Global 2000 companies prioritize SLA strength over total cost of ownership when selecting or switching infrastructure. To address this, ODMs are bundling bare-metal switches with 24/7 support, but these offerings erode the original cost advantage by 30% to 50%. Vendors are also introducing managed services and extending warranties to the network operating system layer. While these measures reduce operational risk and address accountability concerns, they compress pricing benefits and may slow adoption in compliance-intensive segments of the bare-metal switch market.[4]Broadcom Inc., “Tomahawk 5 Silicon Platform,” broadcom.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Switch Type: Branded Variants Move Beyond Niche

Branded bare-metal switches are projected to grow at a 18.53% CAGR from 2026 to 2031, outpacing the overall market as ODMs layer commercial support on commodity hardware. Open Ethernet switches held about 46.36% of the market share in 2025, driven by hyperscalers that self-manage their network operating systems. ODM performance indicates strong enterprise traction, with branded switch revenue rising sharply as buyers pay premiums for single vendor accountability. Enterprise-grade open NOS distributions are replicating proprietary SLAs while retaining cost advantages, enabling penetration into regulated sectors such as finance and healthcare.

The open variant will remain dominant in cloud and telecom environments where engineering depth offsets integration risk, while government and public sector demand increasingly favors branded offerings due to governance and compliance needs. As a result, branded segment revenue is expected to expand from about USD 1.9 billion in 2026 to USD 4.4 billion by 2031, increasing its share of total market value. ODMs combining silicon alignment with full stack support are positioned to capture incremental demand, while pure play manufacturers face margin pressure.

By Port Speed: 400 G bps and 800 G bps Platforms Gain Momentum

The 200+ Gbps segment is expected to expand at a 25.26% CAGR, driven by AI workloads that require higher east-west bandwidth. While the 25/40 Gbps segment accounted for about 38.49% of the market size in 2025, hyperscalers are rapidly scaling 400 Gbps fabrics across multiple data center regions, reducing oversubscription ratios to around 1.5 to 1. Merchant silicon advancements are enabling this transition, with new architectures supporting high-density 800 Gbps deployments at scale.

Declining optics costs and improved port density are expected to make 100 Gbps the default enterprise top-of-rack standard by 2028, shifting 1/10 Gbps to edge and legacy environments. Next-generation silicon offering up to 25.6 Tbps of throughput is intensifying competition in the merchant ecosystem. As a result, the port-speed mix is shifting toward higher-bandwidth tiers, supporting stronger growth in the bare-metal switch market.

By Deployment Mode: Edge Footprints Scale Quickly

Cloud service providers accounted for about 41.63% of deployment revenue in 2025, while edge computing sites are expected to register the fastest growth at 20.32% CAGR during 2026 to 2031. Use cases such as content delivery, industrial IoT, and autonomous systems require sub-10 ms latency, driving demand for localized, energy-efficient 1U switch deployments. Operators are expanding SONiC-based platforms across distributed micro data centers to enable tenant-specific quality of service without vendor lock-in.

Enterprise on-premises refresh cycles are also accelerating as legacy chassis systems approach replacement, with buyers reporting 35% to 45% capex savings compared to proprietary alternatives. The market is therefore expanding on two fronts, hyperscale driven core deployments and distributed edge infrastructure, where efficiency, space optimization, and sustainability influence procurement decisions.

By End User Industry: Public-Sector Mandates Accelerate

Cloud providers accounted for about 44.64% of the bare-metal switch market revenue in 2025, supported by continuous capacity expansion, while government and public sector spending is projected to grow at a 19.22% CAGR. National programs are increasingly specifying open Ethernet fabrics for large-scale AI and digital infrastructure deployments, with Japan allocating JPY 2.1 trillion (USD 14.3 billion) toward open hardware modernization, thereby strengthening demand from public-sector initiatives.

Telecom operators remain the second-largest end-user segment, leveraging bare-metal switches to reduce 5G transport costs. Enterprise adoption continues to lag due to skills gaps and SLA concerns. However, early deployments in latency-sensitive sectors such as high-frequency trading and OTT media are validating performance reliability, indicating gradual adoption across broader enterprise workloads over the forecast period.

Geography Analysis

North America accounts for the largest share of the bare-metal switch market, driven by hyperscaler dominance in the United States and 5G standalone upgrades among Canadian telecom operators. Large-scale network modernization programs are increasingly aligned with sustainability targets, with operators transitioning to 400 Gbps SONiC-based fabrics to reduce power consumption and the carbon footprint. These developments indicate that procurement decisions are no longer driven solely by performance and cost, but also by energy efficiency metrics. The region benefits from mature cloud ecosystems, strong ODM partnerships, and faster refresh cycles, reinforcing its leadership position.

Asia Pacific accounted for about 32.97% of 2025 revenue, supported by aggressive data center expansion across China, India, and Southeast Asia. Government-backed semiconductor and digital infrastructure programs are accelerating the adoption of open networking hardware, with significant investments in domestic manufacturing and networking capabilities. India and China are positioning themselves as key assembly and demand hubs, while Southeast Asian economies are expanding digital government and cloud infrastructure. This combination of policy support, capacity expansion, and cost sensitivity is strengthening the region’s role as a major growth engine for bare metal switch deployments.

The Middle East is projected to grow at 17.12% CAGR through 2031, driven by sovereign cloud initiatives and smart city investments in Saudi Arabia and the United Arab Emirates. Europe shows moderate growth, driven by fragmented procurement structures, although regulatory pressure on energy efficiency is supporting the gradual adoption of open hardware. South America and Africa remain early-stage markets, characterized by budget constraints and reliance on cost-efficient infrastructure. In these regions, bare-metal switches offer a viable alternative to expensive, proprietary systems, enabling gradual adoption as digital infrastructure investments expand.

Competitive Landscape

The bare-metal switch market exhibits moderate fragmentation, with original design manufacturers controlling hardware production, while hyperscale operators and network operating system developers exert influence over software roadmaps and reference architectures. Edgecore Networks, Accton Technology, and Delta Electronics collectively command an estimated 40% to 45% of global ODM shipments, leveraging established relationships with Broadcom and Marvell to secure early access to next-generation merchant silicon platforms. Competitive dynamics are bifurcating into two distinct arenas: a high-volume, low-margin ODM segment where manufacturers compete on manufacturing efficiency and time-to-market, and an emerging branded segment where vendors differentiate through integrated support services and pre-validated network operating system distributions. White-space opportunities are emerging in edge computing, government procurement, and telecommunications Open RAN deployments, where incumbents lack purpose-built offerings and buyers prioritize latency, energy efficiency, or regulatory compliance over raw port density.

Strategic moves emphasize vertical integration and ecosystem partnerships, with ODMs acquiring software capabilities to capture higher-margin services revenue, while hyperscalers contribute open-source network operating systems to commoditize hardware and preserve multi-vendor optionality. Broadcom's patent portfolio, which includes more than 1,200 active filings related to merchant silicon switching ASICs as of December 2025, creates a structural advantage that enables the company to influence ODM roadmaps and maintain 60% to 70% share of the high-speed switching chipset market. Marvell Technology is challenging this dominance through aggressive pricing and co-development agreements with cloud providers, exemplified by its January 2026 announcement of a custom Teralynx variant optimized for Meta Platforms' AI training clusters. Smaller entrants such as NoviFlow and Netberg are targeting niche verticals with specialized offerings, including programmable switches for network function virtualization and ruggedized platforms for industrial edge deployments, though their combined market share remains below 5%. The competitive landscape will likely consolidate as branded bare metal switches gain traction, rewarding ODMs that successfully transition from contract manufacturing to value-added solution providers while penalizing pure-play hardware vendors unable to differentiate beyond cost.

Bare Metal Switch Industry Leaders

Edgecore Networks Corporation

Accton Technology Corporation

Quanta Cloud Technology Inc.

Delta Electronics, Inc.

Celestica Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Edgecore Networks unveiled an 800 Gbps spine switch line based on Broadcom Tomahawk 5, with Q3 2026 shipments to North American and Asia-Pacific hyperscalers

- March 2026: Delta Electronics partnered with Marvell to co-develop 1.6 Tbps edge platforms targeting sub-50 watt per-port power budgets.

- February 2026: Accton signed a USD 420 million multi-year agreement to supply 400 Gbps switches across 25 regions for a top-three cloud provider.

- January 2026: UfiSpace closed a USD 75 million Series C round led by SoftBank Vision Fund to expand Open RAN fronthaul capacity.

Global Bare Metal Switch Market Report Scope

The bare-metal switch market comprises Ethernet switching hardware sold without a preinstalled proprietary network operating system, allowing users to deploy open or third-party NOS platforms. These switches are primarily adopted by hyperscalers, telecom operators, and large enterprises to achieve cost efficiency, programmability, and vendor flexibility in data center and network infrastructure environments.

The Bare Metal Switch Market Report is Segmented by Switch Type (Open Ethernet Switches, Branded Bare Metal Switches), Port Speed (1/10 Gbps, 25/40 Gbps, 100 Gbps, and 200+ Gbps), Deployment Mode (On-premise Data Centers, Cloud Service Providers, Telecom Central Offices, and Edge Computing Sites), End User Industry (Cloud Providers, Telecommunications, Enterprises, Government and Public Sector, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Open Ethernet Switches |

| Branded Bare Metal Switches |

| 1/10 Gbps |

| 25/40 Gbps |

| 100 Gbps |

| 200+ Gbps |

| On-premise Data Centers |

| Cloud Service Providers |

| Telecom Central Offices |

| Edge Computing Sites |

| Cloud Providers (Hyperscale) |

| Telecommunications |

| Enterprises |

| Government and Public Sector |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Switch Type | Open Ethernet Switches | |

| Branded Bare Metal Switches | ||

| By Port Speed | 1/10 Gbps | |

| 25/40 Gbps | ||

| 100 Gbps | ||

| 200+ Gbps | ||

| By Deployment Mode | On-premise Data Centers | |

| Cloud Service Providers | ||

| Telecom Central Offices | ||

| Edge Computing Sites | ||

| By End User Industry | Cloud Providers (Hyperscale) | |

| Telecommunications | ||

| Enterprises | ||

| Government and Public Sector | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the global bare metal switch space by 2031?

The segment is forecast to reach USD 10.6 billion by 2031, advancing at a 14.87% CAGR from 2026 to 2031 according to Mordor Intelligence.

Which region is expected to record the quickest expansion over 2026-2031?

The Middle East is projected to post the fastest 17.12% CAGR through 2031, driven by sovereign data-center investments in Saudi Arabia and the United Arab Emirates, as tracked by Mordor Intelligence.

Which switch type currently commands the largest revenue share?

Open Ethernet models led with 46.36% share in 2025 because hyperscale operators self-manage the software stack, per Mordor Intelligence.

Where are the main obstacles to wider enterprise adoption?

Limited in-house Linux networking expertise and concerns about multi-vendor support remain the two biggest hurdles, especially among regulated verticals.

How are hyperscale cloud providers influencing product road maps?

Operators including Microsoft, Meta and Google co-design reference hardware and contribute to open NOS projects, accelerating silicon upgrades to 400 Gbps and 800 Gbps.

What port-speed range is expected to show the fastest growth?

The 200 Gbps-plus tier is set to expand at a 25.26% CAGR as AI training clusters push demand for 400 Gbps and 800 Gbps fabrics, based on Mordor Intelligence findings.

Page last updated on: